Key Takeaways

HP Inc. shares have fallen sharply over the past year, now trading near their 52-week low of $18.01, creating a notably elevated dividend yield of 6.31% for income investors willing to look past near-term pressure.

📈 HP offers a 6.31% forward dividend yield with a payout ratio of 43.68%, supported by consistent dividend increases and strong free cash flow generation.

💵 The company generated $3.70 billion in operating cash flow and $2.39 billion in free cash flow over the trailing twelve months, maintaining solid cash efficiency despite a difficult demand environment.

🧐 Analysts maintain a consensus rating of “Hold” with a mean price target of $23.21, suggesting meaningful upside from current levels even as macro headwinds keep sentiment cautious.

Updated 2/24/26

HP Inc. has spent much of the past year under significant pressure, with the stock declining from a 52-week high of $35.28 to trade near its 52-week low of $18.01 as of late February 2026. For income investors, that selloff has created an unusually attractive entry point, pushing the forward dividend yield to 6.31%, nearly double where it stood a year ago. The company continues to generate substantial free cash flow, and management has kept the dividend growing through the turbulence.

CEO Enrique Lores remains focused on AI-enabled PC adoption and supply chain diversification, twin priorities that define HP’s medium-term strategic posture. With revenue crossing $55 billion on a trailing basis and a payout ratio comfortably below 50%, HP’s dividend appears well anchored even as the stock navigates one of its more difficult stretches in recent memory.

Recent Events

HP Inc. has been navigating a challenging stretch as the PC hardware market contends with slowing corporate refresh cycles and macroeconomic uncertainty. The stock has been one of the weaker performers in the technology sector over the past twelve months, shedding more than half its value from the 52-week high of $35.28 to its current price near $18.20. That kind of drawdown reflects broader concerns about PC demand softness and margin compression rather than any specific operational collapse.

On the product side, HP has continued to push its AI-enabled PC lineup as the central pillar of its Personal Systems strategy. CEO Enrique Lores has been vocal about the company’s goal of expanding AI PC shipments as a percentage of total volume, positioning HP to benefit from the inevitable commercial refresh cycle that AI-capable hardware typically drives. The company has also made meaningful progress on manufacturing diversification, reducing its dependence on Chinese production facilities ahead of potential trade policy shifts.

The most recent quarterly dividend payment of $0.30 per share, paid in December 2025, marked a step up from the prior quarterly rate of $0.289, confirming that management remains committed to dividend growth even as the stock price has weakened considerably. That increase, while modest in absolute terms, signals confidence in the underlying cash generation of the business and keeps HP on its multi-year streak of annual dividend raises.

Key Dividend Metrics

📈 Forward Dividend Yield: 6.31%

💰 Annual Dividend Rate: $1.20

📆 Last Dividend Payment: $0.30 (December 2025)

📊 Payout Ratio: 43.68%

💎 52-Week Price Range: $18.01 – $35.28

🔍 EPS (TTM): $2.65

Dividend Overview

HP’s dividend yield of 6.31% stands out sharply, not just relative to the broader technology sector but relative to HP’s own recent history. That elevated yield is largely a function of the steep price decline the stock has suffered over the past year rather than any change in the underlying dividend program. For investors who can separate the noise of price volatility from the fundamentals of the payout, the current setup is genuinely compelling.

At an annualized rate of $1.20 per share, based on the most recent quarterly payment of $0.30, the dividend is well covered by both earnings and free cash flow. The 43.68% payout ratio against trailing EPS of $2.65 leaves HP with ample room to absorb earnings variability without putting the dividend at risk. The company does not need to stretch to fund this payout; it flows naturally from the cash the business generates in the ordinary course of operations.

Free cash flow of $2.39 billion over the trailing twelve months provides the clearest window into dividend sustainability. Against an annual dividend obligation that, at the current share count, runs well under $1.5 billion, HP retains meaningful excess capital after paying the dividend. That surplus has historically been allocated toward share repurchases and debt management, both of which have remained consistent features of the capital return program.

The current ratio and balance sheet carry some concentration in debt, a characteristic that is not unusual for a company of HP’s scale and operating model. However, the strength and consistency of operating cash flow generation provides a reliable backstop, and the company has not shown signs of prioritizing debt reduction over shareholder returns in any way that would threaten the dividend trajectory.

Dividend Growth and Safety

HP raised its quarterly dividend from $0.289 to $0.300 per share effective with the December 2025 payment, continuing what has now become a reliable pattern of annual increases. Looking back through the recent dividend history, the progression is clear and consistent: $0.263 in early 2023, $0.276 starting in late 2023, $0.289 beginning in late 2024, and now $0.300 as of late 2025. Each step has been modest, but the direction has never wavered, which matters enormously to investors building a long-term income stream.

The safety of HP’s dividend rests on the payout ratio sitting below 45% and on free cash flow that covers the total dividend obligation with room to spare. Even in a scenario where earnings declined meaningfully from current levels, the payout ratio would remain manageable. HP is not a company that funds its dividend by drawing down cash reserves or by adding to its debt load; it is funded through genuine operating profitability and consistent cash conversion.

Institutional ownership remains elevated, reflecting ongoing confidence from large investors in HP’s capital return discipline. High institutional ownership historically correlates with management accountability around shareholder-friendly policies, and HP has done nothing to undermine that trust. The dividend has grown every year since the company became a standalone entity in 2015, a track record that carries real weight when evaluating long-term income reliability.

HP’s beta of 1.20 reflects a stock that moves with the broader market but is not among the most volatile technology names. For income investors, that moderate beta means dividend reinvestment can occur at reasonably predictable price levels without the whipsaw risk that accompanies higher-growth tech names. The current environment, with shares near a multi-year low, creates a situation where reinvested dividends are accumulating shares at an attractive cost basis.

The broader narrative around HP’s dividend is one of deliberate, unsexy dependability. Management has not chased headline-grabbing dividend increases, nor has it allowed the payout to stagnate. The result is a dividend program that has quietly compounded investor income over the better part of a decade, and that trajectory shows no structural signs of reversal.

Chart Analysis

HPQ has endured a punishing year of price deterioration, shedding more than 44% from its 52-week high of $32.65 to trade at $18.20, which also happens to be the precise 52-week low. That convergence of current price and annual floor is a meaningful signal on its own, indicating that buyers have not yet stepped in with enough conviction to establish any meaningful base. For dividend investors accustomed to holding through volatility, the sheer magnitude of this drawdown warrants serious attention rather than casual dismissal as routine noise.

The moving average picture reinforces the bearish technical narrative. HPQ is trading below both its 50-day moving average of $20.90 and its 200-day moving average of $24.57, and the 50-day has crossed below the 200-day to form what technicians call a death cross. That configuration signals that the shorter-term selling pressure has become entrenched enough to drag the trend baseline lower, which typically precedes continued softness rather than a swift recovery. The gap between the current price and the 200-day average alone represents roughly 35%, meaning HPQ would need a substantial and sustained rally just to reclaim what most analysts consider a neutral technical posture.

The RSI reading of 42.7 sits in moderately oversold territory without quite reaching the sub-30 levels that often attract contrarian buyers hunting for capitulation. That middle-ground reading is in some ways more cautious than an extreme oversold print, because it suggests the stock is weak but not yet washed out, leaving room for further downside before a technical floor firms up. Momentum has not shown the kind of positive divergence that would hint at a near-term reversal, and with price sitting exactly at its 52-week low, there is no established chart support below current levels to speak of.

For dividend investors, the technical picture argues for patience over urgency. The income thesis around HPQ’s yield may look more compelling as the price compresses, but a deteriorating chart with a death cross, no visible support, and price at a one-year low is not a setup that rewards rushing in. Investors already holding the position for the dividend may choose to hold and collect distributions, but those considering a new position would be well served to wait for price to stabilize above the 50-day moving average before treating the technical environment as anything close to constructive.

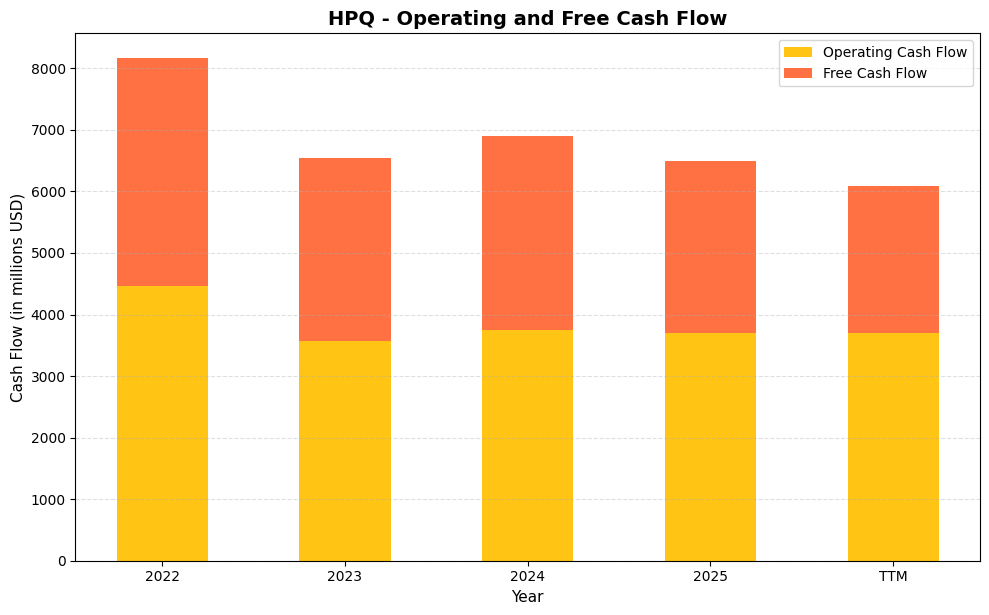

Cash Flow Statement

HP Inc. has demonstrated a reasonably stable free cash flow profile over the past several years, which forms the foundation of its dividend sustainability story. Operating cash flow peaked at $4,463.0 million in fiscal 2022 before settling into a tighter range of $3,571.0 million to $3,749.0 million through fiscal 2023 and 2024, and came in at $3,697.0 million in fiscal 2025. Free cash flow followed a similar arc, declining from $3,698.0 million in 2022 to $2,978.0 million in 2023, recovering modestly to $3,157.0 million in 2024, and then pulling back to $2,800.0 million in 2025. On a trailing twelve-month basis, free cash flow stands at $2,394.5 million, which reflects increased capital spending relative to recent periods. With HP’s annualized dividend obligation running well below the free cash flow line, the payout remains comfortably covered, and dividend investors have little immediate reason for concern about distribution continuity.

Zooming out across the full data set, what stands out is the compression in free cash flow relative to operating cash flow, which signals that capital expenditures have been gradually consuming a larger share of internally generated funds. In 2022, the gap between operating and free cash flow was $765.0 million, but on a TTM basis that spread has widened to $1,302.5 million, pointing to a more capital-intensive operating posture. This is not unusual for a company investing in product refresh cycles and manufacturing capabilities, but it does mean shareholders should monitor whether capex intensity continues to rise or begins to normalize. The core takeaway for income investors is that HP still generates substantial free cash flow in absolute terms, enough to fund dividends, share repurchases, and modest debt management simultaneously, though the cushion has narrowed somewhat from the highs seen in 2022.

Analyst Ratings

The analyst community has settled on a consensus “Hold” rating for HP Inc., with 16 analysts contributing to the current coverage picture. That consensus reflects a view that the stock’s fundamental underpinnings remain intact but that near-term catalysts are limited given the soft PC demand environment and the macro uncertainty that has weighed on hardware spending broadly.

The mean price target of $23.21 implies approximately 27% upside from the current price of $18.20, a spread that is unusually wide for a “Hold” consensus and suggests the analyst community sees real value in the stock even without being willing to issue outright “Buy” recommendations at this stage. The low end of the target range sits at $18.00, essentially in line with the current price and near the 52-week low of $18.01, indicating that the most cautious analysts see limited downside from here. The high-end target of $30.00 implies meaningful recovery potential if PC market conditions improve or if HP’s AI-enabled product strategy begins to show more tangible results in the financial results.

For income investors, the analyst picture is arguably less important than the dividend and cash flow data, but the target distribution is nonetheless encouraging. A floor near the current price combined with a mean target that implies substantial upside creates an asymmetric setup that is worth monitoring. If the consensus shifts toward more upgrades as the PC cycle recovers, price appreciation could accompany what is already a very attractive dividend yield.

Earnings Report Summary

Revenue Growth Resumes at Scale

HP Inc. reported trailing twelve-month revenue of $55.3 billion, a notable improvement from the $53.88 billion reported in the prior comparative period. That increase of roughly 2.6% reflects modest but real top-line momentum, driven primarily by the Personal Systems segment as commercial PC demand showed early signs of stabilization. The AI-enabled PC push that CEO Enrique Lores has championed is beginning to contribute to mix improvement, even if the overall hardware market remains uneven.

The Printing segment continues to face structural headwinds, as the long-term secular decline in print volumes persists. HP has acknowledged this reality and has focused its growth investments elsewhere, but Printing remains a meaningful contributor to overall profitability and cash generation even as its revenue base gradually contracts. Maintaining margins in that segment while investing in growth elsewhere defines much of the operational challenge facing management.

Profit and Cash Flow

Net income on a trailing basis came in at $2.53 billion, translating to EPS of $2.65. The profit margin of 4.57% is consistent with the thin-margin reality of hardware manufacturing at scale. Operating cash flow of $3.70 billion and free cash flow of $2.39 billion confirm that HP’s earnings translate effectively into real cash, which is the metric that matters most for dividend investors evaluating payout sustainability. Return on assets of 5.59% reflects the capital-intensive nature of the business but is broadly in line with industry peers.

What Leadership Had to Say

CEO Enrique Lores has consistently framed HP’s strategic narrative around two themes: the AI PC transition and supply chain resilience. On AI PCs, HP has been advancing its product lineup with embedded AI capabilities aimed at commercial customers who are beginning to evaluate fleet upgrades. The expectation is that as enterprise IT budgets normalize and AI-capable hardware becomes a procurement standard rather than a premium option, HP is positioned to capture a meaningful share of that refresh cycle.

On manufacturing, HP has made substantial progress in reducing its China production exposure, a move that insulates the company from tariff risk and improves supply chain flexibility. With more than 90% of North American-bound products now sourced outside China, HP has largely completed a logistical transformation that many competitors are still working through. That positioning could prove to be a competitive advantage if trade policy continues to evolve in ways that penalize China-dependent supply chains.

Looking Ahead

Management’s near-term outlook reflects the same measured tone that has characterized HP’s guidance approach for several years. The focus remains on execution, cost discipline, and maintaining the capital return program through a period when external demand conditions are not fully cooperative. The dividend increase to $0.30 per quarter, announced alongside the December 2025 payment, was itself a form of forward guidance, signaling that management sees sufficient cash generation ahead to sustain and grow the payout.

For income investors, the most important forward-looking signal is the payout ratio at 43.68% and free cash flow that covers the dividend obligation with a comfortable margin. Those two metrics together suggest that HP can continue raising the dividend annually even if earnings growth remains modest over the next several quarters.

Management Team

HP Inc. is led by Enrique Lores, who has served as President and CEO since November 2019. His tenure has been defined by a focus on operational discipline, a push into AI-enabled personal computing, and a deliberate effort to reshape HP’s manufacturing footprint away from geopolitical risk. Lores has managed the company through a full hardware cycle, including the pandemic-era PC boom and the subsequent demand normalization, without abandoning the capital return commitments that income investors rely on.

Karen Parkhill serves as Chief Financial Officer, a role she assumed in August 2024. Her background spans healthcare and banking, bringing a cross-industry perspective on capital structure management and investor relations. Parkhill’s financial conservatism aligns well with HP’s commitment to maintaining the dividend and managing debt levels through varying demand environments.

Alex Cho continues to lead the Personal Systems division, where the AI PC initiative is centered. His team is responsible for translating the product roadmap into commercial wins as enterprise customers evaluate next-generation hardware. Anneliese Olson oversees the Imaging, Printing, and Solutions segment, managing a business that requires careful cost management and strategic prioritization given the secular softness in print volumes. Dave Shull leads HP Solutions, expanding the services and software layer that HP is building around its hardware base.

Dave McQuarrie runs global sales and commercial operations, a function that is central to HP’s ability to convert product innovation into revenue. Julie Jacobs manages legal and compliance matters, and the overall team brings a depth of experience that reflects well on HP’s ability to navigate an industry in transition. Together, this group has maintained shareholder returns as a consistent priority while managing through one of the more challenging demand environments the PC industry has seen in recent years.

Valuation and Stock Performance

HP’s stock is currently trading at $18.20, uncomfortably close to its 52-week low of $18.01 and far removed from the 52-week high of $35.28. That decline has compressed the market cap to approximately $17 billion, a figure that looks quite modest against trailing revenue of $55.3 billion and free cash flow of $2.39 billion. The trailing P/E ratio of 6.87 is strikingly low by almost any measure, and while HP’s negative book value per share makes price-to-book a less useful metric here, the earnings-based valuation reflects a market that is pricing in significant ongoing headwinds.

At a P/E below 7, HP is trading at a discount to the broader market and to most of its technology hardware peers. The market cap is essentially just over seven times trailing free cash flow, which is cheap for a business with HP’s scale, brand recognition, and established customer relationships. That valuation is not consistent with a company in financial distress; it is more consistent with a company that has fallen out of favor during a soft patch in its end markets.

For long-term income investors, the current price creates an entry point that combines a 6.31% dividend yield with a valuation that leaves meaningful room for price recovery as PC market conditions eventually normalize. The analyst consensus mean target of $23.21 implies 27% upside from current levels, and even the most bearish target of $18.00 suggests the downside from here is limited. HP is not a growth story, and it should not be evaluated as one, but on a cash flow and income basis, the current price is difficult to dismiss as anything other than attractive.

Risks and Considerations

The PC and printing hardware markets remain challenging, and HP’s near-term revenue trajectory depends heavily on whether enterprise IT spending recovers from the cautious posture that has prevailed through 2025. A prolonged delay in commercial PC refresh cycles, particularly if corporate customers defer AI-capable hardware upgrades, would weigh on both revenue and earnings, potentially pushing the payout ratio higher than the current comfortable level of 43.68%.

HP carries meaningful debt on its balance sheet, and while operating cash flow has been sufficient to service that debt comfortably, a sustained deterioration in free cash flow would force management to make harder choices between debt reduction, share repurchases, and dividend growth. The company has managed this balance well historically, but it is a constraint that limits strategic flexibility in ways that a debt-free competitor would not face.

Geopolitical and trade policy risk remains relevant despite HP’s manufacturing diversification effort. The company has successfully reduced its China production exposure for North American-bound products, but its global supply chain and its customer base in international markets still carry exposure to trade friction, currency volatility, and regulatory complexity in jurisdictions where HP does meaningful business.

The secular decline in the Printing segment is a structural reality that will continue to act as a drag on overall company growth. HP has managed this gracefully by extracting cash from the segment while investing in higher-growth areas, but the math of a shrinking business unit eventually limits how much it can contribute to the overall financial picture. Short interest of over 96 million shares also reflects meaningful bearish conviction in the market, which can amplify downside volatility if near-term results disappoint expectations.

Final Thoughts

HP Inc. is not a stock for investors seeking rapid price appreciation or dramatic business transformation. It is a stock for investors who want a mature, cash-generative technology company with a proven commitment to growing its dividend, trading at a valuation that reflects temporary market pessimism rather than permanent business impairment. The 6.31% yield, supported by a sub-44% payout ratio and $2.39 billion in free cash flow, is the clearest expression of what HP offers at its current price.

The risks are real, from PC demand softness to debt levels to printing segment contraction, but none of them represent the kind of existential challenge that would threaten the dividend program that income investors depend on. Enrique Lores and the management team have demonstrated the discipline to maintain capital returns through difficult periods, and the AI PC strategy provides a credible path to renewed growth as enterprise hardware spending eventually recovers. For income-focused investors with a multi-year time horizon, HP at $18.20 deserves serious consideration.