Key Takeaways

💸 GD offers a 1.72% forward dividend yield with 33 consecutive years of growth and a conservative 38.83% payout ratio, making it a dependable income-generating stock.

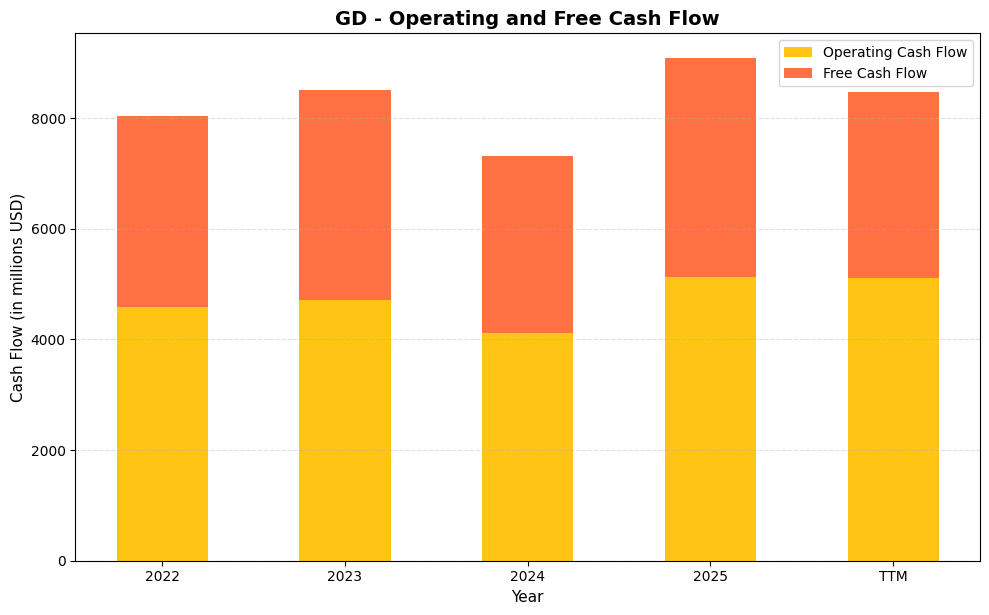

💼 The company generated $5.11 billion in operating cash flow and $3.36 billion in free cash flow over the trailing 12 months, providing strong coverage for dividends and buybacks.

📊 Analyst sentiment is constructive, with a consensus buy rating across 20 analysts and a mean price target of $394.53, reflecting confidence in GD’s earnings stability and long-term contract visibility.

Updated 2/24/26

General Dynamics Corporation (GD) is a defense and aerospace company delivering reliable earnings, strong free cash flow, and consistent dividend growth. With a $95 billion market cap and 33 consecutive years of dividend increases, GD combines a solid financial profile with a deep backlog of government contracts. Its operations span marine systems, combat technologies, and Gulfstream business jets, with trailing twelve-month results showing revenue exceeding $52.5 billion and earnings per share of $15.45.

The company maintains a forward dividend yield of 1.72%, supported by a sub-39% payout ratio and $3.36 billion in free cash flow over the trailing 12 months. General Dynamics’ leadership, led by CEO Phebe Novakovic, has focused on execution and capital discipline, while a consensus buy rating from 20 analysts and a mean price target of $394.53 reflect healthy institutional confidence in the company’s direction.

Recent Events

General Dynamics has continued operating from a position of strength heading into early 2026. Defense demand globally remains elevated, and the company’s marine systems division is benefiting directly from sustained government investment in submarine production, a program that carries multi-year visibility and strong funding support from Congress. The Gulfstream aerospace segment has also been working through its production ramp on newer aircraft models, with delivery schedules and manufacturing throughput remaining key operational focal points for the business.

On the capital allocation front, the company raised its quarterly dividend to $1.50 per share beginning with the April 2025 payment, up from $1.42, continuing a streak of annual increases that now spans 33 consecutive years. That increase represented approximately a 5.6% raise and underscored management’s confidence in the durability of the company’s cash generation. The defense environment broadly remains supportive, with allied nations continuing to expand procurement and U.S. defense budgets remaining a stable foundation for GD’s contract pipeline.

Key Dividend Metrics

🟢 Dividend Yield: 1.72%

🟡 Five-Year Average Yield: 2.27%

🟢 Annual Dividend Rate: $6.00

🟢 Payout Ratio: 38.83%

🟢 Dividend Growth Streak: 33 consecutive years

🟢 Last Dividend Payment: $1.50 (paid January 16, 2026)

🟡 Last Split: 2-for-1 in March 2006

These numbers tell a story of dependability. The forward yield of 1.72% sits below the company’s five-year average of 2.27%, which reflects a stock price that has appreciated meaningfully over the past year. When paired with a sub-39% payout ratio and over three decades of uninterrupted increases, the income profile adds up to something better than flash — it adds up to trust.

Dividend Overview

The dividend at General Dynamics is one of its most dependable traits. While some companies boast yields that are unsustainable or erratic, GD offers something more useful for patient investors: consistency. A 1.72% forward yield may not top income screeners, but it is steady, backed by a healthy balance sheet, and comes with low volatility. For long-term dividend investors, that combination is precisely what matters.

With 33 straight years of growth, General Dynamics has cemented its place among the most reliable dividend payers in the market. That consistency is not just the product of strong profits. It is supported by serious free cash flow generation, with $5.11 billion in operating cash flow and $3.36 billion in free cash flow over the trailing twelve months. The dividends paid over that same period represent a fraction of that output, leaving the coverage ratio firmly in comfortable territory with no balance sheet stress required to sustain it.

The company’s financial position reinforces this picture. General Dynamics is not overleveraged, and its operations run on the kind of long-duration government contracts that most businesses cannot replicate. That structural stability is a primary reason GD can keep rewarding shareholders through varying market environments. The return on equity sits at 17.66% and return on assets at 5.99%, both reflecting efficient use of capital within a capital-intensive industry.

The stock’s beta of 0.40 is also worth appreciating in context. It moves substantially less than the broader market, which can be a meaningful comfort for income investors who prioritize consistent cash flow over price excitement. That combination of low volatility and reliable dividend growth makes General Dynamics a core-type holding for conservative income portfolios.

Dividend Growth and Safety

There is nothing erratic or surprising about how General Dynamics handles its dividend. The most recent increase, which took the quarterly payment from $1.42 to $1.50 per share beginning in April 2025, represented a raise of approximately 5.6%. That pace is consistent with the company’s historical cadence of mid-single-digit to low-double-digit annual increases, and it fits squarely within a capital allocation philosophy that prioritizes sustainability over splashy moves.

Looking at the payout ratio, which stands at 38.83%, there is no meaningful pressure on the dividend. EPS currently sits at $15.45 while the annual dividend is $6.00. That gap is substantial and provides meaningful cushion even if earnings were to soften in a given year. The company has room to continue raising the payout at a healthy rate without approaching any threshold that would concern a conservative income investor.

Capital allocation here is deliberate. General Dynamics is not loading up on debt to chase buybacks or acquisitions. It is sticking to what it knows: delivering for government customers, operating efficiently, and sharing the results with shareholders. That approach has worked for more than three decades of consecutive increases, and nothing in the current financial picture suggests it is about to change.

The most recent dividend was paid at $1.50 per share on January 16, 2026, continuing the same rate established in April 2025. The streak continues, quietly but powerfully, and General Dynamics looks well-positioned to extend it further when the next annual review arrives.

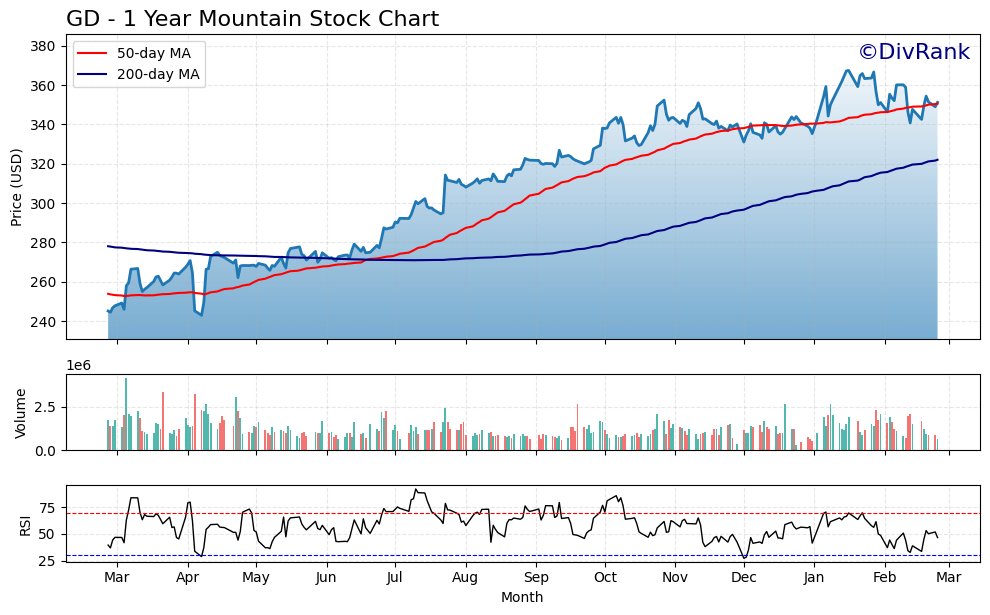

Chart Analysis

General Dynamics has staged an impressive recovery over the past year, climbing from a 52-week low of $242.99 to its current price of $351.18, a gain of roughly 44.5% from trough to present. The stock reached a 52-week high of $367.38 earlier in the cycle and is currently trading just 4.4% below that peak, suggesting the bulk of the recovery momentum has already been captured but that price remains well-supported near recent highs. For a defense contractor of GD’s size and stability, this kind of sustained price appreciation alongside a consistent dividend is exactly the profile income investors want to see. The broader trend over the past twelve months has been constructively bullish, with no signs of a structural breakdown in the chart.

The moving average picture reinforces that constructive read. GD is trading above both its 50-day moving average of $350.52 and its 200-day moving average of $322.03, and the 50-day has crossed above the 200-day to form what technicians call a golden cross, a configuration that historically signals sustained upward momentum rather than a short-term bounce. The gap between the 200-day and the current price is roughly $29, or about 9%, which means long-term trend support is well established and the stock would need a meaningful pullback before that structural foundation came into question. For dividend investors focused on entry points, the proximity of price to the 50-day average near $350 suggests that level could serve as a reasonable near-term support zone on any weakness.

Momentum, as measured by the 14-day Relative Strength Index, sits at 46.67, placing GD in essentially neutral territory. The stock is neither overbought nor showing signs of capitulation to the downside, which is a comfortable position for an income investor evaluating a new entry. An RSI approaching 70 would raise the concern that the stock is running hot and due for a rest; an RSI in the low 30s would suggest selling pressure is dominating. At 46.67, GD is in a balanced state, having absorbed some consolidation pressure after its run toward the 52-week high without surrendering the underlying trend.

Taken together, the technical setup for General Dynamics is supportive rather than urgent. The golden cross, the above-average positioning relative to both moving averages, and the neutral RSI combine to paint a picture of a stock that has already done its heavy lifting on the upside and is now consolidating at elevated levels. Dividend investors are not being asked to chase the stock into overbought conditions, and the well-established 200-day moving average nearly $30 below current price provides a meaningful cushion of trend support. For investors prioritizing income over short-term price appreciation, the current chart does not present a red flag in either direction, making GD a technically stable backdrop for evaluating the fundamental dividend case.

Cash Flow Statement

General Dynamics generates substantial cash flow, and the numbers make a compelling case for dividend sustainability. Operating cash flow climbed from $4,579.0 million in 2022 to $4,710.0 million in 2023 before dipping to $4,112.0 million in 2024, a year that reflected heavier working capital demands tied to program ramp-ups across its defense segments. The recovery was sharp and decisive, with operating cash flow rebounding to $5,120.0 million in 2025 and the TTM figure holding firm at $5,110.0 million. Free cash flow tells a similarly encouraging story. After reaching $3,806.0 million in 2023, it pulled back to $3,196.0 million in 2024 alongside elevated capital expenditures, then surged to $3,959.0 million in 2025. With GD’s annual dividend obligation running well below $2.0 billion, the free cash flow coverage ratio is generous, leaving management ample room to fund dividend increases, share repurchases, and strategic investments without straining the balance sheet.

Viewed across the full four-year arc, General Dynamics has demonstrated a cash-generating engine that is both resilient and growing in capacity. The 2024 moderation was a detour rather than a deterioration, and the 2025 rebound confirms the underlying earning power of the business. Capital expenditure discipline is evident in the relationship between operating and free cash flow. The spread between the two has widened only modestly over time, indicating that reinvestment needs, while real, are not consuming an outsized share of cash generation. For dividend growth investors, this profile is exactly what matters most: a business that consistently converts earnings into actual cash, sustains that conversion through a full business cycle, and emerges with more capacity to reward shareholders than it had going in. The TTM free cash flow of $3,357.3 million, while slightly below the 2025 annual figure due to timing, still represents a payout coverage ratio that most income portfolios would find reassuring.

Analyst Ratings

Analyst sentiment on General Dynamics is constructive heading into early 2026. Across 20 analysts covering the stock, the consensus rating stands at buy, with a mean price target of $394.53. That target implies meaningful upside from the current price of $351.18, suggesting that the analyst community sees the stock as reasonably valued or modestly underpriced relative to its fundamentals and contract visibility. The range of targets is fairly wide, from a low of $327.00 to a high of $444.00, which reflects some divergence of opinion on the pace of aerospace recovery and the trajectory of defense spending priorities.

The lower end of that target range, at $327.00, sits below the current market price, indicating that not all analysts are uniformly bullish, and some caution remains around execution risk in the Gulfstream segment and the potential for defense budget volatility under evolving political conditions. The high end at $444.00 reflects a more optimistic scenario where both the defense backlog converts efficiently and the aerospace unit continues to gain production momentum. The mean target of $394.53 strikes a balance between these views and implies approximately 12% upside from current levels, a reasonable setup for a low-beta, income-oriented name.

With a beta of 0.40 and a well-covered dividend, the investment case here does not hinge on a dramatic re-rating. Even in the absence of significant multiple expansion, the combination of earnings growth, dividend increases, and buyback activity provides a credible path to solid total returns for patient shareholders.

Earning Report Summary

Strong Full-Year Financial Profile

General Dynamics closed out its most recent trailing twelve-month period with $52.55 billion in revenue and net income of $4.21 billion, translating to earnings per share of $15.45. Those figures reflect a business operating at scale across both its defense and aerospace segments, with profitability running at an 8.01% net margin. Operating cash flow of $5.11 billion significantly exceeded net income, which is a hallmark of high-quality industrial businesses and speaks to the non-cash-intensive nature of GD’s government contract portfolio.

Aerospace Segment Execution

The Gulfstream aerospace division has remained a focus area for management, with production throughput and delivery timing at the center of operational attention. Margins in this segment are sensitive to aircraft mix, production rates, and supply chain reliability, and leadership has consistently emphasized investment in manufacturing processes and workforce capability as the foundation for sustainable profitability. Improvement in delivery schedules and economies of scale as production ramps on newer Gulfstream models are expected to drive incremental margin expansion over time.

Defense Segments Provide Steady Foundation

The Marine Systems, Combat Systems, and Technologies divisions continue to provide the stable, contract-driven revenue base that defines the GD investment thesis. Marine Systems in particular benefits from multi-year submarine programs that carry strong Congressional support and predictable funding profiles. Combat Systems has maintained steady demand tied to both domestic procurement and international allied defense spending, while the Technologies segment continues to serve as a meaningful contributor to revenue and earnings across its portfolio of government IT and services programs.

Backlog and Order Visibility

General Dynamics operates with a substantial backlog that provides revenue visibility well beyond any single fiscal year. That pipeline of awarded contracts and options represents one of the most compelling structural advantages in the defense sector, insulating the company from short-term demand fluctuations and providing management with a reliable foundation for capital planning. New award activity has remained healthy, supported by a defense procurement environment that continues to favor established prime contractors with proven execution track records.

Capital Allocation and Shareholder Returns

Management has continued to balance investment in operations with returns to shareholders. Dividends, share repurchases, and debt management remain the primary uses of free cash flow, and the company’s return on equity of 17.66% reflects disciplined deployment of capital over time. The $6.00 annual dividend is well-covered at a 38.83% payout ratio, and the company’s financial profile provides flexibility to continue raising the dividend annually without compromising balance sheet integrity.

Management Team

General Dynamics is led by Chairman and CEO Phebe Novakovic, who has held the top position since 2013. Her leadership style leans heavily on operational rigor and long-term planning. She has earned a reputation for being both strategic and hands-on, helping the company navigate through industry cycles with a steady hand. Over the years, she has overseen key investments in technology, workforce expansion, and production capacity, particularly across the company’s defense and aerospace operations.

Supporting her is a seasoned leadership team. Kimberly Kuryea, the Chief Financial Officer, plays a central role in maintaining the company’s financial health and capital allocation strategy. Jason Aiken, Executive Vice President of Technologies, brings deep operational experience, having previously served as CFO. Together, the executive team has built a stable culture that balances shareholder returns with forward-looking investments in growth, and their collective tenure reflects an organization that values continuity and execution over change for its own sake.

Valuation and Stock Performance

As of February 24, 2026, General Dynamics stock trades at $351.18, giving the company a market cap of approximately $95 billion. The trailing price-to-earnings ratio sits at 22.73 and the price-to-book ratio at 3.70 against a book value per share of $94.90. These multiples reflect a premium relative to the company’s historical averages, driven in part by a stock that has appreciated considerably from the 52-week low of $239.20 while remaining below the 52-week high of $369.70. At current levels, the stock is not cheaply priced, but it is not unreasonably expensive for a business with GD’s earnings quality, contract visibility, and capital return profile.

The stock has moved across a wide range over the past twelve months, with that 52-week spread of $239.20 to $369.70 reflecting shifts in defense spending sentiment, interest rate dynamics, and broader industrial sector rotation. At $351.18, shares sit toward the upper portion of that range, which is consistent with an improved earnings trajectory and continued analyst confidence. The beta of 0.40 means the stock continues to behave as a low-volatility anchor within a diversified portfolio, a characteristic that income investors have long valued in GD.

The analyst consensus mean price target of $394.53 implies roughly 12% upside from current levels. Combined with the 1.72% dividend yield and ongoing share repurchase activity, the total return picture is reasonable for a conservative, income-oriented position. The valuation does not leave much room for disappointment on execution, but General Dynamics has demonstrated over many years that execution is what it does best.

Risks and Considerations

While General Dynamics benefits from long-term defense contracts and a deep backlog, it is not without risks. Shifts in U.S. or allied defense budgets could impact new awards or slow down certain programs. Political transitions, evolving spending priorities in Washington, and debates over discretionary versus mandatory budget allocations all represent variables that could affect the pace of new contract awards, even if existing programs remain well-funded in the near term.

The aerospace division faces its own ongoing challenges. Supply chain constraints, certification timelines, and the complexity of ramping production on newer Gulfstream models have created periodic pressure on delivery schedules and segment-level margins. These are not uncommon issues in aircraft manufacturing, but they can influence both revenue recognition timing and investor expectations in ways that introduce short-term uncertainty around what is otherwise a premium franchise.

Labor dynamics in the Marine Systems segment remain a consideration worth monitoring. Submarine production programs are highly skilled-labor-intensive, and workforce availability, training timelines, and contract negotiations can all affect delivery schedules. Any disruption to production flow in this segment would have downstream implications for revenue timing and cost efficiency, even if the underlying contract values remain intact.

Finally, the current valuation leaves relatively little margin for error. At a P/E of 22.73, shares are priced for continued execution and stable earnings growth. Any shortfall in Gulfstream deliveries, a defense budget surprise, or a broader re-rating of industrial multiples could compress the stock, even without any fundamental deterioration in the business. Investors entering at current levels should be comfortable with that context.

Final Thoughts

General Dynamics stands out not because it is flashy, but because it is steady. It is not trying to reinvent itself every few quarters. Instead, it keeps doing what it does best: manufacturing complex systems, fulfilling high-value defense contracts, and returning capital to shareholders. The balance between its aerospace and defense units offers a cushion during sector slowdowns and provides a measure of diversification that few pure-play defense companies can match.

Leadership is experienced, the order book is deep, and financial discipline runs through every part of the business. With 33 consecutive years of dividend growth, a well-covered payout at 38.83%, and $5.11 billion in operating cash flow backing the whole operation, General Dynamics is the kind of company that does not need to chase headlines to generate value. As long as it continues executing on its backlog and adapting to shifts in defense and aviation trends, it remains a reliable name for long-term income and capital preservation.