Updated 2/23/26

Nutrien Ltd. is a global leader in crop nutrients, playing a vital role in feeding the world. As the largest producer of potash and a key supplier of nitrogen and phosphate fertilizers, the company operates at the heart of the agricultural industry. Farmers depend on Nutrien’s products to maximize yields, making the company an essential part of the global food supply chain.

But like any business tied to commodity prices, Nutrien experiences swings in profitability. When demand for fertilizers is high, revenues and earnings climb. When prices weaken, the company faces financial pressure. This cyclical nature is something investors, especially those focused on dividends, need to consider carefully.

For income investors, the big question is whether Nutrien’s dividend can withstand the ups and downs of the industry. The picture today looks considerably healthier than it did a year ago, so let’s take a deeper look.

Recent Events

Nutrien’s stock has staged a meaningful recovery over the past twelve months, climbing from lows near $45.78 to its current price of $71.91, approaching the 52-week high of $73.55. This rebound reflects improved investor sentiment around agricultural inputs as fertilizer pricing has shown signs of stabilization following a prolonged period of pressure. The company’s market capitalization now stands at approximately $35 billion, reflecting renewed confidence in the earnings trajectory.

On the capital return front, Nutrien has continued to reward shareholders through its share repurchase program while maintaining its quarterly dividend at $0.545 per share. The dividend was last raised from $0.54 to $0.545 beginning with the March 2025 payment, a modest but deliberate signal that management remains committed to growing the payout even in a transitional earnings environment. With full-year EPS now recovering to $3.71, the payout ratio has corrected sharply from the elevated levels seen in prior periods, providing a much more stable foundation for the dividend going forward.

Key Dividend Metrics

🔹 Dividend Yield: 3.06%

📆 Annual Dividend: $2.20 per share

💰 Last Quarterly Payment: $0.545 per share

📈 Dividend Growth Rate (5-Year Avg.): ~5.5%

⚖️ Payout Ratio: 58.63% (well within sustainable range)

✅ EPS: $3.71 (strong recovery year-over-year)

💵 Free Cash Flow: $1.35B (solid support for dividend payments)

📊 Operating Cash Flow: $4.01B

Dividend Overview

Nutrien’s dividend story has improved considerably from where it stood a year ago. The annual dividend now sits at $2.20 per share, producing a yield of 3.06% at the current price of $71.91. While that yield is lower than the elevated readings seen when the stock was trading in the mid-$40s to low $50s, it now comes with a far more reliable earnings foundation beneath it.

The payout ratio has corrected sharply to 58.63%, down from the alarming 158.82% recorded in the prior year when depressed earnings made the dividend look precarious. A payout ratio below 60% is generally viewed as healthy and sustainable, and it gives Nutrien meaningful room to continue growing the dividend or absorb any near-term earnings softness without putting the payout at risk. The company’s operating cash flow of $4.01 billion provides additional confidence that dividend payments are well-covered even after accounting for capital expenditures.

Income investors who were cautious about the dividend’s sustainability during the difficult earnings period of 2023 and early 2024 now have considerably better data supporting the case for holding NTR as an income position. The combination of a recovering payout ratio, steady free cash flow of $1.35 billion, and management’s demonstrated willingness to raise the dividend incrementally paints a more constructive picture heading into 2026.

Dividend Growth and Safety

Nutrien has maintained a five-year average dividend growth rate of approximately 5.5% annually, and the recent dividend history confirms that trajectory has remained intact through the cycle. Looking at payments over the past several years, the quarterly dividend moved from $0.48 in late 2022, to $0.53 in early 2023, then to $0.54 in early 2024, and most recently to $0.545 beginning with the March 2025 payment. These incremental raises reflect a management team that prioritizes consistent, if modest, dividend growth over dramatic increases that could prove difficult to sustain.

The critical shift from the prior report is the dramatic improvement in the payout ratio. When EPS collapsed to levels that pushed the payout ratio above 150%, the dividend looked genuinely at risk. With EPS now recovered to $3.71 and the payout ratio at 58.63%, those concerns have largely dissipated. The dividend is now covered more than 1.6 times by earnings, and free cash flow of $1.35 billion covers the total annual dividend obligation comfortably.

The underlying industry dynamics still introduce variability. Fertilizer prices remain tied to global crop demand, natural gas costs, geopolitical factors, and currency movements, all of which can shift quickly. Nutrien’s earnings will never be as predictable as a utility or consumer staples company, and investors should price in that cyclicality when sizing their positions. But the current earnings recovery and normalized payout ratio mean the dividend has a much wider margin of safety today than it did twelve months ago, and the risk of a cut in the near term appears low as long as the earnings environment remains stable.

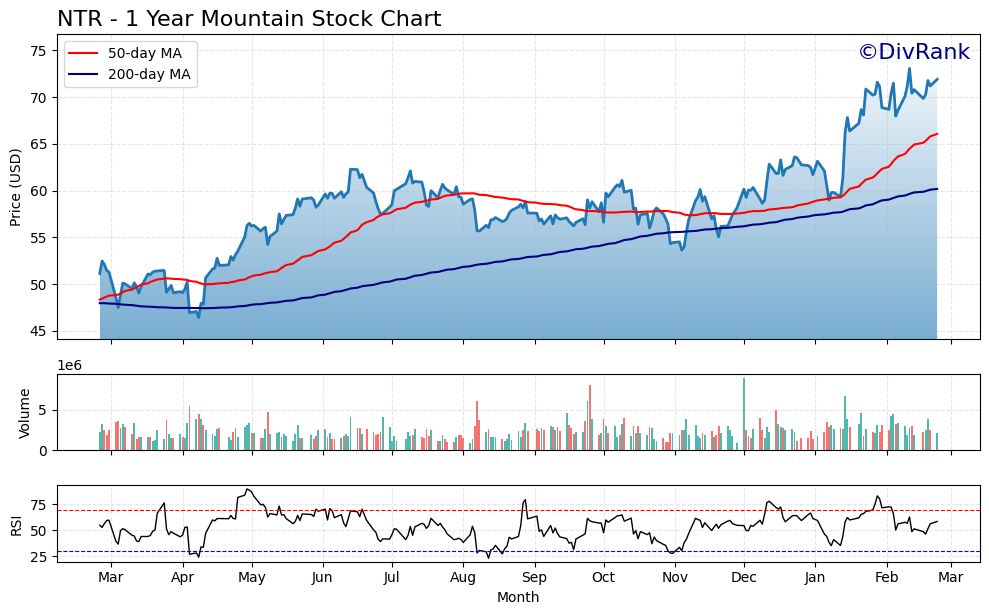

Chart Analysis

Nutrien’s chart tells a compelling recovery story over the past twelve months. The stock carved out a 52-week low of $46.44 before staging a sustained advance that has carried shares to $71.91, a gain of roughly 55% from the trough. That kind of price appreciation in a fertilizer name reflects a meaningful shift in market sentiment around agricultural input demand and potash pricing, and it places NTR within striking distance of its 52-week high of $73.07, just 1.59% below that ceiling as of the most recent close. The proximity to a multi-year resistance level warrants attention, but the underlying trend structure heading into that test is constructive.

The moving average picture reinforces that constructive read. Nutrien’s 50-day moving average currently sits at $66.07, and the 200-day moving average has climbed to $60.19, with the shorter-term average running well above the longer-term one. That configuration is a classic golden cross alignment, a signal that has historically indicated a durable shift from a downtrend into a sustained uptrend rather than a simple short-term bounce. The fact that the current price of $71.91 trades above both averages by meaningful margins adds further confirmation that buyers have been in control across multiple time horizons, not just in recent sessions.

Momentum, as measured by the 14-period RSI reading of 58.66, sits in a healthy middle range. The indicator is elevated enough to confirm that upward price pressure remains intact, yet it stops well short of the overbought threshold near 70, which means the rally has not yet generated the kind of frothy momentum that typically precedes sharp reversals. For investors considering a new position or adding to an existing one, that RSI level is a reasonable signal that there is still room for the trend to continue before the chart becomes technically stretched.

For dividend investors, the technical setup is encouraging on balance. Nutrien has recovered sharply from a deeply oversold condition, established a golden cross, and is now testing resistance near its 52-week high with momentum that has not yet become excessive. A clean breakout above $73.07 on meaningful volume would open the path to price discovery in higher territory, while a brief consolidation just below that level would be a normal and healthy development given the magnitude of the move off the lows. Either outcome is consistent with an income-oriented holding thesis, particularly for investors collecting Nutrien’s dividend while the position matures.

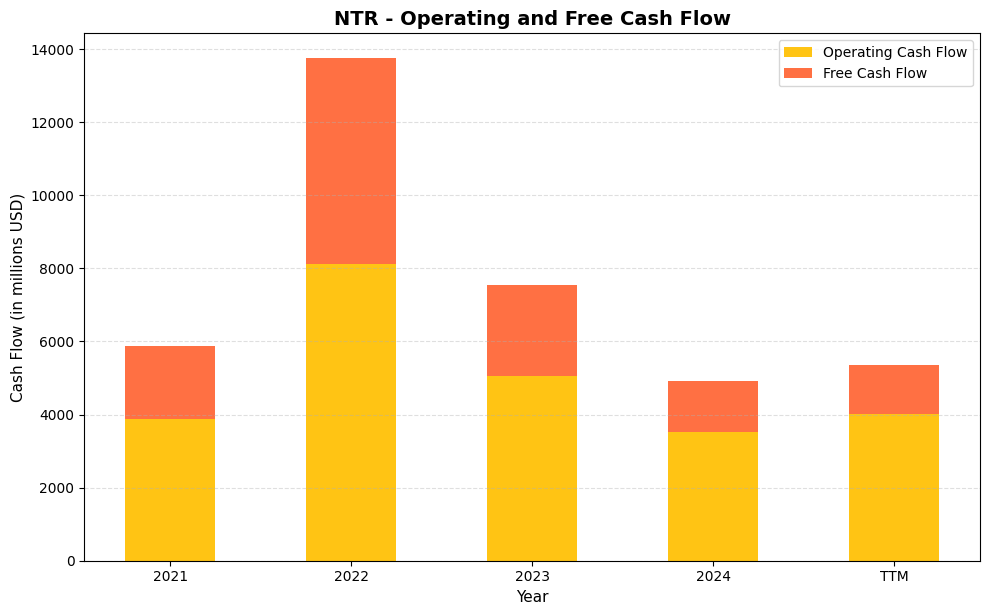

Cash Flow Statement

Nutrien’s cash flow profile tells an important story about the cyclical nature of the fertilizer business. Operating cash flow peaked at $8,110.0M in 2022, a year defined by extraordinary nutrient pricing in the wake of global supply disruptions, then retreated to $5,066.0M in 2023 and further to $3,535.0M in 2024 as commodity prices normalized. The TTM figure of $4,007.0M suggests some stabilization, though it remains well below the 2022 highs. Free cash flow followed the same arc, surging to $5,635.0M in 2022 before compressing to $1,381.0M in 2024 and a TTM reading of $1,350.9M. With Nutrien paying out roughly $1.0B to $1.2B annually in dividends at current rates, the 2024 and TTM free cash flow figures still cover the dividend, but the margin of safety has narrowed considerably compared to the windfall years, which is a dynamic income investors need to monitor closely.

Zooming out across the full period, the 2021 baseline of $2,002.0M in free cash flow is actually a reasonable proxy for what a mid-cycle earnings environment looks like for this business, and the current TTM free cash flow of $1,350.9M is running below that baseline, which reflects both the normalization of potash and nitrogen prices and sustained capital expenditure commitments. Nutrien has been investing meaningfully in its retail network and production capacity, which is visible in the consistent gap between operating and free cash flow across every year in the dataset. That capital intensity is a structural feature, not an anomaly. For shareholders, the key takeaway is that Nutrien’s dividend is a product of cycle management, and the company has historically used share buybacks and variable distribution adjustments to balance returns with balance sheet discipline during leaner periods. The current trajectory warrants attention, but the business generates sufficient cash at mid-cycle conditions to sustain the dividend without distress.

Analyst Ratings

The analyst community has grown more constructive on Nutrien as the stock has recovered and earnings have normalized. Nineteen analysts currently cover NTR with a consensus rating of Buy, reflecting broad confidence in the company’s positioning within the agricultural inputs sector as fertilizer pricing stabilizes and demand from key growing regions remains firm.

The mean price target among covering analysts sits at $72.85, which is modestly above the current price of $71.91, suggesting the stock is trading very close to consensus fair value at this point in the cycle. The range of targets is wide, running from a low of $60.00 to a high of $85.00, which captures both the downside scenario of renewed fertilizer price weakness and the upside case of continued demand recovery combined with operational leverage. Analysts on the more optimistic end of the range point to Nutrien’s scale advantages, its vertically integrated retail network through Nutrien Ag Solutions, and the structural tailwinds of global food security demand as reasons to assign above-consensus valuations.

The consensus Buy rating, combined with a mean target that is essentially in line with the current price, suggests the market has done a reasonable job of pricing in the earnings recovery. Investors adding to positions at current levels are relying more on continued earnings growth and dividend income than on a significant multiple re-rating from current levels. Any upward revisions to fertilizer price forecasts or stronger-than-expected planting season data could push price targets higher and provide additional near-term upside.

Earnings Report Summary

Nutrien’s most recent full-year financials show a company that has worked through the trough of its earnings cycle and emerged in a considerably stronger position. Revenue came in at approximately $25.9 billion, and net income recovered to $2.27 billion, producing EPS of $3.71. That represents a substantial improvement from the depressed earnings that characterized fiscal year 2024, when the combination of weak fertilizer prices and elevated input costs compressed margins across the business.

Operating cash flow of $4.01 billion demonstrates that the underlying business generates substantial cash even in a normalized pricing environment. Free cash flow of $1.35 billion, after accounting for capital expenditures, provides the company with the resources to fund its dividend, continue share repurchases, and invest in the operational improvements needed to maintain its cost position in potash and nitrogen.

The retail segment, operating under the Nutrien Ag Solutions brand, has continued to be a stabilizing force in the business model. This division provides exposure to farmer spending on crop protection, seed, and services in addition to fertilizer, which gives it somewhat less volatility than the pure nutrient segments. The potash and nitrogen segments have benefited from improving volumes and pricing conditions as the supply glut that weighed on the market in 2023 and 2024 has gradually worked itself through the system. The phosphate segment remains the most challenged of the three nutrient divisions, facing ongoing competition and demand variability, but it represents a smaller share of overall earnings.

Profit margin stands at 8.74% and return on equity at 9.22%, both representing meaningful improvements from the prior period. Return on assets of 4.17% reflects the capital-intensive nature of the business but is consistent with where Nutrien has historically operated during mid-cycle conditions. Management has maintained its focus on cost discipline and capital allocation efficiency, which has helped the company convert a higher proportion of revenue into free cash flow as pricing has recovered.

Management Team

Nutrien’s management team has navigated a particularly challenging earnings cycle over the past two years, and the financial results now emerging suggest those efforts to maintain operational discipline and protect the balance sheet have paid off. The team’s decision to continue raising the dividend incrementally, even as earnings were under pressure, reflected confidence in the company’s cash flow generation and the cyclical nature of the weakness rather than a structural deterioration in the business.

Capital allocation decisions have been consistent with the priorities management has communicated to shareholders: maintain the dividend and grow it modestly, execute share repurchases when the stock offers reasonable value, invest in the retail network and nutrient production facilities to preserve competitive advantages, and manage the balance sheet conservatively through the commodity cycle. The incremental raise from $0.54 to $0.545 per quarter, announced alongside the 2024 full-year results, reinforced that message even as earnings were still recovering.

Management’s guidance for 2025 and into 2026 has reflected a measured optimism about demand trends, particularly around North American corn planting intentions and recovering international demand for potash. The company has also continued its focus on reducing the cost of potash production at its Canadian mines, which remains a key long-term competitive advantage given Nutrien’s position as the world’s largest producer of the nutrient.

Valuation and Stock Performance

Nutrien’s stock is currently trading at $71.91, near the top of its 52-week range of $45.78 to $73.55. The stock’s recovery from its lows reflects the meaningful improvement in earnings and the broader stabilization of fertilizer market conditions. Investors who added exposure when the stock was trading in the high $40s to low $50s have been rewarded with both capital appreciation and a higher-than-average entry yield.

At the current price, the trailing P/E ratio of 19.38 is far more reasonable than the inflated multiples seen when depressed earnings made the stock appear expensive on an earnings basis. A price-to-book ratio of 1.37 against a book value per share of $52.54 suggests the market is assigning a modest premium to Nutrien’s asset base, which is appropriate given the company’s dominant market position and cash generation capacity. The stock’s beta of 1.14 reflects its sensitivity to commodity price cycles and broader market movements, which income investors should factor into their position sizing.

With the mean analyst price target at $72.85, the stock is trading essentially at consensus fair value, which means near-term upside depends on either earnings outperformance relative to current expectations or an expansion in the market’s willingness to pay a higher multiple for agricultural input exposure. At a 3.06% yield with a normalized payout ratio of 58.63%, NTR offers a reasonable income profile for investors who are comfortable with the cyclical nature of the business and are focused on the dividend’s sustainability rather than maximizing entry yield.

Risks and Considerations

The most persistent risk for Nutrien shareholders is commodity price volatility. Fertilizer prices, particularly for potash and nitrogen, are set by global supply and demand dynamics that are largely outside the company’s control. A meaningful decline in crop commodity prices could reduce farmers’ willingness to spend on inputs, putting pressure on volumes and selling prices simultaneously and compressing Nutrien’s margins quickly. The earnings cycle of 2023 and 2024 provided a clear reminder of how rapidly conditions can deteriorate when supply exceeds demand.

Nutrien carries a substantial debt load, and while the company has managed its balance sheet responsibly through the cycle, interest expenses represent a real ongoing cost that limits financial flexibility. In a rising rate environment or a scenario where operating cash flow weakens significantly, the debt burden could constrain the company’s ability to maintain its dividend growth trajectory or execute opportunistic share repurchases.

The company’s exposure to geopolitical developments is meaningful given that global potash supply is concentrated in a small number of producing countries. Disruptions to trade flows, sanctions, or export restrictions from competing producers can introduce volatility into pricing and supply availability, which can affect Nutrien both positively and negatively depending on the nature of the disruption.

Macroeconomic headwinds, including changes in global trade policy, currency fluctuations, and shifts in agricultural subsidy regimes across key markets, all have the potential to affect Nutrien’s revenue and earnings in ways that are difficult to predict. Natural gas prices are particularly important for the nitrogen segment, where feedstock costs represent a large portion of production expenses, and a sustained increase in North American natural gas prices could compress nitrogen margins even if selling prices remain stable.

Finally, while the payout ratio has normalized significantly, investors should recognize that Nutrien’s dividend history includes periods of both growth and relative stagnation, and the company will always prioritize balance sheet health and operational investment over maximizing near-term dividend increases. Income investors seeking predictable, recession-resistant dividend growth may find Nutrien’s cyclical earnings profile requires patience and a longer investment horizon than more defensive income alternatives.

Final Thoughts

Nutrien’s investment case looks materially better today than it did a year ago. The combination of recovering EPS at $3.71, a normalized payout ratio of 58.63%, and operating cash flow of $4.01 billion has put the dividend on a genuinely solid footing after a period when its sustainability was a legitimate question. The annual dividend of $2.20 per share, yielding 3.06% at the current price, is now backed by earnings coverage rather than relying primarily on cash flow as a bridge through a trough.

The stock’s recovery to $71.91 means that the most attractive entry points have likely passed for investors who were waiting on the sidelines, and the mean analyst price target of $72.85 suggests consensus fair value is close to current trading levels. That does not make NTR unattractive, but it does mean that return expectations from this point should be calibrated around dividend income and earnings growth rather than multiple expansion.

For income investors who can accept the cyclicality inherent in agricultural inputs, Nutrien offers a compelling combination of scale, global market leadership, and a dividend that has now demonstrated resilience through a genuine earnings downturn. The payout ratio has room to absorb another period of earnings pressure without requiring a cut, and management’s track record of incremental dividend growth through the cycle is an encouraging signal about long-term capital return priorities.