Key Takeaways

💸 Hilltop offers a 1.91% dividend yield with a consistent growth trend and a conservative 27% payout ratio, underpinned by a recent quarterly dividend increase to $0.20 per share.

💼 The company trades just above book value at a price-to-book of 1.04, with a market cap of approximately $2.3 billion and a beta of 0.92, reflecting modest market sensitivity.

📊 Three analysts covering HTH carry an average price target of $38.67, sitting close to the current price of $37.86, suggesting the market is fairly pricing in near-term fundamentals.

Updated 2/24/26

Hilltop Holdings Inc. (HTH), based in Dallas, operates a diversified mix of businesses spanning regional banking, mortgage lending, and capital markets. Through its key subsidiaries, PlainsCapital Bank, PrimeLending, and HilltopSecurities, the company serves a broad range of clients while maintaining a firm commitment to balance sheet strength and risk management. Its leadership team, led by Jeremy Ford, has guided the company through multiple market cycles with a steady hand and a focus on shareholder value.

With a 1.91% dividend yield, a conservative 27% payout ratio, and a recent dividend raise to $0.20 per share, Hilltop offers a reliable income stream supported by consistent financial execution. Trading just above book value with a healthy capital base, it presents a value-oriented option for investors seeking stable returns in the financial services space.

Recent Events

Hilltop Holdings has been active on the capital return front heading into early 2026. The most notable development for income investors was the company’s decision to raise its quarterly dividend to $0.20 per share, paid on February 13, 2026. That marks a step up from the $0.18 per share rate that had been in place throughout 2025, and it continues a pattern of measured annual increases that has been a hallmark of management’s approach to shareholder returns.

On the operating front, Hilltop reported full-year revenue of approximately $1.27 billion, with net income coming in at $165.6 million and earnings per share of $2.66. Return on equity reached 7.79% and return on assets came in at 1.07%, metrics that reflect steady if unspectacular execution across the company’s diversified financial platform. The profit margin of 12.99% signals that Hilltop continues to run its operations with discipline, even as the broader interest rate environment continues to shape conditions in mortgage origination and capital markets activity.

The stock has responded to improving fundamentals, trading near $37.86 as of late February 2026, well above the $27.35 low it reached over the past 52 weeks. That recovery reflects renewed investor confidence in the company’s earnings trajectory and the durability of its diversified business model. With a beta of 0.92, HTH continues to behave as a relatively stable holding, which fits well within an income-focused portfolio construction approach.

Key Dividend Metrics

📈 Forward Yield: 1.91%

💰 Annual Dividend: $0.74 per share

🧮 Payout Ratio: 27.27%

📆 Last Dividend Payment: $0.20 on February 13, 2026

✂️ Last Dividend Increase: $0.18 to $0.20 per share (February 2026)

📦 Dividend Consistency: Steady annual increases since at least 2023

📊 EPS: $2.66 | P/E: 14.23

Dividend Overview

Hilltop pays a forward annual dividend of $0.74 per share, annualizing the most recent quarterly payment of $0.20. At the current price of $37.86, that translates to a yield of 1.91%, which is modest by absolute standards but sits comfortably above the 1.83% five-year average yield that has historically characterized this name. The yield is being supported by a payout ratio of just 27.27%, one of the more conservative figures among regional financial holding companies, which leaves significant room for continued dividend growth without straining earnings.

The dividend history over the past several years tells a straightforward story. Payments held at $0.16 per share through much of 2023, moved to $0.17 in early 2024, stepped up to $0.18 in early 2025, and most recently increased again to $0.20 in February 2026. That cadence of annual increases, while not dramatic, reflects the kind of deliberate capital return philosophy that income investors can plan around. Each raise has been modest and well within the company’s earnings capacity, which is exactly the profile that suggests dividend sustainability rather than stretch.

The 52-week trading range of $27.35 to $40.41 shows that the stock has experienced meaningful price movement over the past year, but its current position near $37.86 places it in the upper half of that range. Insiders continue to hold a meaningful ownership stake alongside institutional investors, which reinforces alignment between management decisions and long-term shareholder outcomes, including the consistent growth of the dividend.

Dividend Growth and Safety

Hilltop’s dividend growth trajectory is methodical rather than aggressive, and that is precisely what makes it credible. The company has moved its quarterly payment from $0.16 to $0.20 over roughly three years, representing cumulative growth of 25% at a pace that tracks closely with earnings growth. There are no signs of a dividend being pushed beyond what the business can comfortably support, and with a payout ratio of 27.27% against EPS of $2.66, there is more than ample coverage even under a scenario where earnings soften.

The earnings base itself is encouraging. Net income came in at $165.6 million for the trailing period, and revenue of $1.27 billion reflects a diversified revenue mix that spans interest income, fee-based advisory, mortgage origination, and capital markets activity. That diversification provides a degree of insulation that a purely loan-dependent regional bank would not have. When one segment faces pressure from rate movements or credit conditions, others can offset the impact.

Operating cash flow for the period came in negative at approximately $38.7 million, which warrants some attention from a dividend safety perspective. For a financial holding company, negative operating cash flow in any given period can reflect changes in loan portfolios or working capital rather than a structural deterioration in earnings power. Net income of $165.6 million demonstrates that profitability remains intact, and the conservative payout ratio provides a wide margin of safety. The beta of 0.92 also reinforces that this is a relatively stable business relative to the broader market, which supports its positioning as a lower-volatility income holding.

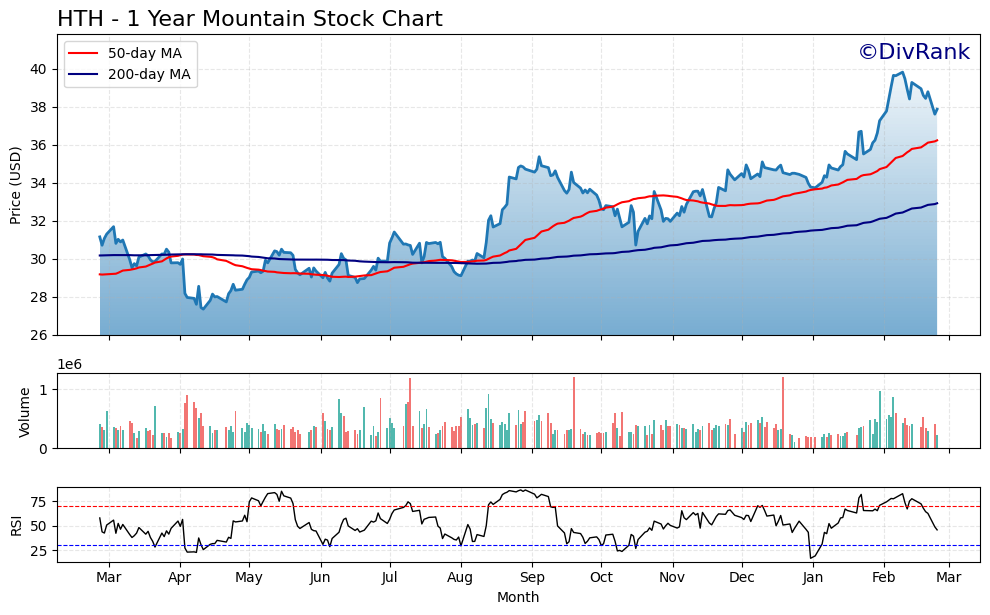

Chart Analysis

Hilton Grand Vacations has staged an impressive recovery over the past year, climbing from a 52-week low of $27.34 to its current price of $37.86, a gain of roughly 38.5% from the trough. That kind of price appreciation over a twelve-month window signals a meaningful shift in investor sentiment toward the name, and the stock now sits just 4.9% below its 52-week high of $39.81. The overall trajectory has been constructive, with price action reflecting a steady accumulation pattern rather than a volatile, news-driven spike. For dividend investors who prioritize capital preservation alongside income, the trend over the past year offers a reasonable degree of comfort.

The moving average picture reinforces that constructive read. HTH is trading above both its 50-day moving average of $36.22 and its 200-day moving average of $32.91, a configuration that technical analysts broadly interpret as a healthy uptrend. More importantly, the 50-day has crossed above the 200-day, forming what is commonly referred to as a golden cross. This pattern tends to attract incremental buying interest from momentum-oriented institutions, which can provide a tailwind for income investors who are already long the shares. The spread between the two moving averages, nearly four dollars at this point, suggests the trend has had time to develop and is not simply a brief crossover that could reverse quickly.

The RSI reading of 45.67 adds an interesting dimension to the setup. At that level, the stock is neither overbought nor oversold, sitting comfortably in neutral territory. What makes this notable is that HTH is trading relatively close to a 52-week high while its momentum oscillator remains well below the overbought threshold of 70. That combination implies the recent price gains have not been driven by speculative excess, and there is room for the stock to continue pressing higher without immediately triggering a momentum-driven reversal. Investors who missed the initial move off the lows may find the current RSI reading somewhat reassuring from a timing perspective.

Taken together, the technical picture for HTH is moderately favorable for dividend-focused investors. The golden cross, the position above both key moving averages, and the neutral RSI collectively suggest the stock is in a sustainable uptrend rather than an overextended one. The proximity to the 52-week high is worth monitoring, as that $39.81 level could act as near-term resistance, but a clean break above it would open the door to further price improvement. For investors whose primary objective is collecting and compounding the dividend, the current chart setup does not present an obvious technical deterrent to initiating or adding to a position.

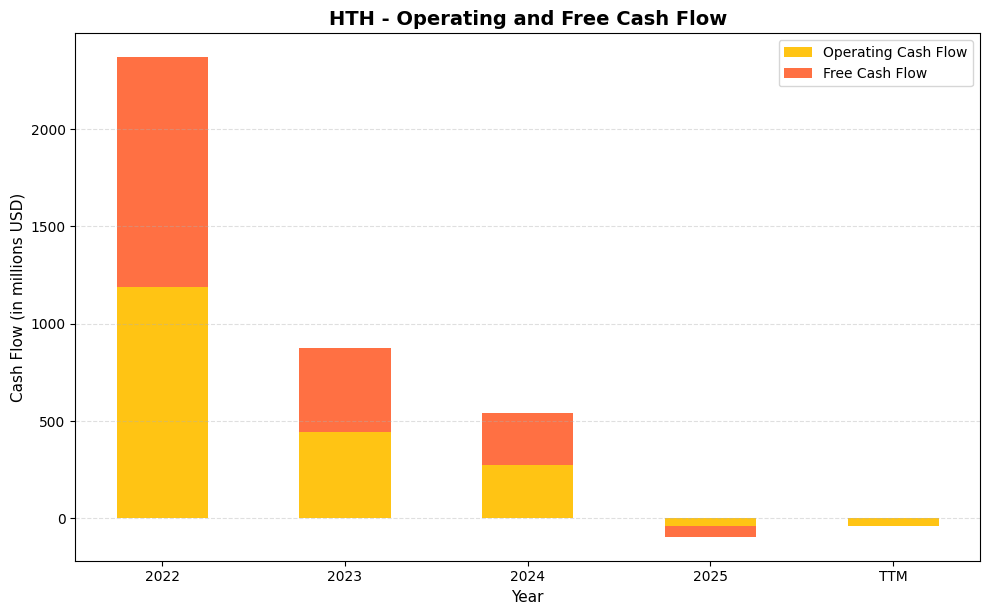

Cash Flow Statement

Hilton Grand Vacations’ cash flow trajectory is one of the most pressing concerns for dividend investors evaluating this name. Operating cash flow has deteriorated sharply over the four-year window shown, falling from $1,189.4 million in 2022 to just $273.9 million in 2024 before turning negative at $38.7 million in the trailing twelve months. Free cash flow has tracked nearly in lockstep, collapsing from $1,179.7 million in 2022 to negative $55.5 million in 2025. When a company is generating negative free cash flow, it is not producing enough internal capital to cover its dividend obligations, which means any distributions to shareholders are effectively being funded through borrowing or asset liquidation rather than organic earnings power. That is a structurally unsustainable condition that warrants serious scrutiny from income-focused investors.

The speed of this deterioration adds important context to the numbers. The 2022 figure benefited from favorable conditions across the vacation ownership segment, including pent-up travel demand and strong sales volume post-pandemic, which created an elevated baseline that was unlikely to persist indefinitely. However, the degree of compression through 2023 and 2024, and then the outright turn negative in the TTM period, suggests the headwinds go beyond simple normalization. Capital efficiency has clearly eroded, as the thin spread between operating and free cash flow across all periods indicates relatively modest capital expenditure requirements, meaning the operating line itself is the problem rather than heavy reinvestment spending. For shareholders, this pattern raises legitimate questions about how long the company can maintain its current capital return framework without a meaningful recovery in core cash generation, and it places the burden of proof squarely on management to demonstrate a credible path back to positive free cash flow.

Analyst Ratings

Analyst coverage of Hilltop Holdings is limited to three firms, and the current consensus does not carry a formal directional rating. The price target range among those analysts spans from a low of $36.00 to a high of $41.00, with a mean target of $38.67. At the current price of $37.86, the stock is trading essentially in line with the analyst consensus, implying that the market has largely absorbed the fundamental improvements seen over the past several quarters.

The proximity of the current price to both the mean target and the book value of $36.42 per share suggests that analysts see limited near-term upside but also limited downside from current levels. The high end of the target range at $41.00 would represent roughly 8% appreciation from current prices, which is a reasonable return expectation for a conservatively managed financial holding company in the current environment. The low-end target of $36.00 sits just below book value, reflecting the floor that a tangible asset base tends to provide for companies like Hilltop. No specific analyst actions were reported in the current period, but the tight clustering of targets around the current price suggests a broadly neutral near-term outlook with a preference for waiting to see how mortgage and capital markets conditions evolve through 2026.

Earning Report Summary

Hilltop Holdings delivered full-year results that reflect steady execution across its diversified platform. Revenue came in at $1.27 billion and net income reached $165.6 million, translating to earnings per share of $2.66. Those results represent a measured but meaningful improvement from prior periods, with the company continuing to benefit from its mix of interest income, fee-based advisory services, and capital markets activity through HilltopSecurities.

Revenue Strength and Business Mix

Revenue of $1.27 billion reflects the contribution of multiple business lines that each respond differently to market conditions. The fee-based businesses within HilltopSecurities have remained a consistent source of income, providing stability that offsets the more cyclical nature of mortgage origination through PrimeLending. Return on equity of 7.79% and return on assets of 1.07% indicate that the company is generating acceptable returns on its capital base, though there remains room for improvement as the interest rate environment and origination volumes evolve through the year ahead.

The profit margin of 12.99% reflects the reality that financial holding companies operate with inherently complex cost structures, including compensation in the securities business and credit costs in the banking segment. Management has continued to emphasize expense discipline alongside revenue growth, which is reflected in the payout ratio holding at a conservative 27.27% even as the dividend was raised.

Cost Management and Capital Position

Hilltop’s common equity tier 1 capital ratio has remained well above regulatory minimums, a point management has consistently emphasized as a competitive advantage and a source of financial flexibility. The company’s book value per share of $36.42 is almost exactly in line with the current stock price, which speaks to the integrity of the balance sheet and the lack of significant unrealized losses that have plagued some peers in the current rate environment. With a price-to-book ratio of 1.04, the stock is no longer the deep discount it represented when it traded below book earlier in its 52-week range, but it remains close enough to intrinsic value to be considered fairly priced rather than stretched.

Leadership Outlook

Management has maintained its long-standing emphasis on disciplined capital allocation, conservative underwriting, and steady shareholder returns. The decision to raise the quarterly dividend to $0.20 per share is consistent with that philosophy, signaling confidence in the earnings trajectory without overcommitting capital. Leadership has also continued to highlight the diversified business model as a strategic advantage, particularly as conditions in mortgage origination and capital markets remain subject to rate-driven variability. The overall tone from management reflects a patient, long-cycle orientation that prioritizes balance sheet strength and sustainable growth over short-term performance optimization.

Management Team

Hilltop Holdings is led by an experienced executive team with deep roots in the financial services industry. At the center is Jeremy Ford, who has served as President and CEO since 2010 and was named Chairman in April 2025. Under his leadership, the company has taken a disciplined approach to growth, consistently emphasizing financial strength and shareholder returns. Ford maintains a meaningful ownership stake in the company, which aligns his decision-making closely with long-term investors.

Supporting him is William Furr, the Chief Financial Officer since 2016. Furr brings years of expertise in financial oversight and has played a critical role in preserving the firm’s strong capital ratios. Other key players include Darren Parmenter, Chief Administrative Officer, and Corey Prestidge, Executive Vice President, both of whom have been instrumental in steering Hilltop’s strategic initiatives. Leadership across the subsidiaries also brings decades of experience, particularly Brad Winges at HilltopSecurities and Steve Thompson at PrimeLending. Together, the team demonstrates a steady hand with a forward-looking mindset that has served long-term shareholders well across multiple market environments.

Valuation and Stock Performance

As of February 24, 2026, Hilltop Holdings is trading at $37.86 per share, putting its market capitalization at approximately $2.3 billion. Over the last twelve months, the stock has moved within a range of $27.35 to $40.41, and its current position near the upper portion of that band reflects the recovery in investor sentiment that has accompanied improving earnings and the recent dividend increase. The stock has shown meaningful appreciation from its 52-week low, gaining roughly 38% from the bottom of the range, which speaks to the repricing that occurred as fundamentals improved.

The current price-to-earnings ratio of 14.23 is reasonable for a diversified financial holding company, sitting comfortably below stretched territory while reflecting an earnings base that has demonstrated consistency. The price-to-book ratio of 1.04 indicates the stock now trades just slightly above its net asset value of $36.42 per share, which is a notable change from earlier in the year when it traded at a discount to book. For value-oriented investors, the current multiple is not a deep discount, but it remains far from an expensive entry point given the quality of the balance sheet and the conservative payout structure.

From a dividend perspective, Hilltop offers a yield of 1.91% supported by a payout ratio of just 27.27%. The company has raised its quarterly dividend annually for several consecutive years, and the most recent increase to $0.20 per share continues that pattern. With a beta of 0.92, the stock moves closely in line with broader markets without the amplified volatility that often accompanies higher-yielding financial names, making it a sensible holding for income investors who prioritize stability alongside income growth.

Risks and Considerations

Hilltop’s mortgage division, PrimeLending, remains sensitive to fluctuations in interest rates and housing market activity. In an environment where rates stay elevated for longer than expected, origination volumes can decline meaningfully, reducing the contribution that segment makes to overall earnings and cash flow. That dynamic has been a persistent headwind for mortgage-focused businesses broadly, and Hilltop is not immune to it despite the offsetting contributions from its other segments.

HilltopSecurities, the investment banking and advisory arm, introduces revenue variability that is tied to capital markets activity and client transaction volumes. During periods of market stress or reduced issuance activity, fee income from this segment can compress, which affects the overall revenue mix and potentially puts more pressure on the banking segment to carry performance. The unpredictability of capital markets revenue is a meaningful factor to monitor, particularly if economic conditions deteriorate through 2026.

The negative operating cash flow of approximately $38.7 million for the trailing period is worth watching, even though net income of $165.6 million indicates that profitability is intact. If operating cash flow remains negative or deteriorates further in upcoming quarters, it could raise questions about the company’s ability to fund dividends and capital expenditures from internally generated cash rather than from balance sheet resources. Management’s track record of conservative capital management provides some reassurance, but this metric deserves attention in forthcoming earnings releases.

Macroeconomic headwinds, including potential credit deterioration in the auto lending portfolio, broader recessionary pressures, or shifts in the regulatory environment for regional financial institutions, also represent risks that could affect earnings and the pace of dividend growth. Hilltop’s diversified model provides a degree of insulation, but no financial holding company is fully shielded from a significant deterioration in the economic backdrop, and investors should monitor credit quality metrics closely as the cycle progresses.

Final Thoughts

Hilltop Holdings offers a quiet strength that does not rely on flash to deliver value. Its leadership team brings long-term focus and consistency to the table, guiding the company through both high and low cycles with a philosophy centered on balance sheet discipline and measured capital returns. The most recent dividend increase to $0.20 per share is a tangible signal that management remains confident in the earnings trajectory heading into 2026.

The stock’s current valuation near book value, combined with a P/E of 14.23 and a payout ratio of just 27.27%, presents a reasonably attractive setup for income investors who prioritize dividend safety and growth sustainability over headline yield. While challenges in mortgage origination, capital markets revenue, and the near-term cash flow picture warrant monitoring, Hilltop’s diversified business mix and conservative management approach continue to provide a credible foundation for the income stream it delivers. For investors with a patient, long-term outlook, Hilltop remains a quietly solid choice in the financial services space.