Updated 2/24/26

First Financial Corporation, trading under the ticker THFF, might not be a household name on Wall Street, but for those who appreciate consistency and steady income, it deserves a closer look. Headquartered in Terre Haute, Indiana, this regional bank has been quietly building a strong reputation over the decades. Its roots go back to the 1800s, and in that time, it has grown into a solid player in the Midwest banking space, serving communities across Indiana and Illinois.

What makes THFF particularly interesting to dividend-focused investors is its ability to stay resilient through changing market conditions. It is not a flashy business, and it does not chase headlines, but it also does not stumble when the pressure is on. That is a quality that matters, especially for investors who rely on consistent cash flow.

Recent Events

First Financial Corporation has continued its quiet but steady march forward heading into early 2026. The bank has maintained its focus on core community banking operations across Indiana and Illinois, and the broader regional banking environment has remained constructive, with interest rate dynamics generally supporting net interest margin stability for well-run institutions like THFF. The company’s conservative lending culture and disciplined cost management have kept it out of the turbulence that has periodically rattled some of its regional peers.

On the dividend front, THFF delivered a meaningful signal to income investors at the start of 2026. The January 2, 2026 dividend payment came in at $0.56 per share, up from the $0.51 per share rate that had been in place throughout 2025. That increase represents a roughly 10% step up in the quarterly payout, reinforcing management’s confidence in the bank’s ongoing earnings power and capital position. The stock has responded well to the combination of strong fundamentals and dividend momentum, trading near $64.74 and sitting not far below its 52-week high of $69.21.

With a beta of just 0.41, THFF continues to trade with considerably less volatility than the broader market, a characteristic that long-term income investors tend to appreciate. The market cap now stands at approximately $769 million, reflecting a meaningful rerating from where the stock traded in the trough of its 52-week range at $42.05.

Key Dividend Metrics

📈 Forward Yield: 3.25%

💸 Annual Dividend Rate: $2.09

📆 Last Dividend Payment: $0.56 (January 2, 2026)

🧮 Payout Ratio: 31.29%

💵 EPS (TTM): $6.68

📊 5-Year Average Yield: 2.84%

🔁 Dividend Growth Outlook: Steady with recent upward momentum

🧱 Dividend Safety: Very strong, well-covered by earnings

Dividend Overview

The dividend picture at First Financial Corporation continues to improve in a measured, sustainable way. The current annual dividend rate of $2.09 per share, combined with the stock’s price of $64.74, produces a yield of 3.25%. While that is modestly below the elevated yields seen in prior periods when the stock was trading at lower levels, it still represents an attractive income proposition given the quality of the underlying business and the extremely conservative payout ratio of just 31.29%.

That payout ratio is one of the more compelling aspects of the THFF dividend story. With EPS running at $6.68 on a trailing basis, the company is retaining a substantial portion of its earnings to fund growth, strengthen capital ratios, and preserve flexibility for future dividend increases. Even a meaningful drop in earnings would leave the dividend thoroughly covered, which is exactly the kind of cushion income investors should be looking for in a core holding.

The January 2026 dividend of $0.56 per share marked a clear step up from the $0.51 quarterly rate maintained throughout 2025, and that increase reflects management’s comfort with the bank’s profitability trajectory. Return on equity has climbed to 13.20% and return on assets sits at 1.40%, both metrics pointing to a bank generating genuine value from its capital base rather than simply managing its balance sheet defensively.

Net income for the trailing twelve months came in at $79.2 million, a figure that speaks to real and durable earnings power. With a profit margin of 31.23% on revenue of $253.6 million, this is a business that converts its top line into bottom-line results at an impressive rate, and those results are what ultimately make the dividend sustainable over the long run.

Dividend Growth and Safety

Reviewing the recent dividend history tells an instructive story about how First Financial manages its payout through varying conditions. Quarterly payments held at $0.54 in mid-2022 before an irregular special-style payment of $0.74 in early 2023. Payments then settled at $0.45 per quarter through much of 2023 and into 2024, before stepping up to $0.51 in early 2025, where they remained for the full year. The most recent payment of $0.56 in January 2026 represents the latest leg of that upward progression, and with a payout ratio still only at 31.29%, there is significant runway for further increases without putting any strain on the balance sheet.

The five-year average yield of approximately 2.84% compared to the current 3.25% yield suggests the dividend has grown faster than the stock price has appreciated over that horizon, which is a favorable dynamic for incoming shareholders. Income investors who purchase THFF at today’s levels are locking in a yield that sits meaningfully above the stock’s historical average, which implies either that the market is still catching up to the improved earnings profile or that there is genuine valuation opportunity embedded in the current price.

From a safety standpoint, the case for THFF’s dividend is straightforward. Earnings per share of $6.68 cover the $2.09 annual dividend by a factor of more than three. The bank’s return on equity of 13.20% and return on assets of 1.40% are both indicators of a well-run, efficient operation that generates consistent profits across interest rate cycles. Short interest of just 187,075 shares signals that the market is not expressing meaningful concern about the company’s near-term prospects.

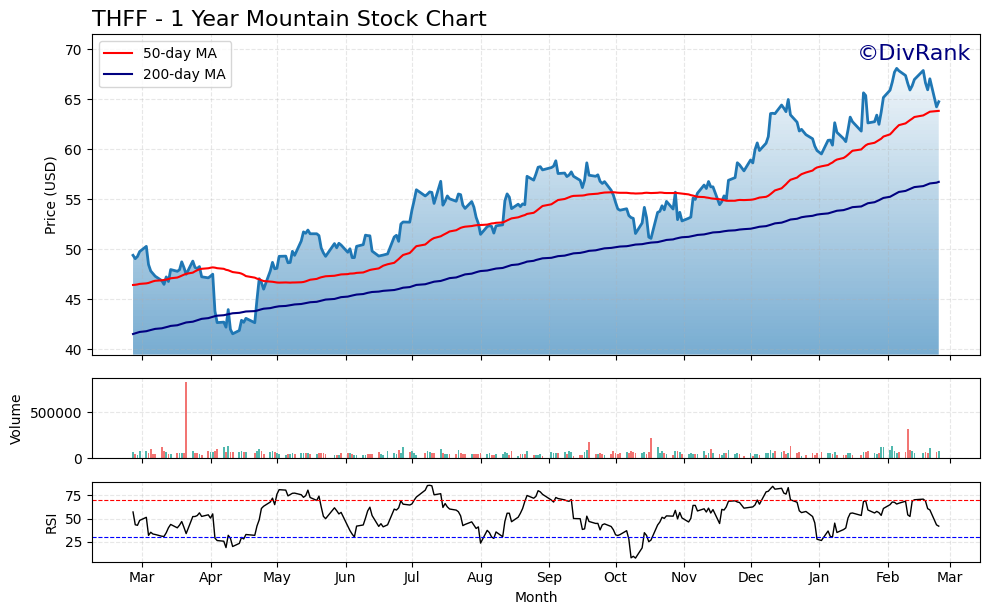

Chart Analysis

First Financial Corporation (THFF) has put together an impressive run over the past year, climbing from a 52-week low of $41.55 to its current price of $64.74, a gain of roughly 56% from the trough. That kind of price appreciation is unusual for a community bank of this size and reflects a meaningful rerating of the stock as investors have grown more comfortable with the regional banking environment following the anxiety that gripped the sector in early 2023. The stock reached a 52-week high of $68.07 before pulling back modestly, and at current levels it sits just 4.89% below that peak, suggesting the bulls have maintained firm control of the tape without allowing the chart to become dangerously extended.

The moving average picture is constructive. THFF is trading above both its 50-day moving average of $63.82 and its 200-day moving average of $56.73, and the 50-day has crossed above the 200-day in what technicians refer to as a golden cross, a configuration that historically signals strengthening intermediate-term momentum. The spread between the two averages, with the 200-day sitting nearly $7 below current price, confirms that this uptrend has been building over several months rather than representing a sudden spike. For dividend investors, a stock trading in a confirmed uptrend with both key moving averages providing support below the current price is a far more comfortable entry backdrop than one where price is stranded below a declining 200-day.

The RSI reading of 41.76 adds an interesting dimension to the setup. At that level, THFF is neither overbought nor oversold in the traditional sense, but it is leaning toward the softer end of the neutral range, which typically reflects a stock that has paused or cooled after a strong advance. Given the magnitude of the move off the 52-week low, some consolidation near current levels is entirely healthy. It also means that dividend-focused buyers are not being asked to chase a momentum-driven surge at a stretched valuation, which is exactly the kind of entry environment that tends to produce solid total return outcomes when the underlying business continues to generate reliable income.

For dividend investors, the overall technical picture reads as moderately favorable. The trend is intact, the moving average structure is bullish, and the RSI suggests the stock has room to move higher without immediately running into overbought conditions. The proximity to the 52-week high is something to monitor, as a clean breakout above $68.07 would be a further positive signal, while a failure at that level could invite a deeper retest of the 50-day moving average around $63.82. Neither scenario would fundamentally alter the income thesis, but understanding the price structure helps investors think about position sizing and whether to accumulate gradually rather than committing all at once at current levels.

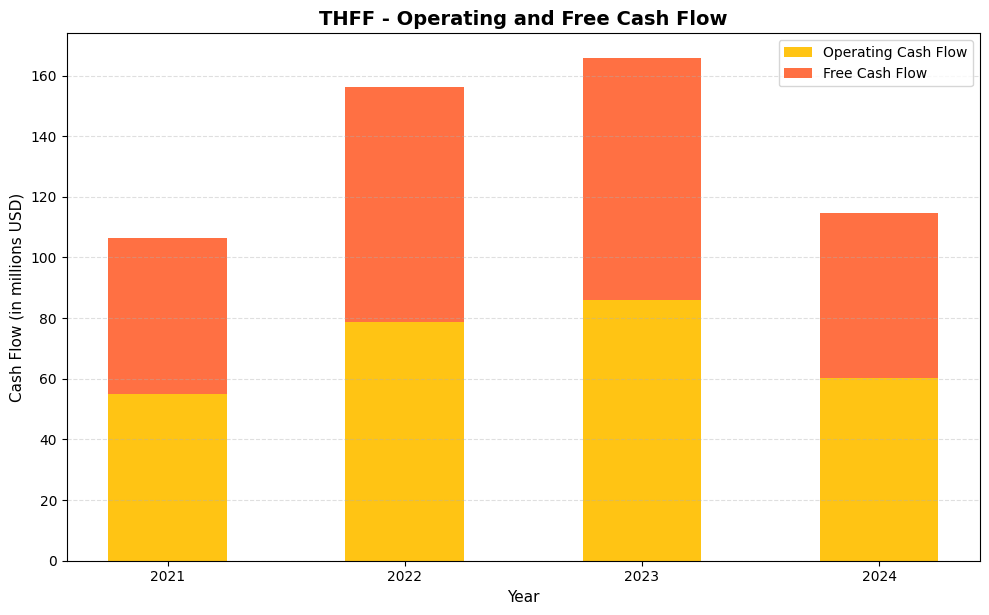

Cash Flow Statement

First Federal Savings & Loan of Lakewood (THFF) has generated consistently positive free cash flow across all four years in our data set, which provides a solid foundation for dividend sustainability. Operating cash flow climbed from $55.1 million in 2021 to a peak of $86.1 million in 2023, before pulling back to $60.4 million in 2024. Free cash flow followed a nearly identical path, rising from $51.2 million in 2021 to $79.5 million in 2023 and then moderating to $54.3 million in 2024. The tight spread between operating and free cash flow in every year reflects minimal capital expenditure requirements, which is typical for a community bank franchise and leaves the vast majority of generated cash available for dividends, buybacks, or balance sheet reinforcement.

The four-year trajectory tells a story of genuine operational improvement followed by a measured normalization, rather than any structural deterioration. The 2022 and 2023 figures were exceptionally strong, likely benefiting from the rising rate environment that expanded net interest margins across the community banking sector. The 2024 step-down to $54.3 million in free cash flow is meaningful, but it still represents a meaningful premium over 2021 levels, confirming that the business retained much of its efficiency gains. For dividend investors, the key takeaway is that THFF has consistently converted earnings into real cash with very little friction from capital spending, and even at the lower 2024 run rate, the company generates enough free cash flow to cover its dividend obligations with room to spare.

Analyst Ratings

Analyst coverage of First Financial Corporation remains limited given its size as a regional community bank, with two analysts currently covering the stock. The consensus sits at a buy rating, and the price target range of $68.00 on the low end to $75.00 on the high end implies meaningful upside from the current price of $64.74. The mean price target of $71.50 suggests analysts see approximately 10.4% price appreciation potential from current levels, which when combined with the 3.25% dividend yield, would represent a total return proposition in the mid-teens over a twelve-month horizon.

The low end target of $68.00 sits just above the current price, suggesting that even the more cautious analyst view sees some room for appreciation. The high end of $75.00 reflects confidence in the bank’s ongoing earnings momentum, improved return on equity, and the dividend growth trajectory evidenced by the step-up to $0.56 per share in January 2026. With the stock trading near $64.74 and below its 52-week high of $69.21, the analyst community broadly views the current level as offering an attractive entry point for investors with a twelve-month outlook.

Earning Report Summary

First Financial Corporation’s most recent reported financials reflect a business performing at a notably elevated level relative to its historical norms. Trailing twelve-month revenue of $253.6 million and net income of $79.2 million translate to earnings per share of $6.68, a figure that reflects both the benefit of a favorable interest rate environment for net interest margin and the bank’s continued discipline on expenses and credit quality.

Profitability at a High Level

The profit margin of 31.23% is among the stronger readings in THFF’s recent history and is well above the levels the bank posted during the lower-rate environment of the early part of this decade. Return on equity of 13.20% represents genuinely competitive performance for a community bank, and return on assets of 1.40% confirms that the profitability improvement is not simply a function of leverage but reflects genuine operational efficiency across the loan and deposit portfolio.

Valuation Context

The P/E ratio of 9.69 is modest given the earnings quality and dividend safety on offer. At a price-to-book of 1.18, the stock is trading at only a slight premium to its tangible asset base of $54.78 per share, which provides a degree of downside support that many higher-multiple names cannot offer. For income investors assessing the risk-reward at current levels, the combination of a low double-digit P/E and a below-1.2x price-to-book is reassuring.

Capital and Dividend Capacity

With $6.68 in earnings per share covering a $2.09 annual dividend, the payout ratio of 31.29% leaves First Financial with significant retained earnings to build book value, fund loan growth, and support future dividend increases. Management’s decision to raise the quarterly dividend to $0.56 in January 2026 signals confidence in sustaining this level of profitability, and the underlying numbers support that confidence. The bank appears well-positioned to continue compounding book value while delivering a growing income stream to shareholders.

Management Team

First Financial Corporation has long been led by a management team that prioritizes conservative capital allocation, credit discipline, and steady shareholder returns over headline-grabbing growth strategies. That culture has been evident in how the bank navigated the interest rate cycle of recent years, emerging with stronger margins and a cleaner loan book than many of its regional peers managed to achieve. The decision to increase the dividend to $0.56 per share beginning with the January 2026 payment reflects a management team that is paying attention to shareholder income and has the earnings capacity to back up that commitment.

The bank’s long institutional history in Terre Haute and its surrounding communities provides management with a stable core deposit base and a deep understanding of its local lending markets, advantages that do not show up easily in financial ratios but matter considerably for long-run risk management. The consistency of THFF’s operating results over time reflects an organization where the leadership team has instilled a culture of prudence, and the current financial metrics suggest that culture remains firmly in place.

Valuation and Stock Performance

At $64.74, THFF is trading near the upper end of its 52-week range of $42.05 to $69.21, a reflection of the significant rerating the stock has experienced as investors have recognized the bank’s improved earnings profile. The move from the 52-week low represents appreciation of more than 50%, which is a substantial run for a low-beta community bank. The question for prospective investors is whether current levels still offer value, and by most measures, the answer is yes.

A P/E of 9.69 on trailing earnings of $6.68 per share is undemanding for a bank generating a 13.20% return on equity with a dividend that is growing and only consuming 31% of earnings. The price-to-book of 1.18 against a book value of $54.78 provides a tangible anchor to valuation that limits downside in adverse scenarios. The mean analyst price target of $71.50 implies roughly 10% upside from the current price, and the 3.25% dividend yield adds meaningfully to the total return equation without requiring any price appreciation to justify ownership.

With a beta of 0.41, THFF is likely to continue trading with considerably less volatility than the broader market, which is both a feature and a constraint. Investors seeking dramatic short-term price moves will look elsewhere, but those building a portfolio around reliable income and capital preservation will find the low-volatility profile appealing. The stock’s market cap of approximately $769 million keeps it in the small-to-mid cap regional bank category, which can limit institutional attention but also means the valuation has not been bid up to levels that would compress the income opportunity.

Risks and Considerations

The most immediate risk for THFF shareholders is the potential for interest rate headwinds. The bank’s strong net interest margin performance over recent periods has been supported by a higher-rate environment, and any meaningful decline in rates could compress margins and reduce earnings, potentially slowing the dividend growth trajectory. Community banks with concentrated deposit franchises can also be sensitive to local economic conditions, and THFF’s geographic focus on Indiana and Illinois means the bank’s credit quality is meaningfully tied to the economic health of the Midwest.

Credit quality is another area to monitor. While current metrics appear healthy based on recent reporting trends, any deterioration in the commercial or consumer loan portfolio would flow directly through to earnings and could pressure the payout ratio upward. The bank’s conservative underwriting culture provides some protection, but no lender is fully insulated from a broad economic slowdown.

Liquidity and trading volume present a practical consideration for larger investors. With a market cap of approximately $769 million and only two analyst contributors to the consensus estimate, THFF operates with limited sell-side coverage and relatively thin trading volume compared to larger regional banks. This can create wider bid-ask spreads and make it harder to build or exit a meaningful position without impacting the price.

Finally, the stock’s strong run from its 52-week low to near its highs means some near-term consolidation is possible, particularly if earnings in upcoming quarters show any moderation from recent elevated levels. Investors entering near current prices should be comfortable with the possibility that the stock’s next move could be sideways or modestly lower before the next leg of appreciation materializes.

Final Thoughts

First Financial Corporation presents a genuinely compelling case for dividend growth investors who value earnings quality, balance sheet conservatism, and a management team that has demonstrated its willingness to reward shareholders. The January 2026 dividend increase to $0.56 per quarter, representing approximately a 10% step-up from the prior rate, is a concrete signal that the bank’s improved profitability is being translated into growing income for shareholders. With a payout ratio of just 31.29%, EPS of $6.68, and a return on equity of 13.20%, the dividend is among the better-covered in the regional banking sector. The current yield of 3.25% at a P/E under 10 and a price-to-book just above 1.1x makes THFF an attractively priced holding for long-term income portfolios, and the analyst consensus pointing to a mean price target of $71.50 suggests the market may not yet be fully reflecting the bank’s current earning power.