Updated 2/23/26

ONE Gas, Inc. (NYSE: OGS) is a regulated natural gas utility serving over 2.2 million customers across Oklahoma, Kansas, and Texas. Spun off from ONEOK in 2014, it has established itself as a reliable player in the utility space, benefiting from predictable revenues and steady demand.

For dividend investors, OGS presents an interesting opportunity. The company offers a stable payout, a respectable yield, and a history of consistent increases. As with any stock, there are factors to weigh, such as debt levels, cash flow, and regulatory risks. Let’s take a closer look at how ONE Gas stacks up for income-focused investors.

🔑 Key Dividend Metrics

💰 Forward Dividend Yield: 3.13%

📈 5-Year Average Yield: 3.29%

📅 Last Dividend Payment: February 20, 2026

🚨 Payout Ratio: 62.24%

💵 Dividend Growth Streak: 10+ years

📊 Last Dividend Increase: 1.5%

📊 Dividend Growth (5-year CAGR): ~3%

Dividend Overview

ONE Gas continues to deliver as a reliable dividend payer, currently offering a yield of 3.13%, which sits modestly below its five-year average of 3.29%. That compression reflects a meaningful appreciation in share price over the past year rather than any reduction in the payout itself, which is a sign investors have grown more comfortable with the company’s stability. Compared to other regulated gas utilities, the yield remains competitive without stretching into territory that might signal financial stress.

The latest quarterly dividend stands at $0.68 per share, reflecting the most recent increase that took effect with the February 20, 2026 payment. The annualized dividend now sits at $2.72, continuing the company’s unbroken streak of annual payout increases. The pace of growth remains measured, consistent with management’s stated goal of prioritizing financial flexibility alongside shareholder returns.

Utilities like OGS are known for their steady dividends, as their business model is relatively insulated from economic swings. That reliability is a key attraction for long-term dividend investors, and ONE Gas has done nothing to disturb that reputation over the past year.

Dividend Growth and Safety

Dividend safety is a crucial factor when evaluating an income stock. At a 62.24% payout ratio, OGS is distributing a meaningful portion of its earnings to shareholders while retaining enough to fund ongoing operations and capital projects. Importantly, this payout ratio has improved from the 67.52% reported a year ago, reflecting stronger earnings per share of $4.29 against a dividend that has grown only modestly. For a regulated utility, a payout ratio in this range is well within the comfort zone and signals that the dividend is on solid footing.

The five-year dividend growth CAGR has settled around 3%, which is a more modest figure than the 6% pace seen in earlier years. Looking at the recent dividend history, increases have been incremental: from $0.65 per quarter in mid-2023, to $0.66 in early 2024, to $0.67 in early 2025, and now $0.68 beginning February 2026. Each step reflects a roughly 1.5% annual increase, consistent with management’s guidance to grow the dividend at 1% to 2% annually through 2029. Income investors should calibrate expectations accordingly, as this is a slow-and-steady income story rather than a dividend acceleration play.

Free cash flow remains negative at approximately negative $209 million, as capital expenditure requirements continue to outpace operating cash generation. Operating cash flow of $579 million is healthy and more than covers the dividend obligation, but the company continues to rely on external financing to fund its infrastructure program. This is a structural reality for capital-intensive regulated utilities, and it is something investors should monitor over the coming years as interest costs and project timelines evolve.

Chart Analysis

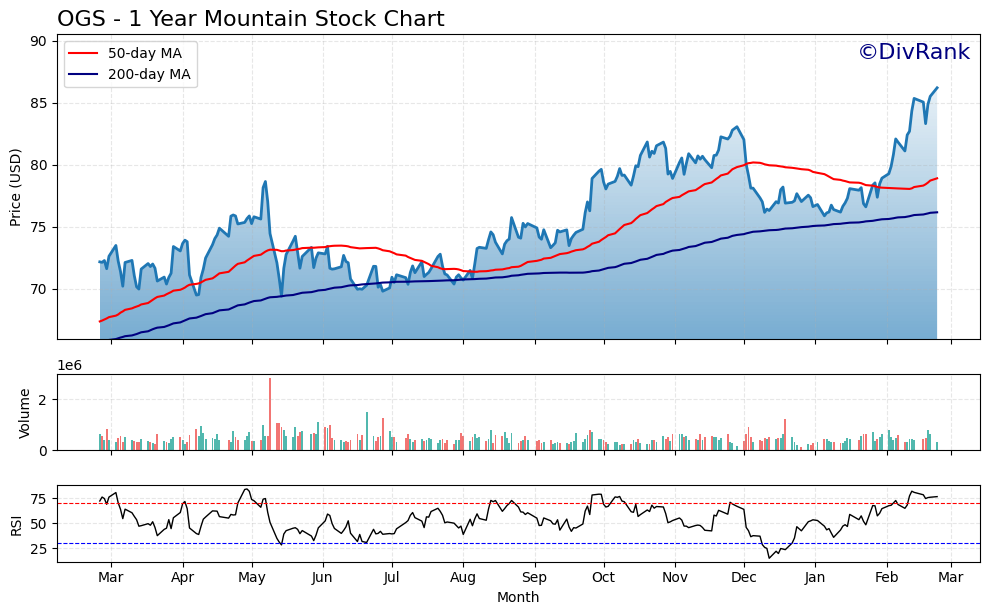

ONE Gas has put together a compelling year of price recovery, climbing from a 52-week low of $69.42 to its current level of $86.21, which also happens to be the 52-week high. That 24.19% move off the trough reflects a decisive shift in sentiment toward regulated utility names, and the fact that OGS is sitting right at the top of its annual range signals that buyers have remained in control throughout the entire advance. There has been no meaningful pullback to speak of in recent months, and the price action has taken on an almost staircase-like quality, with higher lows consistently supporting the uptrend.

The moving average picture reinforces the bullish character of this chart. OGS is trading well above both its 50-day moving average of $78.92 and its 200-day moving average of $76.18, with the shorter-term average sitting above the longer-term one. That configuration is commonly referred to as a golden cross, and it tends to confirm that the intermediate trend is aligned with the longer-term trend. The spread between current price and the 200-day average is now roughly 13%, which tells you the stock has traveled a considerable distance from its base. That kind of separation from a long-term average can sometimes invite consolidation, so dividend investors should keep that in mind when thinking about entry timing.

Momentum, as measured by the 14-period RSI, is running at 76.77, which places OGS squarely in overbought territory. A reading above 70 does not by itself signal a reversal, particularly in a trending utility name with consistent income support, but it does suggest that short-term enthusiasm has outpaced the pace of the underlying price climb. Historically, RSI readings at this level in a regulated utility have often preceded sideways consolidation rather than sharp declines, since the dividend yield itself tends to attract buyers on any weakness and prevents prices from unwinding aggressively.

For dividend investors, the overall takeaway here is straightforward. The trend is unambiguously positive, the moving average structure is supportive, and the company’s regulated earnings profile gives the chart’s strength a fundamental anchor. The primary caution is that buying at a 52-week high with an RSI above 76 means there is limited technical cushion in the near term. Investors who prioritize income and have a multi-year holding horizon can view any modest pullback toward the $78 to $80 range, near the rising 50-day average, as a more favorable entry point that would also lock in a modestly higher starting yield.

Analyst Ratings

The analyst community currently holds a consensus buy rating on ONE Gas, with seven analysts covering the stock. The mean 12-month price target sits at $86.86, essentially in line with the current share price of $86.21, suggesting analysts see the stock as fairly valued at these levels with limited near-term upside on a price basis. The high target of $92.00 implies about 6.7% of potential appreciation from current levels, while the low target of $78.00 represents meaningful downside risk if sentiment shifts or earnings disappoint.

The fact that the consensus has moved to a buy rating is a constructive development relative to the more cautious neutral posture observed a year ago. The stock’s run from the mid-$70s to the upper $80s has absorbed much of the valuation upside that analysts had previously identified, which explains why the mean target and current price are now so closely aligned. For dividend-focused investors, the buy consensus reinforces confidence in the company’s fundamentals, even if the near-term price target leaves little room for capital gains.

With seven analysts covering OGS, the coverage universe is relatively small for a company of this size, which can occasionally lead to larger swings in consensus when individual firms update their ratings. Investors should watch for any changes in the interest rate outlook or regulatory decisions in Oklahoma, Kansas, or Texas that might prompt analysts to revise their targets in either direction.

Earnings Report Summary

ONE Gas posted full-year earnings per share of $4.29, landing within the guidance range of $4.20 to $4.32 that management had established at the start of 2025. Total revenue reached approximately $2.43 billion for the year, supported by rate adjustments and continued customer additions across its three-state service territory. Net income came in at $264 million, reflecting the company’s ability to translate regulated rate structures into steady bottom-line results despite elevated operating and depreciation costs.

Return on equity of 8.07% and return on assets of 3.32% are consistent with what investors would expect from a regulated gas distribution company operating within commission-set rate structures. Profit margin of 10.88% reflects the capital-heavy nature of the business and the cost of ongoing infrastructure investment. Operating cash flow of $579 million provides meaningful coverage of the dividend obligation, which totals roughly $160 million annually at the current payout level.

Management’s capital expenditure program continued at a significant pace in 2025, with investments focused on system integrity, pipeline replacement, and new customer connections particularly in Texas and Oklahoma. The average rate base continued to grow, which sets the foundation for future rate case filings and earnings support. Looking into 2026, investors should watch for regulatory updates from state commissions that could influence the pace and magnitude of rate recovery on recent capital investments.

For dividend investors, the key takeaway from the earnings picture is that the payout is well-covered by operating earnings and that the company is executing within its financial plan. The improvement in payout ratio from 67.52% a year ago to 62.24% today reflects genuine earnings progress, which is encouraging even if the absolute growth rate remains modest.

Valuation and Stock Performance

At its current price of $86.21, ONE Gas trades at a trailing price-to-earnings ratio of 20.10 and a price-to-book ratio of 1.57 against a book value per share of $54.87. The P/E of 20.10 represents a modest premium to where the stock traded a year ago, consistent with the broader re-rating that regulated utilities have experienced as investors have sought income stability. For context, a P/E in the low-to-mid 20s is not unusual for high-quality regulated gas distributors, though it does leave less margin of safety than was available when the stock traded in the mid-$70s.

The 52-week range of $69.75 to $86.79 tells an important story. The stock is currently trading very near its 52-week high, having gained substantial ground from the lows seen earlier in the year. That move reflects both improved investor sentiment toward regulated utilities and confidence in OGS’s earnings trajectory. Market capitalization has grown to approximately $5.17 billion, reflecting the stock’s appreciation over the past twelve months.

With a beta of 0.81, OGS continues to exhibit below-market volatility, which is exactly what income investors seek from a utility holding. At current levels, the stock is not a bargain in a traditional value sense, but it is reasonably priced for a regulated utility with a dependable dividend and improving payout metrics. Investors initiating a position today should be realistic that total return will be driven primarily by the dividend rather than multiple expansion from here.

Risks and Considerations

Interest rate sensitivity remains one of the most meaningful risks for ONE Gas. As a capital-intensive regulated utility that relies on external financing to fund its infrastructure program, higher borrowing costs directly affect the company’s cost of capital and can compress the spread between its regulated return on equity and its actual financing expenses. Any unexpected shift toward a higher-rate environment could pressure margins and limit the pace of future dividend increases.

The company’s persistently negative free cash flow, currently running at approximately negative $209 million, means it continues to depend on debt markets and equity financing to bridge the gap between operating cash generation and capital expenditure needs. While this is a structural feature of large regulated utilities rather than a sign of financial distress, it does mean that dividend growth is constrained by what can be funded sustainably through the rate base and financing activities rather than by organic cash generation alone.

Regulatory risk is an ever-present consideration for a company whose revenues are set by state commissions in Oklahoma, Kansas, and Texas. Unfavorable rate case outcomes, delays in approval for capital recovery mechanisms, or shifts in commission composition could slow the translation of infrastructure investment into earned revenue. Any of these scenarios would put pressure on earnings growth and, by extension, the pace of dividend increases.

The current valuation, with the stock near its 52-week high and the mean analyst price target barely above the current price, limits the near-term margin of safety for new investors. A position initiated at $86 carries more valuation risk than one taken in the mid-$70s a year ago, and income investors should be prepared for the possibility of price consolidation or modest pullbacks even if the underlying business continues to perform in line with expectations.

Final Thoughts

ONE Gas is a solid choice for investors seeking a stable dividend from the utility sector. It offers a respectable 3.13% yield, a history of reliable annual payout increases now extending over a decade, and a regulated business model that provides predictable earnings. The improvement in payout ratio to 62.24% is a genuine positive, reflecting stronger earnings per share rather than a cut in the dividend, and the most recent quarterly increase to $0.68 per share keeps the growth streak intact.

The trade-offs are real but manageable. Free cash flow remains negative, dividend growth is intentionally slow at 1% to 2% per year, and the stock is now trading near its 52-week high with analyst price targets offering limited additional upside in the near term. For investors prioritizing consistency over high growth, OGS still fits the bill, but patience is required and total return expectations should be anchored primarily to the income component.

At its current valuation, the stock is fairly priced rather than deeply discounted, making it a reasonable hold for existing shareholders and a cautious consideration for new investors who value stability over rapid capital appreciation. Long-term performance will depend largely on how effectively management navigates its capital program, maintains constructive regulatory relationships, and translates rate base growth into earnings that can support continued dividend increases.