Key Takeaways

💰 Humana’s dividend yield stands at 1.95%, supported by a conservative payout ratio of 33.12% and a multi-year history of consistent quarterly payments, reflecting the company’s ongoing commitment to returning capital to shareholders.

💵 Operating cash flow came in at $921 million over the trailing twelve months, with free cash flow reaching approximately $1.32 billion, providing baseline coverage for the current dividend obligation.

📊 Analyst consensus sits at “Hold” across 24 firms, with a mean price target of $223.88 against a current price of $174.64, implying meaningful upside on paper but tempered by significant near-term uncertainty in Medicare Advantage.

Updated 2/24/26

Humana Inc. remains one of the largest players in the Medicare Advantage market, but the company is navigating one of the more difficult stretches in its recent history. The stock has fallen sharply from its 52-week high of $315.35 and is now trading near multi-year lows around $174.64, reflecting persistent pressure from elevated medical costs, reimbursement challenges, and a broader reset in managed care valuations. Despite these headwinds, the dividend remains intact, cash flow continues to cover the payout, and the leadership team installed over the past two years is pressing forward with a leaner, more focused operating model.

The yield at current prices has climbed to 1.95%, which is elevated relative to Humana’s historical norms and reflects just how far the stock has pulled back. For dividend growth investors willing to assess the business on a longer time horizon, the combination of a low payout ratio, manageable debt, and a dominant position in government-sponsored healthcare still presents a case worth examining carefully.

Recent Events

Humana has been at the center of ongoing industry-wide turbulence in Medicare Advantage, and the stock’s continued slide toward its 52-week low of $169.61 reflects how seriously the market is weighing those concerns. The company’s deliberate exit from underperforming Medicare Advantage markets, which began under CEO Jim Rechtin in 2024, has continued to reshape its membership profile heading into 2026. While this strategic retreat has trimmed enrollment numbers, management has consistently framed it as a necessary step toward restoring margin discipline rather than a sign of competitive retreat.

The broader Medicare Advantage sector has been under pressure from the Centers for Medicare and Medicaid Services, with rate updates and star rating adjustments creating meaningful uncertainty around bonus payments that many insurers, including Humana, depend on for profitability. Humana’s CMS star ratings have remained a focal point for investors, as any further deterioration would reduce the company’s ability to offer competitive plan benefits and attract new members. The company has been investing in clinical programs and care coordination tools through its CenterWell division in an effort to improve quality scores over time.

On the operational side, Humana’s Medicaid business and its CenterWell primary care and pharmacy operations have continued to develop as secondary growth drivers. These segments represent a meaningful diversification away from pure insurance risk and into care delivery, a shift that management views as central to the company’s long-term value proposition. The transition has required sustained capital investment, which partly explains the compression in operating cash flow relative to peak levels seen in prior years.

Key Dividend Metrics

📈 Dividend Yield: 1.95%

💵 Annual Dividend: $3.54 per share

📅 Last Dividend Paid: $0.885 per share (December 26, 2025)

📊 Payout Ratio: 33.12%

🔁 Dividend Trend: Flat since early 2023, holding at $0.885 per quarter

🔒 Dividend Safety: Covered by free cash flow, though operating cash flow has compressed meaningfully

Dividend Overview

At 1.95%, Humana’s yield is the highest it has been in years, and that elevation is entirely a function of price decline rather than any increase in the dividend itself. The quarterly payment has held steady at $0.885 per share since early 2023, meaning the company has not grown its payout in roughly three years. For investors who bought the stock at higher prices, that stagnation can feel frustrating. For those entering at today’s levels, the yield is more attractive on a relative basis than it has been at any recent point in the company’s history.

The payout ratio of 33.12% based on reported earnings of $10.69 per share tells a reasonably reassuring story about coverage. The company is not stretching itself to maintain the current payment, and there is a meaningful buffer between what it earns and what it distributes. That said, the sharp decline in operating cash flow to $921 million, down significantly from the $2.87 billion reported in the prior period, is a number that demands attention. Free cash flow of approximately $1.32 billion provides some additional comfort, but the direction of cash generation is something investors should monitor closely as results continue to roll in.

Humana’s book value per share of $146.42 against a current price of $174.64 means the stock is trading at just 1.19 times book, which is an unusually compressed multiple for a company of its scale. This is not a REIT or a utility built to distribute the majority of its earnings, but the combination of a low price-to-book ratio and a nearly 2% yield does reframe the dividend in a more income-friendly light than the headline yield alone might suggest.

Dividend Growth and Safety

The dividend growth story at Humana has effectively paused. From early 2023 through the most recent payment in December 2025, the quarterly rate has remained fixed at $0.885. That represents a meaningful shift from the consistent annual increases the company delivered throughout the prior decade, and it reflects the financial pressures that have defined the Medicare Advantage landscape over this period. Management has not signaled a cut, but it has also not provided guidance on when or whether increases might resume.

Safety, in the narrow sense of whether the dividend is at risk of being reduced, appears manageable for now. The payout ratio is conservative at 33%, and free cash flow of $1.32 billion is sufficient to cover the annual dividend obligation of roughly $430 million based on current share count. The concern is not that Humana cannot afford the current payment, but rather that the trajectory of earnings and cash flow needs to stabilize before any resumption of growth becomes realistic. Operating cash flow at $921 million is the lowest figure in recent memory for the company, and a sustained decline from here would begin to compress that safety margin more meaningfully.

Return on equity of 7.04% and return on assets of 4.30% are respectable figures for a managed care company dealing with elevated medical cost ratios, but they are below the levels Humana has historically generated. The profit margin of 0.92% on $129.7 billion in revenue is characteristic of the industry, where high volumes and thin margins are the norm, but the direction of that margin is what matters most in the near term. A recovery in the benefit ratio and a normalization of utilization trends would go a long way toward restoring both earnings power and the foundation for future dividend growth.

Chart Analysis

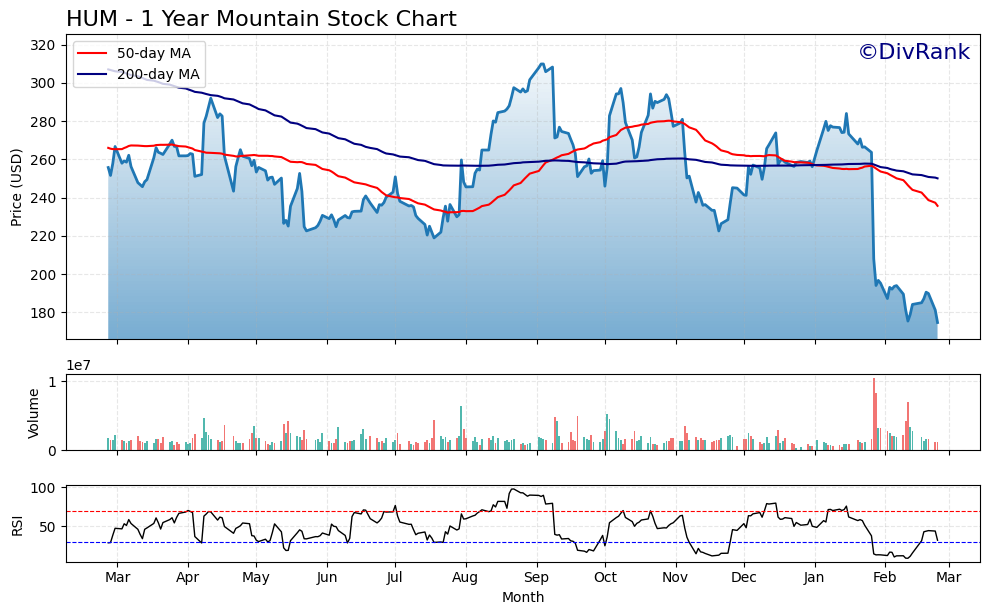

Humana’s chart tells a difficult story over the past twelve months. The stock has shed roughly 44% from its 52-week high of $309.85, and as of the current session it is sitting precisely at its 52-week low of $174.64, meaning there is no technical floor of recent memory beneath today’s price. That kind of sustained, uninterrupted selling pressure reflects more than a routine pullback. It signals a market that has persistently repriced the fundamental earnings outlook for the business, and income investors considering a position here need to take that message seriously before treating the current level as an obvious entry point.

The moving average picture reinforces the bearish trend. Humana’s 50-day moving average sits at $235.66 and its 200-day moving average sits at $250.04, both well above the current price of $174.64. The stock is trading roughly 26% below its 50-day average and nearly 30% below its 200-day average, which illustrates just how far price has disconnected from its own longer-term trend lines. The 50-day has crossed below the 200-day, forming what technicians call a death cross, a configuration that typically confirms a stock is in a sustained downtrend rather than a short-term dip. Until the 50-day begins curling upward and price can reclaim at least the $235 area, the moving average structure offers no constructive signals for buyers.

Momentum indicators are deeply oversold but not yet showing a convincing reversal. The 14-day RSI registers at 32.44, just above the conventional oversold threshold of 30. A reading this low can precede a reflexive bounce, particularly when a stock is also touching a multi-month low, but an oversold RSI alone is not a buy signal. In a stock under this degree of fundamental pressure, the RSI can remain in oversold territory for an extended period or briefly recover before resuming its decline. Investors who have acted on low RSI readings during Humana’s descent over the past year have consistently found lower prices ahead.

For dividend investors, the chart presents a challenging setup. The stock is at a fresh 52-week low with no visible technical support, sitting well below both key moving averages in a confirmed downtrend, and momentum has not yet produced any sign of stabilization. That combination argues for patience over urgency. While the elevated yield that comes with a sharply lower price may appear attractive, the technical picture suggests the market is still in the process of finding a fair value for Humana under its revised earnings expectations. Waiting for price to base and for the 50-day moving average to at least flatten before committing new capital would be a more prudent approach for income-focused investors.

Cash Flow Statement

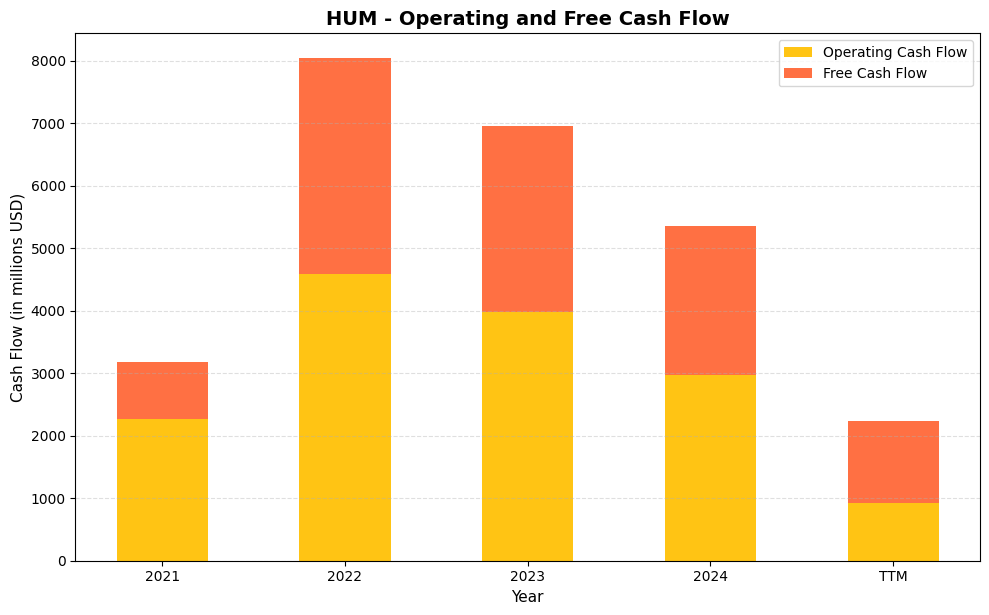

Humana’s cash flow profile tells a story of meaningful volatility over the past four years, and the TTM figures demand careful attention from income investors. Operating cash flow peaked at $4,587.0M in 2022 before declining to $3,981.0M in 2023 and $2,966.0M in 2024, and the trailing twelve months have compressed further to just $921.0M. Free cash flow followed a similar arc, cresting at $3,450.0M in 2022 and stepping down to $2,977.0M in 2023, $2,391.0M in 2024, and now $1,321.3M on a TTM basis. The TTM free cash flow figure still covers Humana’s annual dividend obligation, which runs roughly $700M to $750M at current payout levels, but the margin of safety has narrowed considerably from the comfortable coverage ratios the company enjoyed just two years ago. Investors who anchor their dividend confidence to the 2022 peak should recalibrate around the current run rate.

The broader four-year arc reflects the pressures Humana has faced across its Medicare Advantage business, where rising medical cost ratios have eaten into the operating earnings that ultimately translate into cash generation. The 2021 to 2022 jump from $2,262.0M to $4,587.0M in operating cash flow was exceptional, driven by favorable claims timing and strong enrollment growth, and that baseline was always unlikely to persist. Capital expenditures have remained relatively modest, running in the $400M to $600M range annually, which means the compression in free cash flow is primarily a cash earnings problem rather than a capital spending problem. That distinction matters because it points to the income statement as the source of pressure rather than a strategic investment cycle that might eventually reverse. For dividend growth investors, the near-term priority is stabilization in the MLR and a recovery in operating earnings, both of which management has flagged as central to its 2025 and 2026 outlook. Until that recovery materializes in the cash flow statement, dividend growth is likely to remain on pause.

Analyst Ratings

Twenty-four analysts currently cover Humana, and the consensus sits at a “Hold,” a designation that captures the genuine ambivalence many on the sell side feel about the stock at this juncture. The mean price target of $223.88 represents upside of roughly 28% from the current price of $174.64, which is a meaningful gap and suggests that the analyst community broadly believes the stock is trading below fair value. The wide range of targets, from a low of $146.00 to a high of $344.00, is itself telling. Bears see a scenario where the stock has further to fall, while bulls are anchored to a recovery narrative that assumes Humana’s strategic repositioning plays out successfully over the next twelve to eighteen months.

The low end of the target range at $146.00 sits below the current 52-week low of $169.61, indicating that at least one analyst sees the possibility of additional downside if medical cost trends do not improve or if CMS reimbursement adjustments come in worse than expected. The high end at $344.00 reflects a scenario where the company’s margin recovery accelerates and the market rewrites the multiple higher. The current price of $174.64 is closer to the bear case than the bull case, which at minimum suggests the market is pricing in a significant probability of continued operational difficulty rather than a smooth recovery. For income investors, the practical takeaway is that the dividend appears sustainable at current levels, but the stock itself is not widely viewed as a near-term catalyst.

Earning Report Summary

A Year Defined by Operational Reset

Humana’s most recently reported full-year results showed revenue of $129.7 billion, a figure that reflects the company’s enormous scale in government-sponsored healthcare. Net income came in at $1.19 billion, translating to earnings per share of $10.69. While the top line remains substantial, the profit margin of just under 1% underscores how much the earnings story has changed from the stronger years of 2021 and 2022. The compression is largely attributable to elevated medical cost ratios in Medicare Advantage, where utilization has run above actuarial assumptions for an extended period, and the company has had limited ability to immediately reprice to offset those trends.

Strategic Repositioning in Focus

CEO Jim Rechtin has continued to position the membership exit strategy as the right long-term call, even as it has contributed to near-term revenue and enrollment headwinds. The logic is straightforward: plans that were generating losses or thin margins were dragging on the overall book, and removing them creates a cleaner base from which to rebuild profitability. The CenterWell segment, encompassing primary care, home health, and pharmacy, has been highlighted as a growing contributor that differentiates Humana from pure-play insurers by integrating care delivery with coverage.

Full-year guidance and forward commentary from management have emphasized cost discipline and a measured approach to re-entering markets once pricing conditions improve. The company is not chasing membership growth for its own sake, which is a philosophically different posture than what drove the industry’s aggressive expansion in prior years. Whether that discipline translates into a meaningful earnings recovery in 2026 will depend heavily on how medical cost trends evolve and whether CMS rate updates provide adequate support for the Medicare Advantage product. Investors are watching both variables closely, and the results of the next few quarters will go a long way toward determining whether the current stock price represents a genuine long-term entry point or a value trap in progress.

Management Team

Jim Rechtin, who became CEO in mid-2024, has now had roughly eighteen months to put his operational fingerprints on Humana. His background at Envision Healthcare and OptumCare gave him a care delivery perspective that distinguishes him from executives who came up primarily through the insurance side of the business. That orientation is visible in how the company has talked about its strategic priorities, with clinical quality, cost management, and care integration featuring prominently in investor communications. The membership exit decisions and the continued buildout of CenterWell both reflect his influence on the direction of the enterprise.

Celeste Mellet, who joined as Chief Financial Officer in early 2025, brings a background in infrastructure investing and investment banking that is somewhat unconventional for a managed care CFO. Her presence signals that Humana’s board wanted someone with a rigorous capital allocation lens at a time when the company needs to make careful decisions about where to invest and where to pull back. Her public commentary has focused on financial discipline and aligning the company’s spending with its most durable growth opportunities.

Michelle O’Hara continues in the Chief Human Resources Officer role, with a focus on workforce development and internal culture during what has been a period of meaningful organizational change. The leadership team as a whole is relatively new in its current configuration, and the degree to which it can execute consistently over the next several quarters will be central to restoring investor confidence in both the operating story and the stock’s ability to recover from its current depressed levels.

Valuation and Stock Performance

Humana’s stock is trading near the bottom of its 52-week range, with a current price of $174.64 sitting just above the low of $169.61 and well below the high of $315.35 reached earlier in the period. The decline from peak to trough represents a loss of roughly 45% in share price, which is a striking compression for a company generating nearly $130 billion in annual revenue. The market capitalization has fallen to approximately $21 billion, a figure that reflects just how much sentiment has shifted against the managed care sector broadly and Humana specifically.

On a price-to-earnings basis, the stock trades at 16.34 times trailing earnings of $10.69 per share, which is not an obviously expensive multiple but needs to be evaluated in the context of whether those earnings are at a trough or represent a new normal. The price-to-book ratio of 1.19 is the more compelling valuation data point, as it places the stock at a level where the market is assigning only a modest premium to the company’s stated net asset value. For a business with Humana’s brand, market position, and infrastructure in Medicare Advantage, that is a historically low implied valuation.

The analyst mean price target of $223.88 implies that a significant portion of the sell side views the current price as an overshoot to the downside. Whether that recovery materializes in the near term depends on factors largely outside the company’s direct control, including CMS reimbursement decisions and macroeconomic influences on healthcare utilization. The beta of 0.44 indicates that Humana tends to move less than the broader market, which can be reassuring for income investors who prioritize stability over capital gains but who still want their positions to participate in any sector recovery.

Risks and Considerations

Humana’s dependence on Medicare Advantage as its primary earnings driver creates a concentrated exposure to federal reimbursement policy that few other large-cap companies face to the same degree. The Centers for Medicare and Medicaid Services sets the payment rates that underpin the economics of every plan Humana offers, and changes to those rates, whether through annual benchmark updates or adjustments to the risk adjustment methodology, can have an immediate and material effect on profitability. The company’s experience over the past two to three years is a real-time illustration of how quickly margins can compress when government pricing does not keep pace with actual medical cost inflation, and there is no guarantee that future rate cycles will be more favorable.

The trajectory of medical cost utilization is the most important operational variable in Humana’s near-term outlook and also one of the least predictable. Elevated inpatient and outpatient utilization has persisted longer than the company and its actuaries initially projected, and any further deterioration in the medical cost ratio would put additional pressure on earnings and cash flow. If operating cash flow continues to decline from the $921 million level reported most recently, the cushion between cash generation and the dividend obligation would narrow in a way that would eventually demand a response from management.

The company’s CMS star ratings remain a source of ongoing risk. Plans that fall below four stars lose access to quality bonus payments that can represent a meaningful percentage of total revenue, and they also become less competitive from a benefit design standpoint. Humana has been working to improve its quality scores through clinical investment, but the ratings methodology is complex and the results are not always proportionate to the effort or spending involved. A further decline in star ratings in the near term would compound the existing financial pressures and make the membership recovery story harder to execute.

The competitive environment in Medicare Advantage has also not softened. UnitedHealth Group, CVS Health through Aetna, and a growing number of regional and national competitors continue to invest aggressively in the market. Humana’s deliberate membership reductions have ceded some ground that will need to be recaptured on more favorable terms, and there is execution risk in that process. Finally, the broader economic environment, including labor cost pressures within the healthcare delivery system, creates an ongoing cost challenge that flows through the benefit ratio and affects margins in ways that are difficult to fully offset through pricing alone.

Final Thoughts

Humana is a company trading at a genuine inflection point, and the current price near multi-year lows captures how much uncertainty the market is pricing into its outlook. The dividend, at $3.54 annually and a yield of 1.95%, is covered by free cash flow and supported by a payout ratio that leaves room for the payment to survive a period of continued earnings pressure. The growth of that dividend, however, has been on hold since early 2023, and resumption depends on a recovery in operating performance that has not yet materialized in a convincing way.

For dividend growth investors with a long time horizon and an appetite for sector-specific volatility, the combination of a historically low price-to-book multiple, a nearly 2% yield, and a structurally important position in Medicare Advantage presents a case that is harder to dismiss than the current stock price might suggest. The risks are real and well documented, but so is the company’s scale, its leadership team’s focus on operational discipline, and the long-term demographic tailwind that underpins demand for Medicare products. Humana requires patience and a tolerance for further short-term turbulence, but for investors who do their homework on the managed care sector, it remains a name worth following closely as its turnaround thesis develops throughout 2026.