Key Takeaways

📈 First United Corporation offers a forward dividend yield of 2.62% with a low payout ratio of 24.40%, suggesting a well-covered and potentially growing dividend that has seen two increases since late 2023.

✅ The sole analyst covering FUNC carries a price target of $44.00, implying meaningful upside of roughly 23% from the current price of $35.83, reflecting confidence in the company’s disciplined fundamentals.

💰 First United has grown its quarterly dividend from $0.20 to $0.26 per share over the past two years, with the most recent increase arriving in October 2025, underscoring management’s commitment to rewarding shareholders as earnings improve.

Updated 2/24/26

First United Corporation, trading under the ticker FUNC, might not pop up on most investors’ radars, but for those with a long view and an appetite for stable dividend income, this small regional bank is worth a closer look. Based in Oakland, Maryland, FUNC runs a traditional community banking operation through its subsidiary, First United Bank & Trust, with a focus on personal and small business banking.

Its approach is refreshingly straightforward: build relationships, manage risk carefully, and return profits to shareholders. That philosophy has quietly rewarded investors, especially those in it for the dividend.

Recent Events

First United Corporation has continued to operate as a steady, low-drama community bank in western Maryland, which is precisely what its shareholder base tends to appreciate. The bank has not made any splashy acquisition announcements or major strategic pivots in recent months. Instead, it has focused on executing its core community banking strategy, with management emphasizing organic growth in its existing markets and ongoing investment in technology and customer-facing infrastructure. That consistency in operating posture is a hallmark of how FUNC has built its reputation among regional bank followers.

The bank raised its quarterly dividend to $0.26 per share in October 2025, a step up from the $0.22 rate that had been in place since October 2024. That dividend was paid again in January 2026, confirming the new rate is holding. The progression from $0.20 to $0.22 and then to $0.26 over roughly two years shows a clear, if deliberate, upward trajectory. With a market cap sitting just below $233 million and a beta of 0.52, FUNC continues to trade as a quiet compounder rather than a momentum play. The stock is currently trading at $35.83, which sits in the lower half of its 52-week range of $24.66 to $41.95, suggesting some pullback from earlier highs.

Return on equity has climbed to 13.36% and return on assets stands at 1.26%, both solid readings for a bank of this size and geography. Profit margins of nearly 30% reflect a management team that has kept a firm grip on expenses while growing the revenue base to $83.7 million on a trailing basis.

Key Dividend Metrics

📈 Forward Yield: 2.62%

💵 Annual Dividend Rate: $0.96

📆 Most Recent Dividend Payment: January 16, 2026

📊 Payout Ratio: 24.40%

📉 EPS: $3.77

💡 Last Quarterly Dividend: $0.26 per share

Dividend Overview

First United isn’t chasing headlines with its dividend. Instead, it does what longtime income investors hope for, paying consistently and conservatively while leaving room for modest but meaningful growth. At a current yield of 2.62%, it may not lead the pack among financial sector dividend payers, but the payout is well-covered and has demonstrated real momentum over the past two years.

A payout ratio of just 24.40% shows that FUNC is playing it safe. With earnings per share of $3.77 and a quarterly dividend of $0.26, the bank is retaining the vast majority of its profits for reinvestment and balance sheet strength. That leaves considerable runway for future increases without any meaningful strain on the business.

The current yield of 2.62% sits below the five-year average of roughly 3.40%, which reflects the stock’s appreciation from its lows rather than any weakening in dividend commitment. When yield compresses because the stock price has risen, that is a sign of strength, not a warning flag. Investors who owned FUNC a year ago have benefited from both price appreciation and a dividend that has grown 30% from the $0.20 quarterly level that held through most of 2023 and 2024.

With fewer than 6.5 million shares outstanding and strong earnings coverage, FUNC is more than capable of sustaining and growing its dividend even if the interest rate environment softens. The small share count also means incremental dividend increases are capital-efficient for the company.

Dividend Growth and Safety

FUNC has now executed two dividend increases since late 2023, moving from $0.20 per quarter to $0.22 in October 2024 and then to $0.26 in October 2025. That second step-up of roughly 18% in a single move signals growing confidence from management in the bank’s earnings power. For a company of this size operating in a community banking model, that pace of dividend growth is genuinely encouraging.

Operating cash flow over the trailing twelve months came in at $18.7 million, comfortably ahead of the roughly $6.3 million needed to fund the annual dividend at the current rate and share count. That coverage ratio gives the dividend a wide margin of safety even in a scenario where loan losses or margin compression weigh on near-term earnings. The bank’s net income of $24.9 million provides further reassurance that the payout is firmly supported at the earnings level as well.

Insider ownership remains a constructive feature of the FUNC shareholder structure. Management and insiders holding a meaningful stake in the company tend to think twice before cutting a dividend they themselves collect. Combined with institutional ownership that keeps the stock from being entirely thinly traded, the ownership mix reflects a stable capital base aligned with long-term value creation.

FUNC’s dividend isn’t the kind you chase for immediate yield. It’s the kind you count on for years, the kind that sticks around through cycles and quietly compounds in your portfolio. The recent acceleration in growth rate makes it more interesting today than it was two years ago.

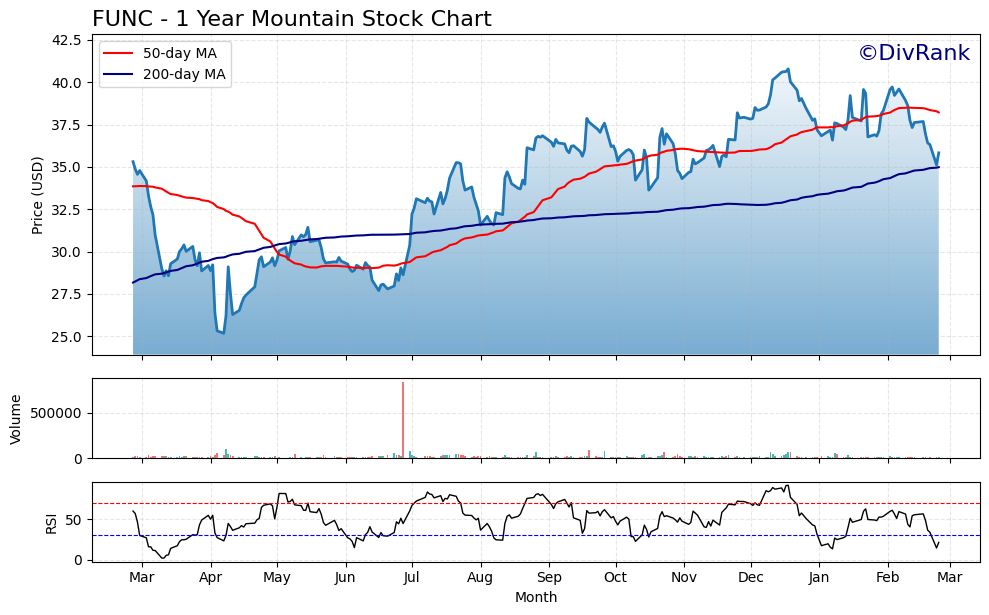

Chart Analysis

First Community Bancorp’s chart tells a compelling recovery story over the past twelve months. Shares have surged roughly 42% off their 52-week low of $25.17, reflecting a meaningful rerating as regional bank sentiment improved and the company’s fundamentals reasserted themselves with investors. The stock reached a peak of $40.79 before pulling back to the current level of $35.83, a retreat of about 12% from that high. That kind of consolidation after a strong run is not unusual, and for dividend investors focused on accumulating shares at reasonable prices, the current setup is more interesting than the chart was six months ago when momentum alone was driving the price higher.

The moving average picture is constructive at the intermediate and longer-term levels. The 200-day moving average sits at $34.98, and with FUNC trading at $35.83, the stock is holding just above that long-term trend line, which now acts as a meaningful floor of technical support. More encouraging is the relationship between the 50-day and 200-day averages, which are configured in a golden cross formation, a pattern where the shorter-term average trades above the longer-term one and is broadly interpreted as a bullish structural signal. The one area of near-term caution is that FUNC has slipped below its 50-day moving average of $38.22, which suggests the recent pullback has some momentum behind it and that the stock may need time to stabilize before reclaiming that level.

The RSI reading of 21.35 is the most striking data point on the chart right now. That figure places FUNC in deeply oversold territory, well below the 30 threshold that most technicians use to flag potential exhaustion of selling pressure. Readings at this extreme rarely persist for long, and historically they tend to precede at least a short-term stabilization or bounce. For a dividend investor, an oversold RSI is not a reason for alarm on its own. It is more useful as a signal that near-term selling may be overdone relative to the underlying business fundamentals, and that waiting for a confirmed reversal rather than chasing earlier strength could prove rewarding.

Taken together, the chart presents a mixed but ultimately encouraging setup for a long-term income investor. The primary trend over the past year has been decidedly positive, the golden cross confirms that longer-term momentum remains favorable, and the stock is holding above its 200-day average despite the recent pressure. The pullback from the 52-week high and the deeply oversold RSI reading suggest that patient investors may have an opportunity to build or add to a position at a more attractive entry point than was available earlier in the year. As always, dividend investors should treat the technical picture as one input alongside payout sustainability and valuation rather than a standalone decision driver.

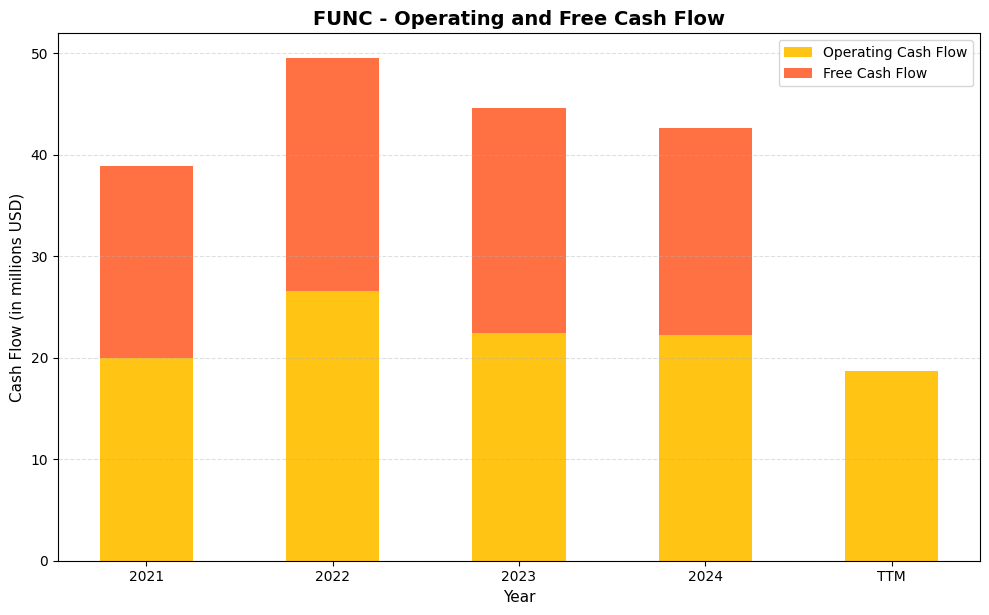

Cash Flow Statement

First Community Bankshares (FUNC) has generated reasonably consistent operating cash flow over the period examined, moving from $20.0M in 2021 to a peak of $26.5M in 2022 before settling back into the low $20M range through 2023 and 2024. Free cash flow has tracked closely with operating cash flow throughout most of this period, reflecting modest capital expenditure requirements that are typical of a community banking business model. The 2023 and 2024 figures of $22.1M and $20.4M in free cash flow are more than sufficient to cover the company’s dividend obligations, which provides a reasonable degree of comfort for income investors focused on payout sustainability. The TTM free cash flow reading of $0.0M does warrant attention, as it suggests either a meaningful capital expenditure event or a timing-related distortion in the most recent trailing period, and investors should monitor whether this normalizes in upcoming quarters.

Stepping back across the full timeline, FUNC’s cash generation profile reflects a business that converts its earnings into actual cash at a high rate, which is a hallmark of well-run community banks with disciplined loan portfolios and controlled overhead. The 2022 peak of $26.5M in operating cash flow likely benefited from the rising rate environment that expanded net interest margins across the regional banking sector, and the subsequent moderation to the $22M range represents a more normalized baseline rather than structural deterioration. Capital intensity has remained low through most of this window, as evidenced by the tight spread between operating and free cash flow in 2023 and 2024, meaning the company has not needed to consume large portions of its operating earnings to maintain or grow its asset base. For dividend-focused shareholders, a business that routinely converts operating income into free cash with minimal friction is exactly the kind of foundation that supports consistent and potentially growing income distributions over time.

Analyst Ratings

Coverage of First United Corporation remains thin, with a single analyst currently tracking the stock. That analyst carries a price target of $44.00, which sits well above the current trading price of $35.83. The implied upside of approximately 23% is meaningful for a stock with a beta of just 0.52, and the target appears grounded in the bank’s demonstrated earnings power and improving return metrics rather than speculative assumptions.

With EPS of $3.77 and a P/E ratio of 9.50, FUNC is trading at a modest multiple relative to its earnings, and the $44.00 target would imply a P/E closer to 11.7 times, still well within reasonable territory for a profitable regional bank with a clean balance sheet. The price-to-book ratio of 1.17 against a book value of $30.64 per share reflects a slight premium to tangible assets, which is consistent with a bank generating returns on equity above 13%.

The limited analyst coverage is a common feature of small-cap community banks and reflects the research economics of covering a $233 million market cap company rather than any fundamental concern about the business. Investors in names like FUNC typically rely on their own due diligence alongside the occasional institutional note, and the price target on record does provide a useful external benchmark for valuation.

Earning Report Summary

How the Full Year Shaped Up

First United Corporation has delivered strong full-year results on a trailing basis, with net income reaching $24.9 million and earnings per share of $3.77. Revenue came in at $83.7 million, representing continued growth from prior periods and reflecting the bank’s ability to expand its earning asset base while managing its cost structure. Return on equity of 13.36% is one of the stronger readings the bank has posted in recent years and compares favorably with peers in the community banking space. The profit margin of 29.79% confirms that management has maintained expense discipline even as the bank has grown.

Digging into the Numbers

Return on assets of 1.26% is a solid figure for a bank of FUNC’s size and geography, indicating that the balance sheet is being deployed efficiently rather than simply growing for the sake of scale. The low payout ratio of 24.40% means that even with two dividend increases executed over the past 18 months, the bank has retained the substantial majority of its earnings for reinvestment. Operating cash flow of $18.7 million provides a clear picture of the core cash-generating engine of the business, and the gap between operating cash flow and the annual dividend obligation of roughly $6.3 million leaves a comfortable buffer for unexpected credit costs or margin compression.

What the Leaders Had to Say

Management at First United has consistently emphasized the importance of maintaining a strong capital foundation and executing on the bank’s community-focused strategy. The decision to raise the quarterly dividend to $0.26 per share in October 2025 was a clear signal that leadership is confident in the sustainability of current earnings levels. Management has also continued to reference ongoing investments in technology and operational infrastructure as priorities, with the goal of improving customer experience and operating efficiency over the medium term without sacrificing the cost discipline that has driven margin improvement.

Looking Towards the Future

Going forward, First United appears positioned to continue its strategy of deliberate organic growth within its existing markets in western Maryland and surrounding communities. The bank’s strong capital ratios, conservative credit culture, and improving return metrics provide a solid foundation for navigating whatever interest rate environment emerges in 2026. Management has not signaled any appetite for transformative acquisitions, which keeps execution risk low and keeps the focus squarely on serving its core customer base and returning capital to shareholders through a growing dividend.

Management Team

First United Corporation is led by a management team with deep roots in community banking and a clear preference for steady execution over headline-grabbing strategy shifts. The leadership approach at FUNC has long prioritized balance sheet conservatism, relationship-driven lending, and consistent capital returns. That philosophy is evident in the bank’s low beta, conservative payout ratio, and its pattern of raising the dividend only when earnings clearly support it.

The CEO and executive team have maintained a consistent strategic direction, investing selectively in technology and infrastructure while keeping operating expenses in check. The alignment between management’s stated priorities and the financial results the bank has delivered, including improving returns on equity and assets, suggests that the team is executing effectively. With insider ownership providing meaningful skin in the game, there is a natural incentive for management to maintain the kind of financial discipline that has historically served FUNC’s shareholders well.

Valuation and Stock Performance

At $35.83, FUNC is trading in the lower half of its 52-week range of $24.66 to $41.95, having pulled back from the highs reached earlier in the cycle. The current P/E ratio of 9.50 times trailing earnings of $3.77 per share is a modest multiple for a bank generating returns on equity above 13% and growing its dividend at a meaningful pace. A price-to-book ratio of 1.17 reflects a slight premium to the $30.64 book value per share, which is entirely appropriate given the profitability profile of the business.

The single analyst covering the stock has set a $44.00 price target, implying upside of roughly 23% from current levels. That target would place FUNC at approximately 11.7 times trailing earnings, still a conservative multiple by most regional bank standards. For income investors, the combination of a 2.62% yield, a growing dividend, and a stock trading below its recent highs creates a reasonably attractive entry point.

With a beta of 0.52, FUNC does not tend to move dramatically with broader market swings, which is both a feature and a limitation. In a risk-on environment, the stock will likely lag high-beta financials. In a period of market stress, it tends to hold up relatively well. For investors who prioritize income stability and capital preservation alongside modest growth, that low-volatility profile is a meaningful part of the total return picture.

Risks and Considerations

As a community bank operating primarily in western Maryland, FUNC carries meaningful geographic concentration risk. Its loan portfolio and deposit base are tied to the economic health of a relatively small regional economy, which means a localized downturn in employment or real estate could have an outsized impact on credit quality compared with a more geographically diversified institution. Investors should be aware that the bank’s fortunes are closely linked to conditions in its core market.

Interest rate sensitivity is a persistent consideration for any bank, and FUNC is no exception. The bank’s net interest margin has benefited from the higher rate environment of recent years, and any meaningful decline in rates could compress margins and reduce earnings power. While the bank’s conservative balance sheet management limits the downside in a stress scenario, margin headwinds remain the most significant near-term earnings risk to monitor.

The stock’s limited analyst coverage and small market cap of roughly $233 million mean that liquidity is relatively thin. Investors looking to build or exit a meaningful position may face wider bid-ask spreads and slower execution than they would experience with larger financial institutions. This illiquidity can also result in price movements that do not always reflect fundamental developments in a timely way.

Finally, while the payout ratio is low and the dividend has grown steadily, FUNC has historically been slow to raise its dividend, and that pattern could continue if management perceives any uncertainty in the operating environment. The dividend is safe by virtually any measure, but investors seeking aggressive income growth may find the pace of increases modest relative to higher-growth dividend payers elsewhere in the financial sector.

Final Thoughts

First United Corporation continues to make a quiet but convincing case for itself as a core holding for dividend-focused investors with a preference for community banking. The combination of a 2.62% yield, a payout ratio below 25%, and a dividend that has grown 30% over the past two years from the $0.20 quarterly level tells a story of a management team that is both profitable and committed to sharing that profitability with shareholders. A P/E of 9.50 and a price-to-book of 1.17 suggest the stock is not expensive relative to its earnings and asset quality, and the $44.00 analyst price target implies meaningful room for appreciation from current levels. FUNC is not a stock for investors seeking rapid dividend growth or high current yield, but for those who value consistency, capital discipline, and a growing income stream from a conservatively run regional bank, it remains a compelling and often overlooked option.