Updated 2/24/26

John Wiley & Sons (NYSE: WLY) is pressing through a challenging stretch in its multi-year transformation, balancing its deep roots in academic publishing with an accelerating pivot toward digital content and AI licensing. Trading near the low end of its 52-week range, the stock has lost meaningful ground over the past year, yet the underlying business continues to generate solid free cash flow. With a forward yield approaching 5% and a payout well-covered by operating cash flow, WLY remains a legitimate candidate for income investors willing to look past near-term earnings noise.

Revenue has stabilized in the $1.67 billion range, net income has improved considerably from a year ago, and management’s ongoing restructuring is beginning to show up in the margin structure. The stock’s sharp discount to analyst price targets adds an element of total-return potential that complements the income thesis here.

Recent Events

Wiley has spent the past several months advancing its repositioning as a digital-first research and learning company. The company has continued expanding its open access publishing footprint, deepening institutional subscription agreements, and building out AI licensing arrangements that monetize its vast repository of peer-reviewed content. These licensing deals, aimed squarely at technology companies developing large language models and AI research tools, represent one of the more compelling emerging revenue threads in the academic publishing space.

On the operational front, management has maintained its cost discipline, continuing to shed legacy infrastructure and redirect resources toward higher-margin digital platforms. The restructuring program that began under interim CEO Matthew Kissner has not yet run its full course, but the direction is clear: fewer physical products, more scalable content delivery, and a leaner cost base to support improved margins into fiscal 2026 and beyond.

The stock itself has been under pressure, sliding from a 52-week high near $47.26 to its current level around $29.35, a decline of roughly 38% from peak. Much of that pressure reflects broader investor skepticism about traditional publishing business models, compounded by some uncertainty around the pace of Wiley’s digital revenue ramp. Despite that, the company’s free cash flow of approximately $167 million over the trailing twelve months provides a meaningful buffer, and the dividend obligation of roughly $75 million annually consumes only a fraction of that figure.

Key Dividend Metrics

📈 Forward Yield: 4.87%

💵 Annual Dividend: $1.42 per share

🎯 Payout Ratio: 75.67% (based on net income)

📅 Last Dividend Paid: $0.355 per share (December 30, 2025)

💰 Free Cash Flow: $166.8 million

📊 FCF Payout Ratio: Approximately 45%

🧮 Operating Cash Flow: $220.1 million

🚨 Dividend Safety: Supported by cash flow; monitor earnings recovery

Dividend Overview

At a yield of 4.87%, Wiley’s dividend sits well above the broader market average and meaningfully ahead of the company’s own historical norm. For income-focused investors, that kind of yield from a business with recurring, subscription-like revenue characteristics is genuinely attractive, particularly when the payout is backed by real cash generation rather than financial engineering.

The reported payout ratio of 75.67% against net income of $1.87 per share and an annual dividend of $1.42 looks more manageable than it did a year ago, when earnings were far thinner. Net income has improved substantially, reaching $101.7 million on a trailing basis, which brings the earnings-based coverage ratio into a more comfortable range. The cash flow picture is even cleaner: free cash flow of $166.8 million against an annual dividend obligation in the neighborhood of $75 million implies a cash payout ratio around 45%, leaving ample room for reinvestment and debt service.

The nuance here is that GAAP earnings, while improved, are still subject to restructuring charges and non-cash items that can distort the picture in any given period. Cash flow tells the more reliable story, and on that basis, the dividend looks well-supported at the current rate.

Dividend Growth and Safety

Wiley’s dividend history over the past two years reflects a pattern of measured, incremental growth rather than aggressive hiking. Starting from $0.3475 per share in April 2023, the quarterly payment has edged higher in a series of modest steps, reaching $0.355 per share by July 2025 and holding there through the December 2025 payment. That progression represents cumulative growth of roughly 2.2% over approximately two and a half years, which is modest but consistent with a company managing its payout carefully through a transition period.

The most recent increase, from $0.3525 to $0.355 per quarter, came in July 2025 and has been maintained through the latest payment. While the pace of growth has been slow, the fact that Wiley has continued increasing rather than freezing or cutting its dividend through a period of meaningful operational and strategic change says something about management’s commitment to the income proposition.

Safety, on balance, looks reasonable. Operating cash flow of $220 million and free cash flow of $167 million both comfortably exceed the annual dividend requirement. Short interest sits at approximately 3.5 million shares, which is not insignificant but reflects a more moderate level of skepticism than was present a year ago. The primary risk to dividend continuity would be a sustained deterioration in cash flow, which does not appear imminent given the current trajectory of the Research segment.

For income investors, Wiley occupies a middle ground: the dividend is not at immediate risk, growth will likely remain slow until the digital transformation matures, and the yield at current prices is genuinely compelling. The setup rewards patience more than momentum.

Institutional ownership remains high, reflecting a base of long-term holders who are evidently willing to ride out the transition. That kind of ownership stability tends to reduce the probability of dramatic dividend policy reversals, as large institutional holders typically make their preferences on capital return clear to management.

Chart Analysis

Wiley’s price action over the past year tells a story of persistent selling pressure and steadily eroding investor confidence. The stock has shed roughly 35% from its 52-week high of $44.99, and at the current price of $29.35 it sits just 1.95% above its 52-week low of $28.79. That proximity to the annual floor is not a minor detail for dividend investors, because it signals that the market has found very little reason to step in and defend the shares at any meaningful level above where they trade today. The broader trend is unambiguously downward, and the price chart reflects a name that has been under consistent distribution for the better part of the last twelve months.

The moving average picture reinforces that bearish read. Wiley is trading below both its 50-day moving average of $30.49 and its 200-day moving average of $36.49, meaning the stock is on the wrong side of both near-term and long-term trend lines. More significantly, the 50-day has crossed below the 200-day, producing what technicians call a death cross. This configuration is typically associated with sustained downside momentum rather than a temporary pullback, and the wide spread between the current price and the 200-day average of nearly $7.00 per share underscores just how far the stock has drifted from any constructive technical foundation. A recovery back to the 200-day would require a move of approximately 24% from current levels, which sets a high bar for near-term mean reversion.

The RSI reading of 53.05 is the one constructive data point in an otherwise cautionary technical picture. Sitting in the mid-range rather than in oversold territory, the momentum indicator suggests that the stock is not yet at an extreme where a sharp snapback becomes statistically probable. In practical terms, this means dividend investors who are watching for a capitulation-style flush before entering a position may need to remain patient, as the current RSI level does not indicate that sellers have fully exhausted themselves. Momentum is neither stretched to the downside nor showing any early signs of a bullish reversal, leaving the near-term path of least resistance ambiguous at best.

Taken together, the technical setup for Wiley is one that warrants caution rather than urgency for income-oriented buyers. The death cross, the position below both moving averages, and the stock’s proximity to a multi-year low all argue for waiting to see whether the $28.79 support level holds under pressure before committing new capital. Dividend investors who already own shares can draw some limited comfort from the fact that the RSI is not signaling a momentum-driven collapse, but the chart offers no clear evidence that a durable floor has formed. Price confirmation, in the form of a sustained hold above the 50-day moving average, would be the minimum technical hurdle worth watching before treating the current level as an attractive entry point.

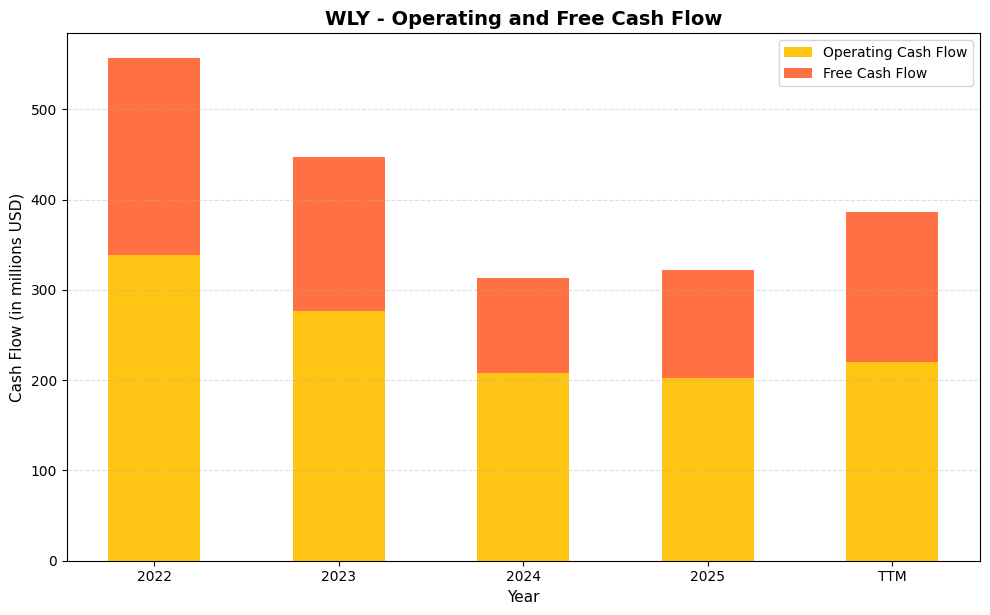

Cash Flow Statement

Wiley’s cash flow picture tells a story of compression followed by tentative stabilization. Operating cash flow peaked at $339.1M in 2022 and declined meaningfully through 2024, landing at $207.6M before recovering modestly to $220.1M on a trailing twelve month basis. Free cash flow followed the same arc, falling from $217.4M in 2022 to a trough of $105.9M in 2024, then rebounding to $166.8M TTM. That TTM free cash flow figure is the number dividend investors should anchor to, because it represents the actual cash available after capital expenditures to fund distributions, debt service, and any reinvestment. Wiley currently pays roughly $90M to $95M in annual dividends, which means free cash flow coverage sits at approximately 1.75x on a TTM basis. That is a workable ratio for a mature publishing and research services business, though it leaves less cushion than investors enjoyed when free cash flow was above $200M.

The multi-year decline from 2022 through 2024 largely reflects the disruptive transition Wiley undertook, including the divestiture of its test preparation business and the restructuring of its publishing segments, all of which pressured operating cash generation during an already unsettled period for academic and professional content providers. Capital expenditures have remained elevated relative to historical norms as the company invests in its research platforms, which explains why free cash flow contracted more sharply than operating cash flow over that stretch. The partial recovery visible in the TTM figures suggests those investments may be beginning to normalize, and if operating cash flow can trend back toward the $240M to $260M range over the next two fiscal years, free cash flow coverage would improve materially. For income investors, the current trajectory is cautiously encouraging rather than definitively reassuring, and continued monitoring of capex intensity and operating margin recovery will be essential to assessing whether the dividend sits on firmer footing going forward.

Analyst Ratings

Analyst coverage of Wiley is sparse at this point, with only a single firm maintaining formal coverage of the stock. That lone analyst carries a price target of $60.00, which implies roughly 104% upside from the current trading price of $29.35. The target has not moved recently, suggesting a steady conviction call rather than a reactionary position, and the implied upside is striking regardless of how conservatively one might discount a single-analyst consensus.

The $60.00 price target appears to reflect a view that Wiley’s transformation will ultimately be recognized in the stock price as digital revenues scale, margins improve, and the company’s AI licensing arrangements prove their commercial value. At a price-to-book of just 2.09 and a P/E of 15.7 times trailing earnings, the current valuation does not demand a heroic recovery scenario to justify meaningful upside.

The thin analyst coverage is itself a risk factor worth noting from a market dynamics perspective, as low coverage can mean that material developments take longer to get priced into the stock. For patient income investors, however, that dynamic can actually work in their favor, allowing positions to be built or maintained at prices that a more heavily followed stock would not sustain.

No recent formal analyst rating changes or price target revisions are on record as of this update. The single existing coverage continues to reflect a constructive view on Wiley’s long-term positioning within the academic research and AI content supply chain.

Earnings Report Summary

Improved Profitability Against a Challenging Revenue Backdrop

Wiley’s most recent reported financial results show a company that has made real progress on the bottom line even as top-line revenue faces ongoing headwinds from the structural shift in publishing. Total revenue on a trailing basis came in at $1.67 billion, down from prior-year levels as the company continues to shed lower-margin legacy businesses and transition volume toward digital formats. Net income, however, improved substantially to $101.7 million, translating to earnings per share of $1.87. That improvement reflects the cumulative benefit of cost restructuring, portfolio rationalization, and margin expansion in the Research segment.

The Research segment continues to anchor results, driven by open access publishing growth, AI content licensing revenue, and a broadening base of institutional subscription agreements. International deals, particularly in emerging research markets, have added to the subscription backlog and provide a degree of revenue visibility that is valuable during a period of broader uncertainty. Research submissions and content output trends have remained positive, suggesting the underlying pipeline of publishable work continues to grow.

Learning Segment Navigates Ongoing Softness

The Learning division has continued to face pressure from a softer academic market and the lingering absence of certain one-time licensing arrangements that boosted prior-year comparisons. While year-to-date performance has been supported by AI-related licensing contributions, the segment has not yet found a durable new growth driver to replace the volume lost from print and traditional courseware formats. Management has maintained its focus on margin efficiency within Learning, and that discipline is evident in the cost structure even when top-line results disappoint.

Outlook and Management Commentary

Management under CEO Matthew Kissner has maintained a consistent message around operational discipline, digital prioritization, and cash flow protection. The company’s profit margin of 6.11% on a trailing basis reflects a business that is generating real earnings while still absorbing transformation costs. Return on equity of 13.61% suggests the underlying business economics remain sound. Free cash flow guidance and EBITDA targets for the current fiscal year are expected to be consistent with the trailing performance, with management continuing to emphasize debt reduction and dividend stability as joint priorities going into fiscal 2026.

Management Team

John Wiley & Sons is led by Matthew Kissner, who has served as President and CEO since July 2024. Kissner brings a combination of deep institutional familiarity with Wiley and broad financial services experience, having previously held senior roles at Pitney Bowes, Bankers Trust, Citibank, and Morgan Stanley, along with private equity work focused on business, financial, and healthcare services. His long tenure within the Wiley ecosystem, including prior stints as Group Executive and Board Chair, gives him a clear-eyed view of where the company needs to go and what it will take to get there.

Christopher Caridi continues in the role of Interim Chief Financial Officer, a position he has held since September 2024. Caridi joined Wiley in 2017 after executive finance roles at Thomson Reuters and Reader’s Digest, and his background at PricewaterhouseCoopers gives him a rigorous accounting foundation. As Corporate Controller and Chief Accounting Officer prior to his interim CFO role, he built the global accounting infrastructure that now underpins the company’s financial reporting and cash management discipline.

The broader leadership team includes Jesse Wiley as Non-Executive Chairman, Danielle McMahan as Executive VP and Chief People Officer, and James Flynn as Executive VP and General Manager of Research and Learning. Together, this team is navigating Wiley through one of the most consequential transitions in its nearly 220-year history, with digital scale and AI-era content strategy at the center of the roadmap.

Valuation and Stock Performance

As of February 24, 2026, Wiley’s stock is trading at $29.35 per share, near the low end of its 52-week range of $28.38 to $47.26. The market capitalization stands at approximately $1.54 billion, a significant compression from where the stock was trading just twelve months ago. That decline has pushed the valuation into territory that looks genuinely inexpensive relative to the company’s cash generation capacity and the single analyst price target of $60.00.

The trailing P/E ratio of 15.7 times is a marked improvement from the elevated levels seen when earnings were depressed by restructuring charges, and at a price-to-book of 2.09 against book value of $14.05 per share, the stock does not carry an egregious premium to tangible assets. The beta of 0.96 suggests the stock trades roughly in line with the broader market from a volatility standpoint, which may surprise investors who associate the publishing sector with defensive, low-volatility characteristics.

The gap between the current price and the $60.00 analyst target is difficult to ignore, even accounting for the thinness of coverage. If the company continues to convert its restructuring progress into sustainable earnings improvement and the market begins to assign higher multiples to its digital and AI licensing revenue, the case for meaningful price appreciation alongside the 4.87% yield becomes more compelling. At current levels, the stock appears to be pricing in a fairly pessimistic scenario that may not match the operational reality of the business.

Risks and Considerations

The structural transformation of the academic publishing industry remains the most persistent risk facing Wiley. Open access mandates from research funders, growing competition from preprint platforms, and the ongoing commoditization of digital content delivery all challenge the traditional subscription model that has long underpinned Wiley’s revenue base. The company’s ability to monetize its content through AI licensing is promising, but the commercial terms and longevity of those arrangements are still being established across the industry, and there is no guarantee that current pricing levels will hold as more content becomes available to AI developers.

Wiley’s debt load continues to limit financial flexibility. While the company has been actively managing its debt stack and free cash flow covers the dividend comfortably, elevated leverage means that any sustained deterioration in operating cash flow would force difficult choices between debt service, dividend maintenance, and investment in digital growth initiatives. The current ratio and liquidity profile bear watching, particularly if interest rates remain elevated and refinancing becomes more expensive.

The company’s dependence on academic and institutional markets creates exposure to fluctuations in research funding, university budgets, and government education spending across its major geographies. Any meaningful pullback in library subscription budgets or a shift in how research institutions allocate resources could pressure the Research segment, which is currently the primary engine of earnings and cash flow. Currency risk is also relevant given Wiley’s international revenue base, with exchange rate movements capable of affecting reported results in ways that do not reflect underlying business performance.

Final Thoughts

John Wiley & Sons at $29.35 presents an unusual combination for dividend investors: a near-5% yield, a payout ratio that has returned to a manageable range on both an earnings and cash flow basis, and a stock trading at less than half the price target set by its lone covering analyst. The transformation is real, the cash flow is genuine, and the incremental dividend increases over the past two years demonstrate that management is not treating the payout as an afterthought during a difficult period.

The risks are meaningful and should not be dismissed, particularly around debt levels, competitive pressures in publishing, and the uncertain pace at which digital and AI licensing revenues will scale. But for an income investor with a two to three year horizon and a willingness to hold through ongoing transformation noise, the current setup at WLY offers a compelling entry point. The yield is high, the cash coverage is solid, and the downside from current prices appears more limited than at any point in the past year.