Updated 2/24/26

Lindsay Corporation (LNN) has built a strong foundation in agricultural irrigation and infrastructure, supported by more than six decades of operational history. With a presence in both domestic and international markets, the company continues to expand its footprint through disciplined financial management, strong leadership, and a growing portfolio of infrastructure projects and irrigation systems.

Recent results reflect a business that continues to generate meaningful free cash flow and maintain conservative financial discipline. Backed by a low payout ratio, a consistent dividend policy, and a leadership team focused on long-term strategy, Lindsay presents a compelling profile for income-focused investors looking for dependable fundamentals and steady operational performance.

Recent Events

Lindsay Corporation has continued to execute across both its irrigation and infrastructure segments over the trailing twelve months, generating $665.9 million in revenue and $73.4 million in net income. While those figures represent a modest step back from the exceptional year-over-year growth seen in fiscal 2025, they still reflect a business operating at a solid level of profitability. EPS came in at $6.75, and the profit margin held at 11.02%, underscoring the company’s ability to manage costs in a more normalized demand environment.

The international irrigation segment continues to play an important role in diversifying revenue away from the more cyclical North American market. Infrastructure activity, while lumpy by nature given its project-driven character, remains a meaningful contributor to overall margins. Lindsay’s operating model is built around disciplined pricing and operational efficiency, and that approach continues to support results even when individual segments face headwinds.

The cash picture remains one of the most attractive aspects for income investors. Operating cash flow reached $110.7 million over the trailing twelve months, and free cash flow came in at $52.2 million. The company is consistently converting earnings into usable cash, which is the clearest measure of dividend sustainability and financial flexibility.

Lindsay’s return on equity stands at 14.59% and return on assets at 6.75%, both reasonable figures for a capital-intensive industrial company. With a beta of just 0.80, the stock continues to trade with less volatility than the broader market, a characteristic that income investors who value stability tend to appreciate.

Key Dividend Metrics

💰 Forward Annual Dividend Rate: $1.48

📈 Forward Dividend Yield: 1.08%

🔄 Last Dividend Payment: $0.37

📉 Payout Ratio: 21.63%

🕐 5-Year Average Yield: ~1.03%

📆 Last Ex-Dividend Date: February 13, 2026

⏳ Price/Book: 2.77

Dividend Overview

If you’re chasing high-yield dividend plays, Lindsay’s 1.08% yield might seem underwhelming at first glance. But it’s important to see the bigger picture. This yield is backed by a very low payout ratio and a well-run company that has demonstrated the ability to grow its dividend steadily over time. The dividend is clearly sustainable, supported by a business model that prioritizes consistent cash generation over aggressive expansion or financial risk-taking.

At 21.63%, the payout ratio gives Lindsay considerable flexibility. The company is using only a small fraction of its earnings to fund the dividend, leaving the remainder available for reinvestment, capital expenditures, and further increases in shareholder returns over time. That measured approach reflects the kind of financial conservatism that long-term income investors tend to find reassuring.

There is also a long track record of uninterrupted dividend payments, and that consistency matters. Investors can count on those regular deposits without worrying about sudden cuts driven by economic cycles or short-term earnings volatility. Lindsay is not a speculative story; it is a reliable, steady compounder operating in essential end markets.

Dividend Growth and Safety

The dividend growth here is modest but consistent, and the direction has been clearly upward. Looking at the recent dividend history, Lindsay raised its quarterly payment from $0.34 in May 2023 to $0.35 in August 2023, held that level through early 2025, then bumped it again to $0.36 in August 2024, and most recently to $0.37 per quarter beginning in August 2025. That $0.37 quarterly rate, which equates to $1.48 annualized, represents a meaningful step up from where the dividend stood just two years ago. The increases reflect real business growth rather than a stretch for yield, which is exactly the kind of dividend behavior long-term investors want to see.

What makes the dividend especially safe is the strength of the company’s cash flow generation. Lindsay is producing $110.7 million in operating cash flow against an annual dividend commitment that is a fraction of that figure. Even after accounting for capital expenditures, there is more than enough free cash flow to cover the dividend with substantial room to spare. That coverage cushion is one of the most important factors in assessing whether a dividend is durable through difficult market conditions.

Earnings have been solid, and profitability metrics like return on equity at 14.59% and return on assets at 6.75% confirm that Lindsay is putting its capital to productive use. Those levels of return support the case for ongoing dividend payments and position the company to continue growing the payout in line with earnings over the coming years.

The stock’s beta of 0.80 reinforces the defensive character of this name. Lindsay tends to move with less intensity than the broader market, which aligns well with the priorities of income investors who prefer capital preservation alongside steady dividend income.

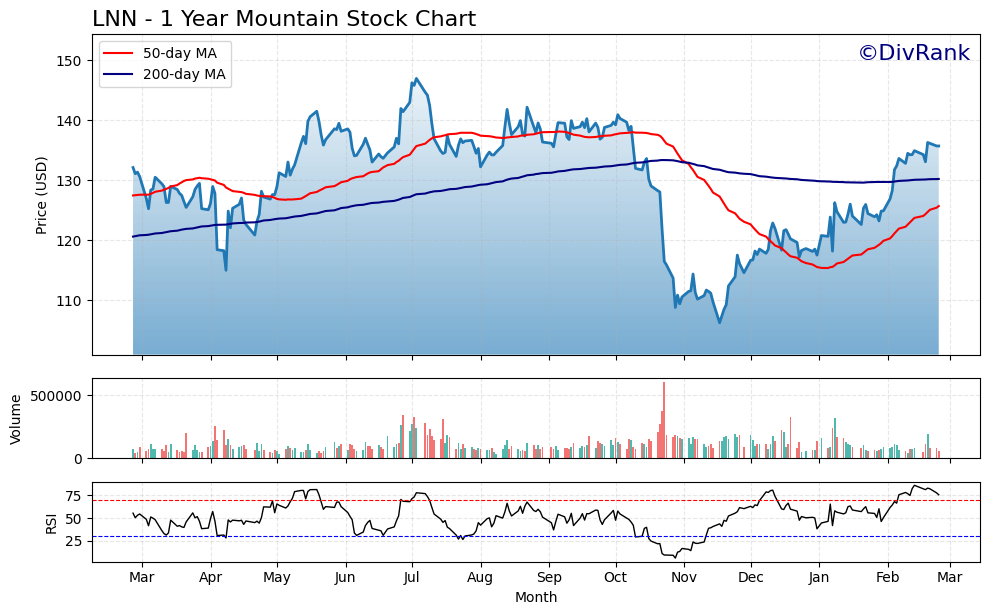

Chart Analysis

Lindsay Corporation has staged a meaningful recovery over the past year, climbing from a 52-week low of $106.28 to its current price of $135.74, a gain of roughly 27.7% off the trough. The stock reached a high of $147.01 during the trailing twelve months before pulling back modestly, and at the current level it sits about 7.7% below that peak. That combination of a strong recovery off the lows and a contained pullback from the highs suggests the underlying demand for shares has been reasonably durable, even as agricultural equipment sentiment has remained uneven across the sector.

The moving average picture tells a mixed but improving story. LNN is trading above both its 50-day moving average of $125.73 and its 200-day moving average of $130.25, which confirms that short and medium-term price momentum is currently constructive. However, the 50-day remains below the 200-day, a configuration technically referred to as a death cross, which signals that the broader trend has not yet fully recovered from the weakness earlier in the year. For dividend investors, the practical implication is that price momentum is recovering but the longer-term trend structure still requires confirmation before one can declare a clean technical uptrend is fully in place.

The RSI reading of 75.76 is the most immediate caution flag visible in the data. A reading above 70 places LNN in overbought territory by conventional standards, indicating that the recent price surge has been sharp enough to stretch near-term valuations relative to recent trading history. This does not mean a reversal is imminent, but it does suggest that new buyers entering at current levels are doing so after a significant run, and some consolidation or a modest pullback would not be unusual before the next leg higher.

For dividend-focused investors, the technical setup warrants patience rather than urgency. The recovery off the lows is encouraging, the stock is holding above both key moving averages, and the proximity to the 52-week high reflects genuine buying interest. The elevated RSI and the unresolved death cross configuration together argue for a measured approach, where waiting for either a pullback toward the $125 to $130 support zone or a confirmed 50-day cross above the 200-day would offer a more favorable risk-adjusted entry point for a stock held primarily for its income and long-term dividend growth credentials.

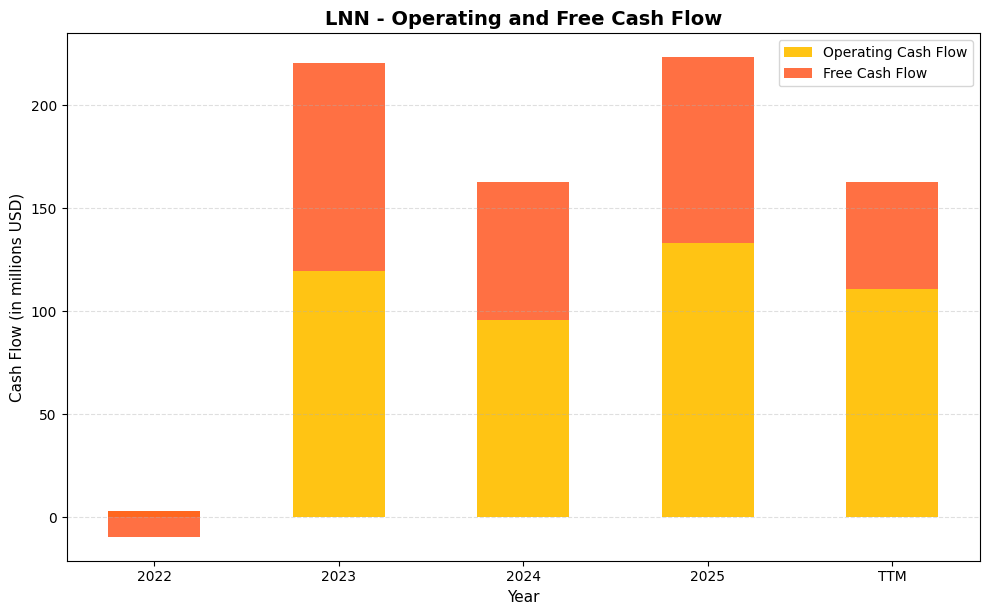

Cash Flow Statement

Lindsay Corporation’s cash generation profile has improved dramatically since the near-breakeven year of 2022, when operating cash flow registered just $3.0 million and free cash flow was negative at $12.5 million. The business has since demonstrated it can convert earnings into real cash at scale, with operating cash flow reaching $119.7 million in 2023, moderating to $95.8 million in 2024, and climbing back to $132.9 million in fiscal 2025. Free cash flow followed a similar arc, hitting $100.9 million in 2023 and settling at $66.8 million in 2024 before recovering to $90.4 million in 2025. The TTM figures of $110.7 million in operating cash flow and $52.2 million in free cash flow reflect some elevated capital spending pulling free cash flow below recent peaks, but the underlying generation remains more than sufficient to cover the current dividend obligation, which runs well under $20 million annually. That coverage margin gives management meaningful flexibility without putting income investors in an uncomfortable position.

The trajectory from 2022 to 2025 tells a story of a company that worked through a capital-intensive period and emerged with a much stronger cash profile. The 2022 trough appears tied to inventory builds and working capital demands that temporarily consumed cash, rather than any structural deterioration in the business model. Since then, Lindsay has demonstrated improving capital efficiency, consistently converting a healthy share of its operating cash flow into free cash flow available for dividends, share repurchases, and balance sheet management. The gap between operating and free cash flow has widened somewhat in the TTM period, signaling that reinvestment spending has picked up, which is not inherently a negative signal for a capital goods manufacturer investing in future capacity. For dividend growth investors, the core message is that Lindsay’s cash flows have normalized at a level that comfortably funds the dividend, and the consistency of that generation across the last three full fiscal years reinforces confidence in the payout’s durability.

Analyst Ratings

Analyst coverage of Lindsay Corporation remains relatively limited, with only two firms actively tracking the stock. The consensus price target mean sits at $134.00, with a low of $128.00 and a high of $140.00. With the stock currently trading at $135.74, Lindsay is sitting just above the average analyst price target, which implies that the sell-side sees limited near-term upside from current levels based on the midpoint estimate.

The high-end target of $140.00 does offer a modest premium to the current price, which suggests at least one analyst sees room for further appreciation if operational momentum continues or if infrastructure activity accelerates. The low-end target of $128.00, meanwhile, implies downside of roughly 5.7% from current levels, reflecting a more cautious view on near-term growth prospects given the moderation in earnings from fiscal 2025 peaks.

With no formal consensus rating available and only two analysts covering the name, LNN is a stock where independent fundamental analysis carries particular weight. The valuation and dividend metrics tell a coherent story of a conservatively run, cash-generative industrial business, and the narrow analyst coverage means the market is not over-scrutinizing every quarterly move. For patient income investors, that combination can be an advantage.

Earning Report Summary

Solid Profitability in a Normalized Environment

Lindsay Corporation’s trailing twelve-month results reflect a business that has settled into a more normalized operating rhythm following the exceptional growth reported in fiscal 2025. Revenue for the period came in at $665.9 million, and net income reached $73.4 million, producing EPS of $6.75. While those figures represent a step back from the $7.03 EPS and rapid revenue growth seen in the prior year, they still reflect a highly profitable business with a durable earnings base.

The profit margin of 11.02% shows the company is managing its cost structure effectively, even as the top line growth rate has moderated. Operating cash flow of $110.7 million confirms that earnings quality remains high, and the 21.63% payout ratio leaves the dividend on very solid footing regardless of near-term demand fluctuations.

Irrigation Navigating a Softer Domestic Cycle

The North American irrigation market has faced headwinds from softer farm income and cautious grower spending, a trend that has weighed on domestic equipment demand for several quarters. International irrigation, however, continues to serve as a meaningful offset, with project activity in regions like the Middle East, Africa, and other emerging markets providing volume that the North American market has not fully supplied. This geographic diversification has been an important structural feature in Lindsay’s ability to maintain revenue and margin resilience through the current agricultural cycle.

Infrastructure Provides Earnings Stability

The infrastructure segment continues to serve as a valuable complement to the irrigation business, contributing margin support and project-driven revenue that can meaningfully move the needle in a given quarter. While infrastructure results can be lumpy due to the timing of large Road Zipper System contracts and other project completions, the segment has established itself as a genuine contributor to overall company performance rather than a secondary consideration. Management’s ongoing investment in the infrastructure pipeline positions Lindsay to capture future project opportunities as they materialize.

Comments from Leadership

CEO Randy Wood has continued to emphasize the company’s focus on global irrigation demand and infrastructure project execution. While acknowledging that the domestic agricultural market faces near-term headwinds from commodity price pressures and farm income variability, Wood has pointed to international growth opportunities and the infrastructure segment’s project pipeline as key drivers of future performance.

Management’s commentary has also addressed the ongoing challenge of tariff-related input costs and supply chain management, areas where Lindsay has been working to refine its sourcing and operational strategies. The overarching message from leadership is one of disciplined execution and a long-term orientation, consistent with the company’s track record of conservative capital management and steady dividend growth.

Management Team

Lindsay Corporation is guided by a steady and experienced leadership group, with Randy Wood serving as President and CEO since January 2021. Under his leadership, the company has sharpened its focus on operational excellence and international expansion. Wood brings a clear sense of direction, emphasizing growth in both the irrigation and infrastructure segments while keeping financial discipline front and center.

The executive bench includes Brian Ketcham as Chief Financial Officer, who plays a key role in maintaining fiscal health and driving shareholder value. Scott Marion heads up the infrastructure segment and has been instrumental in executing on some of the company’s largest projects. The broader leadership team also includes senior professionals overseeing legal, technology, and operations, creating a well-rounded group that is capable of adapting to challenges while staying focused on long-term goals.

Valuation and Stock Performance

Lindsay’s stock is currently trading at $135.74, sitting in the middle portion of its 52-week range of $106.10 to $150.96. The stock has pulled back from its 52-week high of nearly $151, which brings the current price into a more interesting range for income investors evaluating entry points. The market cap stands at approximately $1.44 billion, reflecting a focused mid-cap profile that balances operational scale with the agility of a niche industrial leader.

Valuation metrics are reasonable for a company of Lindsay’s quality. The trailing P/E ratio of 20.11 reflects a modest premium to industrial sector averages but is well supported by the company’s cash generation and conservative balance sheet. The price-to-book ratio of 2.77 and book value per share of $48.92 indicate the stock is priced at a reasonable multiple of its tangible asset base. The beta of 0.80 continues to reflect the stock’s relatively steady behavior compared to broader market swings, a characteristic that income investors seeking defensive positioning tend to value.

With the stock trading essentially at the analyst consensus price target of $134.00, the near-term upside may be limited based on current sell-side estimates. However, for long-term investors focused on dividend growth and capital preservation rather than short-term price appreciation, the current valuation does not appear stretched relative to the company’s earnings power and cash flow profile.

Risks and Considerations

Despite a solid foundation, there are risks that could challenge Lindsay’s trajectory. The company’s agricultural business is sensitive to factors that are often unpredictable, including weather patterns, commodity prices, and changes in farm income. Those variables can directly influence irrigation equipment demand, particularly in North America, and a sustained downturn in farm economics could pressure revenue and earnings more meaningfully than the current modest softness suggests.

The infrastructure segment, while performing well on a relative basis, is still somewhat dependent on the timing and availability of public sector project funding. Delays in government approvals or shifts in infrastructure spending priorities could affect revenue recognition in a given fiscal year. The project-driven nature of this segment introduces an element of lumpiness that can make period-to-period comparisons difficult to interpret.

Foreign exchange exposure remains a genuine consideration given Lindsay’s international revenue base. Currency movements can affect both the reported value of international sales and the competitiveness of Lindsay’s equipment in certain markets. Additionally, ongoing tariff uncertainty and input cost variability introduce margin risk that management must actively manage through pricing discipline and supply chain optimization. While Lindsay has historically navigated these challenges effectively, they remain variables that income investors should monitor alongside the dividend and earnings trajectory.

Final Thoughts

Lindsay Corporation stands out as a disciplined, well-run company with a strong balance between operational focus and financial prudence. Its consistent cash flow generation, low payout ratio, and steady dividend growth history make it a reliable name for income investors who prioritize safety and compounding over headline yield. The recent dividend increase to $0.37 per quarter, representing $1.48 annualized, is a tangible sign that management is continuing to reward shareholders in line with the business’s earnings power.

While the stock appears fairly valued relative to the current analyst consensus target, the longer-term case rests on Lindsay’s ability to sustain cash generation through agricultural cycles, execute on international irrigation growth, and capture infrastructure project opportunities as they emerge. Investors looking for exposure to agricultural and infrastructure markets with a low-beta, dividend-growth profile may find Lindsay to be a steady, well-managed name worth holding for the long term.