Key Takeaways

📈 HomeTrust offers a 1.15% dividend yield with a remarkably low 13.17% payout ratio, leaving substantial room for continued dividend growth and providing strong earnings coverage.

💵 Net income reached $64.4 million over the trailing twelve months, with EPS of $3.73 and a profit margin of 31.24%, reflecting steady improvement in the bank’s core operations.

🔍 Analysts maintain a buy consensus with a mean price target of $48.17, suggesting meaningful upside from the current price of $42.62.

Updated 2/24/26

HomeTrust Bancshares, Inc. is a North Carolina-based regional bank with a growing presence across the Southeastern United States. The company has built a solid foundation through disciplined lending, careful risk management, and a focus on long-term performance rather than short-term growth spikes. Its leadership team, led by CEO Hunter Westbrook, continues to prioritize operational efficiency, conservative financial practices, and strategic market positioning.

The bank has continued to deliver steady results, with earnings per share climbing to $3.73 on a trailing basis, a rising profit margin, and a healthy return on equity above 11%. With a stable and growing dividend, a very low payout ratio, and a stock price that has recovered meaningfully from its 52-week lows, HomeTrust continues to attract attention from dividend-focused investors and analysts who see potential for further upside.

Recent Events

HomeTrust Bancshares has been executing quietly but effectively in recent months. The company made its NYSE debut under the ticker HTB following its exchange listing move announced in 2025, a transition that has brought increased institutional visibility and likely contributed to improved trading volume. The bank also followed through on its previously announced plan to divest two Knoxville branches, part of CEO Hunter Westbrook’s stated strategy of sharpening focus on core markets and eliminating operational drag from underperforming locations.

On the dividend front, HomeTrust raised its quarterly payment to $0.13 per share beginning with the November 2025 distribution, up from the $0.12 it had held steady since late 2024. That increase was confirmed again with the February 2026 payment, which also came in at $0.13, establishing the new baseline. The consistent cadence of these raises reflects management’s confidence in the bank’s earnings trajectory and its commitment to returning capital to shareholders in a measured, sustainable way.

The stock has traded in a 52-week range of $30.95 to $47.64, and at the current price of $42.62, it sits well above its lows while still offering room to close the gap toward analyst targets. Market capitalization now stands at approximately $743 million, reflecting the market’s growing recognition of the bank’s earnings quality and conservative operating model.

Key Dividend Metrics

📈 Forward Dividend Yield: 1.15%

💰 Annual Dividend Rate: $0.52

🔁 Payout Ratio: 13.17%

📅 Last Dividend Payment: $0.13 (February 18, 2026)

📊 Dividend Growth Trend: Raised from $0.10 in 2023 to $0.13 in 2025-2026

🧮 EPS (TTM): $3.73

🛡️ Dividend Safety Indicator: Exceptional coverage, very low payout risk

Dividend Overview

A 1.15% yield is not going to turn heads among investors chasing high-income plays, but for dividend growth investors, HomeTrust’s payout profile is genuinely attractive. The company is directing just 13.17% of its earnings toward the dividend, one of the lowest payout ratios in the regional banking sector. That number tells a clear story: the dividend is extraordinarily well covered, and the bank has significant financial flexibility to continue raising it over time.

This conservative posture is a deliberate choice by management rather than a sign of reluctance to reward shareholders. The bank has been steadily increasing its per-share payment, moving from $0.10 per quarter in early 2023 to the current $0.13, a 30% cumulative increase over roughly three years. Each step has been modest and deliberate, which is precisely what income investors should want to see from a regional bank operating in a rate-sensitive environment.

The most recent payment of $0.13 was distributed on February 18, 2026, continuing the quarterly cadence investors have come to rely on. With EPS running at $3.73 and an annual dividend of just $0.52, the bank would need to absorb a dramatic earnings deterioration before the dividend faced any meaningful pressure. That kind of cushion is rare, and it makes HomeTrust a genuinely dependable income holding.

Dividend Growth and Safety

HomeTrust’s dividend history over the past three years tells a consistent and encouraging story. Starting at $0.10 per quarter in mid-2023, the bank has raised its payment four times, arriving at the current $0.13. The raises have not been dramatic, but they have been reliable, each one signaling management’s confidence in the sustainability of the earnings base. The step from $0.12 to $0.13 that took effect in the fourth quarter of 2025 represents the most recent increase, and it has now been paid twice consecutively, suggesting it is well established as the new floor.

The safety profile of this dividend is exceptional by any reasonable measure. With a payout ratio of just 13.17% and EPS of $3.73, HomeTrust could cut its earnings by more than 85% before the dividend would be technically uncovered at the current level. In practice, of course, no bank would allow earnings to deteriorate to that degree before taking action, but the point stands: there is an enormous margin of safety embedded in this payout. Return on equity at 11.17% and return on assets at 1.41% both reflect a well-run institution generating solid profitability relative to its capital base.

The stock’s beta of 0.89 indicates that HomeTrust moves slightly less than the broader market, which is consistent with the bank’s conservative operating profile. For income investors who prioritize capital preservation alongside dividend income, that lower volatility characteristic adds another layer of appeal. The combination of a growing dividend, a very low payout ratio, and below-market price volatility makes HomeTrust a genuinely low-drama income holding with genuine long-term compounding potential.

HomeTrust’s dividend is not designed to attract yield-seekers. It is designed to persist and grow. That distinction matters for investors who are building portfolios meant to last decades rather than quarters, and it reflects the same disciplined philosophy that management applies to the lending book and the balance sheet.

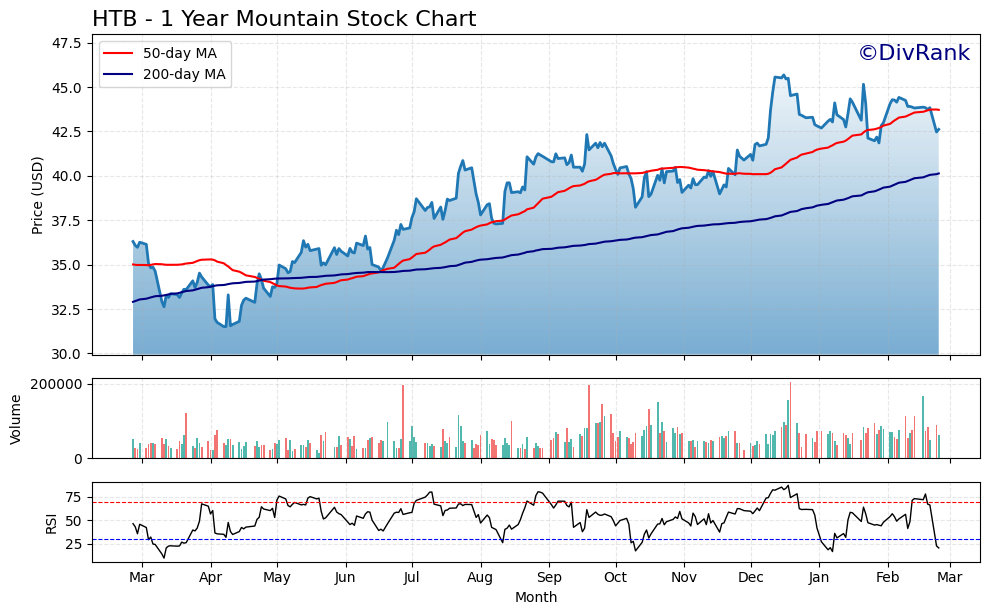

Chart Analysis

HTB has had a strong run over the past year, climbing from a 52-week low of $31.51 to a current price of $42.62, representing a gain of roughly 35% from the trough. That kind of recovery reflects genuine buying interest and improving sentiment around the name. The stock did reach as high as $45.68 over the trailing twelve months, and at the current price it sits about 6.7% off that peak, suggesting some consolidation is underway after what was a meaningful advance. For income investors, this kind of price history matters because it indicates the market has been willing to assign meaningfully higher valuations to the shares, which provides a reasonable margin of support for the dividend yield at current levels.

The moving average picture tells a constructive story. HTB’s 200-day moving average sits at $40.14, and with the stock trading at $42.62, price remains comfortably above that long-term trend line. That is a meaningful positive for dividend investors who care about underlying price stability as much as yield. The 50-day moving average has crossed above the 200-day, forming what technicians refer to as a golden cross, a configuration that historically signals improving intermediate-term momentum. The one caveat is that the current price of $42.62 has slipped below the 50-day moving average of $43.72, which points to some near-term softness. That gap is modest at roughly 2.5%, and the golden cross formation suggests the broader trend remains intact despite the recent pullback.

The RSI reading of 20.27 stands out immediately. A reading that far below the conventional oversold threshold of 30 indicates the stock has experienced sharp selling pressure in a compressed period. Momentum has clearly turned negative in the short run, and traders focused on price action alone may continue to treat the name cautiously until buying volume returns. That said, deeply oversold RSI readings in fundamentally sound dividend payers have historically marked attractive accumulation zones rather than the beginning of sustained breakdowns, particularly when the longer-term trend, as represented by the 200-day average, remains supportive.

For dividend investors, the setup here is one of short-term noise against a longer-term constructive backdrop. The golden cross, the healthy distance above the 200-day moving average, and the stock’s substantial recovery from its 52-week low all suggest the primary trend favors the bulls. The near-term weakness, reflected in the price trading below the 50-day average and an extreme oversold RSI, may represent a better entry point for income-focused buyers willing to look past temporary volatility. Investors already holding the shares for yield have a reasonable technical foundation beneath them, while those considering initiating a position may find the current price more favorable than the levels seen earlier in the year.

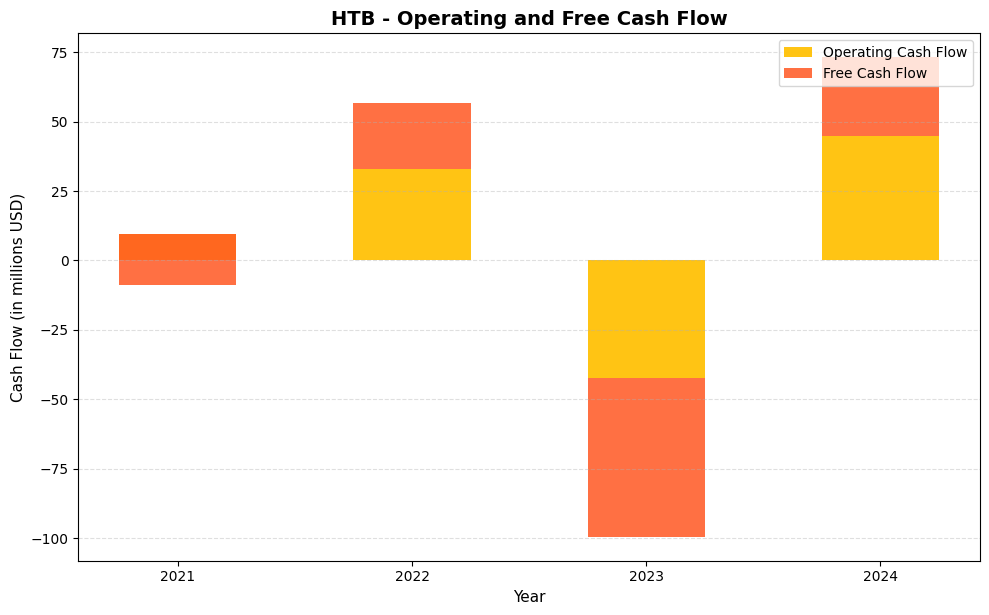

Cash Flow Statement

HTB’s cash flow profile has been anything but linear, which is the first thing dividend investors need to reckon with here. Operating cash flow swung from $9.6M in 2021 to $33.1M in 2022, then cratered to negative $42.4M in 2023 before recovering sharply to $45.0M in 2024. Free cash flow followed a similarly volatile path, registering negative $18.4M in 2021, turning positive at $23.6M in 2022, collapsing to negative $57.1M in 2023, and then rebounding to $28.2M in 2024. The 2024 recovery is genuinely encouraging, and the $28.2M in free cash flow does provide a tangible cushion to support dividend distributions. That said, any income investor evaluating sustainability has to weigh the 2023 trough seriously, because a single bad operating year wiped out meaningful cash generation and sent free cash flow deeply negative.

Zooming out across the full four-year window, HTB has generated cumulative operating cash flow of roughly $45.3M and cumulative free cash flow of negative $23.7M, which tells you that capital expenditures have consumed a significant portion of operating earnings over this period. The 2023 shortfall appears to have been the primary drag, with capex running approximately $14.7M above what operating cash flow could cover that year. The 2024 rebound, where operating CF reached its four-year high of $45.0M and capex was held to roughly $16.8M, suggests management made a deliberate effort to tighten capital discipline after an expensive 2023. For shareholders, the key takeaway is that the business does have the capacity to generate meaningful free cash flow in favorable operating environments, but the year-to-year volatility introduces real uncertainty around dividend reliability, and investors should monitor whether 2024’s efficiency carries into 2025 before treating the recovery as a durable trend.

Analyst Ratings

The analyst community covering HomeTrust Bancshares currently maintains a consensus buy rating, with three firms contributing to the collective outlook. The mean 12-month price target sits at $48.17, with individual targets ranging from a low of $46.50 to a high of $51.00. At the current price of $42.62, the mean target implies upside of roughly 13%, and even the most conservative target of $46.50 represents a gain of approximately 9% from current levels. That range of targets reflects a broadly aligned view that HomeTrust is modestly undervalued relative to its earnings power and balance sheet quality.

The buy consensus is grounded in several observable fundamentals. The bank’s EPS of $3.73 positions it at a P/E ratio of just 11.43, which is below where comparable well-run regional banks with similar return profiles tend to trade. The price-to-book ratio of 1.22 is reasonable for an institution generating an ROE above 11%, as banks earning above their cost of equity typically command a premium to book value. Analysts covering the regional banking space have also noted that HomeTrust’s conservative credit culture and disciplined loan growth strategy reduce the risk of unexpected charge-offs that have tripped up some peers in the current credit cycle.

No specific analyst actions are available for the current period, but the existing price target distribution suggests that the covering firms have not meaningfully revised their views following recent earnings. The tight clustering of targets between $46.50 and $51.00 indicates a consistent read on the company’s near-term earnings trajectory, and the absence of downward revisions in a period of broader banking sector uncertainty speaks well of HomeTrust’s perceived resilience.

Earning Report Summary

Steady Earnings Trajectory Through Late 2025

HomeTrust Bancshares has continued to build on the momentum established in early 2025, delivering full-year trailing EPS of $3.73 and net income of $64.4 million. Those figures represent a clear step forward from the prior year’s results and confirm that the bank’s strategy of prioritizing margin quality over loan volume growth is producing tangible financial results. Revenue of $206 million reflects a 6.2% increase from the prior comparable period, an acceleration that stands out given the headwinds facing many regional banks as the interest rate cycle has shifted.

Return on assets of 1.41% and return on equity of 11.17% are both improvements over prior-year figures and place HomeTrust comfortably in the upper tier of its peer group by profitability metrics. The profit margin of 31.24% is particularly impressive for a bank of this size and reflects both careful expense management and the benefit of a well-positioned loan book. These are not the numbers of a bank that is stretching for growth at the expense of quality. They are the numbers of a business that is executing consistently and compounding value steadily.

Conservative Capital Allocation and Dividend Progress

Management’s capital allocation philosophy remains consistent with prior periods. The bank raised its quarterly dividend to $0.13 per share in the fourth quarter of 2025 and maintained that level through the February 2026 payment, a clear signal that the earnings improvement is viewed as durable rather than transitory. With a payout ratio of just 13.17%, the bank is retaining the overwhelming majority of its earnings to support balance sheet growth and maintain a strong capital position.

Book value per share of $35.04 continues to grow, and at the current price of $42.62, investors are paying a modest premium of roughly 22% above tangible book. For a bank generating an ROE above 11% with a disciplined credit culture and a history of steady dividend increases, that premium appears justified. CEO Hunter Westbrook has reiterated his focus on sustainable financial performance over aggressive growth targets, and the numbers bear that commitment out.

Operational Focus and Market Positioning

The completion of the Knoxville branch divestitures and the consolidation of operations into core markets represent the kind of deliberate strategic housekeeping that tends to improve efficiency ratios over time. HomeTrust’s presence across the Southeastern United States continues to benefit from the region’s demographic and economic growth trends, which provide a favorable backdrop for loan demand and deposit gathering. Management has indicated that loan growth expectations remain measured, with credit quality preservation taking precedence over volume targets. That posture, while not exciting, is exactly what income investors should want from a bank holding that is expected to support a growing dividend stream over a multi-year horizon.

Management Team

Hunter Westbrook has served as Chief Executive Officer of HomeTrust Bancshares and continues to set the tone for the organization’s conservative, long-term-oriented operating philosophy. His consistent public messaging around sustainable performance, disciplined credit standards, and shareholder value creation has been matched by the financial results the bank has produced under his tenure. The decision to list on the NYSE, divest non-core branches, and maintain a very low dividend payout ratio while still growing the per-share payment reflects a coherent and patient capital allocation framework.

The broader executive team has demonstrated stability in key roles across finance, credit, and operations, which is an underappreciated quality in regional banking. Management continuity reduces execution risk and supports the kind of institutional knowledge that helps banks navigate credit cycles without making costly errors. HomeTrust’s return on equity above 11% and its profit margin above 31% are outcomes that require consistent execution across multiple functions, and the current team has demonstrated the capacity to deliver that consistency. For long-term income investors, a stable and aligned management team is one of the most important non-financial factors in assessing dividend reliability, and HomeTrust scores well on that dimension.

Valuation and Stock Performance

HomeTrust shares are currently trading at $42.62, placing the stock roughly in the middle of its 52-week range of $30.95 to $47.64. The P/E ratio of 11.43 is modest for a bank generating an ROE above 11%, a profit margin above 31%, and a track record of consistent earnings growth. At the sector level, well-run regional banks with comparable profitability metrics often trade at P/E ratios in the 12 to 15 range, suggesting that HomeTrust may still carry a modest discount relative to its fundamental quality.

The price-to-book ratio of 1.22 is similarly reasonable. Banks that earn their cost of equity on a sustained basis typically deserve to trade above book value, and at 1.22 times a book value of $35.04 per share, the premium is not excessive. The mean analyst price target of $48.17 implies that the covering firms see the stock as worth approximately 1.37 times book, which would still represent a conservative valuation for a bank of HomeTrust’s earnings profile. The low end of the analyst target range at $46.50 would put the stock at about 1.33 times book, reinforcing the view that even the most cautious covering analysts see meaningful upside from current levels.

The stock’s beta of 0.89 indicates that HomeTrust is a relatively stable holding from a price volatility standpoint, which complements its dividend growth profile well. Investors who entered near the 52-week low of $30.95 have already seen substantial appreciation, but the combination of a still-reasonable valuation, a growing dividend, and a positive analyst consensus suggests that the current entry point at $42.62 is not unreasonable for investors with a multi-year time horizon.

Risks and Considerations

Regional banks are inherently sensitive to interest rate movements, and HomeTrust is no exception. While the bank has demonstrated an ability to manage net interest margin effectively through prior rate cycles, a sustained decline in short-term rates could compress earning asset yields and put modest pressure on profitability. The bank’s ability to reprice deposits and manage funding costs will be a key variable to monitor in the quarters ahead, particularly as the Federal Reserve’s policy path remains uncertain.

Credit quality is always a central concern for any lending institution, and while HomeTrust has maintained a conservative underwriting culture, a deterioration in economic conditions across the Southeastern markets where it operates could lead to higher loan loss provisions and a reduction in net income. The bank’s commercial real estate and business lending portfolios are areas where credit stress tends to emerge first during economic downturns, and investors should watch non-performing asset trends closely in future earnings releases.

The stock’s relatively low dividend yield of 1.15% means that total return depends more heavily on price appreciation than on income alone. If earnings growth stalls or the broader regional banking sector re-rates lower, the stock could give back some of its recent gains even without any fundamental deterioration specific to HomeTrust. Investors who require a higher current income stream may find the yield insufficient relative to alternatives in the current fixed income environment.

Finally, the bank’s relatively small market capitalization of approximately $743 million means that institutional ownership and analyst coverage remain limited. With only three analysts covering the stock, there is less information flow and price discovery than exists for larger banking institutions, which can lead to wider bid-ask spreads and occasional periods of illiquidity. That limited coverage also means that positive developments may take longer to be recognized and priced in by the broader market.

Final Thoughts

HomeTrust Bancshares is not a bank that tries to impress with aggressive growth targets or an outsized dividend yield. What it offers instead is something more durable: a conservatively managed, consistently profitable regional bank that has raised its dividend steadily from $0.10 per quarter in 2023 to $0.13 today, with a payout ratio so low that continued increases appear well within reach for years to come. The combination of a 13.17% payout ratio, EPS of $3.73, and a buy consensus from covering analysts with a mean target of $48.17 adds up to a compelling case for patient, income-oriented investors.

At $42.62 and a P/E of 11.43, the stock is not expensive relative to its earnings quality. The price-to-book ratio of 1.22 is a fair price to pay for a bank earning an ROE above 11% with a disciplined management team that has demonstrated a consistent commitment to shareholder returns. The recent transition to the NYSE, the strategic branch divestitures, and the continued revenue growth to $206 million all point to a management team executing deliberately and without the kind of short-term noise that erodes long-term value.

For dividend growth investors building a portfolio around income streams that compound quietly over time, HomeTrust Bancshares fits that profile well. The yield is modest today, but the growth trajectory, the safety margin, and the fundamental quality of the underlying business make it a name worth holding for the long term.