Updated 2/23/26

Northrim BanCorp (NASDAQ: NRIM) isn’t a stock that grabs headlines, but for income-focused investors, it has a lot to offer. This Alaska-based regional bank has built a solid reputation for stability, responsible management, and steady dividend payments. While regional banks can come with their share of challenges, Northrim’s strong financial footing and consistent dividend growth make it worth considering.

For those seeking reliable income, NRIM checks many of the right boxes. Let’s take a closer look at its dividend profile, valuation, and whether it fits into a long-term dividend strategy.

Key Dividend Metrics

📈 Dividend Yield: 2.51%

💵 Annual Dividend: $0.64 per share

📊 Quarterly Dividend: $0.16 per share

🔄 Dividend Growth: Consistent increases each year since 2023

💰 Payout Ratio: 22.30% (Substantial room for future growth)

📅 Last Dividend Payment: $0.16 per share (December 18, 2025)

🚀 Return on Equity: 21.77%

Dividend Overview

Northrim currently offers a 2.51% dividend yield based on an annual payout of $0.64 per share, distributed at $0.16 per quarter. While the yield sits below the company’s historical averages, that compression reflects meaningful price appreciation from the stock’s 52-week low of $16.18 rather than any reduction in the dividend itself. The income stream remains intact and growing.

One of the most encouraging characteristics of NRIM’s dividend profile is the exceptionally low payout ratio of 22.30%. With EPS of $2.87 and an annual dividend of just $0.64, the company is retaining the vast majority of its earnings, which provides a wide buffer against any earnings pressure and leaves ample capacity for continued dividend increases.

The company’s dividend history reflects a clear and consistent commitment to returning capital to shareholders. Quarterly payments have risen from $0.15 in early 2023 to $0.16 today, representing a measured but dependable upward trajectory that income investors can rely on.

Dividend Growth and Safety

Dividend reliability isn’t just about the current yield, it’s about sustainability and growth. Reviewing NRIM’s recent dividend history tells an encouraging story. The quarterly payment held steady at $0.15 throughout all of 2023, then stepped up to $0.1525 in the first half of 2024, moved again to $0.155 in the second half of 2024, and reached $0.16 for all four quarters of 2025. That progression reflects disciplined, incremental growth rather than headline-grabbing jumps that can later be reversed.

The safety of the dividend is underscored by a payout ratio of just 22.30%, which is among the more conservative in the regional banking sector. Even if earnings were to decline meaningfully from today’s levels, the dividend would be well covered. Return on equity of 21.77% and return on assets of 2.04% both indicate that Northrim is generating strong profits relative to its asset base, which is the foundation of a sustainable income program.

Profit margins of 30.93% and net income of $64.6 million on revenue of $208.9 million further reinforce the picture of a well-run bank with genuine earnings power behind its dividend commitments. Cash flow data is not available at this time, so investors should monitor future disclosures to confirm that operating cash generation continues to support the payout.

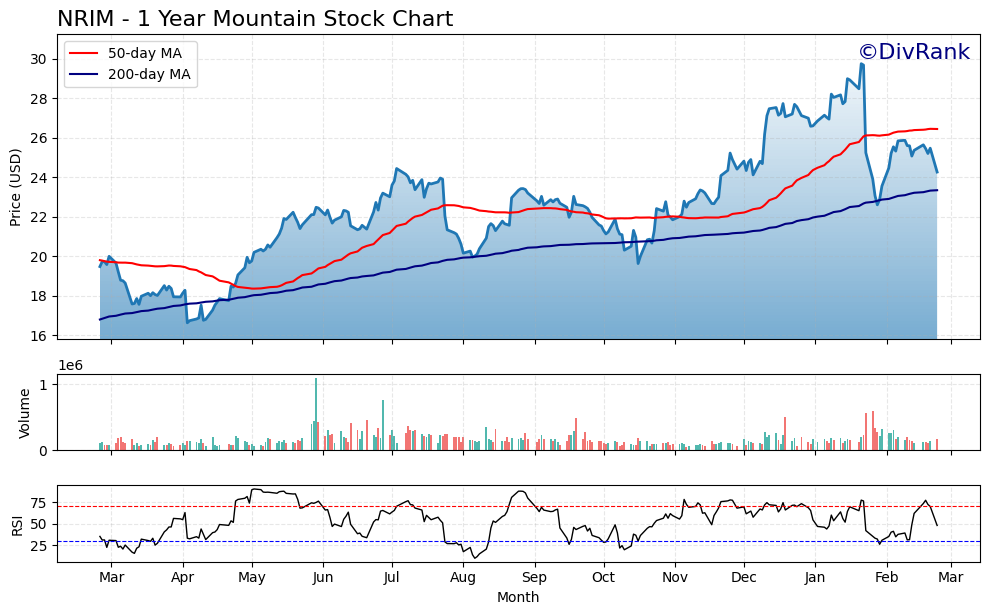

Chart Analysis

NRIM has traced an impressive recovery arc over the past year, climbing from a 52-week low of $16.63 to a peak of $29.76 before pulling back to its current price of $24.27. That low-to-high range represents a gain of nearly 79% at the peak, which speaks to how aggressively the market repriced shares during the recovery phase. The current price sits roughly 18.5% below that 52-week high, suggesting the stock has given back a meaningful portion of its gains in recent months, though it remains well above the lows that defined the trough of the prior cycle.

The moving average picture tells a constructive story for longer-term trend followers. NRIM is trading above its 200-day moving average of $23.35, which confirms the broader uptrend remains technically intact. The 50-day moving average at $26.45 has crossed above the 200-day, producing what technicians call a golden cross, a configuration historically associated with sustained bullish momentum. However, the current price of $24.27 is sitting below that 50-day moving average, which means the stock is in a near-term digestion phase after its strong run. For dividend investors, this setup often represents a more attractive entry window than chasing prices when they are stretched above both averages simultaneously.

The RSI reading of 47.95 places NRIM in essentially neutral territory, neither overbought nor oversold. This is a reasonably healthy reading for a stock that has already experienced a sharp recovery, as it indicates sellers have not abandoned the name but buyers are also not showing signs of panic exhaustion. Momentum is in a holding pattern, which is consistent with the price action of trading between the two key moving averages. There is room for the RSI to move in either direction without hitting extreme readings, giving the stock flexibility to respond to the next material catalyst.

For dividend investors, the technical backdrop is modestly encouraging without being a strong directional signal in either direction. The golden cross and the position above the 200-day moving average suggest the structural trend has not broken down, and the neutral RSI means new buyers are not walking into an overheated situation. The more meaningful consideration is whether the current price near $24.27 provides an attractive enough entry point relative to the dividend yield and the company’s income fundamentals, rather than trying to time a precise technical breakout from here.

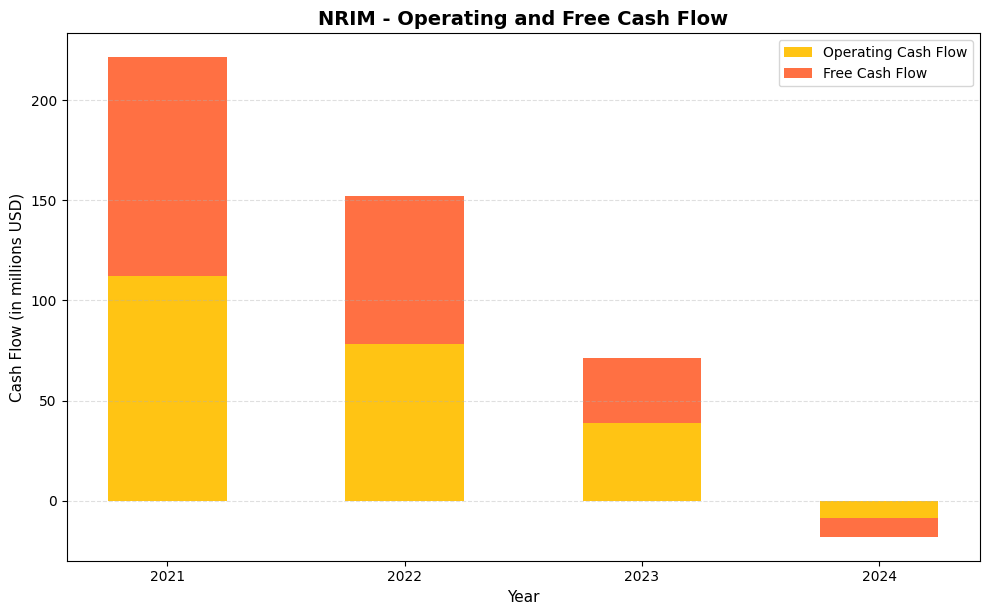

Cash Flow Statement

Northrim BanCorp’s cash flow trajectory over the past four years tells a story that demands attention from income investors. Operating cash flow declined from $112.0M in 2021 to $78.1M in 2022, then dropped more sharply to $38.8M in 2023, before turning negative at $-8.7M in 2024. Free cash flow followed the same arc, moving from a healthy $109.5M in 2021 down to $74.3M, then $32.6M, and finally $-9.3M in 2024. Negative free cash flow in the most recent year means the company is not generating enough internal cash to cover its operational needs and capital expenditures, which raises legitimate questions about near-term dividend sustainability if this trend persists into 2025.

The scale of the deterioration is what gives pause. Over just three years, NRIM went from generating over $100M in operating cash flow to a net cash outflow position, a swing of more than $120M that reflects a combination of margin compression, balance sheet pressures common to regional banks in a higher-rate environment, and shifting deposit dynamics. Capital efficiency, which looked exceptional in 2021 when free cash flow conversion was nearly 98% of operating cash flow, has remained relatively consistent in terms of the gap between operating and free cash flow, suggesting the issue is on the operating side rather than runaway capital spending. For dividend investors, the 2024 figures are a signal to monitor closely rather than a reason to panic outright, as regional bank cash flows can recover meaningfully when rate cycles turn and loan demand stabilizes, but the current numbers leave little margin for error if NRIM intends to maintain or grow its payout.

Analyst Ratings

Analyst coverage of NRIM is limited to two firms, but the consensus is a strong buy with a mean price target of $31.00. Both the low and high targets sit at the same $31.00 level, indicating full agreement among the analysts following the stock. At a current price of $24.27, that target implies upside of approximately 27.7% from today’s levels, a meaningful potential return that complements the dividend income.

Analysts covering Northrim have pointed to the bank’s strong earnings profile, disciplined cost management, and favorable positioning within the Alaska economy as key reasons for their constructive view. The company’s return on equity of 21.77% stands well above the regional banking average, and analysts appear to believe the market has not yet fully reflected that profitability in the stock price.

With only two analysts on record, investors should weigh the consensus price target in that context. The absence of dissenting voices is partly a function of limited coverage rather than universal agreement, and any new analyst initiations could shift the range. That said, the existing targets are consistent and point firmly to the upside from current levels.

Earning Report Summary

Northrim BanCorp delivered strong full-year results that reflect both the quality of its franchise and the favorable operating environment it has navigated. With net income of $64.6 million and EPS of $2.87, the bank generated meaningful profitability on total revenue of $208.9 million. A profit margin of 30.93% places Northrim comfortably above many of its regional banking peers on an earnings efficiency basis.

Profitability and Returns

The headline return figures are impressive by any measure in regional banking. Return on equity of 21.77% indicates that Northrim is generating strong earnings relative to its book value, and return on assets of 2.04% reflects efficient deployment of its balance sheet. These metrics suggest that management has maintained disciplined lending standards while capturing revenue opportunities in its home market.

Balance Sheet Context

Book value per share stands at $14.77, against which the stock trades at a price-to-book ratio of 1.64. While that premium to book is higher than some deep-value regional bank investors might prefer, it is justified by the exceptional return on equity the bank is generating. A bank earning 21.77% on equity deserves to trade above book, and the current multiple appears reasonable given that earnings power.

Earnings Per Share

EPS of $2.87 covers the $0.64 annual dividend more than four times over, which reinforces the safety analysis presented in the dividend section. The low payout ratio of 22.30% is a direct function of that earnings strength, and it provides management with flexibility to either accelerate dividend growth or deploy capital into loan growth and other strategic priorities.

Management’s Take

Leadership has consistently emphasized Northrim’s role as a community-focused institution serving the Alaskan economy, and the financial results reflect the strength of that positioning. The bank’s ability to generate above-average returns on equity while maintaining conservative payout discipline suggests that management is prioritizing long-term shareholder value over short-term income optics.

Valuation and Stock Performance

NRIM currently trades at $24.27 per share, sitting in the lower half of its 52-week range of $16.18 to $30.82. The stock has recovered substantially from its 52-week low but remains well below its peak, which may present an attractive entry point for investors who follow the analyst consensus price target of $31.00.

From a valuation standpoint, the stock trades at a trailing P/E of 8.46, which is genuinely inexpensive for a bank producing a 21.77% return on equity. The price-to-book ratio of 1.64 is slightly elevated relative to some discount-oriented regional bank investors’ preferences, but as noted above, the return on equity justifies a premium to book value. A bank generating more than 20% on its equity should not trade at the same multiple as one generating 8% or 10%.

The market cap of approximately $537 million reflects a small-cap institution, which means liquidity and coverage will differ from money-center banks, but it also means there is more room for re-rating as earnings quality becomes more widely recognized. With short interest of 366,914 shares, there is no unusual bearish pressure on the stock at current levels. The beta of 0.94 suggests NRIM trades with slightly less volatility than the broader market, which is consistent with its stable business model and conservative financial management.

Risks and Considerations

As a bank operating primarily in Alaska, Northrim’s fortunes are closely tied to the economic conditions of a single state. Alaska’s economy is influenced by oil prices, federal spending, tourism, and fishing, any of which can experience significant volatility. A sustained regional downturn could pressure loan growth, increase credit losses, and weigh on the earnings that support the dividend.

Like all banks, NRIM is sensitive to interest rate movements. The favorable rate environment of recent years has supported strong net interest margins, but any meaningful decline in rates engineered by the Federal Reserve could compress those margins and reduce earnings power. Management has demonstrated skill in navigating rate cycles, but the risk is real and warrants ongoing attention.

Operating cash flow data is not currently available, which limits the ability to independently verify dividend sustainability from a cash generation perspective. Investors should monitor future filings to confirm that reported net income is translating into genuine cash available for distribution. This is a disclosure gap rather than a confirmed problem, but it is worth flagging for thorough due diligence.

Analyst coverage is limited to two firms, both converging on a $31.00 price target. While that consensus is constructive, the narrow coverage base means there is less information diversity than investors in more widely followed stocks enjoy. New coverage initiations, particularly those with differing views, could introduce price volatility that the current consensus does not anticipate.

The stock’s 52-week range of $16.18 to $30.82 reflects meaningful price swings even within a single year. Investors purchasing at current levels should be prepared for continued volatility, particularly given the small-cap profile of the company and the sensitivity of regional bank stocks to broader financial sector sentiment.

Final Thoughts

For investors focused on dividend income and long-term value, Northrim BanCorp presents a compelling combination of earnings quality, dividend discipline, and valuation appeal. The payout ratio of just 22.30%, return on equity of 21.77%, and a consistent pattern of annual dividend increases all point to a management team that takes its income obligations seriously while building the underlying business.

At $24.27 per share, the stock trades at a trailing P/E of 8.46 and sits roughly 21% below the analyst consensus price target of $31.00. For a bank generating the kind of returns on equity that Northrim is producing, that valuation looks genuinely attractive rather than a value trap.

Overall, NRIM is a solid Alaska-focused regional bank with a growing dividend, a conservative payout structure, and the financial strength to support continued shareholder returns. For those looking to add a dependable dividend grower with meaningful upside potential to their portfolio, it remains a name worth serious consideration.