Key Takeaways

💸 IBM offers a forward dividend yield of 3.00% and has raised its dividend for 29 consecutive years, backed by consistent free cash flow that comfortably covers the annual payout.

💼 The company generated $13.19 billion in operating cash flow and $12.77 billion in free cash flow over the trailing twelve months, reflecting disciplined capital spending and durable cash generation.

📊 Analysts maintain a buy consensus across 19 firms, with a mean price target of $324.95, well above the current trading price of $229.32, suggesting meaningful upside is being priced in over the medium term.

Updated 2/24/26

IBM has spent the past several years quietly repositioning itself around hybrid cloud, artificial intelligence, and enterprise software. Under the leadership of CEO Arvind Krishna, the company has made measurable progress with platforms like Red Hat and watsonx, while continuing to generate reliable free cash flow and maintain its nearly three-decade streak of dividend increases.

Backed by solid operating metrics and a growing presence in generative AI, IBM remains at the intersection of innovation and income. At the current price of $229.32, the stock has pulled back notably from its 52-week high of $324.90, creating a more attractive entry point for dividend growth investors who have been watching from the sidelines.

Recent Events

IBM has seen meaningful stock price weakness over the past several months, with shares sitting at $229.32 after touching a 52-week high of $324.90. That pullback of more than 29% from peak levels reflects a broader reassessment of large-cap technology valuations, as well as some investor caution around near-term growth expectations in enterprise IT spending. For long-term dividend investors, the decline has pushed the yield back up to 3.00%, the most attractive level it has been in some time relative to the recent trading range.

On the business front, IBM has continued advancing its AI agenda through the watsonx platform, which remains central to the company’s pitch to enterprise customers. The hybrid cloud narrative, anchored by Red Hat and OpenShift, continues to gain traction as large organizations look for ways to manage workloads across on-premise and cloud environments without ceding control to a single hyperscaler. IBM’s positioning as a neutral, enterprise-grade AI and cloud partner has resonated with a segment of the corporate market that values reliability over novelty.

The dividend itself continues its steady march forward. The most recent quarterly payment of $1.68 per share was made on February 10, 2026, consistent with the prior three quarters. IBM has now raised its dividend for 29 consecutive years, a streak that has survived multiple recessions, a major business restructuring, and the divestiture of its managed infrastructure services segment. That kind of consistency is not accidental, and it reflects a deliberate capital allocation philosophy that Krishna and his team have reinforced throughout the current transition.

Key Dividend Metrics

🧮 Forward Dividend Yield: 3.00%

📈 5-Year Average Yield: 4.50%

💰 Forward Annual Dividend: $6.72 per share

📆 Payout Ratio: 60.23%

🏆 Dividend Growth Streak: 29 consecutive years

📊 Last Ex-Dividend Date: February 10, 2026

📅 Last Payment Date: February 10, 2026

Dividend Overview

At 3.00%, IBM’s current yield is the most compelling it has looked in quite a while. The 5-year average yield of 4.50% tells you that the stock spent much of the recent past trading at lower prices relative to its dividend, and today’s yield sits closer to that historical norm than it did when shares were near $324. For investors who missed the run-up, the current price offers a more reasonable starting yield with the potential for price recovery built in.

IBM is paying $6.72 per share annually, structured as four quarterly payments of $1.68. With roughly 934 million shares outstanding, that represents a substantial cash commitment each year, one the company has demonstrated it can sustain through both growth periods and downturns.

The payout ratio has improved considerably and now stands at 60.23%, a much more comfortable picture than the elevated levels seen in prior periods when earnings were suppressed. With EPS of $11.15 over the trailing twelve months, IBM is covering its $6.72 annual dividend with genuine earnings power rather than relying entirely on cash flow to make up the gap. That said, cash flow remains the more telling metric for dividend safety, and operating cash flow of $13.19 billion against a total dividend outlay of roughly $6.3 billion leaves an enormous buffer.

Free cash flow of $12.77 billion tells much the same story. IBM is generating cash at nearly twice the rate it needs to pay dividends, and the remaining free cash flow after distributions supports continued investment in AI infrastructure, acquisitions, and debt management. The dividend is not just sustainable at current levels, it has room to keep growing.

Dividend Growth and Safety

IBM’s 29-year consecutive dividend growth streak is one of the more underappreciated stories in the technology sector. The company has raised its payout through the dot-com bust, the financial crisis, years of revenue decline, a major corporate spin-off, and now a full-scale business transformation centered on AI and hybrid cloud. The consistency of that commitment reflects how deeply the dividend is embedded in IBM’s identity as a shareholder-focused enterprise.

The growth in the dividend itself has been measured rather than aggressive. Looking at the recent history, IBM moved from $1.66 per quarter in early 2023 to $1.67 in mid-2024, and then to $1.68 beginning in May 2025, where it has remained through the February 2026 payment. That is a modest pace of increase, but it is increase nonetheless, and it is being delivered against a backdrop of genuine business transformation rather than stagnation.

With a payout ratio of 60.23% and free cash flow of $12.77 billion, the safety profile of IBM’s dividend is solidly above average for a company of its size and complexity. The shift toward recurring revenue from software subscriptions and AI services continues to add predictability to the cash flow mix, which is exactly what dividend investors want to see underlying a multi-decade payout commitment.

IBM’s beta of 0.69 reflects a stock that moves less aggressively than the broader market in either direction. For income-focused investors, that lower volatility is a meaningful characteristic, particularly during periods of market turbulence when dividend payers often attract capital from more speculative names. IBM’s combination of moderate yield, consistent growth, and below-market volatility makes it a genuinely defensive component within a technology-sector allocation.

Chart Analysis

IBM has endured a sharp reversal over the past year, sliding from a 52-week high of $313.19 down to a current price of $229.32, a drawdown of roughly 26.78% from peak levels. The stock is now trading just 6.33% above its 52-week low of $215.67, which tells you how compressed the trading range has become on the downside. What began as a strong uptrend through much of the prior year has clearly broken down, and the price action in recent months reflects genuine seller conviction rather than a routine consolidation. For dividend investors accustomed to IBM’s historically stable chart behavior, the speed and depth of this decline is meaningful context.

The moving average picture confirms the deterioration in trend. IBM is currently trading well below both its 50-day moving average of $290.81 and its 200-day moving average of $277.11, meaning the stock sits approximately 19.6% beneath its 50-day and roughly 17.3% beneath its 200-day. That kind of separation from both major trend lines signals that the damage is not superficial. The one constructive technical footnote is that the 50-day moving average still sits above the 200-day, preserving what is technically classified as a golden cross formation from an earlier period of strength. However, if the current price weakness persists, those two averages could converge and potentially invert, which would shift the longer-term trend signal from neutral to bearish.

The RSI reading of 20.51 is the most striking data point on the chart. A reading that far below the conventional oversold threshold of 30 indicates that selling pressure has been relentless and that IBM is now in deeply oversold territory by almost any standard measure. Historically, RSI readings at these extremes can precede at least a technical bounce or period of stabilization, as sellers become exhausted and short-term buyers step in to capture what appears to be a discounted entry. That said, oversold conditions can persist longer than expected when the underlying narrative driving the selloff remains unresolved, and investors should not treat a low RSI as a standalone buy signal.

For dividend investors, the chart presents a classic tension between price risk and income opportunity. The significant pullback from highs has mechanically pushed IBM’s yield higher, which may attract income-focused buyers who are comfortable owning the stock at these levels for the long term. The proximity to the 52-week low around $215 suggests that level could serve as a meaningful technical support zone worth monitoring. Investors who are considering a position would be well served by watching whether IBM can stabilize near current levels and begin reclaiming ground toward its moving averages before adding meaningful exposure, given that the trend, at this moment, remains decidedly against the bulls.

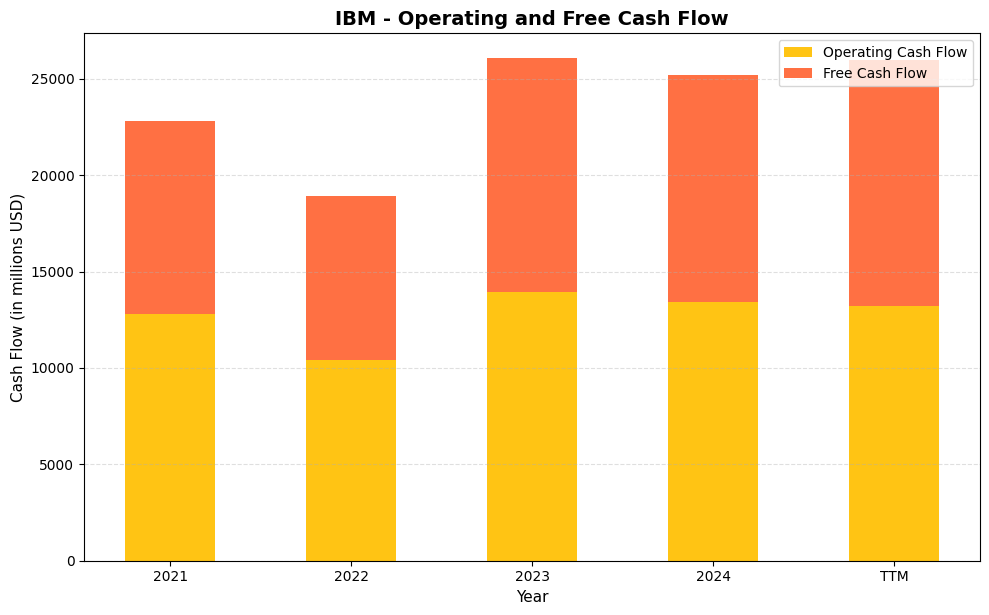

Cash Flow Statement

IBM’s cash flow profile is one of the more compelling parts of the investment case for dividend investors. Operating cash flow dipped from $12,796 million in 2021 to $10,435 million in 2022, a period that reflected integration costs and portfolio repositioning following the Kyndryl spinoff. The business then rebounded sharply to $13,931 million in 2023 and has held near that level, printing $13,445 million in 2024 and $13,193 million on a trailing twelve-month basis. Free cash flow tells an even more encouraging story. After falling to $8,463 million in 2022, it climbed to $12,121 million in 2023, came in at $11,760 million in 2024, and has since expanded to $12,771 million on a TTM basis. IBM’s annual dividend obligation runs roughly $6 billion, which means free cash flow is currently covering the dividend at better than 2x. That is a wide and comfortable margin of safety for income investors.

The multi-year trajectory here reflects a company that has meaningfully improved its capital efficiency after shedding the low-margin managed infrastructure business through the Kyndryl spinoff. Capital expenditures have remained disciplined, hovering well below the gap between operating and free cash flow, which signals that IBM is not sacrificing investment to manufacture a favorable free cash flow number. The 2022 trough now looks like a one-time reset rather than a structural deterioration, and the recovery to consistently above $11 billion in annual free cash flow over the past two years reinforces that view. For shareholders, this level of cash generation supports not only the current dividend but also IBM’s stated commitment to growing the payout over time, while still leaving room for bolt-on acquisitions in the hybrid cloud and AI infrastructure space that management has prioritized as the next phase of the growth strategy.

Analyst Ratings

The analyst community is broadly constructive on IBM, with a consensus buy rating across 19 covering firms. The mean price target of $324.95 sits roughly 42% above the current price of $229.32, which is an unusually wide gap for a large-cap technology company with a stable operating profile. That spread suggests analysts believe the recent pullback from the 52-week high has created a meaningful valuation opportunity, particularly given IBM’s improving earnings quality and free cash flow generation.

Price targets range from a low of $218.00, which sits just below the current trading price and reflects the more cautious view that near-term growth headwinds in consulting and infrastructure could persist, to a high of $390.00 among the most optimistic forecasters who are pricing in accelerating AI adoption and software segment expansion. The distribution of targets skews decisively toward the upside, with the mean and high both implying substantial appreciation from current levels.

The breadth of that range captures the genuine debate around IBM’s transition trajectory. Bulls argue that the combination of watsonx AI deployments, Red Hat’s continued growth, and a more favorable earnings base creates a compelling re-rating opportunity. Bears point to consulting softness, competitive pressure from hyperscalers, and the stock’s elevated Price/Book of 6.58 as reasons for caution. With no recent analyst actions available, the consensus price target of $324.95 remains the clearest signal of where the Street sees fair value once near-term uncertainty clears.

Earning Report Summary

A Solid Start to the Year

IBM’s most recent full-year results reflect a business that has found its footing in a more challenging IT spending environment. The company reported EPS of $11.15 on revenue of $67.53 billion, with a profit margin of 15.69% that reflects genuine improvement in the quality of IBM’s earnings mix. Return on equity of 35.16% is a standout figure, demonstrating that IBM is generating substantial value from its asset base even as it continues to invest in next-generation capabilities.

The software segment remains the primary growth engine, driven by Red Hat and the broader hybrid cloud platform. OpenShift and the associated middleware portfolio have continued to attract enterprise customers who need a consistent operating environment across on-premise data centers and multiple cloud providers. This is a stickier revenue profile than IBM’s legacy hardware cycles, and it provides the recurring cash flow that supports both continued investment and the dividend commitment.

Consulting and Infrastructure Dynamics

Consulting has faced ongoing pressure as enterprise customers have become more selective about discretionary project spending. This is a theme that has played out across the IT services sector, and IBM has not been immune to the caution. Infrastructure, while cyclical by nature, is approaching a new mainframe cycle with the z17 platform, which has been architected with embedded AI capabilities as a core design principle rather than an afterthought. That transition creates both near-term caution and medium-term optimism as customers plan upgrade cycles.

IBM’s total AI business, tracked since the company began disclosing the category, has continued to accumulate at a meaningful pace. The watsonx platform has become the primary vehicle for enterprise AI deployments where data governance, explainability, and integration with existing workflows are priorities. These are not characteristics that appeal to every buyer, but they align well with regulated industries and large enterprises that cannot simply migrate to consumer-oriented AI tools.

Looking Ahead

With free cash flow of $12.77 billion and a payout ratio now comfortably below 65%, IBM’s financial foundation supports continued dividend growth alongside ongoing business investment. The company has consistently communicated a capital allocation framework that prioritizes the dividend, followed by targeted acquisitions and debt management. Operating cash flow of $13.19 billion confirms that the underlying cash generation capacity remains intact even as reported earnings fluctuate with restructuring and acquisition-related charges.

CEO Arvind Krishna has maintained a consistent message around IBM’s long-term positioning, emphasizing that enterprise AI adoption is a multi-year cycle and that IBM’s differentiation lies in trust, security, and integration depth rather than raw model performance. CFO James Kavanaugh has continued to reinforce the free cash flow framework as the primary lens through which IBM’s financial health should be evaluated, a perspective that income investors are well positioned to appreciate.

Management Team

IBM’s leadership is anchored by Arvind Krishna, who serves as Chairman and Chief Executive Officer. Since taking the helm in 2020, Krishna has played a central role in driving the company’s evolution toward hybrid cloud infrastructure and AI-driven solutions. His focus has been on reshaping IBM to better align with the future of enterprise technology, including automation, cybersecurity, and data platforms. The consistency of IBM’s strategic messaging under Krishna has been one of the more underrated aspects of the company’s recovery, giving institutional investors a clear framework against which to evaluate progress.

Working alongside him is James Kavanaugh, IBM’s Senior Vice President and Chief Financial Officer. Kavanaugh has been pivotal in executing the company’s financial strategy while supporting innovation-led investment. He brings a pragmatic approach to managing IBM’s balance sheet and cash flow, ensuring that even during periods of transformation, shareholder returns and financial stability remain priorities. His emphasis on free cash flow as the defining metric of IBM’s financial health has been a consistent thread through every earnings call and investor presentation.

Together, Krishna and Kavanaugh form a leadership team that emphasizes long-term vision while staying grounded in operational discipline. Their efforts to shift IBM’s business mix toward software and AI services, and away from legacy hardware dependency, reflect a leadership mindset that is focused on relevance and reinvention without abandoning the shareholder return commitments that have defined IBM for decades.

Valuation and Stock Performance

IBM shares are trading at $229.32, down substantially from the 52-week high of $324.90 and sitting closer to the low end of the 52-week range of $214.50 to $324.90. That positioning changes the valuation conversation considerably compared to where it stood when the stock was near peak levels. At the current price, the trailing P/E of 20.57 is a meaningful discount to where IBM was being valued just a few months ago, and it compares favorably to many large-cap technology peers that still carry elevated multiples.

The Price/Book of 6.58 against a book value per share of $34.86 reflects IBM’s intangible-heavy business model, where the value lies in software platforms, client relationships, and intellectual property rather than hard assets. Return on equity of 35.16% justifies a premium to book, as IBM is generating strong returns from the capital base it has assembled through years of investment and restructuring.

With a mean analyst price target of $324.95 and the stock at $229.32, the implied upside of roughly 42% is the most compelling it has been in several years. Free cash flow of $12.77 billion against a market cap of approximately $214 billion implies a free cash flow yield of nearly 6%, which is an attractive starting point for investors evaluating total return potential. At current levels, IBM offers an unusual combination of a 3.00% dividend yield, below-market beta of 0.69, and meaningful price appreciation potential if the company continues executing on its AI and hybrid cloud strategy.

Risks and Considerations

IBM operates in one of the most competitive segments of the technology industry, where hyperscalers like Microsoft, Amazon, and Google are investing tens of billions of dollars annually in cloud and AI infrastructure. IBM’s enterprise positioning and hybrid cloud focus offer some differentiation, but sustaining that differentiation requires continuous investment, talent retention, and a product roadmap that keeps pace with rapidly evolving customer expectations. Any slowdown in AI adoption among enterprise customers, or a shift in procurement preferences toward hyperscaler-native solutions, could pressure IBM’s software growth rates more than current forecasts anticipate.

Consulting represents a meaningful portion of IBM’s revenue, and the softness in discretionary project spending that has characterized recent quarters may persist longer than expected if enterprise IT budgets remain constrained. A prolonged period of consulting weakness would put additional pressure on overall revenue growth and could slow the pace of margin improvement that analysts are currently projecting.

IBM’s balance sheet carries a substantial debt load, and while the company’s cash generation is more than sufficient to service that debt at current interest rates, any meaningful increase in refinancing costs or a deterioration in operating cash flow could create pressure on capital allocation priorities. The company’s ability to continue growing the dividend while also investing in AI capabilities and managing debt obligations depends on maintaining the free cash flow trajectory that has been established over the past several years.

Finally, IBM’s international revenue exposure creates sensitivity to currency fluctuations and geopolitical developments. A strengthening dollar relative to major currencies where IBM generates significant revenue, particularly in Europe and Asia, can create headwinds to reported results even when underlying business performance is solid. Macro uncertainty, trade policy changes, and regional economic slowdowns all represent variables that IBM’s management team must navigate carefully alongside the internal execution challenges of ongoing business transformation.

Final Thoughts

IBM at $229.32 is a materially different investment proposition than IBM at $324.90. The business has not changed, the dividend has not been cut, and the strategic direction remains intact. What has changed is the price, and with it, the yield has moved back to 3.00%, the P/E has compressed to a more reasonable 20.57, and the free cash flow yield has climbed to nearly 6%. For dividend growth investors, that combination of improved entry metrics and a 29-year consecutive growth streak is difficult to ignore.

The transformation narrative under Arvind Krishna has progressed consistently, and IBM’s financial results now reflect a company that has genuinely shifted its center of gravity toward software and AI rather than simply describing the intention to do so. The payout ratio of 60.23% and free cash flow coverage of approximately two times the annual dividend commitment represent the healthiest dividend safety profile IBM has shown in several years.

Challenges remain, particularly in consulting and the competitive dynamics of enterprise AI, but IBM has demonstrated the operational discipline and cash generation capacity to manage through those headwinds while continuing to reward shareholders. For investors who value the combination of income, modest volatility, and participation in the enterprise AI cycle, the current price represents one of the more attractive setups IBM has offered in recent memory.