Updated 2/23/26

Otis Worldwide Corporation (NYSE: OTIS) has been a powerhouse in the elevator and escalator industry for well over a century. From towering skyscrapers to busy commercial centers, Otis elevators keep the world moving. The company’s strong global presence, reliable service contracts, and consistent cash flows make it an interesting choice for dividend investors looking for stability.

While Otis isn’t a flashy, high-yield stock, it does offer steady dividend payments backed by solid earnings. The company’s business model, which includes a significant portion of recurring revenue from maintenance services, provides a level of predictability that dividend-focused investors tend to appreciate.

Key Dividend Metrics

📈 Forward Dividend Yield: 1.78%

💰 Annual Dividend Payout: $1.68 per share

🔄 Recent Dividend Growth: Increased from $1.56 to $1.68

🛡 Payout Ratio: 47.14% (Sustainable)

📅 Ex-Dividend Date: February 13, 2026

📊 Latest Dividend Payment: $0.42 per share

🏛 Market Cap: $35.3 billion

Dividend Overview

Otis isn’t the type of stock that grabs headlines for its dividend yield, but it is one that pays consistently and grows its payout steadily over time. The dividend yield currently sits at 1.78%, which is a meaningful step up from where it stood a year ago, and it remains well-supported by underlying earnings and cash flow.

The payout ratio of 47.14% is comfortably within sustainable territory, meaning Otis continues to retain a solid share of its earnings for reinvestment while still returning capital to shareholders. Over the past year, the company raised its quarterly dividend from $0.39 to $0.42 per share, lifting the annualized payout from $1.56 to $1.68. That increase represents roughly a 7.7% bump, a notably stronger rate of growth than the company delivered in the prior year’s cycle.

What makes Otis particularly appealing is its steady revenue from service contracts. While new elevator installations fluctuate with economic cycles, maintenance and repair services provide a dependable stream of income. That kind of reliability is valuable for dividend investors looking for long-term income security, and it gives the company the confidence to keep growing its payout even when the new equipment business faces headwinds.

Dividend Growth and Safety

For investors prioritizing safety and reliability over raw yield, Otis continues to make a compelling case. The company’s ability to consistently generate cash flow allows it to keep dividends flowing without stretching its financials, and the most recent dividend increase signals that management remains committed to rewarding shareholders.

The progression of quarterly payments tells the story clearly. Otis held its quarterly dividend at $0.34 through early 2024, then raised it to $0.39 in May 2024, and raised it again to $0.42 in May 2025, where it has remained through the most recent February 2026 payment. Two consecutive annual increases demonstrate a disciplined but accelerating approach to payout growth.

Looking at cash flow, Otis generated $1.596 billion in operating cash flow over the last reported year, with free cash flow coming in nearly as strong at approximately $1.594 billion. Against an annual dividend obligation that is well within reach given the company’s earnings base and 47.14% payout ratio, those figures reinforce that the dividend is on firm footing. Debt levels remain elevated in an absolute sense, as is common for industrial companies of this scale, but cash generation more than covers dividend commitments with room to spare.

Cash Flow Statement

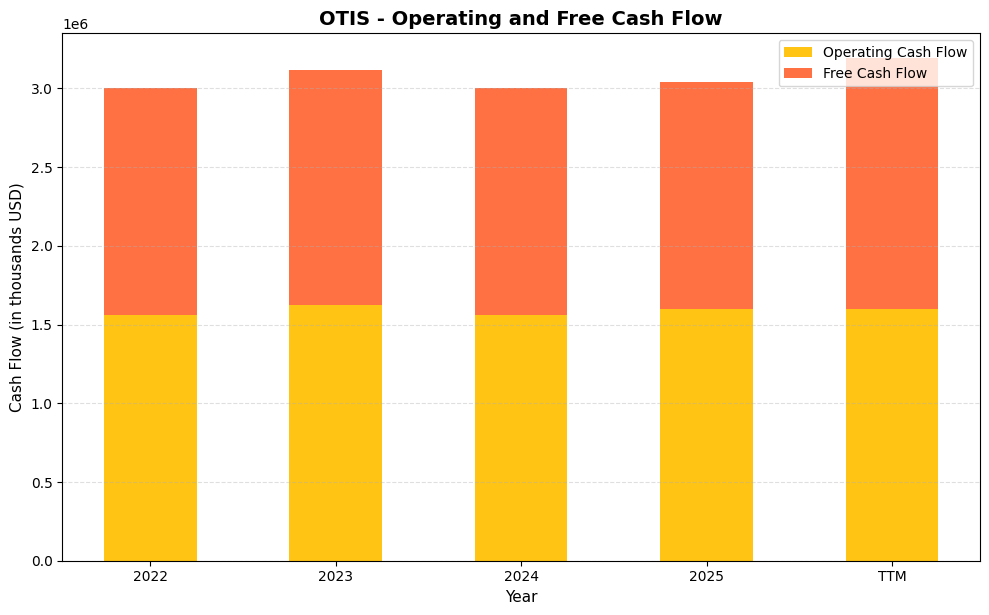

Otis Worldwide has demonstrated a remarkably consistent cash generation profile over the past several years, which is precisely the kind of foundation dividend growth investors want to see. Operating cash flow has held in a tight band, running from $1.56 billion in 2022 to $1.63 billion in 2023, then settling back to $1.56 billion in 2024 and recovering modestly to $1.60 billion in 2025. Free cash flow has tracked closely alongside, ranging from $1.44 billion to $1.49 billion across those same years, reflecting a capital-light business model that requires relatively modest reinvestment to sustain its earnings power. The TTM free cash flow figure of approximately $1.59 billion is particularly encouraging, as it suggests capital expenditures have compressed recently, leaving more cash available for dividends, buybacks, and debt management. With the company paying out roughly $600 million annually in dividends, free cash flow covers that obligation more than twice over, which provides a substantial margin of safety for income investors.

What stands out across this four-year window is not dramatic growth but rather the durability and predictability of cash generation, which is arguably more valuable for a dividend investor than a lumpy, high-variance cash flow profile. Otis operates a service-heavy business where its large global elevator maintenance and modernization contracts generate recurring revenue that translates reliably into operating cash. The conversion of operating cash to free cash flow has consistently run above 90 percent, which signals disciplined capital allocation and a business that does not need to spend heavily on physical infrastructure to stay competitive. The slight uptick in TTM free cash flow, driven by a narrower gap between operating and free cash figures, reinforces the capital efficiency story. For shareholders, this means the dividend is well-funded from actual cash rather than accounting earnings, the payout has room to grow without straining the balance sheet, and management retains flexibility to continue its share repurchase program alongside the dividend commitment.

Chart Analysis

Otis Worldwide has had a choppy twelve months, carving out a wide range between its 52-week low of $83.75 and its 52-week high of $102.40, a spread of roughly 22 points that reflects genuine uncertainty about the stock’s direction rather than calm, steady accumulation. The shares are currently sitting at $90.55, which puts them about 11.6% below that peak and only 8.1% above the trough. That positioning in the lower half of the annual range is not alarming for a slow-growth, high-quality compounder, but it does tell investors that the momentum that carried Otis into triple digits earlier in the year has faded and the stock is still working through that digestion process.

The moving average picture sends a mixed signal. On the encouraging side, Otis is trading above both its 50-day moving average of $88.87 and its 200-day moving average of $90.39, which means the price action is at least constructive in the near term. The concern is that the 50-day average remains below the 200-day, a configuration technically known as a death cross, which signals that the intermediate trend has been deteriorating even as the price itself has bounced. The gap between the two averages is narrow, around $1.50, so a sustained push higher from current levels would bring the 50-day back above the 200-day relatively quickly. Until that crossover occurs, the technical backdrop carries a mild bearish undercurrent that income investors should keep in mind when sizing a position.

The RSI reading of 63.38 adds a genuinely positive layer to the near-term picture. That level is firm without being stretched into overbought territory, which typically begins above 70. Momentum is building off the lows in a measured way, suggesting that buyers are stepping in with some conviction but that the stock has not yet run so far so fast that it becomes vulnerable to a sharp pullback. For dividend investors who are patient by nature, this kind of steady RSI climb is preferable to a spike, since it tends to produce more durable price support beneath the position.

Taken together, the chart tells a story of a quality franchise that sold off meaningfully from its highs and is now in early recovery mode. The price is above both moving averages, momentum is constructive, and the valuation is well off peak levels, all of which creates a reasonable setup for long-term income buyers. The unresolved death cross is the one technical blemish worth watching, and investors who prefer to wait for a confirmed golden cross before adding exposure would have a defensible reason to do so. For those already holding Otis for its dividend, the current technical picture does not flash any warning signs serious enough to reconsider the thesis.

Analyst Ratings

Recent Upgrades

📈 Among the 14 analysts currently covering Otis, the mean price target stands at $102.50, implying meaningful upside from the current price of $90.55. The high end of the range reaches $120.00, reflecting that some analysts see considerable recovery potential as the stock trades near the lower end of its 52-week range.

📈 The low analyst price target of $90.00 sits essentially at the current market price, suggesting that even the most cautious analysts covering the stock see limited additional downside from current levels, which itself is a modest form of reassurance for income-oriented holders.

Recent Downgrades

📉 With no formal consensus rating available across the analyst group and the stock trading near the bottom of its 52-week range of $84.00 to $106.83, sentiment has clearly cooled from earlier in the year. Concerns about China construction exposure, slower new equipment demand, and broader industrial cycle uncertainty have weighed on the stock’s multiple, compressing the P/E from prior-year levels despite solid underlying earnings per share of $3.50.

📉 The stock’s beta of 1.01 suggests it is moving broadly in line with the market, meaning the recent price softness reflects both company-specific concerns and broader macro caution rather than any idiosyncratic collapse in fundamentals.

Consensus Price Target

Across 14 analysts, the mean price target of $102.50 represents approximately 13.2% upside from the current price of $90.55. The range from $90.00 to $120.00 is wide, reflecting genuine disagreement about how quickly the new equipment business can recover and how the China construction market evolves through the remainder of 2026. For dividend investors who are less focused on near-term price targets, the more relevant takeaway is that the stock is trading well below its recent highs while the dividend continues to grow, which improves the forward yield and the long-term entry point for income seekers.

These mixed analyst opinions highlight the importance of considering both potential opportunities and risks associated with Otis Worldwide. While some analysts are encouraged by the company’s stable earnings and strategic positioning in the service segment, others express caution due to external economic factors and construction market dynamics. Investors should weigh these insights carefully when evaluating the stock.

Earnings Report Summary

Otis Worldwide’s most recently reported financials show a business that continues to generate reliable earnings and cash flow, even as the new equipment segment navigates a challenging environment. Full-year revenue came in at $14.43 billion, a modest increase from the prior year’s $14.3 billion, and net income reached $1.384 billion, producing earnings per share of $3.50.

Service Segment Strength

The service segment remains the core driver of Otis’s financial stability. Maintenance and modernization demand continued to support revenue growth, with the service portfolio providing a recurring income base that cushions the impact of new equipment volatility. The company’s global maintenance portfolio, which spans nearly 2.4 million units, gives Otis an enviable annuity-like revenue stream that competitors find difficult to replicate at scale.

Operating cash flow of $1.596 billion and free cash flow of $1.594 billion demonstrate that the service business generates cash efficiently and with minimal capital intensity. Those figures gave management the confidence to raise the quarterly dividend from $0.39 to $0.42 per share in 2025, and they support continued payout growth going forward.

New Equipment Challenges

The new equipment segment continues to face headwinds, particularly from a sluggish construction environment in China. Softer demand in that market has pressured new installation volumes and weighed on overall revenue growth, keeping the top line expansion modest rather than robust. The Americas, EMEA, and other Asia Pacific markets have provided some offset, but China remains the most significant swing factor for this segment.

Despite these pressures, Otis has managed to protect its profitability through pricing discipline and cost efficiencies, keeping the profit margin at 9.59% and return on assets at 13.52%. The company’s ability to maintain earnings quality while absorbing new equipment weakness speaks to the structural resilience of the overall business model.

Looking Ahead to 2026

Management has expressed continued confidence in the service segment’s ability to drive organic growth through 2026, with modernization demand and maintenance contract wins expected to keep that revenue stream expanding. New equipment recovery in China remains the key variable, and any stabilization there would be a meaningful positive catalyst for the overall earnings trajectory. With free cash flow running near $1.6 billion, Otis has ample capacity to continue dividend growth, pursue selective acquisitions, and return capital through share repurchases.

Financial Health and Stability

Otis operates in a capital-intensive industry, which means debt management is a crucial factor. The company carries a significant total debt load, which is a well-established characteristic of its balance sheet given the aggressive share repurchase program it has executed over the years. That program is also responsible for the negative book value per share of $13.83, a figure that reflects capital returns to shareholders rather than underlying financial weakness.

From a profitability standpoint, Otis maintains solid margins. With a profit margin of 9.59% and return on assets of 13.52%, the company is efficiently converting revenue into earnings and deploying its asset base productively. Operating cash flow of $1.596 billion and near-identical free cash flow confirm that reported earnings are backed by real cash generation, which is the ultimate test of dividend sustainability.

A key factor in Otis’s financial health is its recurring revenue from maintenance contracts. Unlike companies that rely solely on new product sales, Otis has a built-in buffer that helps cushion the impact of economic downturns. This recurring income stream makes Otis more predictable compared to other industrial stocks that face more cyclical demand swings, and it is the primary reason the dividend has continued to grow even as the new equipment business has encountered turbulence.

Valuation and Stock Performance

At a current share price of $90.55, Otis trades at a price-to-earnings ratio of 25.87. The stock is sitting near the lower end of its 52-week range of $84.00 to $106.83, having pulled back meaningfully from its highs earlier in the period. That pullback has pushed the forward dividend yield up to 1.78%, making the current entry point more attractive for income investors than it was when the stock was trading in the $100 to $106 range.

The market cap of approximately $35.3 billion reflects the scale and quality of the business, and the P/E of 25.87 is consistent with what investors typically pay for a high-quality industrial franchise with defensive characteristics. While the multiple isn’t cheap in an absolute sense, it is reasonable relative to the predictability of Otis’s earnings and the strength of its service segment cash flows. The negative price-to-book ratio of -6.55 is a byproduct of the company’s buyback history rather than a red flag, and investors should focus on earnings and cash flow based metrics when assessing valuation.

With the mean analyst price target at $102.50, the stock would need to appreciate roughly 13% from current levels to reach consensus, a return that combined with the 1.78% dividend yield represents a reasonable total return scenario for patient income investors. The stock’s beta of 1.01 suggests volatility broadly in line with the market, meaning significant additional drawdowns would likely require a broader market event rather than a company-specific catalyst.

Risks and Considerations

Debt Levels — Otis carries a substantial total debt load that requires careful balance sheet management. While operating cash flow comfortably covers interest obligations, any sustained rise in borrowing costs or deterioration in cash flow could constrain financial flexibility.

China Exposure — The new equipment segment’s performance is meaningfully tied to construction activity in China. A prolonged downturn in that market would continue to pressure new installation volumes and could limit overall revenue growth despite service segment strength.

Modest Revenue Growth — With revenue growing at a low single-digit pace, Otis is not a high-growth story. Investors seeking aggressive capital appreciation may find the company’s steady, incremental trajectory unsatisfying relative to higher-growth industrial peers.

Cyclical New Equipment Demand — While maintenance services provide a defensive buffer, new elevator sales remain tied to commercial and residential construction cycles. A broader real estate slowdown in key markets could dampen this segment further and offset service segment gains.

Global Uncertainty — As a global company operating across dozens of markets, Otis is exposed to currency fluctuations, regulatory changes, and geopolitical risks that could affect reported earnings even when underlying business performance is solid.

Final Thoughts

Otis Worldwide isn’t the kind of stock that will deliver rapid capital appreciation, but for long-term investors looking for a steady and growing dividend payer, it offers genuine appeal. The 1.78% yield is now more attractive than it has been in some time, given the stock’s retreat from its 52-week highs, and it is backed by a 47.14% payout ratio and nearly $1.6 billion in annual free cash flow.

The company’s most recent dividend increase, lifting the quarterly payment from $0.39 to $0.42, demonstrated management’s continued commitment to growing the payout. Two consecutive annual raises, with the annualized dividend moving from $1.56 to $1.68, show that Otis is not merely maintaining its dividend but actively building it at a pace that outstrips inflation.

The dominant market position in the global elevator and escalator industry, combined with a maintenance portfolio approaching 2.4 million units, gives Otis a recurring revenue foundation that most industrial companies cannot match. The new equipment segment faces real headwinds, particularly in China, but the service business provides enough stability and growth to keep the overall earnings and cash flow picture intact. For income investors willing to accept modest yield in exchange for consistency and safety, Otis Worldwide remains a solid holding in a diversified dividend portfolio.