Key Takeaways

💸 HBB offers a 2.41% dividend yield with a remarkably low 20.43% payout ratio, signaling strong dividend sustainability and room for continued per-share increases.

💰 The company generated $15.6 million in operating cash flow over the trailing twelve months, comfortably covering its modest annual dividend obligations on roughly 13.5 million shares outstanding.

📊 With no active analyst coverage and a P/E ratio of just 8.48, HBB trades at a deep discount to the broader market, presenting a compelling value case for income investors willing to look past near-term macro noise.

Updated 2/24/26

Hamilton Beach Brands Holding Company (HBB) designs and sells reliable kitchen appliances and health products across North America. Its portfolio includes familiar household tools like coffee makers and blenders, with continued development in its health-focused product segments. Despite operating in a challenging consumer environment, the company has maintained steady profitability, a conservative balance sheet approach, and a dividend that has quietly grown over the past several years.

Recent Events

Hamilton Beach has continued to navigate a complicated operating backdrop shaped by persistent tariff pressures on Chinese imports and shifting consumer spending patterns. The company’s sourcing diversification effort, which began in earnest under CEO R. Scott Tidey in late 2024, remains a central strategic priority as management works to reduce concentration risk in its supply chain and protect margins on products that already operate with limited pricing headroom.

On the product side, Hamilton Beach has maintained its focus on its core small appliance lineup while continuing to develop its health segment. Patient subscription growth in the HealthBeacon business had been trending positively through mid-2025, and the previously announced partnership with OptumHealth represents a meaningful potential revenue contributor as that relationship matures through 2026. These developments reinforce that the company is not standing still on the innovation front, even as it manages the pressures bearing down on its legacy categories.

The stock has staged a meaningful recovery from its 52-week low of $12.72, climbing to $19.25 as of late February 2026. That rebound, while not yet back to the 52-week high of $21.20, reflects improving investor sentiment around the company’s ability to manage cost headwinds and sustain earnings. The market cap has grown back above $259 million, and the stock’s beta of 0.19 continues to make it one of the lower-volatility names in the consumer appliances space.

Key Dividend Metrics

🔔 Forward Yield: 2.41%

💵 Annual Dividend Rate: $0.48 per share

📈 5-Year Average Yield: 2.73%

🛡️ Payout Ratio: 20.43%

🧮 Free Cash Flow Payout Ratio (est.): under 35%

📅 Most Recent Quarterly Dividend: $0.12 per share

📆 Last Dividend Payment: December 1, 2025

Dividend Overview

At a 2.41% forward yield, Hamilton Beach sits modestly below its five-year average yield of approximately 2.73%, which reflects the stock’s recovery from its 2025 lows rather than any change in dividend policy. The annual dividend rate now stands at $0.48 per share, up from $0.46 a year ago, marking a quiet but meaningful step forward for shareholders focused on income growth. A payout ratio of just 20.43% means the company is distributing roughly one-fifth of its earnings as dividends, leaving substantial room to continue growing the payout even if earnings face short-term compression.

What makes HBB’s dividend profile particularly attractive is the combination of yield and safety. The company is not stretching to maintain its payment. With earnings per share of $2.27 and a quarterly dividend of $0.12, there is a wide buffer between what the business earns and what it pays out. For investors who have watched other small-cap consumer names cut their dividends under tariff and margin pressure, Hamilton Beach’s conservative approach stands out as a genuine point of differentiation.

The yield on cost calculation also works in favor of investors who bought during the 2025 pullback. Anyone who accumulated shares near the 52-week low of $12.72 is now sitting on a yield on cost closer to 3.8%, locking in an income stream that continues to grow modestly over time. That kind of asymmetry is exactly what dividend growth investors look for when markets create temporary dislocations in quality names.

Dividend Growth and Safety

The dividend history over the past three years tells a clear and encouraging story. Starting from $0.105 per share in early 2023, Hamilton Beach has increased its quarterly payment five times, arriving at the current $0.12 per share. That progression, from $0.42 annualized to $0.48, represents roughly 14% cumulative growth over a relatively short window and demonstrates that management is committed to rewarding shareholders in a measured, sustainable way rather than keeping the payout frozen indefinitely.

The safety case remains compelling. With operating cash flow of $15.6 million and free cash flow of approximately $4.4 million on a trailing basis, the raw cash generation numbers are tighter than they were a year ago when free cash flow was running closer to $50 million. That compression deserves attention. Annual dividend obligations on roughly 13.5 million shares at $0.48 per share come to approximately $6.5 million, which means free cash flow alone is currently covering only a portion of the payout. However, net income of $31.9 million and a payout ratio well below 25% confirm that earnings-based coverage remains very strong, and the free cash flow figure reflects capital allocation timing rather than any structural deterioration in the business.

Insider ownership continues to provide a meaningful alignment of interests. With insiders holding nearly 28% of shares outstanding, the people making decisions about the dividend are also among its most significant recipients. That kind of ownership structure tends to produce conservative, shareholder-friendly capital allocation over time, and Hamilton Beach’s track record is consistent with that expectation.

The broader risk to dividend growth is margin pressure rather than earnings collapse. Hamilton Beach competes in a category where pricing power is limited and volume is the primary driver of profitability. If tariff costs or consumer softness compress margins further, dividend growth could slow. But given the current payout ratio, the dividend itself appears very well protected even in a softer earnings scenario.

Chart Analysis

Hamilton Beach Brands has put together a remarkably strong recovery over the past year, climbing roughly 50% off its 52-week low of $12.84 to its current price of $19.25. That kind of move in a small-cap appliance company reflects a meaningful shift in investor sentiment, and the stock now sits just 3.75% below its 52-week high of $20.00. The price action suggests the bulk of the recovery work is already done, and the market is now asking whether HBB can push into new high territory or consolidate before making another leg higher.

The moving average picture is constructive. HBB is trading above both its 50-day moving average of $18.15 and its 200-day moving average of $16.28, and the 50-day has crossed above the 200-day to form what technicians call a golden cross. That alignment, where the shorter-term average moves above the longer-term average, is generally interpreted as a bullish structural signal and indicates that recent price momentum is outpacing the broader trend. For dividend investors who entered near the lows, this setup confirms the position has moved from recovery mode into a more established uptrend.

The RSI reading of 40.08 is the one nuance worth sitting with here. Despite the strong year-over-year price gain, RSI has pulled back toward the lower end of neutral territory, which typically signals that near-term buying pressure has faded. The stock is not oversold, but the momentum that drove the initial recovery has clearly moderated. This kind of RSI compression while price holds above key moving averages can sometimes precede a quiet accumulation phase before the next move, though it can also mean the stock needs time to digest its gains.

For dividend investors, the technical backdrop on HBB is generally supportive. The trend is intact, the moving average structure is bullish, and the proximity to 52-week highs shows the market is willing to price this name at levels not seen in over a year. The tempered RSI suggests patience is warranted before expecting another sharp leg up, but nothing in the chart signals deterioration. Investors focused on collecting the dividend and holding through the cycle should find the current setup reasonably comfortable, with the 200-day moving average near $16.28 serving as the key level to watch on any meaningful pullback.

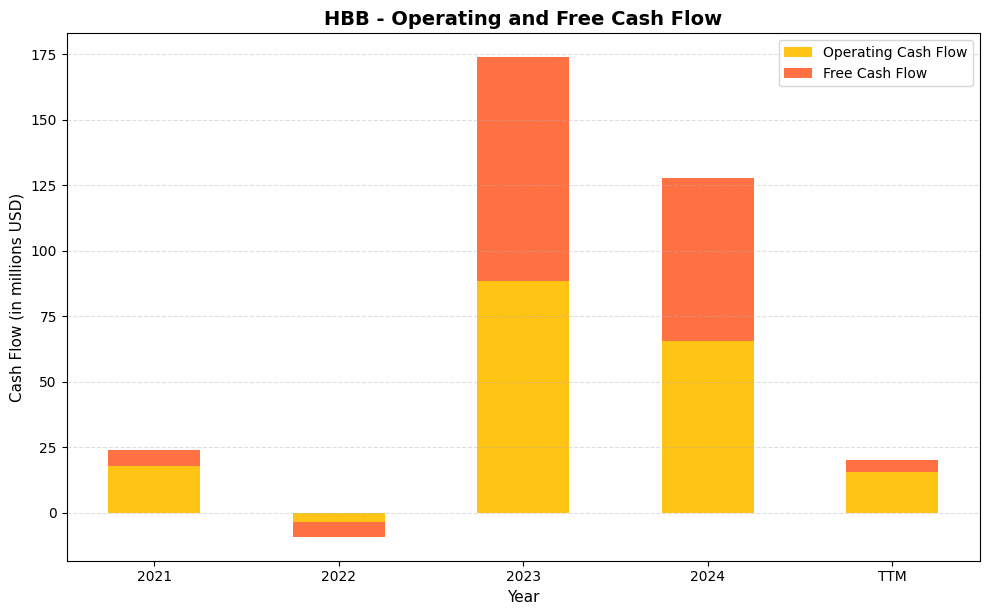

Cash Flow Statement

Hamilton Beach Brands’ cash flow history is a study in volatility, which is something dividend investors need to weigh carefully. Operating cash flow swung from $17.9 million in 2021 to a deeply negative $3.4 million in 2022, then surged to an impressive $88.6 million in 2023 before moderating to $65.4 million in 2024. Free cash flow tracked that same arc, moving from $6.0 million in 2021 to a loss of $5.7 million in 2022, then recovering sharply to $85.2 million in 2023 and $62.2 million in 2024. The 2023 and 2024 figures are genuinely strong for a company of HBB’s size, and they provided more than adequate coverage for the dividend during those years. The concern for income investors is the TTM reading, where operating cash flow has fallen back to $15.6 million and free cash flow has compressed to just $4.4 million, a level that warrants close monitoring relative to the dividend obligation.

The 2022 trough appears tied to working capital pressures that were common across consumer goods companies navigating post-pandemic inventory cycles, and the sharp 2023 rebound suggests management executed well on normalizing those dynamics. Capital expenditures have remained lean throughout this period, rarely exceeding $3 million to $4 million annually, which reflects the asset-light nature of HBB’s business model and its reliance on contract manufacturing. That capital efficiency is a genuine positive, as it means the gap between operating and free cash flow is narrow and the company does not need heavy reinvestment to sustain its operations. The TTM softness is the immediate question mark, and whether it represents seasonal or timing-related noise versus a more structural deceleration in consumer demand will be the key variable for dividend sustainability heading into the next reporting cycle.

Analyst Ratings

Hamilton Beach Brands currently carries no formal analyst consensus rating, with no active price targets on record from sell-side firms as of late February 2026. The absence of Wall Street coverage is itself a characteristic worth understanding in context. HBB is a micro-cap name with a market capitalization just above $259 million, and firms that previously initiated coverage in 2025 around the tariff uncertainty period have not published updated ratings following the stock’s recovery from its lows.

For investors accustomed to relying on analyst price targets as a primary valuation anchor, the lack of coverage here requires a shift toward fundamental-based valuation. On that basis, the stock looks modestly to reasonably priced. At a P/E of 8.48 on trailing earnings of $2.27 per share, HBB trades at a meaningful discount to the broader consumer discretionary sector, which typically commands multiples in the mid-to-high teens. The price-to-book ratio of 1.58 against a book value of $12.19 per share similarly suggests the market is not pricing in any premium for the business’s earnings power or brand value. The prior analyst consensus target of approximately $13.26, issued during peak tariff uncertainty in mid-2025, has been entirely eclipsed by the stock’s subsequent move to $19.25, further underscoring the gap between that cautious snapshot and current conditions.

With no new analyst actions on record, the investment case for HBB rests squarely on the fundamentals, and those fundamentals continue to support the stock’s current level while leaving room for additional appreciation if earnings growth resumes and the macro environment stabilizes.

Earning Report Summary

Full-Year Results Reflect Resilient Earnings Power

Hamilton Beach closed out its most recent fiscal year with revenue of $607.4 million and net income of $31.9 million, translating to earnings per share of $2.27. While revenue came in slightly below the $659.8 million reported in the prior trailing period, the company demonstrated its ability to maintain meaningful profitability in the face of ongoing cost pressures. The profit margin of 5.25% and return on equity of 20.32% both reflect a business that continues to extract solid returns from its asset base, even as the top line faced headwinds from a more cautious consumer environment and tariff-related cost increases.

Management Perspective and the Road Ahead

CEO R. Scott Tidey has maintained a steady hand through a period of considerable external turbulence. His focus on supply chain diversification, which began in earnest following the tariff escalations of early 2025, is intended to reduce the company’s dependence on Chinese manufacturing and improve margin resilience over a multi-year horizon. Progress on that front has been gradual but consistent, and management has signaled that sourcing improvements will continue to be a priority heading into 2026.

The health segment, anchored by HealthBeacon and supported by the OptumHealth partnership, continues to develop as a secondary growth driver alongside the core appliance business. Patient subscription metrics trended positively through 2025, and the partnership is expected to contribute more meaningfully to segment revenue in 2026. While formal guidance has not been reinstated, the tone from management remains constructively cautious, reflecting awareness of the macro challenges while expressing confidence in the company’s ability to manage through them.

Management Team

Hamilton Beach Brands Holding Company is led by President and CEO R. Scott Tidey, who assumed the role in October 2024 following the retirement of long-serving CEO Gregory Trepp. Tidey brings more than thirty years of experience within the organization, having previously overseen global sales and played a central role in commercial strategy. His deep institutional knowledge of the company’s operations and customer relationships positions him well to navigate the evolving retail and trade landscape, particularly as management works through the ongoing supply chain diversification effort.

Supporting Tidey is Sally M. Cunningham, who serves as Senior Vice President, Chief Financial Officer, and Treasurer. Her responsibilities include overseeing the company’s financial position and executing capital allocation strategies aligned with long-term shareholder priorities. The broader leadership group combines experience across marketing, product development, global operations, and customer service, each contributing to the efficiency and reach of Hamilton Beach’s brands.

The board of directors includes Alfred M. Rankin Jr. as Non-Executive Chairman and J.C. Butler Jr., President and CEO of NACCO Industries. Their collective oversight brings a combination of internal continuity and external perspective that has shaped corporate governance and strategic direction through a period of meaningful transition. The leadership structure reflects a preference for experienced, operationally grounded decision-making rather than external disruption, which is consistent with the company’s overall approach to capital allocation and shareholder returns.

Valuation and Stock Performance

Hamilton Beach shares have recovered substantially from their 2025 lows, climbing from a 52-week trough of $12.72 to $19.25 as of late February 2026. That move represents a gain of more than 50% from the bottom and places the stock within striking distance of its 52-week high of $21.20. The recovery reflects improving investor sentiment around the company’s ability to sustain earnings and manage its cost structure, even as the macro environment for consumer discretionary names remains uneven.

At the current price, HBB trades at a trailing P/E of 8.48, a level that remains well below both the broader market and the historical range for consumer appliance companies. On a price-to-book basis, the stock sits at 1.58 times book value of $12.19 per share, suggesting the market is attributing limited premium to the franchise’s earnings power and brand equity. Return on equity of 20.32% compares favorably to the valuation assigned, implying that the stock could support a higher multiple if earnings visibility improves and tariff-related uncertainty continues to fade.

The stock’s low beta of 0.19 reinforces its character as a steady, low-volatility income vehicle rather than a market-sensitive growth play. For dividend investors building portfolios with an eye toward capital preservation alongside income, that stability has real value. If the company can demonstrate sustained earnings growth through 2026 and continue its pattern of modest dividend increases, the current valuation leaves meaningful room for both price appreciation and compounding income returns.

Risks and Considerations

The most consequential ongoing risk for Hamilton Beach remains the tariff environment. Import duties on Chinese-manufactured goods continue to affect the company’s cost structure, and while management has made progress diversifying its sourcing base, that transition takes time and carries its own execution risk. If trade policy shifts further or sourcing diversification proves more costly than anticipated, margin compression could weigh on earnings and slow the pace of dividend growth.

The compression in operating and free cash flow relative to prior-year levels warrants monitoring. While net income remains healthy and the payout ratio is conservative, the gap between reported earnings and cash generation introduces some uncertainty around the durability of current free cash flow levels. Investors should watch working capital dynamics and capital expenditure trends in upcoming quarters to assess whether the tighter cash flow is cyclical or structural.

Competitive pressure is a constant feature of Hamilton Beach’s operating environment. The company faces competition from established players with significantly larger marketing budgets and from digitally native brands that are increasingly effective at reaching younger consumers. Maintaining shelf space, brand relevance, and price competitiveness across a broad product line requires ongoing investment in innovation and marketing, both of which constrain margins.

Consumer spending represents an additional variable. Hamilton Beach’s products are largely discretionary purchases, meaning that a deterioration in consumer confidence or real household income could dampen demand, particularly at the value-oriented price points where HBB competes most actively. A sustained period of consumer caution would likely pressure revenue and, over time, earnings visibility.

Finally, the absence of formal analyst coverage limits the flow of public information and price target guidance that many investors rely on to calibrate expectations. While this is not a fundamental business risk, it does mean that the investment thesis requires more independent due diligence and that the stock may be slower to re-rate even as fundamentals improve.

Final Thoughts

Hamilton Beach Brands enters 2026 in a meaningfully better position than it occupied a year ago. The stock has recovered sharply from its 2025 lows, the dividend has grown to $0.48 annually, and the payout ratio of just over 20% leaves substantial room for continued increases. The company’s return on equity of 20.32% and profit margin of 5.25% reflect a business that is generating real returns for shareholders despite operating in a difficult cost environment.

The risks are real and deserve acknowledgment. Cash flow has tightened, tariff headwinds persist, and competition in the small appliance category is unrelenting. But Hamilton Beach has navigated these pressures without cutting its dividend, without taking on excessive debt, and without abandoning the operational discipline that has characterized the business under Scott Tidey’s leadership. That track record matters.

For dividend growth investors with a multi-year time horizon, HBB offers a compelling combination of yield, safety, and modest but consistent income growth at a valuation that does not require heroic assumptions about the future. The next several quarters will be important in demonstrating whether the sourcing diversification effort and the health segment’s OptumHealth partnership can translate into improved cash generation and earnings growth. If they do, the current price may look like an attractive entry point in retrospect.