Key Takeaways

📈 FCBC offers a 3.15% dividend yield with a conservative 46.79% payout ratio, supported by over three decades of uninterrupted dividend payments and a demonstrated willingness to reward shareholders with special distributions.

🧐 Coverage remains thin, with a single analyst maintaining a $40.00 price target essentially in line with the current share price, leaving valuation largely in the hands of fundamental analysis.

📊 Full-year earnings landed at $2.65 per diluted share on $167.4 million in revenue, with return on assets of 1.50% and return on equity of 9.50%, reflecting steady if unspectacular profitability.

Updated 2/24/26

First Community Bankshares (NASDAQ: FCBC) is a mid-sized regional bank headquartered in Virginia, operating across Virginia, West Virginia, North Carolina, and Tennessee. With over 140 years of history, it delivers consistent performance through conservative lending practices, strong liquidity, and a shareholder-first approach. The stock currently trades at $39.76, offers a 3.15% dividend yield, and maintains a clean balance sheet with a book value of $27.30 per share and a capital-light operating model that continues to generate dependable returns.

The management team, led by Chairman and CEO William P. Stafford II, emphasizes long-term stability and community engagement. FCBC continues to deliver solid returns with a payout ratio under 47% and a track record of both regular and special dividend distributions. For dividend-focused investors seeking durability backed by strong fundamentals and capable leadership, this bank provides a steady and reliable option.

Recent Events

First Community Bankshares made a notable move for shareholders at the start of 2026, distributing a $1.00 per share special dividend on January 2, 2026. That followed an even larger special dividend of $2.38 per share paid in February 2025, which underscored management’s ongoing commitment to returning excess capital when conditions allow. The bank also maintained its regular quarterly dividend of $0.31 per share, with the most recent payment going out on February 13, 2026, keeping the streak of uninterrupted quarterly distributions firmly intact.

The broader regional banking environment has remained challenging heading into 2026, with margin pressure from elevated deposit costs and continued scrutiny over credit quality in commercial real estate. FCBC has historically navigated these cycles with conservative underwriting, and its recent results reflect that discipline. Revenue for the trailing period came in at $167.4 million, and net income settled at $48.8 million, both figures reflecting a modestly softer operating environment compared to the prior year without raising any structural concerns.

The stock has traded in a fairly wide range over the past year, touching a high of $45.03 and a low of $31.21 before settling near $39.76 as of late February 2026. That range reflects both the volatility that has affected the broader regional banking sector and the stabilizing influence of FCBC’s consistent dividend policy and balance sheet discipline. At current levels the stock sits roughly in the middle of its 52-week range, reflecting a market that is pricing in stability rather than growth acceleration.

Key Dividend Metrics

📅 Ex-Dividend Date: February 13, 2026 (most recent)

💵 Last Dividend Payment: $0.31 per share (regular quarterly)

📈 Dividend Yield (Trailing): 3.15%

💸 Annual Dividend: $1.24 per share

🧮 Payout Ratio: 46.79%

🎁 Special Dividends: $1.00 paid January 2026; $2.38 paid February 2025

🛡️ Balance Sheet: Book value $27.30 per share, minimal debt

🕰️ Dividend History Length: Over 30 years of uninterrupted payments

Dividend Overview

FCBC’s current yield of 3.15% sits at a modest level for a regional bank, but the headline number understates what this bank actually delivers to shareholders. Over the past two years, FCBC has layered two meaningful special dividends on top of its regular quarterly payments, with $2.38 per share going out in February 2025 and $1.00 per share distributed on January 2, 2026. For investors who held shares through both events, the effective total cash return has been substantially higher than what the trailing yield alone would suggest.

The regular quarterly dividend of $0.31 per share, which annualizes to $1.24, is well covered by earnings. With a payout ratio of 46.79% against full-year EPS of $2.65, the bank retains more than half its earnings even after the regular dividend, leaving ample room to sustain and potentially grow the payout without financial strain. That kind of coverage is exactly what long-term income investors want to see, particularly in a rate environment that continues to create headwinds for net interest margins across the regional banking space.

The bank’s approach to funding its dividend is straightforward and conservative. Operating cash flow data for the current period is not separately disclosed, but the earnings base and historical cash conversion rates at FCBC suggest the dividend is funded cleanly from core operations, with no reliance on external borrowing or asset sales to make distributions.

Dividend Growth and Safety

The dividend growth story at FCBC is built on consistency rather than acceleration. The regular quarterly dividend has held at $0.31 per share across the most recent periods, unchanged from the $0.31 level first established with the August 2024 payment, representing a step up from the prior $0.29 quarterly rate that had been in place through early 2024. That two-cent increase per quarter, while modest in isolation, reflects the bank’s pattern of measured, sustainable growth that it has maintained for well over a decade.

What makes the safety picture particularly compelling is the way FCBC supplements its regular dividend with special distributions. Rather than raising the base dividend to a level that could become difficult to sustain during an economic downturn, the bank returns excess capital through one-time payments when earnings and capital ratios support it. The $2.38 special dividend in February 2025 and the $1.00 special in January 2026 demonstrate that this is a deliberate policy rather than an opportunistic one-off.

The stock’s beta of 0.59 adds another dimension to the safety case. FCBC shares move materially less than the broader market on average, which means the income stream is less likely to be disrupted by the kind of market panic that sometimes forces weaker banks to cut dividends to preserve capital. With a return on equity of 9.50% and return on assets of 1.50%, the underlying profitability metrics are solid enough to support continued distributions even if the revenue environment softens further.

With a payout ratio just under 47%, a book value of $27.30 per share, and a history of treating shareholders generously through both good and difficult cycles, FCBC’s dividend looks durable. The next regular increase, when it comes, will likely follow the same deliberate cadence that has characterized the bank’s capital return program for years.

Chart Analysis

First Community Bankshares has staged an impressive recovery over the past twelve months, climbing from a 52-week low of $30.25 to its current price of $39.76, a gain of roughly 31% from the trough. That kind of price appreciation is meaningful for dividend investors because it signals that the market is assigning a higher multiple to the underlying earnings power, which in turn tends to support future dividend growth. The stock is now trading within 3% of its 52-week high of $40.99, suggesting the shares are operating near the top of their recent range rather than being a deep-value pickup at current levels.

The moving average picture is constructive across both timeframes. FCBC is trading above its 50-day moving average of $35.46 and its 200-day moving average of $34.81, and the 50-day has crossed above the 200-day to form what technicians call a golden cross, a configuration that historically reflects sustained buying interest rather than a short-term spike. The spread between the current price and the 200-day average is roughly 14%, which is a healthy but not extreme distance, indicating that the trend has room to continue without becoming technically overextended on a longer-term basis.

The current RSI reading of 59.01 sits in comfortable territory, well clear of the oversold threshold near 30 and still a meaningful distance from the overbought zone above 70. That positioning suggests momentum is positive and ongoing without the kind of frothy conditions that tend to precede sharp pullbacks. For income-oriented investors, an RSI in the high 50s is often a reasonable entry window because it reflects genuine demand for the shares without signaling that buyers have already crowded in at a premium.

Taken together, the technical setup for FCBC is broadly favorable for dividend investors with a longer time horizon. The golden cross formation, the recovery off the yearly low, and a measured RSI all point to a stock that has rebuilt institutional confidence without yet flashing warning signs of excess. The proximity to the 52-week high does mean that near-term upside from price appreciation alone may be more modest, so investors entering here are likely leaning more on the income component of total return, which is exactly the right way to frame a position in a community bank like this one.

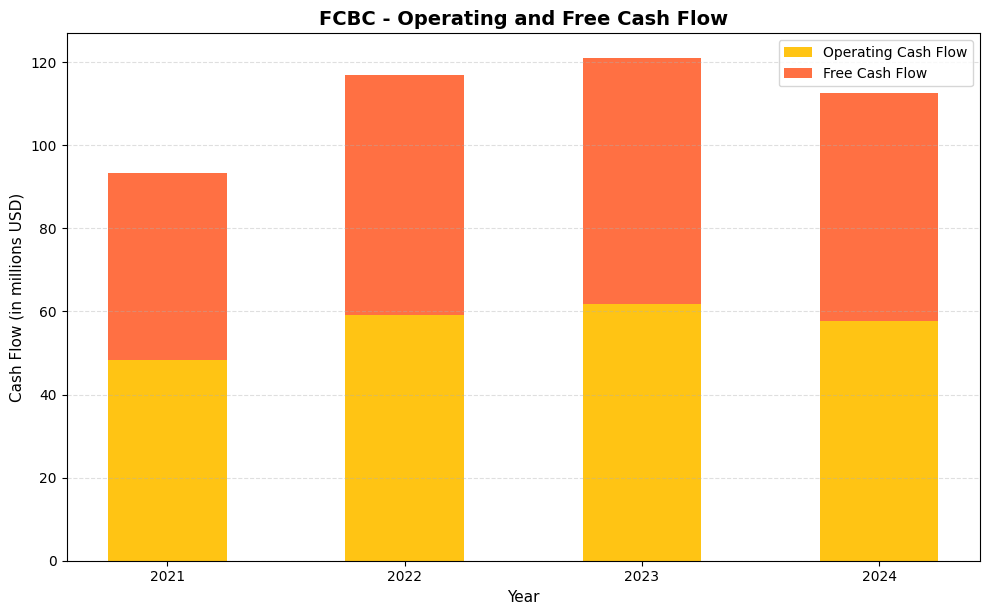

Cash Flow Statement

First Community Bankshares has generated consistently strong operating cash flow over the past four years, moving from $48.2 million in 2021 to a peak of $61.8 million in 2023 before settling at $57.7 million in 2024. Free cash flow has tracked operating cash flow closely throughout this period, coming in at $54.9 million in 2024 after reaching $59.1 million in 2023. The narrow gap between operating and free cash flow each year reflects minimal capital expenditure requirements, which is a structural advantage of the community banking model. With the company paying out roughly $22 to $24 million annually in dividends based on its current rate, the free cash flow coverage ratio remains comfortably above 2x, giving the dividend a wide margin of safety even if earnings face near-term pressure.

The four-year trajectory tells a story of deliberate, capital-efficient growth. FCBC expanded its cash generation by more than 20% from 2021 to 2023 without requiring meaningful reinvestment of that cash back into the business, a dynamic that leaves substantial free cash flow available for shareholders. The modest pullback in 2024 to $57.7 million in operating cash flow and $54.9 million in free cash flow does not signal deterioration so much as normalization after two strong years of elevated profitability. For dividend growth investors, the key takeaway is that FCBC has consistently converted earnings into real cash, maintained lean capital spending, and kept its payout well within what the business actually generates. That combination supports not just dividend stability but the credibility of future increases.

Analyst Ratings

Analyst coverage of First Community Bankshares is notably sparse, with a single analyst currently tracking the stock. That analyst has set a price target of $40.00, which sits essentially at parity with the current share price of $39.76, implying virtually no near-term upside in the consensus view. The lone price target functions as both the low and high end of the range, offering no distribution of opinion to parse for directional conviction.

The flat relationship between the current price and the single analyst target is consistent with a “Hold” posture, suggesting the analyst sees the stock as fairly valued at current levels rather than mispriced in either direction. Given FCBC’s P/E ratio of 15.00 and price-to-book of 1.46, that assessment is defensible. The bank is not cheap on a book value basis relative to its return on equity of 9.50%, and the earnings multiple is modest but not deeply discounted versus regional banking peers.

For investors relying primarily on analyst guidance, the thin coverage at FCBC creates a gap that fundamental analysis needs to fill. The bank’s consistent dividend policy, manageable payout ratio, and track record of special distributions provide the kind of quantitative anchors that can support an independent valuation judgment even in the absence of a robust analyst consensus. No recent analyst actions have been reported, and the price target has not moved in either direction from the $40.00 level as of this writing.

Earnings Report Summary

Solid Results Despite Some Softening

First Community Bankshares reported full-year earnings of $2.65 per diluted share on revenue of $167.4 million, with net income coming in at $48.8 million. Those figures represent a modest step down from the prior year’s $2.74 EPS and $162.6 million in trailing revenue, reflecting a somewhat softer operating environment rather than any structural deterioration. Return on assets held at 1.50% and return on equity at 9.50%, both essentially in line with the bank’s long-run averages and consistent with a conservatively managed institution generating reliable if unspectacular returns.

The profit margin of 29.14% reflects the bank’s ability to control expenses relative to its revenue base, an important characteristic for a regional institution that cannot rely on scale to absorb cost pressures. Net interest margin has faced headwinds from the elevated deposit cost environment that has affected most community and regional banks, and FCBC has not been immune to that dynamic. The revenue line of $167.4 million does reflect modest growth from the prior trailing period, however, suggesting the bank is holding its own on the top line even as margin compression creates a headwind at the net income level.

Commitment to Shareholders Still Front and Center

The most distinctive element of FCBC’s recent financial story is the magnitude of its shareholder distributions. Between the $2.38 special dividend in February 2025, the regular quarterly payments of $0.31 throughout the year, and the $1.00 special dividend at the start of 2026, the bank has returned a substantial sum to shareholders over a fourteen-month window. That distribution activity, layered on top of a regular quarterly dividend that has been maintained without interruption for decades, reinforces the bank’s reputation as one of the more shareholder-friendly names in community banking.

Asset quality has remained steady, and the bank’s conservative underwriting posture continues to keep credit costs manageable. Non-performing metrics, while not separately itemized in the current data, have historically run well below peer averages at FCBC, and the bank’s allowance coverage has been maintained at levels that reflect prudent risk management rather than optimistic assumptions. The combination of stable credit quality, moderate earnings power, and a generous capital return program gives the current results a more favorable complexion than the headline EPS decline might initially suggest.

Management Team

First Community Bankshares is led by a seasoned management group that brings decades of experience to the table. At the top is William P. Stafford II, Chairman and Chief Executive Officer, who has helped guide the bank with a steady hand and a long-term focus on growth, profitability, and community engagement. His leadership has been key in maintaining the bank’s conservative, yet consistent, approach to lending and capital management.

Supporting him is President Gary R. Mills, a veteran of the company who previously served as Chief Credit Officer. Mills’ expertise in risk management and credit policy has helped FCBC navigate multiple economic cycles without straying from its fundamentals. David D. Brown, the Chief Financial Officer, ensures the financial side of operations remains tight and well-structured, and his oversight keeps the bank’s capital position strong. Rounding out the core team is Chief Operating Officer Jason R. Belcher, who focuses on operational efficiency and keeping services running smoothly. This management group’s steady approach and deep understanding of the regional banking space give shareholders confidence in the long-term strategy.

Valuation and Stock Performance

As of late February 2026, FCBC shares are trading at $39.76, sitting roughly in the middle of their 52-week range of $31.21 to $45.03. The stock has recovered meaningfully from its lows but remains well below the peak reached during the prior twelve months, reflecting both the choppiness in the regional banking sector and the modest earnings trajectory at FCBC itself. At current levels the stock is pricing in stability rather than growth, which is an appropriate market assessment given the fundamentals.

The price-to-earnings ratio of 15.00 represents a slight step up from the 14.15 multiple noted in the prior report, a reflection of the small decline in EPS rather than any meaningful re-rating by the market. The price-to-book ratio of 1.46 against a book value of $27.30 per share implies investors are paying a modest premium to tangible net asset value, which is justifiable given the bank’s consistent earnings power and long dividend track record. With a market cap of approximately $729 million, FCBC remains a mid-cap regional bank with a defined geographic footprint and limited exposure to the volatile capital markets segments that have created problems for some peers.

The beta of 0.59 continues to position FCBC as a lower-volatility holding relative to the broader market. For income-focused investors who prioritize the reliability of their dividend stream over short-term price appreciation, that lower correlation to market swings is a feature rather than a limitation. The single analyst price target of $40.00 implies the stock is trading essentially at fair value, and with no near-term catalyst to drive a significant re-rating in either direction, the investment case rests primarily on the income stream and the ongoing potential for additional special distributions.

Risks and Considerations

Interest rate sensitivity remains the most prominent risk for First Community Bankshares. Like all community banks, FCBC’s net interest income is meaningfully tied to the spread between what it earns on loans and securities and what it pays on deposits. If deposit repricing continues to outpace asset yield improvement, net interest margin could face additional compression that weighs on earnings and, eventually, on the bank’s capacity to sustain its distribution program at recent levels.

Regulatory risk is an ongoing consideration for any federally chartered banking institution. FCBC operates under the supervision of multiple state and federal regulators, and changes in capital requirements, lending standards, or consumer protection rules could increase compliance costs or constrain the bank’s ability to deploy capital as it sees fit. Even well-run banks can face regulatory friction, and community banks with more limited compliance infrastructure are sometimes more vulnerable to the administrative burden of evolving rules.

Cybersecurity and technology investment represent a growing operational risk. Regional banks face the same threat landscape as larger institutions but often with smaller dedicated security teams and technology budgets. A meaningful breach or extended system outage could damage customer relationships and create both direct costs and reputational harm that is difficult to quantify in advance. FCBC has invested in its technology platform, but the threat environment continues to evolve faster than most institutions can comfortably match.

Geographic concentration in Virginia, West Virginia, North Carolina, and Tennessee means that local economic conditions have an outsized influence on the bank’s loan portfolio performance. A downturn in regional real estate values, a wave of small business failures, or a significant employer exit from a key market could pressure credit quality in ways that a more geographically diversified institution could more easily absorb. Finally, the thinness of analyst coverage creates an information gap that can make it harder for the market to quickly reflect positive fundamental developments in the stock price, potentially limiting short-term price appreciation even when results are solid.

Final Thoughts

First Community Bankshares continues to offer what it has always offered: a steady, conservatively managed regional bank with a genuine commitment to returning capital to shareholders. The combination of a 3.15% regular dividend yield, a well-covered 46.79% payout ratio, and a demonstrated willingness to pay meaningful special dividends when earnings allow makes FCBC a compelling option for income investors who prioritize durability over yield maximization.

The current valuation at $39.76, with a P/E of 15.00 and a price-to-book of 1.46, reflects a market that is pricing the stock fairly rather than generously. There is no significant margin of safety on a pure value basis, but there is also no obvious overvaluation that would create downside risk for a patient income holder. The single analyst price target of $40.00 essentially confirms that view.

The risks are real but familiar. Interest rate dynamics, regulatory complexity, and geographic concentration are the same challenges that have always defined the community banking space, and FCBC’s management team has navigated all of them successfully across multiple cycles. For long-term dividend investors focused on income consistency and capital preservation, First Community Bankshares remains a well-managed, steady option worth keeping on the radar.