Updated 2/24/26

Greene County Bancorp (NASDAQ: GCBC) is a steadily growing community bank headquartered in upstate New York, operating with over $3 billion in assets. Through disciplined lending, conservative financial management, and a strong focus on customer relationships, the bank has built a reputation for consistent earnings growth, solid credit quality, and a well-covered dividend.

Led by a seasoned management team and supported by a high insider ownership stake, GCBC continues to expand its footprint across the Hudson Valley and Capital Region. With a long-standing commitment to shareholders and a growing dividend supported by low payout ratios, the stock appeals to investors seeking stability and steady income.

Recent Events

Greene County Bancorp has continued its steady operational march into early 2026, with the bank’s most recent dividend payment of $0.10 per share landing on February 13, 2026, representing the fourth consecutive quarter at that level and the highest per-share quarterly payment in the company’s recent history. That incremental climb from $0.09 to $0.10 per quarter reflects the kind of quiet, deliberate progress that defines how this management team operates.

On the financial performance side, the numbers remain compelling for a bank of this size. Revenue has reached nearly $82 million on a trailing basis, and net income stands at $36.5 million, producing an earnings per share figure of $2.16. Return on equity has climbed to a notably strong 15.33%, a meaningful step up from prior periods and a figure that compares favorably with many larger regional banking peers. Return on assets at 1.20% is also healthy and consistent with a well-run community bank franchise.

The stock currently sits at $22.49, within the lower half of its 52-week range of $20.00 to $27.41. Shares pulled back meaningfully from the top of that range, but the underlying business metrics have not deteriorated. For a bank posting a profit margin of 44.58% and a payout ratio of just under 18%, the current price level looks more like opportunity than warning sign.

Key Dividend Metrics 📊

📈 Dividend Yield: 1.77%

💵 Annual Dividend: $0.39 per share

📅 Last Dividend Payment: $0.10 per share (February 13, 2026)

📉 Payout Ratio: 17.67%

📊 5-Year Average Yield: 1.32%

🧱 Dividend Growth Streak: More than a decade of steady payouts

🪙 Last Stock Split: 2-for-1 in March 2023

Dividend Overview

GCBC isn’t a high-yield play, and that’s just fine. The bank pays a 1.77% yield at the current price, modest on an absolute basis but backed by one of the most conservative payout structures in the regional banking space. The annualized dividend now stands at $0.39 per share, and with earnings per share of $2.16, the coverage is extraordinarily wide.

The payout ratio of 17.67% is a standout figure. Very few dividend-paying companies in any sector operate with this degree of cushion, and in banking, where capital retention is essential for growth and regulatory compliance, that conservatism is a feature rather than a limitation. The bank simply does not need to stretch to maintain its dividend, and that gives management significant flexibility in how it allocates capital going forward.

GCBC also runs like clockwork when it comes to distributions. Investors can expect quarterly payments delivered consistently, with the most recent hitting accounts on February 13, 2026. The regularity of those payments is part of what makes this name appealing to income-oriented portfolios, particularly those that favor predictability over headline yield.

The 2023 stock split, a 2-for-1 move, brought more liquidity into the stock and signaled management’s intent to keep shares accessible to individual investors. For a company of this size, maintaining an investor-friendly capital structure makes a real difference in long-term shareholder engagement.

Dividend Growth and Safety

The dividend history tells a clear and encouraging story. Starting from $0.07 per quarter in May 2023, the bank has steadily lifted its payout through $0.08, then $0.09, and now $0.10 per quarter, reaching that level in the August 2025 payment and holding it through the most recent February 2026 distribution. That progression, while measured, reflects real earnings growth and a management team that prefers to raise the dividend only when it can do so durably.

With EPS of $2.16 and a quarterly dividend of $0.10, the bank is retaining the overwhelming majority of its earnings. That retained capital funds loan growth, supports the balance sheet, and keeps the bank well positioned for whatever the regulatory or economic environment demands. A return on equity of 15.33% confirms that this retained capital is being put to productive use rather than sitting idle.

Operating cash flow of nearly $33.9 million provides further reassurance. The dividend at its current annualized rate of $0.39 per share requires only a fraction of that cash generation, leaving ample room to fund capital expenditures, maintain liquidity buffers, and continue growing the payout over time. There is no scenario visible in the current financials where the dividend would be under pressure.

Insider ownership remains elevated, aligning management’s interests squarely with those of long-term shareholders. Short interest in the stock is negligible at just over 38,000 shares, suggesting no meaningful skepticism from the institutional side about the company’s near-term trajectory. For dividend investors, that combination of low payout ratio, rising earnings, and aligned ownership is about as strong a foundation as you can find in the community banking space.

The current yield of 1.77% sits comfortably above the stock’s five-year average yield of 1.32%, which suggests the shares are offering above-average income relative to their own history. That’s typically a positive entry signal for income investors who track yield relative to historical norms.

Chart Analysis

Greene County Bancorp has had a choppy but ultimately range-bound year, trading between a 52-week low of $20.40 and a high of $26.21, a spread of roughly 29% that reflects the kind of regional bank volatility income investors have had to stomach since rates moved to the forefront of market concern. The stock currently sits at $22.49, which places it about 14% below its 52-week peak and only about 10% above its annual floor. That positioning tells a fairly clear story: GCBC ran higher earlier in the cycle, gave back a meaningful portion of those gains, and is now consolidating in the lower half of its annual range without yet showing a convincing floor.

The moving average picture is a study in mixed signals. The 50-day moving average sits at $23.05 and the 200-day at $22.90, and the fact that the 50-day has crossed above the 200-day constitutes a technical golden cross, which is generally interpreted as a bullish longer-term signal. However, the current price of $22.49 is trading below both averages, which means GCBC has slipped under the very setup that the golden cross was meant to confirm. For dividend investors, this is a setup worth watching rather than acting on immediately, as a recovery back above both moving averages would add meaningful technical credibility to any near-term upside case.

The RSI reading of 32.77 is pressing close to oversold territory, with the conventional threshold sitting at 30. Momentum has clearly been to the downside in recent weeks, and the stock has not yet found the kind of stabilizing price action that would suggest sellers are exhausted. That said, readings in the low 30s have historically marked periods of attractive entry for patient income investors in community bank names, particularly when the underlying dividend and fundamentals remain intact. The RSI alone is not a buy signal, but it does indicate that the recent selling pressure has been substantial and that a mean-reversion bounce would not be technically surprising.

For dividend-focused investors, the chart presents a situation where price weakness has created a more attractive yield entry point, but confirmation is still lacking. GCBC needs to reclaim and hold above its 200-day moving average near $22.90 to shift the near-term technical tone. Investors who prioritize income over precise timing may find the current price level reasonable given the proximity to the 52-week low and the oversold RSI, while those who prefer to see technical momentum align before committing capital would be justified in waiting for a close back above both moving averages before adding exposure.

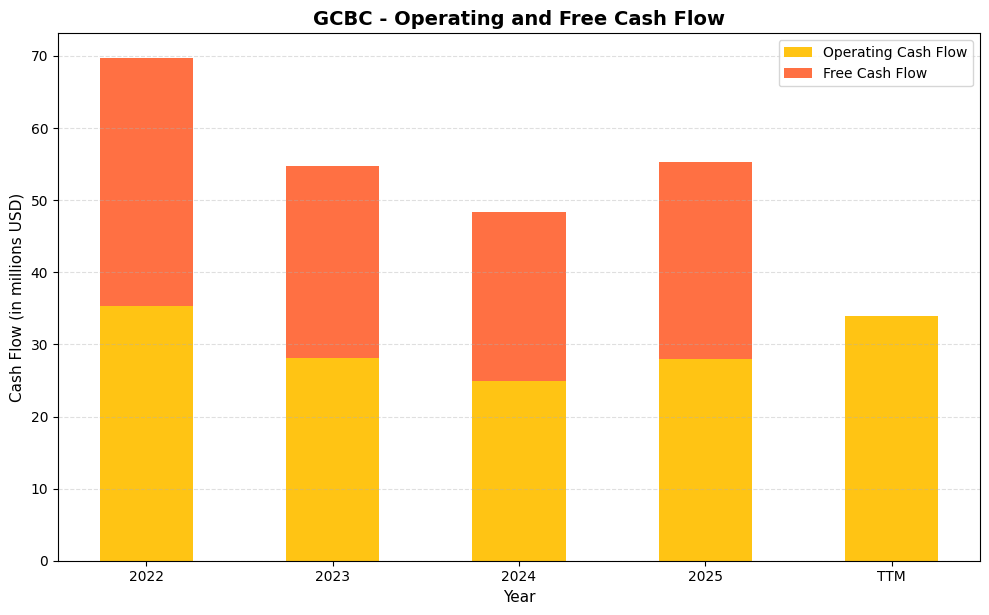

Cash Flow Statement

Greene County Bancshares has generated positive operating cash flow consistently across the measurement period, which provides a reasonable foundation for evaluating dividend sustainability. Operating cash flow ran at $35.4 million in 2022 before declining to $28.1 million in 2023 and $24.9 million in 2024, then recovering to $28.0 million in 2025 and reaching $33.9 million on a trailing twelve-month basis. Free cash flow has tracked closely with operating cash flow throughout, sitting at $34.3 million in 2022, compressing to $23.4 million at the 2024 trough, and rebounding to $27.3 million in 2025. The TTM free cash flow figure of $0.0 million is an anomaly likely reflecting a timing difference in capital expenditure reporting rather than a genuine collapse in cash generation, and investors should weight the 2025 annual figure more heavily when assessing how comfortably the dividend is covered by actual cash produced by the business.

The broader trend over this four-year window tells the story of a community bank that absorbed a meaningful squeeze in cash generation between 2022 and 2024, most plausibly driven by the higher interest rate environment compressing net interest margins and lifting funding costs, before beginning a clear recovery in 2025. Capital expenditures have remained minimal throughout, consistently representing less than $1.5 million annually, which reflects the asset-light infrastructure typical of a focused community banking model and means that virtually all operating cash flow converts into free cash flow available for dividends, buybacks, or retained capital. For dividend investors, the recovery trajectory from the 2024 trough is the most encouraging signal in this dataset, because it suggests the worst of the earnings and cash flow pressure has passed and that the current dividend level is being supported by a genuinely improving stream of cash rather than balance sheet maneuvering. Shareholders watching for confirmation of sustainability should monitor whether the TTM operating cash flow trend near $33.9 million is sustained into the next reporting period, as that level comfortably covers the dividend at current payout rates.

Analyst Ratings

Greene County Bancorp continues to attract limited formal analyst coverage, which is not unusual for a small-cap community bank with a market capitalization just under $383 million. No current consensus rating or formal price target data is available from the major brokerage platforms, and no recent analyst actions have been reported for the stock in this period.

The absence of active coverage does not diminish the investment case, but it does mean that price discovery for GCBC is driven primarily by fundamental value and retail investor interest rather than institutional research recommendations. In that context, the bank’s own financial metrics serve as the clearest guide to fair value. With a P/E ratio of 10.41, a price-to-book of 1.48, and EPS of $2.16, the stock screens as reasonably priced for a bank delivering 15.33% return on equity and a 44.58% profit margin.

The last known analyst action on record was an upgrade from sell to hold in April 2025, which reflected improving quarterly earnings momentum at the time. Given that earnings and return metrics have continued to strengthen since then, a reassessment from any firm initiating fresh coverage would likely start from a constructive baseline. For now, investors are largely on their own in evaluating the stock, which has historically suited the patient, long-term income investor that GCBC tends to attract.

Earning Report Summary

Strong Profitability Across the Trailing Period

Greene County Bancorp’s trailing twelve-month financial results paint a picture of a bank operating at a high level. Net income of $36.5 million on revenue of nearly $82 million translates to a profit margin of 44.58%, which is exceptional by any standard in regional banking. Earnings per share of $2.16 provide the foundation for the bank’s well-covered dividend and its ongoing capacity to retain capital for growth.

Return on equity has risen to 15.33%, a notable achievement for a community bank that continues to prioritize capital preservation alongside growth. Return on assets at 1.20% reflects efficient deployment of the balance sheet and confirms that the bank’s asset base, which has crossed $3 billion, is being put to productive use. These are not the metrics of a bank treading water; they reflect genuine operating improvement over prior periods.

CEO Perspective and Focus on Long-Term Strategy

CEO Donald Gibson has consistently emphasized organic growth and community relationships as the pillars of the bank’s strategy, and the financial results validate that approach. The bank’s growth from its first billion in assets, which took over a century, to more than $3 billion in a fraction of that time reflects the compounding power of disciplined community banking done right. Gibson’s focus on maintaining credit quality and managing the balance sheet conservatively has kept the bank out of the kind of trouble that has periodically afflicted more aggressive regional lenders.

The bank continues to monitor the broader interest rate environment carefully, with deposit pricing and net interest margin management remaining central to the conversation at the leadership level. There is no indication that management is reaching for yield or taking on incremental risk to sustain earnings growth, which is exactly the posture that long-term dividend investors should want to see.

Expense Discipline and Credit Quality

Operating expenses remain well managed relative to the bank’s revenue base, and credit quality indicators continue to reflect the conservative underwriting standards that have defined GCBC’s lending culture for decades. The allowance for credit losses remains appropriately funded, and there are no signals of deteriorating loan performance in the bank’s core markets across upstate New York and the Capital Region.

Steady Outlook Moving Forward

With earnings momentum intact, a rising dividend, and a balance sheet that remains conservatively managed, the outlook heading into the remainder of 2026 is constructive. Management’s stated priorities of organic growth, credit discipline, and community focus have produced consistent results, and there is little in the current environment to suggest a meaningful departure from that trajectory.

Management Team

Greene County Bancorp’s leadership is built around a team with deep community ties and a steady hand on long-term growth. Donald E. Gibson serves as President and CEO and has been with the bank for over three decades. Since taking the CEO role in 2007, he has overseen a period of consistent expansion, taking the bank from a local institution to a regional player with over $3 billion in assets. His philosophy revolves around organic growth, sound banking fundamentals, and staying deeply connected to the communities the bank serves.

Nick Barzee, Chief Financial Officer and Senior Vice President, adds another layer of financial discipline to the leadership team. With a background in public accounting and corporate finance, he has helped steer the bank through periods of growth and uncertainty with a conservative but forward-thinking approach. John Antalek oversees lending as Chief Lending Officer, helping to keep credit quality high while expanding the loan book in a sustainable way. Scott Houghtaling, Chief Credit and Banking Officer, provides oversight on credit risk and helps maintain balance as the bank grows. The board of directors is led by Jay Cahalan and supported by professionals from fields ranging from finance to hospitality, bringing diversity and broad oversight to strategic decisions.

Valuation and Stock Performance

As of February 24, 2026, Greene County Bancorp shares are trading at $22.49, sitting in the lower portion of the stock’s 52-week range of $20.00 to $27.41. The pullback from the upper end of that range has occurred against a backdrop of improving fundamentals, which creates an interesting dynamic for value-conscious income investors evaluating the stock today.

The current market cap stands at approximately $383 million, keeping GCBC firmly in small-cap territory. Valuation metrics are undemanding given the bank’s profitability profile. The price-to-earnings ratio of 10.41 is modest for a bank generating a 15.33% return on equity and a profit margin above 44%, and the price-to-book ratio of 1.48 represents a reasonable premium to the $15.17 book value per share given the quality of the earnings stream. For context, well-run community banks with returns on equity in the mid-teens typically command higher multiples than GCBC is currently receiving.

The stock’s beta of 0.39 reflects its historically low correlation to broader market swings, making it a natural fit for defensive income portfolios. Over a longer timeframe, patient shareholders have been rewarded by a combination of dividend growth and capital appreciation, and the current valuation does not appear to price in the continued earnings momentum the bank has demonstrated. For investors focused on total return over a multi-year horizon, the current entry point looks more attractive than the recent price history alone might suggest.

Risks and Considerations

Interest rate sensitivity remains the most prominent variable for any community bank, and GCBC is no exception. A sustained decline in rates could compress net interest margins and weigh on the earnings growth that has driven the recent dividend progression. Conversely, a sharp rate increase could pressure borrowers and elevate credit costs. Management has navigated rate cycles with discipline historically, but this risk is structural and does not disappear regardless of how well the bank is run.

Geographic concentration is a meaningful consideration for a bank whose operations are focused on upstate New York, the Hudson Valley, and the Capital Region. If local employment conditions weaken or regional real estate markets soften, loan quality and deposit growth could be affected. The bank’s conservative underwriting standards provide a buffer, but no community lender is fully insulated from the economic cycles of its home market.

Regulatory compliance costs continue to rise across the banking industry, and community banks often bear these burdens disproportionately relative to their size. Changes in capital requirements, consumer protection rules, or reporting standards can require meaningful investment in staffing and systems, which can create margin pressure even for a well-managed institution like GCBC.

Competition from larger national banks and technology-driven financial services providers remains a long-term structural challenge. GCBC has historically differentiated itself through personalized service and deep community relationships, but sustaining that advantage requires ongoing investment in digital capabilities and customer experience. The bank’s conservative capital allocation approach means technology investment competes with other priorities, and falling behind on digital infrastructure could gradually erode its competitive positioning over time.

Final Thoughts

Greene County Bancorp enters 2026 in genuinely strong financial shape. Earnings per share of $2.16, a return on equity of 15.33%, a profit margin above 44%, and a payout ratio of under 18% collectively describe a bank that is performing at a high level while remaining firmly committed to capital discipline. The dividend has grown steadily from $0.07 per quarter in mid-2023 to $0.10 today, and the earnings foundation suggests further growth is achievable without any meaningful strain on the bank’s finances.

The stock’s current price of $22.49 and P/E ratio of 10.41 do not fully reflect the quality of the underlying business, which creates a patient investor’s setup rather than a speculative one. The low beta, high insider ownership, negligible short interest, and conservative management philosophy all point to a company that is unlikely to generate dramatic headlines but quite likely to keep delivering steady results for shareholders who give it time.

Risks around interest rates, geographic concentration, and competitive pressure are real and worth monitoring, but none of them represent near-term threats to the dividend or to the bank’s fundamental operating trajectory. For long-term income investors who value consistency, transparency, and a management team that has consistently done what it said it would do, Greene County Bancorp remains a sound and straightforward holding.