Updated 2/23/26

Northrop Grumman (NYSE: NOC) is one of the leading names in the defense industry, specializing in aerospace, cybersecurity, and autonomous systems. As a key contractor for the U.S. government, the company benefits from long-term contracts that provide steady revenue. While it may not be the first stock that comes to mind for high-yield investors, it has consistently rewarded shareholders with growing dividends over the years.

For those who prioritize dividend growth and stability over sheer yield, Northrop Grumman presents an interesting case. With solid financials, a sustainable payout ratio, and a long history of dividend increases, it deserves a closer look from income-focused investors who value compounding over yield-chasing.

Recent Events

Northrop Grumman has continued to benefit from a robust defense spending environment heading into 2026. The company reported full-year revenue of approximately $41.95 billion, reinforcing its position as one of the largest defense contractors in the world. The B-21 Raider stealth bomber program, which weighed on results in prior periods, has made meaningful progress, and management has signaled improving production economics on that platform. The stock has surged sharply over the past year, climbing from a 52-week low of $449.21 to a recent high of $745.55, reflecting renewed investor confidence in defense sector fundamentals and NOC’s execution. Geopolitical tensions across Europe and the Indo-Pacific continue to drive demand for Northrop’s advanced systems, and the company’s backlog remains robust, supporting revenue visibility well into the latter part of the decade.

Key Dividend Metrics

📌 Dividend Yield: 1.25%

📌 Annual Dividend Payout: $9.24 per share

📌 Payout Ratio: 30.91% (well-covered by earnings)

📌 5-Year Average Dividend Yield: 1.60%

📌 Dividend Growth Streak: Over 20 years

📌 Last Dividend Payment: $2.31 per share

📌 Most Recent Ex-Dividend Date: December 1, 2025

Dividend Overview

Northrop Grumman may not be a high-yield dividend stock, but it has a strong track record of rewarding investors with consistent and growing payouts. The current dividend yield of 1.25% has compressed as the share price has appreciated significantly, but what stands out is the company’s demonstrated ability to raise its dividend year after year regardless of market conditions.

A key factor behind this reliability is its defense contracts, which provide predictable and long-duration cash flows. Unlike cyclical industries that fluctuate with economic conditions, government defense spending tends to be structurally stable, allowing Northrop Grumman to maintain a steady dividend policy without major disruptions.

The payout ratio, sitting at just under 31%, indicates that the company has ample room to continue raising dividends. Since a lower payout ratio means a company is using only a small portion of its earnings to pay dividends, this conservative approach is a positive sign for both sustainability and future growth potential.

Dividend Growth and Safety

One of the standout features of Northrop Grumman’s dividend policy is its strong and consistent growth trend. The company has increased its dividend for over two decades, and that upward trajectory shows no signs of stopping. The most recent increase brought the quarterly payment to $2.31 per share, up from the prior rate of $2.06, representing a raise of approximately 12% and pushing the annualized payout to $9.24 per share.

Dividend Growth Rate

✅ 10-Year CAGR: Approximately 11%

✅ 5-Year CAGR: Around 9%

These numbers reflect Northrop Grumman’s commitment to rewarding shareholders while maintaining financial flexibility. The progression through the recent dividend history tells that story clearly: the quarterly payment moved from $1.73 in early 2023, to $1.87 later that year, then to $2.06 in mid-2024, and most recently to $2.31 in mid-2025. That is a consistent staircase of raises that income-growth investors can rely on.

Dividend Safety

With a payout ratio of just 30.91%, the dividend is well-covered by earnings. This conservative ratio means the company retains the majority of its profits for reinvestment in programs, capital expenditures, and share repurchases while still delivering a growing payout to shareholders. Free cash flow of approximately $2.90 billion further supports the dividend, which costs the company roughly $1.30 billion annually at current share counts, leaving substantial coverage. Even during uncertain economic times, steady revenue from long-term government contracts makes a dividend cut highly unlikely.

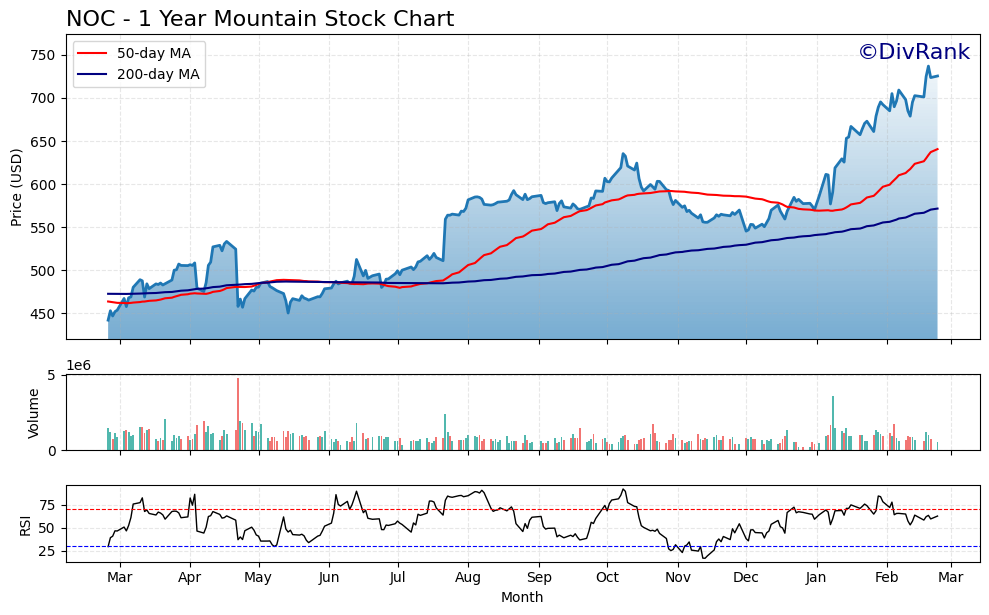

Chart Analysis

Northrop Grumman’s price chart tells a compelling recovery story over the past twelve months. Shares bottomed near $442.26 at the 52-week low before staging a broad, sustained advance that has carried the stock to $725.39, a gain of roughly 64% from that trough. That kind of price appreciation is unusual for a mature defense contractor, and it reflects a meaningful re-rating in how the market is pricing both the company’s earnings power and its long-term contract backlog. With the 52-week high sitting at $736.87, NOC is now trading within 1.56% of its annual peak, which places it firmly in breakout territory rather than recovery mode.

The moving average picture reinforces the bullish technical setup. The 50-day moving average has crossed above the 200-day moving average, a pattern technically referred to as a golden cross, and that configuration has historically signaled durable uptrends rather than short-term bounces. The 50-day currently sits at $640.61 and the 200-day at $571.66, both well below the current price of $725.39. That separation between price and both moving averages suggests the trend has genuine momentum behind it, and it also means dividend investors who have been accumulating shares over the past year are sitting on meaningful unrealized gains that provide a cushion against near-term volatility.

The Relative Strength Index reading of 62.54 adds useful context to the momentum picture. A reading in the low-to-mid 60s indicates solid upside momentum without crossing into the overbought territory that typically accompanies readings above 70. For income investors, this is actually a favorable zone because it suggests the move has room to continue without the elevated reversal risk that comes with an overextended rally. The stock is not flashing warning signs of a crowded trade, even as it approaches its 52-week high.

For dividend-focused investors, the technical picture at NOC is about as constructive as it gets for a large-cap defense name. The combination of a golden cross, price trading meaningfully above both major moving averages, and an RSI that reflects momentum without excess suggests the current uptrend is intact and not yet exhausted. Investors evaluating an entry point should watch the $736.87 high as the key level to clear for a confirmed breakout, while the 50-day moving average near $640 represents a logical area where longer-term buyers have historically stepped in. The chart supports a patient, accumulate-on-pullbacks approach that aligns well with a dividend growth strategy.

Cash Flow Statement

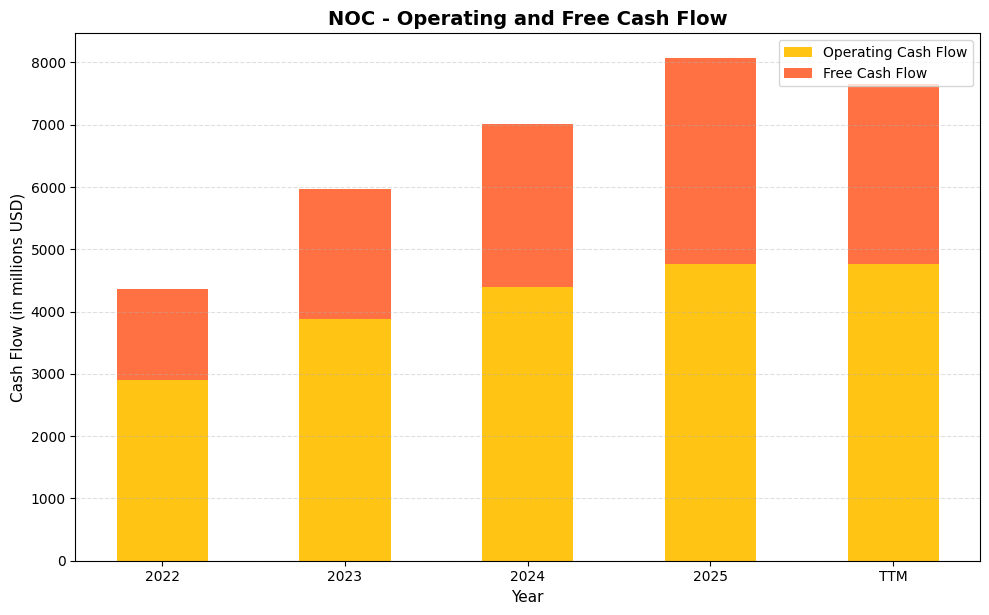

Northrop Grumman’s cash flow profile has strengthened considerably over the past three years, and the trajectory makes a compelling case for dividend sustainability. Operating cash flow climbed from $2,901.0M in 2022 to $4,388.0M in 2024 and reached $4,757.0M in 2025, a gain of roughly 64% over that span. Free cash flow tells an even more encouraging story, expanding from $1,466.0M in 2022 to $3,307.0M in 2025. With the company paying out approximately $1.6B in dividends annually, the current free cash flow generation covers that obligation more than twice over, which is precisely the kind of cushion long-term income investors want to see. The TTM free cash flow of $2,899.9M reflects some timing variability relative to the full-year 2025 figure, but the underlying generation capacity is not in question.

What makes this trend particularly meaningful for shareholders is the improvement in capital efficiency alongside raw cash growth. Capital expenditures consumed a larger share of operating cash flow in 2022, when the gap between operating CF and free CF was roughly $1,435.0M. By 2025 that gap had narrowed to approximately $1,450.0M in absolute terms, but operating cash flow had scaled so significantly that free cash flow as a percentage of operating cash flow improved from about 50.5% in 2022 to nearly 69.5% in 2025. That shift signals that NOC is extracting more distributable cash from each dollar of operations, a dynamic that supports not only the current dividend but also the company’s consistent history of annual payout increases. For dividend growth investors, a business converting nearly 70 cents of every operating dollar into free cash is one that earns a high degree of confidence in future income reliability.

Analyst Ratings

The analyst community currently holds a consensus buy rating on Northrop Grumman, with 21 analysts contributing to that view. The mean price target sits at $724.39, nearly in line with the current share price of $725.39, which suggests the stock is trading right around fair value in the eyes of the Street. The range of targets is wide, however, spanning from a low of $587.22 to a high of $815.00, reflecting meaningful disagreement about how much runway the stock has following its sharp appreciation over the past year.

Analysts who are more bullish point to the company’s expanding backlog, improving B-21 program economics, and a sustained global defense spending cycle as catalysts that could push the stock toward the higher end of that range. Those with more cautious targets acknowledge the strong fundamentals but flag valuation as a concern given how far the stock has already moved from its 52-week low of $449.21. At the current price, investors are essentially paying for near-term perfection, which is a dynamic worth monitoring as new program updates and budget news emerge throughout 2026.

Overall, the consensus reflects cautious optimism. The buy rating signals confidence in the company’s long-term positioning within the defense sector, but the mean target being essentially at the current price means analysts are not projecting meaningful near-term upside from current levels based on existing models.

Earnings Report Summary

Northrop Grumman delivered a strong full-year financial performance for the period reflected in its most recent results. Revenue came in at approximately $41.95 billion, consistent with the guidance range the company had provided and reflecting sustained demand across its aerospace systems, mission systems, and space segments. Net income reached $4.18 billion, and earnings per share of $29.09 represent a solid result that comfortably covers both the dividend and continued reinvestment in growth programs.

Operating cash flow of $4.76 billion and free cash flow of approximately $2.90 billion demonstrate that the company’s earnings quality remains high, with cash generation closely tracking reported income. Return on equity of 26.17% and a profit margin of nearly 10% are commendable figures for a defense contractor of this scale, where cost-plus contracts and program execution risk can sometimes pressure margins.

The B-21 Raider program, which had been a source of margin headwinds in prior periods due to fixed-price development challenges, has shown signs of stabilization. Progress on production milestones has supported investor confidence that the worst of the program-related earnings drag is behind the company. Meanwhile, the space and cybersecurity segments continue to grow as areas of strategic investment by the U.S. government, providing Northrop with diversification beyond traditional aircraft and weapons platforms.

Looking ahead, the company is expected to sustain revenue in the low-to-mid $40 billion range through 2026, supported by a backlog that extends well beyond the current fiscal year. Earnings per share growth should remain in the high-single-digit to low-double-digit range, which is consistent with continued dividend increases in the 10% neighborhood.

Valuation and Stock Performance

Northrop Grumman has experienced a remarkable re-rating over the past twelve months, with the stock climbing from a 52-week low of $449.21 to a high of $745.55, and currently trading at $725.39. That move has compressed the dividend yield to 1.25% and pushed the valuation to levels that warrant careful consideration from new buyers.

Current Valuation Metrics

📊 Trailing P/E: 24.94

📊 Price-to-Book Ratio: 6.18

📊 Book Value Per Share: $117.42

📊 Market Cap: Approximately $103.5 billion

A trailing price-to-earnings ratio of nearly 25 represents a meaningful premium to where the stock traded just a year ago. For context, the defense sector has historically commanded P/E multiples in the high-teens to low-twenties, so Northrop is now priced toward the upper end of that historical range. The price-to-book of 6.18 is also elevated, though the company’s high return on equity of 26.17% provides some justification for that premium.

Stock Performance

📈 52-Week High: $745.55

📉 52-Week Low: $449.21

📊 Current Price: $725.39

Trading just 3% below its 52-week high, the stock has limited near-term technical upside based on recent price action alone. The beta of 0.04 reflects the stock’s extremely low correlation to broader market movements, which is an attractive characteristic for investors seeking portfolio stability. For long-term dividend growth investors, the current valuation means patience is required, as multiple expansion is unlikely to add to total returns from here. The investment thesis depends more heavily on continued earnings growth and dividend increases than on further multiple expansion.

Risks and Considerations

Even with its strong dividend track record, Northrop Grumman is not without risks, and investors should weigh several factors carefully before adding to or initiating a position at current prices.

The company relies heavily on U.S. government defense spending, which introduces concentration risk. While defense budgets have historically grown due to global security concerns, political shifts, continuing resolutions, or unexpected budget sequestration could delay program funding and create revenue uncertainty. Any change in administration priorities around defense spending programs would likely register quickly in Northrop’s order activity and backlog metrics.

The B-21 Raider program, while improving, remains a long-term fixed-price development contract that has historically pressured margins. Fixed-price programs expose the company to cost overruns that cannot be passed back to the government, and if production ramp-up encounters further engineering or supply chain challenges, margins could come under renewed pressure in ways that are difficult to forecast.

At a current yield of just 1.25%, Northrop Grumman is not a meaningful income source for investors who need current cash flow from their portfolios. The yield has fallen substantially as the stock price has risen, and investors buying at current levels are accepting a lower starting yield than was available as recently as twelve months ago. Those willing to hold for the dividend growth may still see strong long-term income, but the math requires patience.

Geopolitical uncertainty, while often a tailwind for defense contractors, can also introduce supply chain disruptions, labor shortages, and component availability challenges that raise costs and compress margins. The defense industrial base continues to face workforce and materials constraints that are not fully resolved, and Northrop is not immune to those pressures even as end-market demand remains strong.

Final Thoughts

For dividend investors focused on growth and stability, Northrop Grumman continues to present a compelling long-term case. The recent dividend increase to $2.31 per quarter, bringing the annualized payout to $9.24 per share, demonstrates that management remains committed to rewarding shareholders at a pace well above inflation. The payout ratio of 30.91% and free cash flow coverage leave plenty of room for additional increases in the years ahead.

The primary consideration for new investors today is valuation. At a P/E of nearly 25 and with the stock trading near its 52-week high, the margin of safety is thinner than it was a year ago. The consensus analyst price target of $724.39 sits essentially at the current price, meaning the Street sees limited near-term upside without positive catalysts. Existing holders have been well rewarded, and the dividend growth story remains intact.

For those prioritizing dividend growth over immediate high yield, Northrop Grumman remains one of the defense sector’s most reliable compounders. New buyers should consider waiting for a pullback toward the $650 to $680 range to establish a more favorable entry point, while current holders have every reason to stay the course with a company that has consistently delivered for income-growth investors over the long term.