Updated 2/24/26

Johnson Outdoors Inc. designs and manufactures outdoor recreational products, including well-known brands like Minn Kota, Humminbird, and Jetboil. With a heritage dating back to 1970 and leadership under CEO Helen Johnson-Leipold, the company blends deep-rooted industry experience with a steady, family-guided approach. Its conservative balance sheet posture and consistent dividend policy reflect a management team committed to financial discipline, even as the business works through a prolonged revenue downturn.

Recent Events

Johnson Outdoors has been navigating one of the more difficult stretches in its recent history, and the pressure on its core fishing business remains the central story heading into 2026. The Minn Kota and Humminbird brands, which together form the backbone of the company’s revenue, have faced softening retail demand as consumers pull back on discretionary outdoor equipment spending. Dealer destocking, which weighed heavily on results throughout fiscal 2024 and into fiscal 2025, has been a persistent headwind, and the company has been working to right-size channel inventory across its distribution network.

The stock has staged a dramatic recovery from its 52-week low of $21.33, trading near $50.50 as of late February 2026, not far from its 52-week high of $51.55. That move represents a near-doubling off the lows, and it reflects a meaningful shift in investor sentiment, likely driven by expectations that the destocking cycle is nearing its end and that normalized demand could support a meaningful earnings recovery. Short interest has been declining from elevated levels, which may also be contributing to the upward momentum as bearish bets get unwound.

On the operational front, management has continued to invest in product development across its camping and diving segments, and the Jetboil brand has maintained its position as a category leader in portable outdoor cooking. The company has also kept its capital spending disciplined, with no long-term debt on the balance sheet and operating cash flow of $54.7 million providing a meaningful cushion for ongoing investment and dividend maintenance.

Key Dividend Metrics

💰 Forward Dividend Yield: 2.65%

📅 Last Dividend Payment: $0.33 per share (January 8, 2026)

🏦 Payout Ratio: 272.34% (based on net income; cash flow coverage is substantially better)

📈 Annual Dividend Rate: $1.32 per share

💵 Free Cash Flow (ttm): $31.95M

📊 Price-to-Book Ratio: 1.26

🔎 Operating Cash Flow (ttm): $54.7M

🧾 Book Value Per Share: $40.21

Dividend Overview

The payout ratio of 272% is the first number that catches the eye, and understandably so. Against a reported net loss of $22.3 million and earnings per share of negative $2.19, the $1.32 annual dividend appears entirely disconnected from reported profitability. But the net income figure is distorted by non-cash items and charges that do not reflect the company’s actual ability to generate cash. Operating cash flow of $54.7 million tells a very different story, and free cash flow of nearly $32 million confirms that the business is generating real liquidity well in excess of its roughly $13 million annual dividend obligation.

The yield has compressed considerably from where it stood during the depths of the selloff. At $50.50, the forward yield sits at 2.65%, compared to the elevated levels income investors could have captured when the stock was trading near its 52-week low in the low $20s. That compression is a natural consequence of the stock’s strong recovery, and it means new buyers are entering at a more normalized yield rather than the distressed-level income opportunity that existed earlier in the cycle.

Management has maintained the quarterly dividend at $0.33 per share without interruption throughout this downturn, with the most recent payment made on January 8, 2026. The consistency of that payment across twelve consecutive quarters at the same rate signals that the board views the dividend as a core commitment rather than a discretionary payout. For income investors, that kind of institutional steadiness carries real weight, particularly during periods when earnings are temporarily impaired.

With the stock now trading at 1.26 times book value, the valuation discount that characterized much of the past year has largely closed. The dividend remains supported by cash flow, but the margin of safety has narrowed relative to where it stood when the stock was trading below book. Income investors considering a position here are buying into a steady, if unspectacular, income stream backed by a clean balance sheet rather than a deep-value bargain.

Dividend Growth and Safety

Johnson Outdoors has held its quarterly dividend at $0.33 per share since the fourth quarter of fiscal 2023, when it was raised modestly from $0.31. In the twelve payments spanning April 2023 through January 2026, the company has delivered exactly that rate without a single reduction or suspension. That stability is not accidental. Management has consistently prioritized dividend continuity over aggressive growth, a philosophy that suits the cyclical nature of the outdoor recreation industry and the family-controlled ownership structure.

Dividend growth has effectively been flat over the past two-plus years, and with the company still reporting net losses, there is little near-term catalyst for another increase. The more relevant question for income investors is whether the $0.33 quarterly rate is sustainable, and on a cash flow basis, the answer appears to be yes. The $1.32 annual payout requires approximately $13.8 million in cash given the share count, and free cash flow of nearly $32 million covers that obligation more than twice over.

The absence of long-term debt removes a major source of dividend risk. There are no debt covenants to restrict distributions, no maturity walls to navigate, and no refinancing pressures that could force a tradeoff between servicing debt and maintaining the dividend. That structural advantage is easy to overlook when reviewing the headline payout ratio, but it matters enormously for long-term income reliability.

Revenue trends remain the variable most worth monitoring. Full-year revenue of approximately $625.7 million reflects the ongoing pressure across the fishing and watercraft segments, and a return to meaningful earnings will depend on demand normalizing in those core markets. If the recovery takes longer than anticipated, free cash flow could compress, though the balance sheet provides substantial buffer before the dividend would come under genuine pressure.

Chart Analysis

Johnson Outdoors has staged one of the more dramatic recoveries in the small-cap consumer discretionary space over the past twelve months. Starting from a 52-week low of $21.17, the stock has more than doubled to reach its current price of $50.50, which also happens to be the 52-week high. That kind of price action, a 138.6% rally off the trough with no meaningful overhead resistance above the current level, tells a story of sustained institutional accumulation rather than a short-term speculative burst. When a stock arrives at a new 52-week high with momentum still intact, it typically signals that buyers remain in control and that prior resistance levels have been cleared decisively.

The moving average structure confirms the bullish trend. The 50-day moving average sits at $45.75 and the 200-day moving average sits at $38.23, and the stock is trading comfortably above both. More importantly, the 50-day has crossed above the 200-day, forming what technicians call a golden cross. This pattern is significant not because it predicts the future with certainty, but because it reflects a meaningful shift in the stock’s intermediate and long-term trend. The gap between the current price of $50.50 and the 200-day moving average of $38.23 represents roughly a 32% cushion, which gives dividend investors a substantial buffer before the long-term trend would even begin to show signs of deterioration.

The RSI reading of 56.8 adds an encouraging nuance to this picture. Many stocks that have rallied as sharply as JOUT tend to arrive at new highs in overbought territory, with RSI readings above 70, which can signal near-term exhaustion. An RSI near 57 suggests the momentum is healthy but not overextended, meaning the stock has room to continue higher before running into the kind of technical fatigue that often precedes a pullback. This moderate momentum reading is actually a constructive signal for investors considering a position, as it reduces the probability of buying into a short-term peak.

For dividend investors, the technical picture here is genuinely supportive. A golden cross, a 52-week high with no overhead resistance, and a non-overbought RSI combine to paint a chart that favors patient, income-oriented holders. The primary risk to monitor is the distance the stock has traveled in a short period. A reversion toward the 50-day moving average around $45.75 would represent a roughly 9% pullback and should be treated as normal digestion rather than a trend break. Long-term income investors would likely view any such consolidation as an opportunity to establish or add to a position at more favorable dividend yield levels.

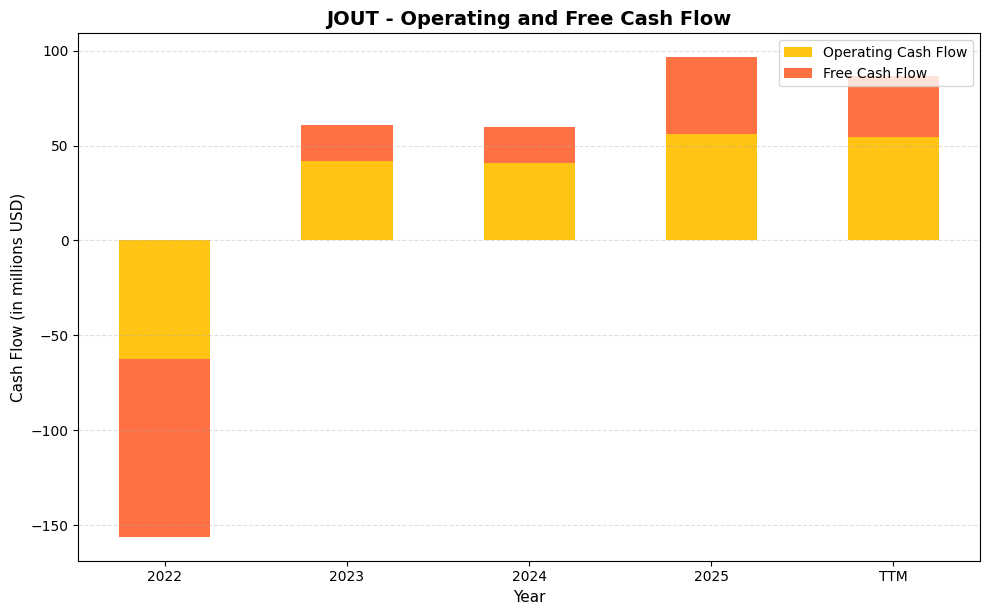

Cash Flow Statement

Johnson Outdoors has moved through a meaningful cash flow recovery over the past three fiscal years, and the trajectory tells an encouraging story for dividend sustainability. The company posted deeply negative operating cash flow of $62.1 million in fiscal 2022, with free cash flow falling to a concerning $93.8 million deficit that year. Since then, the turnaround has been sharp and consistent. Operating cash flow stabilized at $41.7 million in fiscal 2023, held nearly flat at $41.0 million in fiscal 2024, and then accelerated meaningfully to $56.2 million in fiscal 2025. Free cash flow followed a parallel path, recovering to $19.0 million in both 2023 and 2024 before jumping to $40.2 million in fiscal 2025. The TTM figures of $54.7 million in operating cash flow and $32.0 million in free cash flow confirm that the improvement is durable rather than a one-year event, and they provide a reasonable coverage cushion for JOUT’s current annual dividend commitment.

The context behind these numbers matters for shareholders. The fiscal 2022 cash flow collapse was driven by aggressive inventory builds during a period of supply chain disruption, a capital allocation decision that proved costly when consumer demand softened. The subsequent years reflect not just a normalization of working capital but also a more disciplined approach to inventory management and capital spending. With capital expenditures running at roughly $16 million to $22 million annually in recent periods, Johnson Outdoors is not a heavy capital consumer relative to its revenue base, which means a larger share of operating cash flow flows through to free cash. At $40.2 million in fiscal 2025 free cash flow against a dividend program that costs the company well under $20 million per year, the payout appears comfortably funded from internally generated cash, without relying on debt or asset sales to bridge any gap.

Analyst Ratings

Analyst coverage of Johnson Outdoors is thin, with only one analyst actively tracking the stock. That single analyst has set a price target of $55.00, which sits roughly 9% above the current trading price of $50.50. The target implies a measured but positive view on the company’s prospects, suggesting that the analyst sees room for continued appreciation even after the stock’s substantial recovery from its lows.

The $55.00 price target likely reflects expectations for earnings normalization as the dealer destocking cycle concludes and demand in the fishing and outdoor equipment categories stabilizes. The Humminbird and Minn Kota brands retain strong market positions, and a return to positive net income would remove the distortions that have complicated the fundamental picture throughout fiscal 2024 and 2025.

The limited coverage is itself worth considering. Small-cap consumer cyclicals with family-controlled ownership structures often attract fewer analysts, which can create both informational gaps and potential mispricings. With one analyst and a consensus price target sitting just above current levels, the stock is not pricing in a dramatic earnings recovery, but neither is it priced for ongoing deterioration.

Investors should monitor whether additional analyst coverage emerges as the earnings recovery thesis becomes more visible. A re-rating toward broader coverage and more constructive price targets would likely require evidence of meaningful revenue improvement and a return to positive earnings per share, developments that the current operating cash flow trajectory suggests are achievable if market conditions cooperate.

Earnings Report Summary

A Prolonged Recovery Cycle

Johnson Outdoors closed out the most recent reported fiscal year with full-year revenue of approximately $625.7 million and a net loss of $22.3 million, or $2.19 per share. The loss, while smaller than the $26.5 million loss reported in fiscal 2024, reflects an earnings environment that has not yet returned to positive territory. Revenue has declined meaningfully from peak levels as the outdoor recreation demand surge of the pandemic era reversed and channel destocking weighed on orders across the fishing, watercraft, and camping segments.

The fishing segment, anchored by Minn Kota trolling motors and Humminbird fish finders, continued to face the most acute pressure, as these products sit at higher price points and are particularly sensitive to consumer confidence and discretionary spending. Watercraft and camping products also saw softer demand, consistent with the broader trend of consumers reprioritizing spending away from outdoor gear purchased heavily during 2020 and 2021.

Margin and Cost Dynamics

Gross margins remained under pressure, reflecting the combination of lower volume reducing overhead absorption, promotional pricing used to move aging inventory, and an unfavorable product mix. Operating expenses have been managed carefully, with management maintaining a lean cost structure to limit cash burn during the downturn. The $54.7 million in operating cash flow, despite the net loss, indicates that working capital management and depreciation-heavy expense structures are helping preserve actual liquidity even as reported earnings remain negative.

Management’s Posture

CEO Helen Johnson-Leipold has maintained a consistent message throughout the downturn, framing the current period as a cyclical correction rather than a structural impairment of the business. Her emphasis on brand investment, product innovation, and operational discipline reflects the long-term orientation that has characterized Johnson family leadership for decades. The company has avoided the kind of reactive cost-cutting that can damage brand equity, instead positioning itself to capture demand when the market normalizes.

CFO David Johnson has continued to highlight the balance sheet’s strength as a strategic asset. With no long-term debt and operating cash flow well above dividend requirements, the company retains significant financial flexibility to fund product development and maintain shareholder distributions without external financing.

Capital Allocation Discipline

Capital expenditures have remained measured, consistent with the company’s practice of investing in maintenance and targeted product development rather than large-scale capacity expansion. Depreciation and amortization continue to run at levels that partially explain the gap between net income and operating cash flow, and free cash flow of nearly $32 million reinforces that the business is not consuming cash at the rate suggested by the headline earnings figures.

The narrative from management is one of patient endurance. Johnson Outdoors has navigated difficult cycles before, and the combination of a clean balance sheet, established brand franchises, and a committed leadership team positions the company to emerge from this period with its competitive standing intact. The pace of that recovery will depend largely on when consumer demand for premium fishing and outdoor equipment returns to more normalized levels.

Management Team

At the helm of Johnson Outdoors is Helen Johnson-Leipold, who has served as Chairman and CEO since 1999. As a member of the Johnson family, she brings a deep understanding of the company’s heritage and long-term strategic priorities. Her leadership emphasizes brand stewardship, global operations, and product innovation, ensuring that near-term financial pressures do not compromise the company’s position in its core markets.

Supporting her is a seasoned executive team with tenure that reflects institutional stability. David W. Johnson, the Chief Financial Officer, has been central to maintaining the company’s debt-free balance sheet and disciplined capital allocation approach throughout the current downturn. John C. Moon, serving as Chief Information Officer and Vice President, oversees the technological infrastructure that supports product development and operational efficiency. Karen James, Vice President of Global Operations, brings supply chain expertise that is particularly relevant given ongoing pressures in global manufacturing and logistics. Patricia Penman, Vice President of Marketing Services and Global Communication, leads brand strategy and market engagement across the company’s portfolio of outdoor recreation brands.

The longevity and cohesion of this leadership team is a meaningful attribute for long-term investors. The family-controlled ownership structure and experienced management bench reduce the risk of strategic whipsawing and reinforce the company’s commitment to its established approach of conservative financial management combined with brand-led product development.

Valuation and Stock Performance

Johnson Outdoors stock has experienced a remarkable turnaround over the past several months. As of February 24, 2026, shares are trading at $50.50, near the top of the 52-week range of $21.33 to $51.55. The stock has essentially doubled from its lows, a move that reflects a significant reassessment of downside risk and growing investor confidence that the earnings recovery cycle is approaching. Market capitalization now stands at approximately $528 million, moving the company back toward mid-small-cap territory.

The price-to-book ratio has re-rated from deeply discounted levels to 1.26 times book value, with book value per share at $40.21. That re-rating removes the deep-value argument that was available to investors who bought near the lows, though the stock still trades at a reasonable multiple of tangible assets for a company with established brand value and zero long-term debt. The single analyst covering the stock has a price target of $55.00, implying roughly 9% upside from current levels.

With the P/E ratio not meaningful due to the current net loss, price-to-book and enterprise value-to-cash flow metrics are the more relevant valuation tools. At 1.26 times book, the stock is no longer a bargain in the traditional sense, but it is not expensive for a business with $54.7 million in operating cash flow and a clean balance sheet. The forward yield of 2.65% is closer to the stock’s historical norm, reflecting the price recovery rather than the distressed yield levels of recent months.

The beta of 0.90 suggests relatively modest volatility relative to the broader market, and the short interest of approximately 374,000 shares has declined meaningfully from prior elevated levels, reducing the technical overhang that contributed to price instability earlier in the cycle. The stock’s near-term performance will likely be driven by evidence of earnings normalization, with positive EPS in upcoming quarters serving as the most meaningful potential catalyst for continued appreciation toward and beyond the $55.00 analyst target.

Risks and Considerations

The most immediate risk facing Johnson Outdoors is the pace and completeness of the revenue recovery. The company has posted declining top-line results for multiple consecutive periods, driven primarily by weakness in the fishing segment where Minn Kota and Humminbird compete at premium price points. If consumer demand for high-end outdoor equipment remains suppressed longer than anticipated, revenue could stay depressed and the path back to positive earnings could extend further into fiscal 2026 and beyond.

Margin recovery is closely tied to volume. Much of the gross margin compression has resulted from lower overhead absorption at reduced production levels and elevated promotional activity to clear dealer inventory. A return to healthier margins depends on volume rebounding to levels that allow fixed costs to be spread more efficiently, and there is no guarantee that volume will recover on the timeline that appears to be baked into the current stock price near 52-week highs.

The macroeconomic backdrop presents ongoing uncertainty. Consumer discretionary spending on premium outdoor recreation products is sensitive to employment trends, consumer confidence, and broader economic conditions. A deterioration in the economic environment, or a prolonged period of elevated interest rates constraining consumer borrowing and spending, could delay the demand recovery that the current valuation appears to anticipate.

Supply chain considerations remain relevant, particularly given the company’s global manufacturing footprint and exposure to input cost volatility. Any disruption in key component sourcing, combined with the currency exposure inherent in international operations, could add cost pressure at a time when margins are already below historical norms. Investors should also be mindful that the stock’s rapid recovery from its lows has reduced the margin of safety that characterized the investment opportunity earlier in the cycle, meaning the risk-reward profile today is less asymmetric than it was when shares were trading below book value.

Final Thoughts

Johnson Outdoors has navigated an extended and painful cyclical downturn with its financial foundation largely intact. The combination of zero long-term debt, $54.7 million in operating cash flow, and an uninterrupted dividend at $0.33 per quarter reflects a management team that has prioritized durability over short-term earnings optics. The stock’s recovery from $21.33 to near $50.50 signals that the market is beginning to price in a normalization of demand across the fishing, camping, and watercraft segments, though actual earnings have yet to confirm that recovery in reported numbers.

For dividend growth investors, Johnson Outdoors occupies a specific niche: it is not a high-yield opportunity at current prices, nor is it a rapid dividend grower. What it offers is a consistent, cash-flow-supported quarterly payment backed by a clean balance sheet and a family-led management team with a demonstrated commitment to maintaining distributions through difficult cycles. The 2.65% yield at current prices is modest, but it comes with the reassurance of twelve consecutive quarters at the same rate and a balance sheet that provides genuine flexibility. Investors considering the stock here are essentially making a bet that the earnings recovery the market is starting to price in will materialize and drive the stock toward and above the single analyst’s $55.00 price target.