Updated 2/24/26

Landmark Bancorp, Inc. is a regional bank based in Kansas with a long-standing reputation for consistent financial performance and shareholder returns. The company has continued to build on its operational momentum, posting full-year net income of $18.8 million and earnings per share of $3.22, supported by disciplined lending and improving profitability metrics. Its leadership team, under CEO Abby Wendel, continues to prioritize smart expansion, cost control, and customer-focused service.

Recent Events

Landmark’s share price has held up well in the current environment, trading at $27.40 and sitting comfortably within its 52-week range of $21.31 to $29.56. After a strong run that brought the stock near its highs, the price has pulled back modestly from that $29.56 peak, offering income investors a slightly more attractive entry point than was available at the top.

The financial results underlying that price performance remain compelling. Revenue came in at $68.3 million, and the bank’s profit margin reached 27.50%, reflecting continued discipline on the cost side. Return on equity improved to 12.65%, a meaningful step up from the 11% range reported in prior periods, and return on assets held steady at 1.18%, both of which are solid benchmarks for a community bank of this size.

The most noteworthy recent development from a dividend perspective is the February 2026 quarterly payment, which came in at $0.21 per share. This marks a step up from the $0.20 quarterly rate that was in place throughout 2025, continuing Landmark’s pattern of measured, incremental dividend increases that reward long-term shareholders without stretching the payout structure.

With a market cap of approximately $166.4 million, Landmark remains a small-cap name, but its consistent execution and improving profitability have kept investor interest steady. The low short interest of just 111,300 shares suggests there is little bearish pressure on the stock at current levels.

Key Dividend Metrics

📈 Dividend Yield: 2.97% (Forward)

💵 Annual Dividend: $0.81

📊 Payout Ratio: 24.82%

🧱 5-Year Average Yield: 3.49%

📅 Last Dividend Payment: February 12, 2026 ($0.21/share)

🔁 Price/Book: 1.04

📉 Beta: 0.28 (Low volatility)

Dividend Overview

Landmark’s forward dividend yield of 2.97% sits just under the 3% threshold, which may not turn heads at first glance, but the context makes the income story considerably more interesting. That yield is underpinned by a payout ratio of just 24.82%, meaning the bank is distributing less than a quarter of its earnings as dividends. For income investors, that kind of cushion is reassuring.

With earnings per share at $3.22 and an annualized dividend running at $0.81, the coverage ratio is strong. There is no sign of strain in the payout whatsoever, and the recent increase to $0.21 per quarter confirms that management views the dividend not as a static obligation but as a reflection of improving earnings power. The bank is growing into a higher payout, not being stretched toward one.

The five-year average yield of 3.49% tells a useful story about where the stock has come from. The current yield compression relative to that average is a direct result of price appreciation, which means long-term holders are enjoying both capital gains and a strong yield on cost. Newer investors are picking up a yield that, while below the historical average, is supported by much stronger underlying earnings than the bank was generating several years ago.

The dividend history reflects a deliberate and consistent approach to income returns. Landmark moved its quarterly payout from $0.1814 through 2023, then stepped it up to $0.1905 in early 2024, followed by a move to $0.20 in early 2025, and now to $0.21 in February 2026. Each increment is modest, but the direction is clear and the pattern is reliable, which is exactly what dividend growth investors value in a community bank name.

Dividend Growth and Safety

The safety profile of Landmark’s dividend is one of the strongest features of this investment case. A payout ratio of 24.82% is exceptionally conservative, leaving the bank with substantial retained earnings to fund loan growth, absorb credit costs, or continue building book value without ever putting the dividend at risk.

The improvement in return on equity to 12.65% is a particularly encouraging sign. A year ago that figure was running closer to 11%, and the upward trend indicates that the bank is not only maintaining its discipline but actually improving the productivity of shareholder capital. Return on assets at 1.18% also reflects sound asset quality management and efficient deployment of the balance sheet.

Book value per share of $26.44 compared to a current price of $27.40 means the stock is trading at just 1.04 times book, which provides a fundamental floor that many other financials lack at current valuations. For dividend investors, book value support reduces the risk of permanent capital loss even in a more difficult rate environment.

The beta of 0.28 reinforces the low-volatility character of this stock. Landmark does not swing dramatically with broader market sentiment, which suits income-oriented investors who prioritize consistency over excitement. Dividend growth has been steady rather than aggressive, but the trajectory, moving from $0.1814 per quarter just a few years ago to $0.21 today, demonstrates a genuine commitment to increasing shareholder income over time.

What makes the growth story credible going forward is the combination of a conservative payout ratio and improving earnings. If EPS continues to expand, Landmark has significant room to increase the dividend without approaching any level of financial stress. That optionality is a meaningful safety net, and it distinguishes this bank from peers that are already paying out a much higher fraction of earnings to sustain their yields.

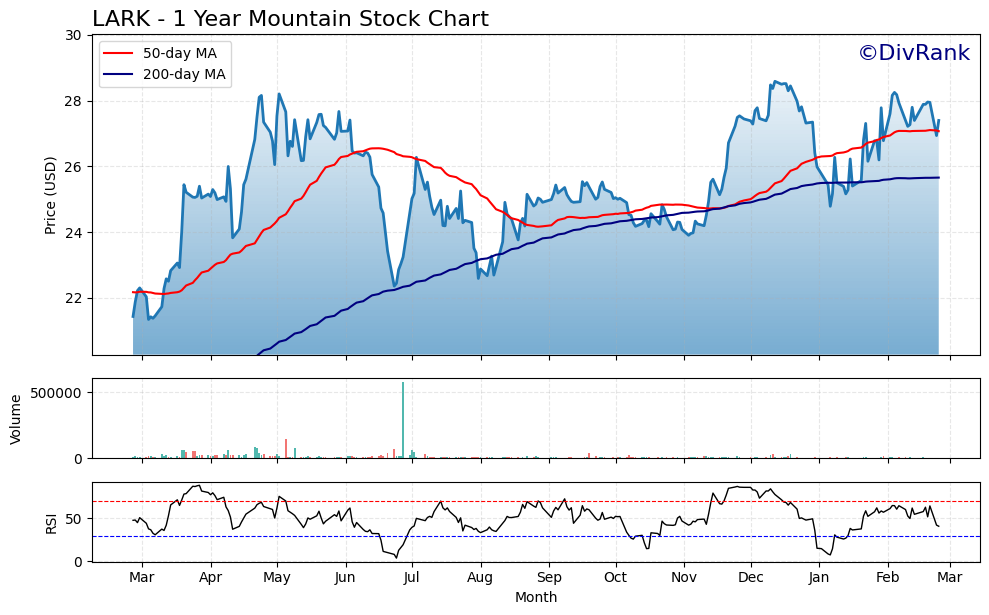

Chart Analysis

LARK has staged a meaningful recovery over the past year, climbing roughly 28% off its 52-week low of $21.34 to trade near $27.40 at the time of this writing. That kind of sustained move off a trough reflects genuine buying interest rather than a short-lived bounce, and the stock now sits within striking distance of its 52-week high of $28.59, just 4.16% below that level. For a community bank name that rarely attracts speculative momentum, this steady upward grind is an encouraging sign that the market is gradually repricing the shares toward fairer value.

The moving average picture reinforces that constructive view. LARK is trading above both its 50-day moving average of $27.07 and its 200-day moving average of $25.66, and the 50-day has crossed above the 200-day to form what technicians call a golden cross. That configuration typically signals that intermediate-term momentum has aligned with the longer-term trend, which is precisely the setup dividend investors prefer to see when building or adding to a position. The spread between the two averages is still relatively narrow, suggesting this is an early-stage bullish alignment rather than an overextended one.

The RSI reading of 40.79 adds an interesting wrinkle to the picture. That level sits in the lower half of the neutral range, well clear of overbought territory and edging toward the oversold threshold without quite reaching it. In practical terms, this tells us that the recent price action has cooled enough to wash out near-term froth, yet the stock has not been subjected to the kind of panic selling that would push the indicator below 30. For income-focused investors, a moderately soft RSI combined with a golden cross setup is often a favorable entry condition, as it suggests shares are consolidating rather than deteriorating.

Taken together, the technical profile for LARK leans modestly constructive for dividend investors. The trend is up, the moving averages are aligned bullishly, and momentum has pulled back to a level that does not imply excessive risk of buying at a near-term peak. With the stock only about 4% below its 52-week high, there is limited runway before LARK would be testing breakout territory, so investors watching this name for an entry may want to monitor whether the shares can consolidate above the $27 level before making a commitment. The charts alone do not make a dividend thesis, but they are certainly not working against one here.

Cash Flow Statement

Landmark Bancorp’s cash flow profile has compressed meaningfully since 2021, and that trajectory deserves close attention from income investors. Operating cash flow peaked at $31.2 million in 2021 before sliding to $24.8 million in 2022, then dropping sharply to $12.6 million in 2023. The partial recovery to $14.2 million in 2024 is encouraging, but it still represents less than half the operating cash generation the company produced just three years ago. Free cash flow has tracked nearly in lockstep, moving from $29.8 million in 2021 to $11.9 million in 2024, which tells you that capital expenditures are not the problem here. The business is simply generating less cash from operations, and that reality tightens the margin of safety around the dividend in a way that warrants ongoing monitoring.

The capital efficiency picture is actually one of the cleaner aspects of this story. The gap between operating and free cash flow has remained narrow throughout the entire period, never wider than $1.4 million in any given year, which confirms that LARK is not consuming meaningful capital to sustain its operations. The concern is squarely on the cash generation side rather than the capital allocation side. The 2023 trough appears to coincide with the broader pressure on community bank earnings from the rate cycle and deposit cost increases, and the modest 2024 improvement suggests the bottom may be in. For dividend investors, the key question going forward is whether operating cash flow can rebuild toward the $20 million range, because at current levels the dividend coverage is serviceable but leaves little room for error if earnings come under renewed pressure.

Analyst Ratings

Landmark Bancorp does not currently carry a formal analyst consensus rating, and no recent analyst actions have been published for LARK. This is not unusual for a small-cap community bank with a market cap of approximately $166 million, as institutional coverage of banks in this size range tends to be limited. The absence of a price target does not diminish the investment case, but it does mean that investors need to rely on fundamental analysis rather than Wall Street guidance when evaluating the stock.

Looking at the valuation metrics in place, the stock’s current P/E of 8.51 is modest by almost any measure, and with the price at $27.40 against book value of $26.44, the market is assigning only a marginal premium to a bank that is generating 12.65% return on equity. That combination of low P/E and near-book pricing suggests the stock is not priced for growth expectations, which can be an advantage for income investors looking for a margin of safety.

With short interest of just 111,300 shares, there is no meaningful bearish positioning against LARK at this time. The stock is trading well within its 52-week range, and the recent dividend increase to $0.21 per quarter sends a constructive signal about management’s confidence in current and near-term earnings. For a stock without active analyst coverage, the internal signals from the company itself become the most meaningful indicators of sentiment.

Earning Report Summary

Landmark Bancorp delivered a strong full-year result, with net income of $18.8 million and earnings per share of $3.22 representing a meaningful improvement over prior periods. The bank’s profit margin of 27.50% reflects a business that has successfully expanded revenues while maintaining control over its cost structure, a combination that has been central to the improved profitability narrative at Landmark over the past several quarters.

Growth Where It Matters

Total revenue reached $68.3 million, and the improvement in return on equity to 12.65% confirms that earnings growth has translated into better utilization of shareholder capital. Return on assets at 1.18% is a healthy benchmark for a community bank, indicating that Landmark is generating solid income relative to its balance sheet size without taking on excessive risk. These figures collectively paint a picture of a bank that is operating with more efficiency than it was a year ago.

The improvement in profitability has been accompanied by the bank’s continued focus on its core regional markets in Kansas, where loan demand in commercial real estate and residential lending has supported balance sheet growth. Management’s emphasis on disciplined underwriting standards has helped keep credit quality stable even as the loan book has expanded.

Keeping Costs in Check

The 27.50% profit margin is a notable achievement for a bank of Landmark’s size, and it reflects the cumulative benefit of prior efficiency initiatives, including branch consolidation moves that reduced noninterest expenses in earlier periods. That operational discipline appears to have become embedded in how the bank manages its cost base, rather than being a one-time benefit.

With a P/E ratio of 8.51 against EPS of $3.22, the market is valuing these earnings quite conservatively. If credit conditions remain stable and the interest rate environment continues to support net interest margins, there is a reasonable case that earnings can be sustained or modestly expanded, which would further reduce the payout ratio and create additional room for dividend growth.

Strong Capital and Steady Payouts

Book value per share stands at $26.44, and the stock is trading at just 1.04 times that figure, which is a tight premium that reflects both the bank’s financial health and the market’s measured approach to small-cap regional bank valuations. Shareholder equity remains a solid foundation for the bank’s operations and supports its capacity to continue growing the dividend incrementally.

The February 2026 dividend of $0.21 per share marked the most recent step up in Landmark’s quarterly payout, continuing the pattern of annual increases that has characterized the bank’s dividend program. At an annualized rate of $0.81, the dividend represents a modest but growing claim on earnings that is clearly well within the bank’s capacity to sustain.

Looking Ahead

Abby Wendel’s leadership continues to set a tone of disciplined growth and operational focus. With efficiency improvements already reflected in the margin profile and credit quality appearing stable, the outlook for continued solid performance rests on the trajectory of interest rates and the health of Landmark’s Kansas regional markets. Both factors bear watching, but the bank enters the current period from a position of genuine financial strength.

The full-year results did not need to be dramatic to make a strong impression. Consistent earnings, improving returns, and a conservative balance sheet continue to be the core of Landmark’s investment story, and the numbers behind that story remain firmly intact.

Management Team

Landmark Bancorp is led by a management team that combines fresh strategic perspective with deep institutional experience. At the helm is Abby M. Wendel, who became President and CEO in March 2024. Her background in consumer banking and strategy at UMB Bank gave her a strong foundation in both growth execution and operational efficiency, and her tenure at Landmark has already shown results in the form of improved margins and a more focused cost discipline across the organization.

Mark A. Herpich, Executive Vice President, Secretary, and Chief Financial Officer, has been with Landmark since 2001 and provides the continuity and institutional knowledge that complements Wendel’s forward-looking orientation. His command of the bank’s financial structure, risk management frameworks, and regulatory relationships gives the leadership team a stable and experienced financial backbone. Together, Wendel and Herpich represent a pairing of vision and experience that has proven effective in navigating the bank through a demanding period for regional financial institutions.

Valuation and Stock Performance

Landmark Bancorp’s stock is currently trading at $27.40, sitting roughly in the middle of its 52-week range of $21.31 to $29.56. The stock has pulled back modestly from its annual high, which actually improves the income and valuation picture relative to where investors who chased the peak would have entered. The current price represents a more balanced risk-reward setup than was available at the top of the range.

The trailing P/E of 8.51 is notably lower than the 11-plus multiple the stock carried in earlier periods, which reflects both the earnings growth that has occurred and a more measured market rerating. At these levels, Landmark looks genuinely inexpensive relative to its earnings power. The price-to-book of 1.04 is essentially at par with book value, a valuation that provides a meaningful floor and suggests the stock is not pricing in much optimism about future growth, even though the bank’s operational trajectory has been consistently positive.

The market cap of approximately $166.4 million keeps Landmark firmly in small-cap territory, which limits institutional participation but also means the stock has not been bid up by momentum-driven flows. A beta of 0.28 confirms the low-volatility character that makes LARK suitable for income-focused portfolios where capital preservation is as important as yield. For investors who want steady appreciation alongside a growing dividend, the current entry point looks more compelling than it has for much of the past year.

Risks and Considerations

Landmark’s geographic concentration in Kansas remains the most fundamental risk in the investment thesis. As a regional bank whose business is closely tied to local economic conditions, any meaningful slowdown in Kansas’s economy, whether driven by agricultural stress, commercial real estate softening, or broader regional employment trends, could weigh on both loan growth and credit quality simultaneously. This concentration risk is a structural feature of community banking that does not disappear regardless of how well management executes.

Interest rate sensitivity continues to be a factor worth monitoring. Landmark has navigated the recent rate environment effectively, with improving net interest margins reflected in the stronger profitability metrics, but any shift in Federal Reserve policy or competitive pressure on deposit pricing could compress margins in future periods. Banks of Landmark’s size often have less flexibility than larger institutions when it comes to repricing liabilities quickly, which makes the rate environment a persistent variable in the earnings outlook.

Credit quality has held up well, but the broader economic backdrop for regional banks warrants continued attention. If commercial real estate valuations soften or small business borrowers come under stress, provisioning requirements could increase and put pressure on net income. Even with the current low payout ratio providing a buffer, a sustained deterioration in credit quality would eventually affect earnings and the pace of dividend growth.

The limited analyst coverage of LARK means that price discovery relies heavily on fundamental investors and insiders rather than a broad institutional following. While the low short interest is a positive signal, the lack of coverage also means that material developments at the company may take longer to be reflected in the stock price than would be the case for a more widely followed name. Investors should be prepared for periods of low trading volume and potential pricing inefficiency in either direction.

Final Thoughts

Landmark Bancorp continues to demonstrate the qualities that make it an appealing holding for dividend growth investors with a patient, long-term orientation. Net income of $18.8 million, EPS of $3.22, return on equity of 12.65%, and a payout ratio under 25% add up to a dividend profile that is both safe and capable of continued growth. The February 2026 increase to $0.21 per quarter is the latest evidence that management is committed to sharing improving earnings with shareholders in a disciplined way.

The valuation at 8.51 times earnings and 1.04 times book is modest by almost any measure, and the stock’s pullback from its 52-week high of $29.56 to the current $27.40 has improved the risk-reward balance for prospective buyers. This is not a stock that promises excitement or rapid price appreciation, but it does offer a combination of income, fundamental stability, and earnings-backed dividend growth that is genuinely difficult to find in today’s market at these valuations.

Risks are real, particularly around geographic concentration and interest rate sensitivity, but they appear manageable given the bank’s conservative capital position and low payout ratio. Abby Wendel and Mark Herpich have continued to execute well, and the operational improvements embedded in the margin structure suggest the bank is in a better competitive position today than it was when the current leadership pairing came together.

For investors who appreciate steady, well-supported income from a financially sound regional bank, Landmark Bancorp remains a name that deserves a place on the watchlist and, for those with a long time horizon, potentially in the portfolio.