Updated 2/24/26

Kadant Inc. (KAI) designs and manufactures critical components used in process industries worldwide, with a focus on pulp and paper, fiber processing, and industrial automation systems. The company combines consistent cash flow generation with disciplined capital management, making it a reliable presence in the industrial space. Revenue has crossed $1.05 billion on a trailing twelve-month basis, and its recent financials show steady gross margins and a conservatively managed balance sheet.

Despite a modest yield, Kadant continues to reward shareholders with measured dividend growth and a conservative payout ratio. Backed by a focused leadership team, the company has maintained healthy profitability, navigated macroeconomic headwinds, and preserved operating efficiency across its global footprint.

Recent Events

Kadant has continued to demonstrate operational resilience heading into early 2026, even as the broader industrial machinery sector faces uneven demand conditions. The company has been navigating a careful balance between capital equipment order softness and the steady performance of its aftermarket parts business, which has historically provided a more durable revenue base through economic cycles. Management has remained focused on execution in its core fiber processing and industrial flow control segments, with particular attention to margin preservation as input cost pressures persist in select regions.

On the financial front, trailing twelve-month revenue came in at $1.05 billion, representing a modest improvement from the prior period and reflecting the company’s ability to sustain its top line despite mixed industrial demand. Net income reached $101.97 million, producing diluted EPS of $8.65. Return on equity stands at 11.21% and return on assets at 6.33%, both reflecting a business that continues to generate acceptable returns on its capital base without taking on excessive risk.

Kadant’s profit margin of 9.69% reflects the reality of a competitive industrial supplier environment, but it also underscores the company’s ability to maintain pricing discipline. With short interest at approximately 1.37 million shares, the stock continues to attract some skepticism from traders, though the overall short position remains manageable relative to the company’s market capitalization of nearly $4 billion.

The stock is currently trading at $335.70, comfortably above the midpoint of its 52-week range of $244.87 to $387.53. That positioning reflects investor confidence in the company’s fundamentals, even as the broader industrial sector contends with uncertain end-market demand. Kadant’s beta of 1.23 means it tends to move with some additional sensitivity relative to the broader market, which is worth keeping in mind during volatile periods.

Key Dividend Metrics

📈 Forward Dividend Yield: 0.42%

💰 Annual Dividend Rate: $1.36

📆 Most Recent Dividend Payment: $0.34 per share

📅 Last Ex-Dividend Date: January 8, 2026

📊 Payout Ratio: 15.26%

🧭 5-Year Average Yield: 0.52%

🧱 Dividend Growth: Modest and steady

🏦 Dividend Coverage: Conservative and well-supported

Dividend Overview

Kadant isn’t a go-to name if you’re looking for a high-yield paycheck from your portfolio. With a forward yield of 0.42%, it won’t appeal to income hunters focused on big payouts. But where Kadant shines is in its commitment to consistent, well-covered dividend payments that reflect genuine financial discipline rather than a stretch to attract income-oriented buyers.

The company pays what it can afford, no more and no less. That kind of restraint is reflected in a payout ratio of just 15.26%. They’re not straining to impress with the dividend, but they are absolutely serious about maintaining it. That’s exactly the sort of approach you want to see when prioritizing dividend safety and capital preservation over headline yield.

Kadant has also been increasing its dividend steadily over the years. The most recent quarterly rate of $0.34 per share represents a step up from the $0.32 quarterly rate that held throughout most of 2024, bringing the annualized payout to $1.36. That increase, which took effect with the April 2025 payment, marks a 6.25% raise over the prior quarterly rate. It’s not flashy growth, but it’s consistent and backed by a business that generates more than enough cash to support it.

The dividend is fully supported by net income, and with a payout ratio well below 20%, the company has ample breathing room. Even if earnings experience some softness in the coming quarters, the current dividend level carries virtually no risk of a cut. That kind of coverage is exactly what dividend growth investors should be looking for in an industrial name.

Dividend Growth and Safety

Kadant’s dividend growth won’t knock your socks off, but it’s the kind you can count on. Reviewing the dividend history over recent years tells a clear story: the company moved from $0.29 per quarter throughout 2023, stepped up to $0.32 in April 2024, and then raised again to $0.34 in April 2025. That’s a pattern of annual increases that reflects management’s confidence in the underlying cash generation of the business. The five-year average yield of around 0.52% remains close to where the current yield sits today, suggesting the stock price and dividend have grown in reasonably close proportion over time.

The more important story is safety. With a payout ratio of just 15.26%, Kadant has one of the more conservative dividend strategies in the industrial space. They’re not sacrificing financial flexibility or taking on leverage simply to fund a larger payout. That restraint is precisely why this dividend feels so reliable across different points in the business cycle.

The company’s earnings base further strengthens the safety profile. Net income of $101.97 million against total annual dividend obligations that remain a small fraction of that figure means there is substantial room before any coverage concern could arise. Combine that with a focused management team and a business model that generates recurring aftermarket revenue, and you get a dividend that is not just sustainable but quietly resilient.

Short interest of approximately 1.37 million shares introduces a modest element of volatility potential, but this is far less alarming than the levels observed in prior periods. For long-term holders collecting the dividend, a positive earnings surprise or a guidance raise could generate meaningful price appreciation on top of the income stream, giving the total return profile more appeal than the yield alone might suggest.

All in all, Kadant’s dividend may not be the star of your portfolio, but it plays a reliable supporting role. For investors who value steady income, capital preservation, and a conservative payout approach, this is a company worth keeping on your radar.

Chart Analysis

Kadant’s price chart tells a constructive story over the trailing twelve months. The stock has traveled from a 52-week low of $247.20 all the way to a peak of $380.03 before settling at its current level of $335.70, a round-trip that reflects both the broader market volatility of the period and the underlying demand for KAI shares on any meaningful pullback. The 35.8% recovery from the annual low is a strong indication that buyers have been consistently stepping in at lower prices, and the current position just 11.67% off the 52-week high suggests the stock remains in the upper range of its annual trading band rather than showing signs of sustained distribution.

The moving average picture is unambiguously positive. KAI is trading above both its 50-day moving average of $314.11 and its 200-day moving average of $309.82, and critically, the 50-day has crossed above the 200-day to form what technicians call a golden cross. This configuration is generally interpreted as a signal that intermediate-term momentum has shifted in favor of the bulls, and for a dividend growth stock like KAI, it also suggests the kind of price stability that allows an income-focused investor to build or add to a position with reasonable confidence in the technical backdrop. The spread between the current price and both moving averages, roughly $21 above the 50-day and $26 above the 200-day, provides a reasonable cushion before any near-term softness would challenge the trend.

The RSI reading of 54.56 sits in a comfortable middle ground. The stock is neither overbought nor oversold, which means there is no immediate technical warning of an exhausted rally or a crowded trade that could unwind sharply. A reading in the mid-50s often reflects healthy, measured momentum rather than speculative froth, and for an investor more focused on dividend income than short-term price swings, it removes one potential source of near-term volatility risk from the equation.

Taken together, the technical picture for KAI is broadly supportive for dividend growth investors evaluating an entry. The confirmed uptrend, the golden cross formation, and the neutral RSI all point to a stock that has regained its footing after a sharp correction and is consolidating in a healthy manner. The pullback of nearly 12% from the 52-week high may actually represent a more attractive entry point than the peak would have offered, and the strong recovery from the annual low reinforces the idea that long-term holders of this name have been rewarded for patience. Investors adding for income should be mindful that a retest of the 50-day moving average near $314 remains a plausible scenario on any broader market weakness, but the overall trend remains intact.

Cash Flow Statement

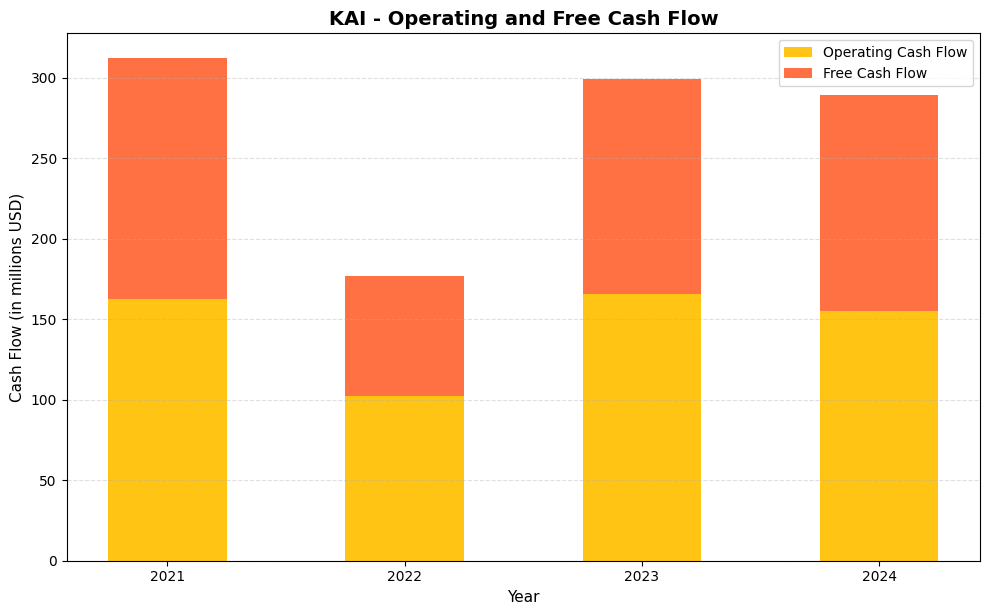

Kadant’s cash flow profile reflects a business that reliably converts earnings into real cash, which is the foundation any dividend investor should start with. Operating cash flow came in at $162.4 million in 2021, dipped to $102.6 million in 2022, then recovered strongly to $165.5 million in 2023 before settling at $155.3 million in 2024. Free cash flow followed a similar arc, moving from $149.6 million in 2021 down to $74.4 million in 2022, then rebounding to $133.7 million in 2023 and holding essentially flat at $134.3 million in 2024. That 2022 trough deserves attention, but the swift recovery in subsequent years suggests it reflected a timing or investment cycle rather than any structural deterioration in the business. With free cash flow running comfortably above $130 million in each of the last two years, the dividend remains exceptionally well covered relative to Kadant’s modest annual payout obligations.

What stands out across this four-year window is how capital-efficient Kadant’s model actually is. The gap between operating cash flow and free cash flow has stayed relatively narrow in most years, meaning the company is not consuming large amounts of cash on maintenance or growth capital expenditures just to sustain its earnings power. The 2022 compression was the exception, and even in that year, the business still generated $74.4 million in free cash flow. For shareholders, that consistency matters more than any single year’s number because it speaks to the repeatability of the cash generation. A company that reliably produces free cash flow in the $130 million range has substantial flexibility to grow its dividend, reduce debt, or pursue bolt-on acquisitions without putting income distributions at risk. Kadant’s track record here gives dividend growth investors a credible foundation to expect continued payout increases going forward.

Analyst Ratings

Kadant carries a consensus rating of Buy among the three analysts currently covering the stock, reflecting a generally constructive view of the company’s fundamentals and its positioning within the specialty industrial machinery space. The average 12-month price target sits at $341.00, which implies modest upside of roughly 1.6% from the current price of $335.70. That tight gap between the current price and the mean target suggests the stock is trading close to where the Street sees fair value in the near term.

The range of analyst targets provides useful context. The high target of $380.00 represents a potential upside of approximately 13.2% from current levels, while the low target of $303.00 implies roughly 9.7% downside, indicating that even the most cautious analyst on the name is not calling for a dramatic decline. That relatively narrow bear case is consistent with Kadant’s track record of earnings stability and conservative financial management.

With only three analysts actively covering the stock, Kadant remains a relatively under-followed name on Wall Street for a company of its size and quality. That limited coverage can create inefficiencies, and it means that a positive earnings surprise or a strategic announcement could attract new analyst attention and potentially move the consensus target meaningfully. For now, the existing Buy consensus reflects confidence in the business without pricing in exceptional near-term growth.

The current price of $335.70 sits comfortably within the analyst target range and just below the mean, which suggests the stock is neither egregiously overvalued nor trading at a deep discount to Street expectations. Investors entering near current levels are essentially paying close to consensus fair value, with the upside scenario dependent on Kadant continuing to execute on margins and demonstrating resilience in its order book through the rest of 2026.

Earning Report Summary

Steady Performance in a Mixed Industrial Environment

Kadant Inc. delivered full-year results that reflect a business managing through uneven industrial demand with characteristic discipline. Trailing twelve-month revenue of $1.05 billion represents a modest increase from the prior period, showing that the company’s diversified end-market exposure has helped stabilize the top line even as some customers have delayed capital equipment decisions. The aftermarket parts business has continued to provide a steady recurring revenue base, partially offsetting variability in new equipment orders.

Net income of $101.97 million and diluted EPS of $8.65 reflect solid earnings generation, though the current EPS figure represents some moderation from the elevated levels seen in prior years. Profit margin of 9.69% demonstrates that Kadant continues to manage its cost structure effectively, and a return on equity of 11.21% confirms that management is deploying capital productively. These are not blockbuster numbers, but they reflect a business that executes consistently rather than one that swings dramatically with the cycle.

What’s Working

The recurring revenue component of Kadant’s business continues to be a key differentiator. Parts and consumables demand has remained relatively stable, providing cash flow predictability that underpins both the dividend and the company’s ability to invest in product development. The company’s global footprint also allows it to capture demand across different regional business cycles, reducing the impact of any single geography softening at a given point in time. Management has continued to emphasize operational efficiency, and the results in margin preservation reflect that focus.

Guidance and Expectations

Kadant has historically guided conservatively and then met or exceeded its targets, a pattern that has helped build credibility with the investor community. With full-year revenue of $1.05 billion now on the books, the focus turns to whether demand conditions in 2026 will support a return to more meaningful top-line growth. Capital equipment order activity will be a key indicator, as a recovery in industrial investment spending could provide a meaningful uplift to both revenue and earnings per share relative to the current EPS of $8.65.

Leadership’s View

CEO Jeffrey Powell has maintained a measured but confident tone in his communications with investors, acknowledging the macro headwinds facing capital equipment buyers while expressing confidence in the durability of Kadant’s business model. His emphasis on the resilience of the aftermarket business and the quality of the company’s global execution has been consistent, and the financial results have generally backed up that narrative. Powell’s approach reflects a management culture that prioritizes long-term value creation over short-term financial engineering.

Overall, Kadant’s recent financial performance tells the story of a company navigating a challenging industrial environment without losing its footing. Margins are intact, the balance sheet remains sound, and the dividend continues to grow. That combination of stability and modest progress is precisely what long-term industrial investors should expect from a business of this caliber.

Management Team

Kadant Inc. is led by a management team with deep experience in the industrial and manufacturing sectors. At the top is Jeffrey L. Powell, who has served as President and CEO since 2019. Powell has emphasized operational discipline and long-term strategic growth during his tenure, helping guide the company through both steady growth periods and more challenging macroeconomic environments. His consistent messaging around the durability of Kadant’s recurring revenue streams and the quality of its global operations has resonated with long-term investors.

Michael J. McKenney, the Executive Vice President and Chief Financial Officer, brings a steady hand to Kadant’s financial strategy. He has played a central role in maintaining the company’s solid balance sheet and its ability to generate consistent returns on equity and assets, which are foundational to Kadant’s capacity to sustain and grow its dividend over time.

The broader leadership team includes industry veterans from engineering, global operations, and business development roles. Their collective background supports Kadant’s efforts to drive product innovation while staying responsive to changing customer needs across international markets. This depth of experience is a meaningful competitive asset as the company navigates evolving industrial technology trends and shifting global trade dynamics.

Valuation and Stock Performance

Kadant’s share price of $335.70 sits well above the midpoint of its 52-week range of $244.87 to $387.53, reflecting investor confidence that has built over the past year despite an uneven industrial backdrop. The stock’s recovery from its 52-week low represents a gain of more than 37%, which is a meaningful move for a company that is often perceived as a steady, low-drama compounder rather than a high-growth story.

From a valuation perspective, Kadant trades at a price-to-earnings ratio of 38.81 times trailing earnings, which is elevated relative to the broader industrial machinery peer group. That premium reflects the market’s willingness to pay up for the quality of Kadant’s recurring revenue base, its consistent execution, and its conservative financial management. The price-to-book ratio of 3.99 times book value of $84.14 per share similarly suggests that investors are assigning meaningful franchise value to the business beyond its tangible assets.

With the current price sitting just below the analyst mean target of $341.00, the stock is trading close to consensus fair value, which limits the near-term upside catalyst to an improvement in earnings trajectory or a positive shift in industrial demand conditions. For long-term holders, however, the valuation reflects a business that has earned its premium through consistent delivery, and the combination of modest dividend growth and potential capital appreciation continues to make Kadant an appealing holding for patient investors with a quality bias.

Risks and Considerations

Kadant operates in capital equipment markets that are inherently cyclical, meaning that a slowdown in industrial investment spending or a broader global economic contraction could weigh materially on new order activity. Customers in the pulp, paper, and fiber processing industries tend to defer large equipment purchases when business conditions deteriorate, and a sustained downturn in these end markets would put pressure on both revenue and earnings per share.

The company’s international exposure introduces additional complexity, as a meaningful portion of Kadant’s revenue is generated outside the United States. Currency fluctuations, trade policy changes, and geopolitical developments in key manufacturing regions can all affect the company’s results in ways that are difficult to predict or fully hedge. Any escalation in trade tensions affecting Kadant’s supply chain or customer base could create margin pressure or demand disruption.

The current P/E ratio of 38.81 represents a relatively demanding valuation that leaves limited room for earnings disappointment. If Kadant were to report results meaningfully below current EPS of $8.65, or if management were to lower guidance, the stock could face a valuation reset that would be more painful than it might be for a lower-multiple industrial peer. Investors entering at current prices should be comfortable with that valuation risk.

Ongoing innovation requirements in industrial technology also represent a longer-term consideration. Staying competitive in specialty machinery requires continuous investment in product development and engineering capability. If competitors were to introduce more advanced or cost-effective solutions, Kadant could face pricing pressure or market share erosion in certain product lines. The company has a solid track record of managing this challenge, but it remains an area that warrants ongoing attention.

Final Thoughts

Kadant Inc. presents a well-managed, financially disciplined company that has carved out a dependable niche in the industrial manufacturing ecosystem. Its leadership team brings a measured, thoughtful approach to growth, backed by a track record of operational excellence and consistent execution across varying market conditions. The recent dividend increase to $0.34 per quarter, representing a 6.25% raise from the prior rate, reinforces the company’s commitment to returning capital to shareholders in a sustainable and growing fashion.

The stock’s current valuation at a P/E of 38.81 reflects the market’s confidence in Kadant’s ability to deliver steady performance over the long haul. While the yield of 0.42% is modest, the dividend is exceptionally well-covered at a 15.26% payout ratio, and the company’s net income of just over $102 million provides a robust foundation for continued incremental increases in years to come.

Investors should remain mindful of the risks that come with industrial cyclicality, international exposure, and a premium valuation that leaves little margin for error. Kadant operates in a complex, evolving space that requires both innovation and adaptability, and while its consistent track record suggests it has those qualities, the current price demands continued execution to justify holding at these levels.

For those with a long-term horizon and an appreciation for quality industrial operators that compound steadily rather than spectacularly, Kadant offers a compelling combination of dividend reliability, financial discipline, and durable competitive positioning.