Updated 2/23/26

Nucor Corporation (NUE) has built a reputation as one of the strongest names in the steel industry. As the largest steel producer in the United States, the company has mastered the art of navigating economic cycles while maintaining profitability. What makes Nucor stand out is its ability to run efficiently, keeping costs low while maximizing cash flow.

For dividend investors, this remains an attractive stock to consider. The company has been consistently rewarding shareholders through its dividend program, proving its commitment even when the steel industry faces headwinds. Nucor’s stock has recovered meaningfully from its 52-week low of $97.59, currently trading around $178.85 and sitting closer to the top of its annual range, which reflects renewed investor confidence in the company’s earnings trajectory and long-term positioning.

Recent Events

Nucor has been navigating a complex operating environment heading into 2026. The domestic steel market has faced pressure from softening demand in key end markets, including automotive and commercial construction, while steel pricing has remained volatile against a backdrop of shifting global trade policy. Tariff discussions in Washington have continued to create uncertainty, though Nucor as a domestic producer generally benefits from protective trade measures that limit foreign competition. The company has remained focused on its capital allocation priorities, continuing to fund its dividend, pursue share repurchases, and invest in its ongoing capacity expansion initiatives. Nucor’s transition to higher-value steel products and its growing downstream businesses have also remained central themes for management, as the company works to reduce its sensitivity to raw commodity steel pricing cycles.

Key Dividend Metrics

📈 Dividend Yield: 1.23% — Well-supported by free cash flow generation and a conservative payout structure.

💰 Annual Dividend: $2.24 per share — Reflecting the most recent quarterly payment of $0.56.

🔁 Dividend Growth Streak: 52 consecutive years — One of the longest active streaks in the entire market.

📊 Payout Ratio: 29.39% — A conservative level that leaves substantial room for continued increases.

📆 Last Dividend Payment: $0.56 per share, paid December 31, 2025.

Dividend Overview

Nucor has one of the most reliable dividend programs in the industrial sector. With an extraordinary 52-year history of raising dividends, the company has demonstrated a deep and consistent commitment to rewarding shareholders regardless of economic conditions. The most recent quarterly payment of $0.56 per share represents a modest but meaningful increase from the $0.55 rate that held through most of 2025, continuing a pattern of steady annual growth that income investors have come to rely on.

The payout ratio of 29.39% confirms that the dividend is highly sustainable. With earnings per share of $7.51 supporting an annual dividend of just $2.24, Nucor retains the vast majority of its profits for reinvestment and share repurchases. Some companies pay out nearly all of their earnings in dividends, which can lead to cuts during downturns. Nucor avoids that trap entirely, ensuring its dividend is both secure and positioned to grow over time.

Dividend Growth and Safety

For investors focused on dividend stability, Nucor continues to check all the important boxes. The company has now extended its consecutive annual dividend increase streak to 52 years, placing it firmly among the elite Dividend Kings. The most recent increase, from $0.55 to $0.56 per share quarterly, came with the December 2025 payment and marks the latest step in a five-decade journey of uninterrupted shareholder income growth.

The steel industry is highly cyclical, meaning profits can fluctuate considerably depending on economic conditions and commodity pricing. However, Nucor’s approach to cost management, which relies heavily on electric arc furnace technology and a variable compensation structure for employees, allows it to remain profitable even when steel prices decline sharply. This is the structural reason its dividend has continued growing through multiple recessions and steel downturns. The current payout ratio near 29% provides a meaningful buffer, and with operating cash flow of $3.23 billion in the trailing period, the company has more than enough cash generation to support the dividend even if earnings compress modestly in the near term.

Of course, the company’s earnings remain tied to steel prices and industrial demand, so investors should expect that dividend growth may moderate during weaker periods. That said, Nucor’s history across more than five decades suggests it will continue rewarding shareholders over the long run, even if the pace of increases varies from year to year.

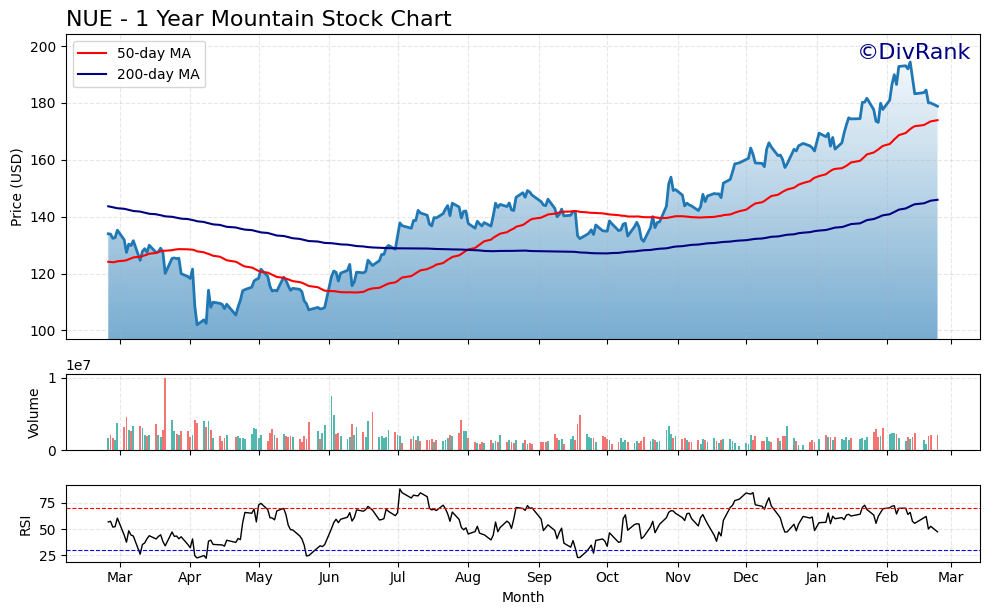

Chart Analysis

Nucor’s price chart tells a compelling recovery story over the trailing twelve months. Shares bottomed near $102.02 at the 52-week low before staging a 75.3% advance to the current price of $178.85, a move that reflects both the broader recovery in steel demand and renewed investor confidence in Nucor’s earnings durability. The stock is now trading within 8% of its 52-week high of $194.42, which means the bulk of the recovery work has already been done and the chart is entering territory where near-term resistance becomes a more relevant consideration for prospective buyers.

The moving average picture is constructive. Nucor is trading above both its 50-day moving average of $173.95 and its 200-day moving average of $145.96, and the 50-day has crossed above the 200-day to form what technicians call a golden cross, a configuration that historically signals sustained upward momentum rather than a short-lived bounce. The gap between the current price and the 200-day average is nearly $33, which provides a meaningful cushion against a retest of longer-term support. For dividend investors who are less concerned with short-term timing, the fact that price is holding comfortably above both trend lines suggests the underlying technical structure remains intact.

The RSI reading of 47.41 is particularly interesting in the context of a stock sitting near annual highs. A reading in the mid-40s indicates that momentum has cooled from what were likely overbought conditions earlier in the rally, without sliding into oversold territory. In practical terms, this suggests the recent consolidation near $178 to $180 is a digestion of gains rather than the beginning of a meaningful reversal. For income-focused investors, a neutral RSI at elevated price levels is often a more comfortable entry point than chasing a stock with an RSI pushing above 70.

Taken together, the technical setup for Nucor presents a reasonable backdrop for dividend investors evaluating a new position or adding to an existing one. The trend is clearly up, the moving averages are properly aligned, and the momentum indicator suggests the stock is neither overheated nor under pressure. The primary caution is that the stock is approaching the upper boundary of its one-year range, so patience around the $175 to $178 area may offer a marginally better risk-adjusted entry should any softness materialize. For long-term holders focused on Nucor’s dividend growth track record, the chart does nothing to argue against the thesis.

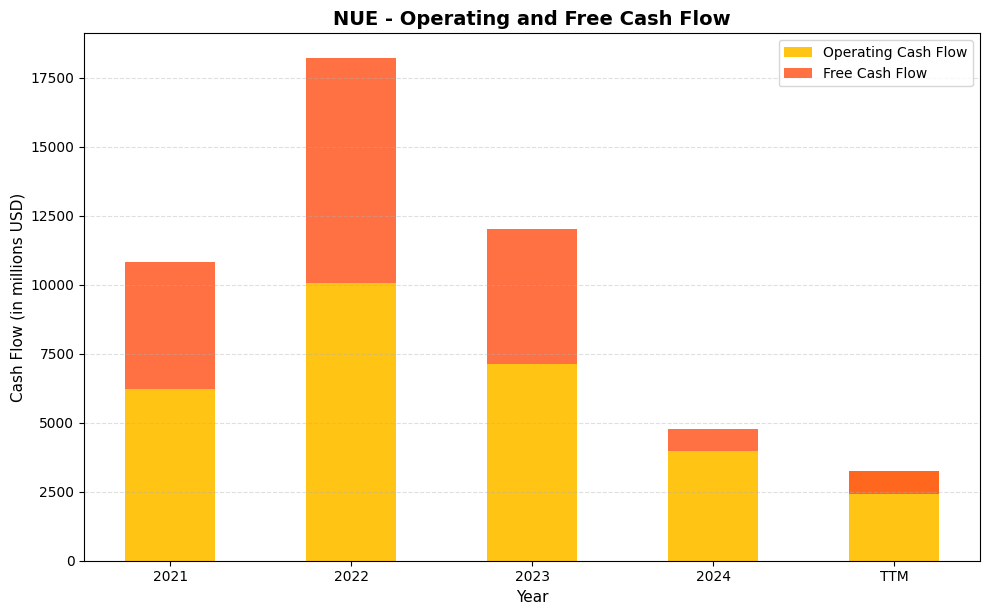

Cash Flow Statement

Nucor’s cash flow profile has shifted materially over the past few years, and income investors need to understand what’s driving that shift before drawing conclusions about dividend safety. Operating cash flow peaked at $10.1 billion in 2022, a year when steel prices were running exceptionally hot, then retreated to $7.1 billion in 2023 and further to $4.0 billion in 2024 as the steel cycle normalized. The TTM figure of $3.2 billion reflects continued pressure from softer steel pricing and elevated capital spending. Free cash flow tells a sharper story: it fell from a cycle-peak $8.1 billion in 2022 to just $806 million in 2024, and the TTM figure has turned negative at $808 million. That negative free cash flow number is the headline risk for dividend coverage right now, though it reflects an aggressive capital expenditure cycle rather than deteriorating core operations, an important distinction for long-term holders.

Zooming out across the full period shown, Nucor generated enormous cumulative cash flows during the 2021 and 2022 supercycle years, which funded both a dramatically higher dividend and significant share repurchases while also seeding the company’s ongoing capacity expansion program. The current capex intensity, which is compressing near-term free cash flow, is largely the product of investments in new sheet mills and downstream diversification that management expects to lift the earnings floor in future cycles. Nucor’s dividend commitment of roughly $540 million annually remains well within reach of operating cash flow at current levels, so the payout itself is not in jeopardy even as free cash flow runs temporarily negative. The more meaningful question for shareholders is how quickly the new capacity translates into incremental earnings power when the next upcycle arrives, because that answer will determine whether Nucor returns to its pattern of aggressive variable supplemental dividends and buybacks or remains in a more restrained capital return posture through the mid-cycle.

Analyst Ratings

The analyst community currently holds a consensus buy rating on Nucor, with 13 analysts contributing to the current coverage universe. The mean price target of $186.08 implies modest upside of roughly 4% from the current price of $178.85, suggesting that the stock is trading near fair value in the eyes of the street. The range of targets is fairly wide, spanning from a low of $162.00 to a high of $206.00, which reflects the genuine uncertainty around steel pricing and demand conditions over the next twelve months.

Analysts who are more constructive on the name point to Nucor’s cost advantages, its downstream diversification strategy, and the potential for tariff protections to support domestic steel pricing. Those with more cautious targets tend to emphasize the cyclical earnings risk, particularly if construction and manufacturing activity soften further or if a trade policy reversal opens the door to more imported steel. With the stock sitting below the mean target but above the bear case, the consensus view is that Nucor is appropriately valued for a patient, income-oriented investor willing to accept some near-term earnings variability.

Earnings Report Summary

Nucor’s most recent full-year results reflect a steel industry that has been under meaningful pricing and volume pressure. The company generated revenue of $32.49 billion and net income of $1.74 billion for the trailing period, translating to earnings per share of $7.51. These figures represent a significant step down from the elevated earnings Nucor produced during the 2022 and 2023 commodity supercycle, when the company earned more than $18 per share in a single year. The current profit margin of 5.37% is leaner than recent peak levels but still demonstrates the company’s ability to generate meaningful income throughout a down cycle.

Operating cash flow came in at $3.23 billion, a strong figure that underscores the cash-generative nature of Nucor’s business model even when net income is compressed. Free cash flow turned negative at approximately $808 million for the period, reflecting elevated capital expenditure as the company continues investing in capacity expansion and product mix upgrades. This level of investment spending is deliberate and management has been transparent about prioritizing long-term competitive positioning over short-term cash generation. Return on equity of 9.36% and return on assets of 4.81% are both consistent with a company in a mid-cycle earnings trough rather than one facing structural deterioration.

Looking ahead, the key variables for Nucor’s earnings recovery are domestic steel prices, utilization rates at its mill network, and the trajectory of construction and industrial end markets. Management has signaled continued confidence in the long-term demand picture, supported by infrastructure investment, reshoring of manufacturing, and the ongoing buildout of data center and energy infrastructure across the United States.

Management Team

Nucor is led by Leon Topalian, who has served as President and Chief Executive Officer since 2019. Topalian joined Nucor in 1996 and worked his way through various operational and leadership roles before assuming the top position, giving him a deep understanding of the company’s decentralized culture and manufacturing operations. His tenure has been characterized by continued investment in value-added products and downstream capabilities, as well as a disciplined approach to capital allocation that has kept the balance sheet in solid condition even through the current earnings downcycle.

Steve Laxton serves as Executive Vice President and Chief Financial Officer, overseeing the company’s financial strategy, capital markets activity, and investor relations function. The broader management team reflects Nucor’s long-standing practice of promoting from within, which has historically contributed to strong cultural cohesion and operational consistency across its facilities. This management philosophy is part of the reason Nucor has been able to sustain its dividend growth streak through multiple industry cycles over more than five decades.

Valuation and Stock Performance

From a valuation perspective, Nucor sits in an interesting position for income investors evaluating an entry point. The stock currently trades at $178.85, well above its 52-week low of $97.59 but still approximately $18 below its 52-week high of $196.90. The trailing price-to-earnings ratio of 23.81 is somewhat elevated relative to historical norms for a cyclical steel company, reflecting the fact that current earnings are depressed relative to what Nucor is capable of generating in a stronger pricing environment. On a normalized earnings basis, the stock looks considerably more attractive.

The price-to-book ratio of 1.96 against a book value per share of $91.30 is a reasonable multiple for a company with Nucor’s operational efficiency and return profile. With a market cap of approximately $40.9 billion and a beta of 1.84, the stock carries above-average volatility relative to the broader market, which is expected for a cyclical industrial name. For long-term dividend investors, that volatility can create attractive accumulation opportunities when the market becomes overly pessimistic about near-term steel conditions, as it did when the stock fell toward the low end of its 52-week range.

Risks and Considerations

The most persistent risk for Nucor investors is the cyclical nature of the steel industry. Steel prices are heavily influenced by broader economic conditions, construction activity, and manufacturing output. When these factors soften simultaneously, as they have in recent periods, earnings can compress significantly even for a well-run operator like Nucor. The current EPS of $7.51 compares to peak earnings well above $18 per share, illustrating just how wide that cyclical swing can be.

Global trade policy represents another material risk. While domestic steel producers generally benefit from tariffs on imported steel, policy shifts in Washington can alter the competitive landscape quickly. Any significant reduction in trade protections, or retaliatory measures from trading partners that slow U.S. industrial exports, could weigh on domestic steel demand and pricing power. The uncertainty around trade policy has been a recurring theme in recent quarters and is unlikely to fully resolve in the near term.

Capital expenditure commitments are also worth monitoring. Nucor is currently investing heavily in expanding capacity and upgrading its product mix, which has pushed free cash flow negative. While this investment is strategic and management has a strong track record of deploying capital wisely, sustained negative free cash flow limits financial flexibility and could become a concern if the earnings environment deteriorates further before demand recovers.

Finally, with a beta of 1.84, Nucor’s stock is considerably more volatile than the broader market. Investors who are sensitive to portfolio drawdowns should be prepared for meaningful price swings, particularly during periods of economic uncertainty or commodity market disruption. That said, for investors with a long time horizon, this volatility has historically created favorable entry points rather than permanent impairment of value.

Final Thoughts

For dividend investors, Nucor remains one of the most reliable names in the industrial sector. It combines steady income, a 52-year consecutive dividend growth streak, and genuine financial resilience, making it a strong candidate for a long-term income-oriented portfolio.

The current yield of 1.23% is modest, but it is backed by one of the longest uninterrupted dividend growth records in the entire market and a payout ratio well below 30%, which means the income stream is extremely well protected even in a challenging earnings environment. The most recent increase to $0.56 per quarter confirms that management remains committed to continuing that growth tradition despite the cyclical earnings headwind.

While near-term stock performance will remain sensitive to steel prices, industrial demand, and trade policy developments, Nucor’s structural advantages, including its low-cost electric arc furnace model, decentralized culture, and disciplined capital allocation, give it a durable competitive position that dividend investors can rely on through multiple market cycles. Investors who focus on dividend safety and long-term compounding will likely continue to find Nucor a rewarding fit for their portfolio.