Updated 2/24/26

Jacobs Solutions Inc. operates at the intersection of engineering, infrastructure, and technology, serving a mix of public and private sector clients across the globe. The company has steadily built a reputation for delivering complex projects in sectors like transportation, energy, water, and life sciences. With a market cap of approximately $15.9 billion and a strong order backlog that continues to reflect healthy demand, Jacobs maintains resilience and forward momentum even amid shifting economic conditions.

Led by CEO Bob Pragada and a seasoned management team, Jacobs combines operational discipline with a strategic focus on high-growth areas. Recent financials reflect consistent revenue growth and healthy cash flow, while the dividend, now yielding just under 1%, has shown a meaningful upward trend with the most recent payment stepping up to $0.36 per share.

Recent Events

Jacobs Solutions has remained active on multiple fronts heading into early 2026. The company continues to win and execute on large-scale infrastructure and government contracts, with demand across its core verticals in water, transportation, life sciences, and advanced facilities remaining structurally elevated. Federal spending on infrastructure, combined with continued global investment in energy transition and environmental remediation, has kept Jacobs’ pipeline full and its backlog in strong shape.

The company also made a notable move in its capital return program. On February 20, 2026, Jacobs paid a quarterly dividend of $0.36 per share, representing a meaningful step up from the $0.32 per share paid throughout most of 2025. That increase signals management’s confidence in the durability of the company’s cash flows and its ongoing commitment to rewarding shareholders. The annualized rate now stands at $1.44, a figure that reflects a deliberate and accelerating approach to dividend growth.

On the broader strategic front, Jacobs continues to sharpen its focus following the earlier separation of its Critical Mission Solutions business into Amentum. That restructuring has allowed the company to concentrate resources on its highest-margin and fastest-growing segments, and the benefits are beginning to show up in free cash flow generation, which came in at over $1.08 billion on a trailing basis. Revenue reached $12.39 billion, reflecting continued momentum across the business.

Key Dividend Metrics

📈 Forward Dividend Yield: 0.97%

💰 Forward Annual Dividend Rate: $1.44

🧮 Payout Ratio: 33.77%

🔄 5-Year Average Yield: 0.75%

📅 Most Recent Ex-Dividend Date: February 20, 2026

💵 Last Dividend Payment: $0.36 per share

⏳ Trailing Yield: 0.97%

🔍 Dividend Growth: Accelerating and Well Covered

Dividend Overview

Jacobs isn’t trying to impress with a flashy dividend yield, and that’s entirely by design. The current yield of just under 1% won’t dominate a screen of high-income names, but it reflects something more meaningful: a company that prioritizes the sustainability and growth of its payout over the optics of a headline number.

The payout ratio sits at a comfortable 33.77%, which means Jacobs is retaining the majority of its earnings to reinvest in the business while still delivering consistent cash returns to shareholders. That ratio gives the company significant room to continue raising the dividend without straining its financials, even in quarters where earnings face one-time headwinds.

This approach makes Jacobs particularly appealing for investors who care more about dividend durability than immediate yield. The trajectory matters here. Looking at recent payment history, the quarterly dividend moved from $0.2151 in mid-2023 to $0.2399 in early 2024, then to $0.2871 later that year, followed by a jump to $0.3168 in early 2025, before settling at $0.32 for several quarters and then stepping up again to $0.36 in February 2026. That is a clear and consistent upward march that compounds meaningfully over time.

The annualized dividend of $1.44 represents the current baseline, and given the trajectory of the past several years, there is little reason to expect that growth stops here. Jacobs has demonstrated it will reward patient shareholders who hold through the modest yields on the way to a much higher cost-basis yield over time.

Dividend Growth and Safety

Jacobs has built a compelling track record of dividend growth over the past few years. From $0.2151 per quarter in 2023 to $0.36 per quarter as of February 2026, the company has grown its quarterly payment by roughly 67% in under three years. That is not the pace of a company treating its dividend as an afterthought. It reflects a board and management team that are systematically increasing capital returns as the business generates more free cash flow.

Safety is where Jacobs stands out most clearly. Free cash flow came in at approximately $1.09 billion on a trailing basis, which covers the total annual dividend obligation many times over. Operating cash flow of $960 million is equally reassuring. These figures confirm that the dividend is being paid from genuine operational strength rather than financial engineering or balance sheet maneuvers.

The payout ratio of 33.77% leaves substantial room for continued increases even if earnings experience some near-term volatility. With EPS at $3.80 and a $1.44 annual dividend, the coverage ratio is conservative and sustainable by any reasonable measure. The company’s beta of 0.77 also speaks to the lower-volatility nature of the stock, which tends to attract long-term, income-oriented shareholders who value consistency over excitement.

Institutional ownership remains dominant, reflecting the confidence that large, long-term capital allocators have in Jacobs’ fundamentals and management discipline. While the yield may not win over investors seeking immediate income, the combination of safety, consistent growth, and strong cash flow generation makes Jacobs a genuinely compelling dividend compounder for patient investors.

Chart Analysis

Jacobs Solutions has had a turbulent twelve months on the price chart, with shares carving out a wide range between the 52-week low of $108.63 and the 52-week high of $163.62. That nearly $55 spread tells the story of a stock that experienced meaningful selling pressure after reaching its peak, and the current price of $134.53 sits roughly 17.78% below that high-water mark. On the more constructive side, the stock has recovered about 23.84% from its 52-week trough, which suggests buyers have stepped in at lower levels and established at least a near-term floor. The broader price action, however, still reflects a market that has been reassessing the stock’s valuation after a period of relative strength earlier in the year.

The moving average picture reinforces the cautious near-term read. Jacobs is trading below both its 50-day moving average of $137.32 and its 200-day moving average of $140.05, meaning the stock has failed to reclaim either of those key technical thresholds. More concerning for trend followers is the presence of a death cross, a formation where the 50-day moving average crosses below the 200-day moving average, which is typically interpreted as a signal that intermediate-term momentum has shifted in favor of the bears. Both moving averages are now sitting above the current price, which means they may act as layers of overhead resistance on any attempted recovery. Dividend investors tracking re-entry points should watch closely for a sustained close above the $137 level as an early sign that conditions are beginning to stabilize.

The relative strength index reading of 51.64 places Jacobs in essentially neutral territory, straddling the midpoint of the 0 to 100 scale without showing signs of being either oversold or overbought. This reading tells us that the recent selling pressure has not been extreme enough to push the stock into deeply discounted momentum territory, which can sometimes precede sharp reversals. At the same time, the lack of any oversold condition means there is no immediate technical catalyst signaling that a bounce is imminent. The RSI in this range is consistent with a stock that is digesting losses and searching for directional conviction, rather than one that is coiling for a strong move in either direction.

For dividend investors, the chart presents a picture of a stock in a defined downtrend that has not yet shown the technical evidence of a meaningful reversal. The death cross, the position below both moving averages, and the neutral RSI together suggest patience is warranted before adding aggressively at current levels. That said, the recovery from the 52-week low and the stabilization of RSI near 50 indicate the situation is not deteriorating further at an accelerating pace. Income-focused investors who already hold the stock may find comfort in the fundamental dividend profile while the technicals work through this consolidation phase, but those looking to initiate a position would benefit from waiting for the price to reclaim its 50-day moving average as a minimum condition for improved technical confidence.

Cash Flow Statement

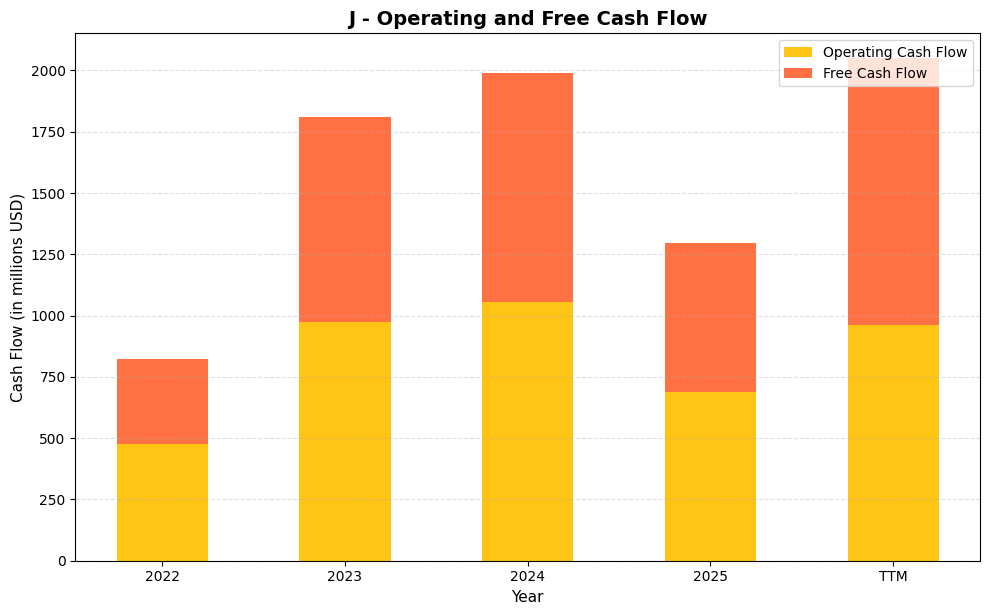

Jacobs Solutions has demonstrated a meaningful step-change in cash generation since 2022, with operating cash flow climbing from $474.7 million to a peak of $1,054.7 million in 2024 before settling to $686.7 million in 2025. Free cash flow followed a similarly impressive trajectory, rising from $347.1 million in 2022 to $933.6 million in 2024, and the TTM figure of $1,088.9 million actually surpasses the 2024 full-year operating cash flow total, a signal that capital expenditure requirements remain lean relative to the cash the business generates. For dividend investors, this matters because free cash flow is the true funding source for shareholder distributions, and a company consistently converting operating earnings into free cash at a high rate carries far less payout risk than one dependent on accounting income alone.

The broader trend across the period shown reflects a business that has become substantially more capital-efficient over time. The jump from $474.7 million in operating cash flow in 2022 to nearly $975 million in 2023 was not a one-year anomaly, as 2024 confirmed the higher run rate and the TTM figure reinforces it. The 2025 annual figure of $686.7 million looks softer in isolation, but the TTM free cash flow of $1,088.9 million suggests timing and working capital movements are at play rather than any structural deterioration. For shareholders, the combination of growing absolute free cash flow and relatively modest capital expenditure needs points to a company well-positioned to sustain dividend growth, fund share repurchases, and maintain financial flexibility without stretching its balance sheet to do so.

Analyst Ratings

The analyst community remains broadly constructive on Jacobs Solutions heading into late February 2026. Fifteen analysts cover the stock, and the consensus view is a buy. The mean price target sits at $157.53, which implies approximately 17% upside from the current price of $134.53. The range of estimates spans from a low of $137 to a high of $180, reflecting some divergence in views about the pace of recovery and the near-term earnings trajectory, but the central tendency is clearly bullish.

At the low end of the target range, the $137 figure is only modestly above the current price, suggesting that more cautious analysts are waiting for clearer earnings momentum before getting more aggressive. The mean of $157.53, however, represents a meaningful re-rating opportunity if Jacobs can execute on its backlog, sustain free cash flow growth, and continue demonstrating margin improvement across its core infrastructure and advanced facilities segments.

The $180 high target reflects the bull case scenario, where Jacobs benefits from a sustained infrastructure spending cycle, continued wins in life sciences and water, and further operational leverage as the post-Amentum business model matures. With the stock currently trading near the lower end of its 52-week range of $105.18 to $168.44, the risk-reward setup implied by analyst targets looks reasonably attractive, particularly for long-term investors who can tolerate some near-term price uncertainty.

Earning Report Summary

Jacobs Solutions has been operating in a revenue environment that reflects steady underlying demand across its key verticals. Full-year revenue reached $12.39 billion, a meaningful increase from prior periods and a sign that the company’s post-restructuring focus is beginning to show up in the top line. Net income came in at approximately $459 million, with earnings per share of $3.80, reflecting an improved operating environment relative to the prior year’s investment-related charges that had weighed heavily on reported results.

Top-Line Performance Holds Up

Revenue growth has been driven by continued strength in infrastructure spending, with the company’s Infrastructure and Advanced Facilities segment remaining the primary contributor. Demand from government clients across water, transportation, and environmental services has remained elevated, supported by federal infrastructure programs that continue to fund large, multi-year projects. Backlog levels remain robust, providing strong revenue visibility into fiscal 2026 and beyond.

Earnings and Margins Improving

The shift away from the prior year’s one-time investment charges has allowed reported earnings to normalize significantly. EPS of $3.80 represents a much cleaner picture of the company’s underlying profitability. Operating cash flow of $960 million and free cash flow exceeding $1.08 billion confirm that the earnings power of the business is genuine and not dependent on accounting adjustments. Profit margins at 3.50% reflect the services nature of the business but are supported by a volume and backlog profile that keeps cash generation well above reported net income.

Leadership Remains Optimistic

CEO Bob Pragada has continued to emphasize the quality and diversity of the company’s project pipeline, pointing to sustained momentum in life sciences, energy transition, and transportation as areas where Jacobs is winning high-value work. CFO Venk Nathamuni has reinforced the company’s commitment to strong cash conversion and responsible capital allocation, including the continued ramp in dividend payments as free cash flow generation improves.

Focused on Shareholder Value

Jacobs has remained active in returning capital to shareholders. The step-up in the quarterly dividend to $0.36, announced alongside the February 2026 payment, reflects confidence in the company’s ability to sustain and grow its cash returns. Share repurchases have also continued as part of the broader capital return framework, supporting earnings per share over time.

Outlook

Management has maintained a constructive posture on the forward outlook, citing strong demand across public and private sector clients, a healthy backlog, and improving operational efficiency. The company’s ability to convert more than 100% of net income into free cash flow, which has been demonstrated in the trailing twelve months, remains a key financial target and a significant source of confidence for dividend investors.

Management Team

Jacobs Solutions is led by Bob Pragada, who serves as both Chair and Chief Executive Officer. With over three decades of global business leadership and military experience, including 17 years with Jacobs and nine years as a Civil Engineer Corps and Seabees Officer in the U.S. Navy, Pragada brings a depth of experience and a steady hand at the helm. His tenure has been defined by a strategic commitment to reshaping Jacobs into a more focused, higher-margin business, and the results of that effort are increasingly visible in the company’s cash flow profile and capital return trajectory.

Venk Nathamuni, the Chief Financial Officer, plays a critical role in shaping the company’s financial direction and execution. His leadership in capital management and long-term planning continues to underpin Jacobs’ strategic decisions, including the disciplined approach to dividend growth and debt management that has characterized recent fiscal years. Joanne Caruso, as Chief Legal and Administrative Officer, helps ensure that the company operates with integrity and compliance across all its global operations.

Patrick Hill, President of Global Operations, oversees the implementation of major projects worldwide, while Shannon Miller leads as Strategy, Growth and Digital Officer, bringing a forward-thinking vision to Jacobs’ transformation and innovation efforts. Together, the executive team presents a blend of operational depth, financial rigor, and strategic foresight that has served the company well through a period of significant portfolio change.

The broader Board of Directors complements this leadership with a strong lineup of professionals from various industries. Individuals like Louis Pinkham and Priya Abani add diverse perspectives that help guide the company’s governance and long-term outlook.

Valuation and Stock Performance

Jacobs Solutions currently trades at $134.53, placing it meaningfully below its 52-week high of $168.44 and representing a discount of roughly 20% from that peak. The stock has recovered well from its 52-week low of $105.18, but remains in the lower half of its annual range, which creates an interesting entry point for investors who believe the company’s fundamental story remains intact.

The P/E ratio of 35.40 is not cheap in absolute terms, but it reflects the market’s willingness to assign a premium to a business with strong free cash flow generation, a large and growing backlog, and exposure to secular tailwinds in infrastructure, water, and energy transition. The price-to-book ratio of 4.59 against a book value of $29.29 per share similarly reflects a quality premium rather than a value trap. The market cap of approximately $15.9 billion places Jacobs squarely in large-cap territory.

The mean analyst price target of $157.53 implies roughly 17% upside from current levels, and the high target of $180 suggests the bull case is considerably more optimistic. For a stock trading near the bottom of its 52-week range with a consensus buy rating and a dividend that just stepped up to $0.36 per quarter, the current price appears to offer a reasonable margin of safety for long-term investors. The low beta of 0.77 further supports the case for Jacobs as a lower-volatility holding within a diversified income-growth portfolio.

Risks and Considerations

Jacobs carries some residual complexity from the separation of its Critical Mission Solutions business into Amentum. While that transaction was intended to sharpen the company’s strategic focus, the ongoing financial relationship with Amentum, including any mark-to-market exposure on retained interests, can introduce earnings volatility that is difficult to predict and may obscure the underlying operational performance of the core business.

The company’s global footprint exposes it to currency fluctuations, regulatory shifts in key markets, and geopolitical developments that can delay project starts or increase costs unexpectedly. These risks are inherent to any large engineering firm operating across dozens of countries, and Jacobs is not immune to the project execution risks that come with complex, multi-year government and commercial contracts.

Government budget dynamics represent a particular area of attention. A meaningful portion of Jacobs’ revenue is tied to public sector clients, including U.S. federal agencies and state and local governments. Any significant pullback in infrastructure appropriations or shifts in spending priorities could affect both revenue growth and backlog conversion rates. Labor market tightness in skilled engineering disciplines also continues to present cost pressures, and the company must continue investing in talent acquisition and retention to maintain execution quality on its growing project pipeline.

At a P/E of 35.40, the stock’s valuation leaves limited margin for earnings disappointment. If free cash flow growth stalls or if the company reports earnings that fall short of expectations, the multiple could compress meaningfully, creating downside risk even for long-term holders. Investors should weigh these considerations against the company’s strong cash generation and track record of disciplined capital allocation.

Final Thoughts

Jacobs Solutions offers a balanced and compelling picture for long-term dividend growth investors. It is a well-run company with an experienced leadership team, a diversified footprint across resilient sectors, and a dividend that has grown at an impressive pace over the past several years. The step-up to $0.36 per quarter in February 2026, representing a 67% increase from the $0.2151 quarterly payment of 2023, is a concrete demonstration of management’s commitment to rewarding shareholders.

With free cash flow exceeding $1.08 billion, a payout ratio of just 33.77%, and a consensus buy rating from 15 analysts with a mean price target of $157.53, the fundamental case for Jacobs is straightforward. The stock’s current position near the lower half of its 52-week range provides a reasonable entry point for investors with a multi-year horizon. For those who value consistency, responsible management, and a dividend that is growing faster than the yield headline suggests, Jacobs deserves a close look.