Key Takeaways

💰 ITW carries a 2.12% dividend yield with 52 consecutive years of dividend growth, supported by a 59.29% payout ratio and a per-share annual dividend now at $6.44.

💵 The company generated $2.17 billion in free cash flow over the trailing twelve months, comfortably covering dividend obligations and ongoing share repurchases.

📊 Analyst sentiment leans cautious, with a consensus hold rating and a mean price target of $278.62, sitting below the current trading price of $294.56.

Updated 2/24/26

Illinois Tool Works, with a history that stretches back to 1912, has built its reputation on consistency, margin strength, and a disciplined approach to growth. Operating through a decentralized structure across seven segments, the company serves a broad range of industries from automotive to food equipment. Its long-standing dividend track record, coupled with solid cash flow and operational efficiency, makes it a compelling option for income-focused investors.

The company reported $16.04 billion in trailing twelve-month revenue alongside $10.50 in earnings per share, maintaining strong margins and a return on equity that remains exceptionally high at 93.72%. With $2.17 billion in free cash flow, a 59.29% payout ratio, and a dividend now running at $6.44 per share annually, ITW continues to execute on its shareholder-first strategy while navigating a mixed macroeconomic backdrop.

Recent Events

Illinois Tool Works has been navigating a period of measured resilience as it moves through the early months of 2026. The company has remained active on the capital return front, continuing its pattern of share buybacks alongside its steadily growing dividend. The most recent quarterly dividend payment of $1.61 per share reflects the increase that took effect in the second half of 2025, when ITW lifted its quarterly rate from $1.50 to $1.61, representing a roughly 7.3% step up and extending the company’s remarkable streak of consecutive annual dividend increases to 52 years.

On the operational front, ITW has continued to lean into its 80/20 simplification framework, focusing resources on its highest-return product lines while reducing complexity across segments. This approach has historically protected margins during periods of softer demand, and management has shown no signs of abandoning it. The company’s seven business segments, spanning automotive OEM, food equipment, welding, construction products, and specialty products, continue to benefit from this discipline even as certain end markets face uneven demand conditions.

Broader industrial sentiment has been shaped by persistent uncertainty around global trade policy, particularly as tariff discussions continue to influence sourcing and manufacturing decisions in the automotive and construction segments. ITW’s global footprint means currency movements in Europe and Asia remain a variable worth watching, and the company’s exposure to automotive production cycles keeps it tethered to some of the more volatile corners of the industrial economy.

Key Dividend Metrics

💵 Forward Dividend Yield: 2.12%

📈 5-Year Average Yield: 2.21%

🔁 Dividend Growth Streak: 52 consecutive years

📅 Most Recent Ex-Dividend Date: December 31, 2025

💰 Annual Dividend (Forward): $6.44 per share

🧮 Free Cash Flow Coverage: Fully covered by $2.17B in FCF

📊 Payout Ratio: 59.29%

🏦 Most Recent Dividend Payment: $1.61 per share

Dividend Overview

Illinois Tool Works isn’t trying to chase headlines with aggressive payouts or flashy moves. Instead, it simply delivers, a trait that long-term income investors can truly appreciate.

The company’s current forward yield sits at 2.12%, a touch below its five-year average of 2.21%, which reflects the stock’s strong price appreciation over the past year as shares have climbed toward the upper end of their 52-week range. That compression in yield is the natural result of a rising share price outpacing dividend growth, not any deterioration in the underlying payout. The annual dividend now stands at $6.44 per share, up from $6.00 previously, following the mid-2025 increase that moved the quarterly rate from $1.50 to $1.61.

The payout ratio of 59.29% sits higher than ITW’s historical norms but remains well within a manageable range given the company’s consistent earnings and cash generation. With $2.17 billion in free cash flow against a dividend obligation that runs well below that figure, the payout is secure. Institutional ownership remains high, reinforcing confidence that the company’s capital return program is viewed as durable rather than discretionary.

Dividend Growth and Safety

When it comes to dividend safety, ITW continues to check the important boxes, even as the payout ratio has moved modestly higher.

It starts with profitability. A return on equity of 93.72% and return on assets of 17.05% reflect a business that converts capital into earnings with exceptional efficiency. These are not numbers that appear in companies struggling with dividend sustainability. The profit margin of 19.11% across $16 billion in revenue underscores the operating leverage built into ITW’s model, and it helps explain why management has been able to grow the dividend through multiple economic cycles without interruption.

Dividend growth has averaged in the mid-to-high single digits annually over the past several years, and the most recent increase of approximately 7.3% fits squarely within that range. Management’s long-term EPS growth target of 7% to 10% provides a credible runway for continued increases, assuming end-market conditions remain broadly stable. The balance sheet does carry a meaningful debt load, as evidenced by the elevated price-to-book ratio and modest book value per share of $11.18, but ITW has managed leverage strategically for decades and the operating cash flow of $3.13 billion leaves ample room to service obligations while rewarding shareholders.

Chart Analysis

Illinois Tool Works has staged an impressive recovery over the past year, climbing from a 52-week low of $214.37 to its current price of $294.56, a gain of roughly 37% from trough to present. That kind of price appreciation in a diversified industrial compounder reflects genuine institutional accumulation, not just sector rotation noise. The stock is now within striking distance of its 52-week high of $299.60, sitting just 1.68% below that level, which tells you the market is assigning a high-conviction valuation to ITW’s earnings power and capital return profile heading into the next phase of the cycle.

The moving average picture is unambiguously constructive. The 50-day moving average has crossed above the 200-day moving average, forming what technicians call a golden cross, a configuration that historically signals sustained upward momentum rather than a short-lived bounce. With the 50-day currently at $266.33 and the 200-day at $254.00, and the stock trading at $294.56, ITW is running well clear of both trend lines. That kind of stacked alignment, where price sits above the 50-day, which sits above the 200-day, is the technical setup dividend growth investors want to see when initiating or adding to a position.

Momentum is elevated, with the 14-day RSI registering 70.74, nudging into technically overbought territory. For pure traders, that reading can signal a short-term pause or modest pullback is possible. For dividend investors with a multi-year horizon, a brief consolidation near current levels would actually be a healthier outcome than a parabolic extension, as it would allow the moving averages to catch up and establish a firmer support base beneath the share price. The RSI reading reflects genuine buying pressure rather than speculative excess, given that the move has been built on a full year of steady accumulation.

The overall technical picture for ITW is favorable for income-oriented investors who are comfortable entering a name near its highs. The trend is well-established, the moving average structure is supportive, and the proximity to the 52-week high suggests price discovery is happening at the upper end of the valuation range rather than in distressed territory. Investors considering a new position may want to watch for any short-term pullback toward the $280 area as a more conservative entry, though those already holding shares have every reason to feel the technical backdrop is confirming the fundamental thesis.

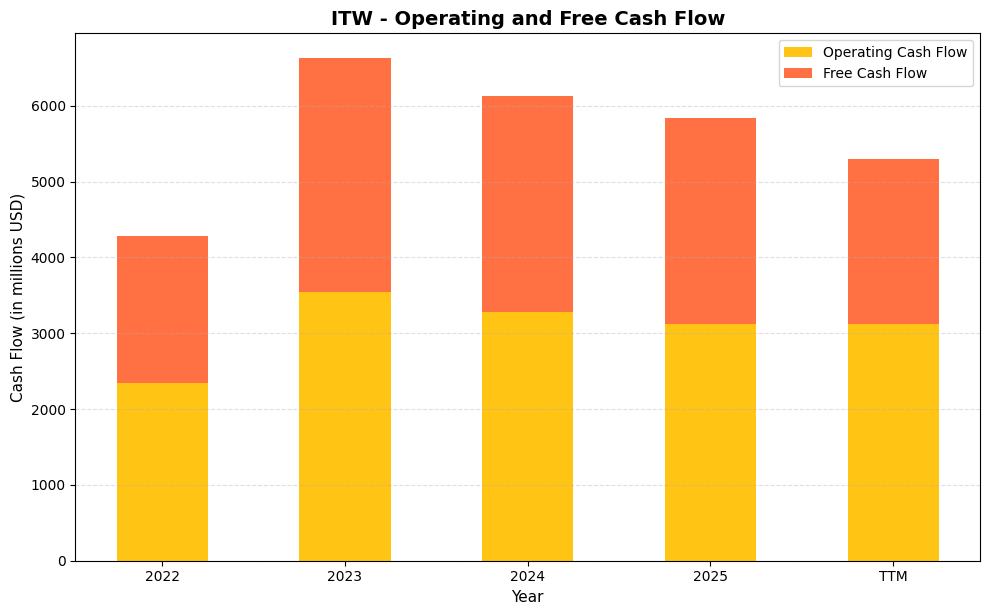

Cash Flow Statement

Illinois Tool Works generates the kind of free cash flow that dividend investors dream about. Operating cash flow climbed sharply from $2,348.0 million in 2022 to a peak of $3,539.0 million in 2023, a jump of over 50% in a single year that reflected strong margin execution and working capital discipline. The company has settled into a more normalized range since then, with operating cash flow of $3,281.0 million in 2024 and $3,126.0 million in 2025. Free cash flow has followed a similar trajectory, reaching $3,084.0 million in 2023 before moderating to $2,844.0 million in 2024 and $2,707.0 million in 2025. Even at these “moderated” levels, ITW is converting an enormous share of its earnings into actual cash, which is the foundation of a durable and growing dividend. The TTM free cash flow figure of $2,166.7 million reflects some timing differences relative to the full fiscal year, but the underlying cash generation capacity of this business is not in question.

Zooming out across the full period shown, the trend tells a compelling story about capital efficiency. The 2022 base of $1,936.0 million in free cash flow was already well above what most industrial peers produce, yet ITW expanded that figure by nearly 60% over the following year before allowing it to gradually normalize as capital spending patterns shifted. The company’s asset-light, 80/20-simplified operating model keeps capital expenditures relatively modest, which means a high percentage of operating cash flow flows straight through to free cash flow. In 2025, ITW converted roughly 86% of its operating cash flow into free cash flow, a ratio that speaks to tight operational controls and limited reinvestment requirements at the segment level. For shareholders, this means the dividend, the share repurchase program, and any bolt-on acquisition capacity are all drawing from a deep and reliable pool of cash, one that has grown substantially since 2022 even after the post-2023 normalization.

Analyst Ratings

The analyst community has maintained a cautious stance on Illinois Tool Works heading into early 2026. The consensus rating across 16 analysts sits at hold, reflecting a view that the stock’s strong price performance over the past year has brought valuation into a range that limits near-term upside. The mean price target of $278.62 sits meaningfully below the current trading price of $294.56, suggesting that at current levels the average analyst sees the stock as modestly extended relative to intrinsic value estimates.

The range of price targets tells a more nuanced story. The low-end target of $219.00 reflects concerns about cyclical exposure and the possibility of earnings pressure if industrial demand softens further, while the high-end target of $312.00 reflects confidence in ITW’s margin discipline and cash flow durability. The stock’s current price of $294.56 sits near the top of that range, which helps explain the overall hold consensus. Investors considering a new position at current prices are essentially betting that ITW can grow into its valuation through continued earnings expansion, rather than expecting multiple expansion to do the heavy lifting.

Earning Report Summary

A Mixed Start to the Year

Illinois Tool Works closed out the most recent reporting period with results that reflected its characteristic margin strength even against a backdrop of softer top-line growth. Trailing twelve-month revenue of $16.04 billion reflects the scale of the business, though growth has been modest as several end markets, particularly automotive and construction, have faced uneven demand conditions. Earnings per share of $10.50 represent solid absolute profitability, and the net income figure of $3.07 billion confirms that the business continues to convert revenue into bottom-line results at an enviable rate.

Segment Performance: A Mixed Bag

ITW’s decentralized segment structure means performance varies considerably across the business. Automotive OEM has continued to face pressure from softer North American and European production volumes, though international markets have provided partial offsets. Food equipment has demonstrated more resilience, with service revenues holding up well. Construction products remain among the more challenged areas given the rate-sensitive nature of that end market, while welding and specialty products have been relatively stable. The company’s 80/20 simplification strategy continues to protect margins across segments, even where volumes have disappointed.

Cash Flow and Capital Moves

Operating cash flow of $3.13 billion for the trailing twelve months demonstrates that ITW’s earnings translate reliably into cash, a critical factor for dividend investors assessing sustainability. Free cash flow of $2.17 billion reflects higher capital expenditures relative to prior periods, though the absolute level remains sufficient to fund dividends and repurchases. The company has continued executing on its share buyback program, reducing the share count and providing a per-share earnings tailwind that supports continued dividend growth even in periods of modest revenue expansion.

Looking Ahead

Management has maintained a disciplined tone around capital allocation and margin targets, consistent with ITW’s long-standing operating philosophy. The company’s 80/20 framework, combined with its focus on enterprise initiatives that have historically contributed meaningful basis points of margin improvement, positions it to defend profitability even if top-line growth remains muted. Free cash flow is expected to continue exceeding dividend requirements, and management’s commitment to the annual dividend increase streak shows no signs of wavering. The primary question heading into the back half of 2026 is whether end-market demand stabilizes enough to support a return to organic revenue growth.

Management Team

Illinois Tool Works is led by a deeply experienced leadership group that reflects stability and a strong understanding of its decentralized operating model. E. Scott Santi serves as Chairman and CEO, having been with the company since the early 1980s. His leadership has been instrumental in maintaining ITW’s long-standing strategy of operational efficiency and disciplined growth. His familiarity with the business and long-term vision has helped guide the company through a variety of economic cycles.

Supporting Santi is CFO Michael Larsen, who has proven adept at managing the company’s finances with a focus on strong cash flow and capital allocation. The broader executive team includes specialists overseeing ITW’s seven diverse segments, such as Automotive OEM, Construction Products, and Polymers & Fluids. Their collective approach emphasizes autonomy and accountability at the business unit level, which has long been a hallmark of ITW’s culture. This setup continues to support innovation, responsiveness to customer needs, and steady profitability across market cycles.

Valuation and Stock Performance

Illinois Tool Works is currently trading at $294.56, near the upper end of its 52-week range of $214.66 to $303.16. The stock has staged a substantial recovery from its lows, and that price appreciation has pushed valuation metrics into territory that warrants attention from income investors evaluating entry points. The trailing P/E of 28.05 reflects a premium relative to ITW’s historical averages, and the price-to-book ratio of 26.36 is elevated, though the latter is partly a function of the company’s aggressive share repurchase history rather than an absence of underlying asset value.

The mean analyst price target of $278.62 sits roughly 5.4% below the current price, which is an unusual position for a stock with a hold consensus, as it implies modest downside to consensus fair value estimates. The high-end target of $312.00 offers limited upside from current levels, while the low-end target of $219.00 suggests meaningful downside risk if cyclical conditions deteriorate. For dividend investors, the math at current prices produces a 2.12% yield, which is slightly below ITW’s five-year average, reflecting the price appreciation that has compressed the yield modestly. The stock is best understood as a quality compounder trading at a full valuation, appropriate for patient long-term holders but less compelling as a new purchase for those prioritizing immediate yield.

Risks and Considerations

Illinois Tool Works operates across several cyclical end markets, including automotive, construction, and general manufacturing, which means its revenue and earnings remain sensitive to the broader industrial demand cycle. A sustained slowdown in global manufacturing activity or a contraction in automotive production could weigh on organic growth across multiple segments simultaneously, limiting the company’s ability to offset weakness in any single area.

Currency exposure is a persistent consideration given ITW’s global revenue base. The company generates a meaningful portion of its sales outside the United States, and exchange rate movements in Europe and Asia can create headwinds to both reported revenue and earnings, independent of underlying business performance. This has been a recurring factor in recent quarters and is unlikely to disappear as a variable in the near term.

The company carries a substantial debt load relative to its book value, a condition that reflects decades of share repurchases and leverage management rather than operational distress, but one that nonetheless reduces financial flexibility in a rising rate environment. The modest book value per share of $11.18 against a share price of $294.56 illustrates how aggressively capital has been returned over the years, and while cash flow coverage is strong, any sustained deterioration in earnings would narrow the margin of safety on the balance sheet.

Dividend growth investors should also be mindful that the payout ratio has moved higher, reaching 59.29% on trailing earnings. That level is still manageable, but it leaves less room than ITW has historically maintained, meaning that future dividend increases will depend more directly on continued earnings growth rather than ratio compression as a safety buffer. If earnings growth stalls, the pace of dividend increases could moderate further, which may not align with the expectations of investors who have grown accustomed to mid-to-high single digit annual raises.

Final Thoughts

Illinois Tool Works remains a steady name in the industrial landscape. Its leadership team, decentralized structure, and strong margins continue to differentiate it from peers. The dividend growth streak now stands at 52 consecutive years, the most recent increase brought the annual rate to $6.44 per share, and free cash flow continues to support that commitment with room to spare. Those are not small accomplishments for a company operating across as many diverse end markets as ITW does.

The stock is not cheap at current levels, and the analyst consensus reflecting a mean target below the trading price is a signal worth taking seriously. For existing holders, the case for staying the course remains intact given the quality of the business and the durability of the dividend. For investors evaluating a new position, patience may be rewarded by waiting for a more favorable entry point, particularly given that the yield at $294.56 sits slightly below the five-year average. As long as the company maintains its operational discipline and continues growing earnings in the mid-single-digit range, it is likely to remain a fixture in long-term, income-oriented portfolios.