Key Takeaways

💸 EQIX offers a forward dividend yield of 1.98% with a decade-long streak of annual increases and a consistent track record of dividend growth near 10% annually.

💰 Operating cash flow reached $3.91 billion over the trailing twelve months, with free cash flow expanding to $2.83 billion, reflecting improved capital efficiency across the business.

📊 Analysts maintain a positive outlook with an average price target of $1,019.42, suggesting meaningful upside from current levels, with 26 analysts covering the stock at a consensus buy rating.

📈 Full-year revenue reached $9.26 billion with net income of $1.35 billion, and the company raised its quarterly dividend to $4.69 per share, marking a continued trajectory of shareholder returns.

Updated 2/25/26

Equinix (EQIX) operates one of the largest global networks of interconnected data centers, supporting a wide range of digital infrastructure needs for enterprise, cloud, and network customers. With over 250 data centers worldwide and strong recurring revenue, it has become a core utility for the digital economy. Its financial profile is marked by consistent cash flow, healthy margins, and a long track record of disciplined capital allocation.

The company also offers a growing dividend, supported by strong free cash flow and a decade of uninterrupted increases. Its leadership team continues to balance expansion with financial stability, while investor confidence remains high with nearly all shares held by institutions. Between its rising AFFO, expanding global footprint, and long-term contracts, Equinix offers a compelling mix of stability and growth.

Recent Events

Equinix has remained active on the operational and strategic front heading into early 2026. The company has continued its global data center expansion program, advancing new builds in key markets across Europe, Asia-Pacific, and the Americas as demand for AI-ready infrastructure and enterprise interconnection accelerates. These developments reflect a broader industry shift in which colocation providers are becoming essential partners for hyperscalers and enterprises managing hybrid cloud environments at scale.

The company also confirmed its latest quarterly dividend of $4.69 per share, representing a 10.1% increase from the $4.26 per share paid throughout most of 2024. That step up marks another year of consecutive dividend growth since Equinix converted to a REIT structure in 2015, reinforcing its commitment to returning capital to shareholders even while investing heavily in capacity expansion.

Institutional support remains firmly in place. The overwhelming majority of shares continue to be held by professional asset managers and pension funds, a dynamic that has historically provided a stabilizing floor for the stock during periods of broader market volatility. With beta sitting at 1.07, Equinix trades in close alignment with the market, making it a reasonably predictable name for income-oriented investors seeking growth exposure.

The stock has staged a meaningful recovery from its 52-week low of $701.41, with shares now trading at $951.90, not far from the 52-week high of $992.90. That recovery reflects growing conviction around Equinix’s positioning in the AI infrastructure buildout and its ability to generate durable free cash flow through long-term customer contracts.

Key Dividend Metrics

💸 Forward Dividend Yield: 1.98%

📈 Annual Dividend Rate: $19.23

💰 Last Quarterly Dividend: $4.69

🧾 Payout Ratio: 136.34%

📅 Recent Dividend History: $4.69 per quarter throughout 2025

📊 Dividend Growth (Year-over-Year): ~10.1%

Dividend Overview

Equinix might not dazzle you with a sky-high yield. At just under 2%, it sits on the lower end of what income investors typically seek. But what it lacks in yield, it makes up for in reliability and upward momentum.

The payout ratio of 136.34%, while elevated on the surface, requires context. For REITs, earnings-based payout ratios frequently overstate the true dividend burden because of how depreciation flows through net income. What matters far more is whether operating and free cash flow can comfortably support the distribution, and at $3.91 billion in operating cash flow against an annual dividend commitment well below that threshold, Equinix clears that bar with room to spare.

Thanks to its deeply embedded customer base, long-term contracts, and global scale, cash flow is remarkably steady. Add to that its data-centric model, which benefits from secular growth in cloud, AI, and enterprise connectivity, and you have a dividend that is well anchored and well positioned to continue growing.

Dividend Growth and Safety

Since converting to a REIT in 2015, Equinix has raised its dividend every single year without exception. The most recent increase, from $4.26 per share quarterly to $4.69, represents a year-over-year gain of approximately 10.1%, a step up from the prior growth rate of around 8% and a sign that management’s confidence in the cash flow outlook is strengthening rather than softening.

This is the kind of pace that transforms a modest starting yield into a genuinely compelling income stream over time. Investors who have held EQIX for several years have seen their effective yield on cost climb substantially, thanks to this consistent cadence of increases. The compounding effect of dividend growth at this rate over a decade is difficult to replicate in most income investments.

The safety profile reflects a business that generates far more cash than it needs to sustain its distribution. Operating cash flow of $3.91 billion and free cash flow of $2.83 billion provide a wide cushion relative to annual dividend obligations. The company does carry a meaningful debt load, which is typical for capital-intensive infrastructure REITs, but it has consistently managed that debt responsibly through disciplined refinancing and strong earnings before interest, taxes, depreciation, and amortization.

The business model is structurally sticky. Once customers are interconnected within Equinix’s global fabric, the cost and complexity of migrating workloads to another provider is substantial. That creates a predictable, recurring revenue base that few REITs can match, and it is the foundation on which dividend safety ultimately rests. In an environment where many dividend payers have been cautious about raising distributions, Equinix is moving confidently in the other direction.

Chart Analysis

Equinix has staged an impressive recovery over the past year, climbing roughly 31% off its 52-week low of $726.09 to trade at $951.90, just a fraction below its 52-week high of $957.87. That kind of price trajectory signals a sustained shift in institutional sentiment, not a short-term bounce. The stock has essentially reclaimed the entire range it surrendered during the broader REIT selloff, and the proximity to a fresh 52-week high suggests buyers have been consistently willing to step in at higher prices rather than fade the rally.

The moving average picture reinforces the bullish case. The 50-day moving average sits at $814.30 and the 200-day moving average at $803.40, both comfortably below the current price, meaning EQIX is trading roughly 17% above each of those trend lines. Importantly, the 50-day has crossed above the 200-day, forming what technicians refer to as a golden cross. This configuration typically reflects a durable shift in trend direction rather than a temporary spike, and for dividend investors it often signals the kind of price stability that allows income-focused positions to compound without the distraction of steep drawdowns.

The one area deserving attention is momentum. The current RSI reading of 82.38 places EQIX firmly in overbought territory, well above the conventional 70-level threshold. Readings at this level do not automatically predict a reversal, but they do indicate that a significant amount of near-term optimism is already priced into the stock. Investors looking to establish or add to a position may find better entry points if they exercise patience, as short-term consolidation or a modest pullback toward the $900 area would not be unusual or unhealthy given the magnitude of the run.

For dividend-focused investors, the overall technical setup is constructive. The golden cross, the distance from the 52-week low, and the proximity to all-time highs all point to a stock in a well-established uptrend. The elevated RSI is the primary caution flag, suggesting that the risk-to-reward ratio for new capital is somewhat less favorable right now than it would be after even a minor consolidation. Long-term holders who already own EQIX for its data center growth story and dividend progression have little reason for concern in the current chart structure.

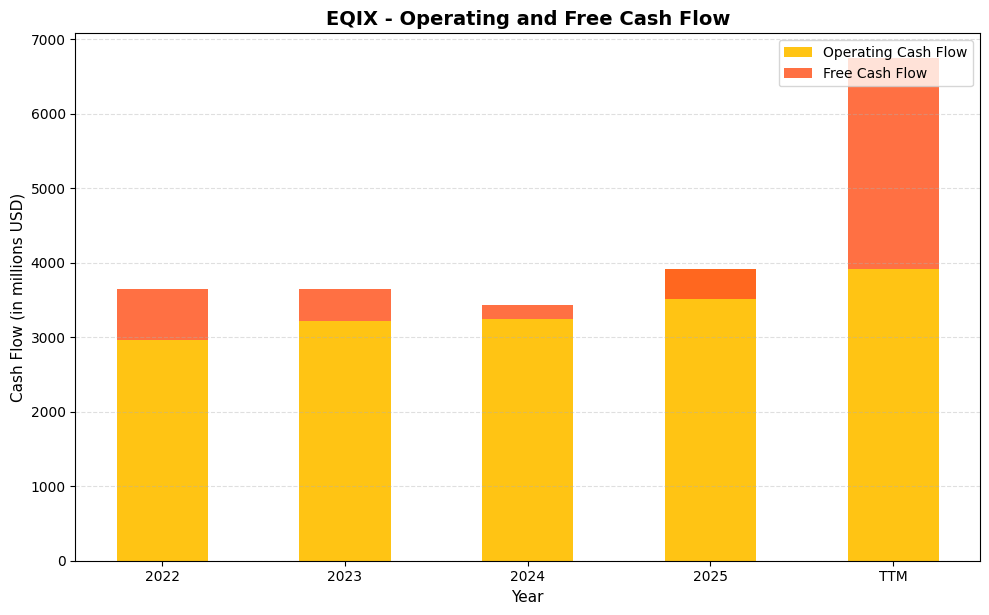

Cash Flow Statement

Equinix generated $3,911.0 million in operating cash flow over the trailing twelve months, continuing a steady upward trajectory that began at $2,963.0 million in 2022 and climbed through $3,217.0 million in 2023 and $3,249.0 million in 2024. That operating cash flow progression is genuinely strong and speaks to the durability of the company’s colocation and interconnection model, where long-term customer contracts and high switching costs translate into predictable, recurring revenue. Free cash flow tells a more complicated story, however. After sitting at $685.0 million in 2022, it compressed to $436.0 million in 2023 and further to $183.0 million in 2024 before turning negative at $400.0 million in 2025, reflecting the massive capital expenditure program Equinix has been executing across its global expansion. The TTM free cash flow of $2,833.3 million appears to reflect a normalization or one-time shift in capex timing rather than a structural improvement, and investors should watch subsequent quarters to confirm whether that figure represents a sustainable run rate. For dividend sustainability purposes, Equinix funds its distribution primarily through AFFO rather than traditional free cash flow, and operating cash flow at nearly $3.9 billion provides a solid foundation for that calculation.

Zooming out across the full data set, the pattern here is that of a REIT in aggressive growth mode, deliberately sacrificing near-term free cash flow to build out capacity that should generate returns for years to come. Capital efficiency, measured simply by how much free cash flow the business retains per dollar of operating cash flow, deteriorated materially from 2022 through 2025 as the denominator grew modestly while the numerator shrank and eventually went negative. For dividend investors, this is a trade-off that requires patience and conviction in the long-term asset value being created. The xScale joint venture strategy, where Equinix co-develops hyperscale data center capacity with deep-pocketed partners, is designed in part to recycle capital and reduce the strain of funding expansion entirely on balance sheet. Shareholders who can evaluate Equinix on AFFO per share growth and data center demand fundamentals rather than traditional free cash flow screens will find the underlying cash generation picture considerably more reassuring than the free cash flow line alone would suggest.

Analyst Ratings

The analyst community remains broadly constructive on Equinix heading into early 2026. Across 26 analysts covering the stock, the consensus sits at buy, with an average price target of $1,019.42 that implies roughly 7% upside from the current price of $951.90. The range of targets is wide, spanning from a low of $870 to a high of $1,200, reflecting a mix of near-term caution around capital expenditure cycles and longer-term optimism about Equinix’s position in the AI and cloud infrastructure buildout.

The $1,200 high-end target reflects the most bullish view on the street, likely anchored to scenarios where AI-driven demand for interconnection and colocation accelerates beyond current expectations and margin expansion follows from operating leverage. The $870 low-end target, sitting below current levels, likely captures concerns about rising capital costs, currency headwinds from the company’s global footprint, or valuation compression in the broader REIT sector.

The mean target of $1,019.42 is meaningful in that it sits near the 52-week high of $992.90, suggesting analysts view a move toward recent highs as achievable without requiring an exceptional macro backdrop. With the stock recovering from its 52-week low of $701.41 and now trading near $951.90, the market appears to be converging toward the analyst consensus, with the primary question being whether execution on the company’s expansion pipeline can sustain the current pace of cash flow growth.

Earning Report Summary

A Strong Full-Year Performance

Equinix closed out the fiscal year with full-year revenue of $9.26 billion, reflecting continued expansion in digital infrastructure demand across all major regions. The Americas remained a core driver of growth, with enterprise and cloud customers continuing to deepen their reliance on Equinix’s interconnection platform. Net income for the year came in at $1.35 billion, a solid result that reflects both top-line growth and ongoing margin discipline.

Earnings per share reached $13.80 for the full year, while operating cash flow of $3.91 billion and free cash flow of $2.83 billion underscore the company’s ability to convert revenue into durable liquidity. The profit margin of 14.58% and return on equity of 9.72% reflect a business that is generating real returns on its substantial asset base, even as it continues to invest heavily in new capacity.

Leadership Perspective and Future Outlook

CEO Adaire Fox-Martin has consistently emphasized the company’s alignment with long-term digital trends, particularly the accelerating demand for AI-ready infrastructure, sovereign cloud solutions, and enterprise interconnection at scale. Her commentary has highlighted improving sales conversion rates and a growing pipeline of opportunities in markets where Equinix is expanding capacity.

The leadership team’s capital allocation philosophy remains focused on funding organic expansion through a combination of operating cash flow and disciplined use of capital markets, while maintaining the dividend growth trajectory that has been a hallmark of the REIT since 2015. With free cash flow now at $2.83 billion, management has meaningfully more flexibility than in prior years to balance reinvestment with shareholder returns.

Dividends and Capital Investment

Equinix declared a quarterly dividend of $4.69 per share throughout 2025, representing a 10.1% increase over the $4.26 quarterly rate that was in place for much of 2024. This continues a decade-long trend of annual dividend increases since the company’s conversion to REIT status. Capital investment remains elevated as Equinix builds out new data center capacity in strategic markets, positioning the company to capture demand from customers at the intersection of cloud, AI, and digital transformation. The combination of rising dividends and a strengthening free cash flow profile is a constructive setup for income investors with a long-term horizon.

Management Team

Equinix’s management team has a reputation for consistency and long-term vision. Leading the way is Adaire Fox-Martin, who has brought a deep background in enterprise technology and a clear focus on customer engagement and global expansion to the CEO role. Her leadership reflects a strategic continuation of Equinix’s core focus on interconnection and infrastructure growth, with added emphasis on operational excellence and navigating the rapidly evolving landscape of AI infrastructure demand.

Keith Taylor, the longtime CFO, continues to be a steady presence. He is known for his disciplined financial stewardship, particularly in navigating Equinix through major capital investment cycles while maintaining strong cash flow generation. His approach has balanced growth with profitability, ensuring that the company remains well-capitalized even during expansion-heavy years, a quality that has become increasingly valued as interest rates have remained elevated longer than many anticipated.

The broader executive team combines infrastructure expertise with global market insight, spanning from engineering to commercial strategy. They have proven their ability to adapt Equinix’s model to different regional dynamics while maintaining the high standards and uptime requirements demanded by their customers. As the company grows deeper into markets like AI infrastructure, edge computing, and sovereign cloud, the current team’s experience will likely remain a critical competitive asset.

Valuation and Stock Performance

Equinix stock has staged a meaningful recovery over the past year, climbing from a 52-week low of $701.41 to a current price of $951.90, just below the 52-week high of $992.90. That recovery represents a gain of approximately 36% from the trough, reflecting growing market conviction around the company’s positioning in the AI infrastructure buildout and the improving free cash flow trajectory.

From a valuation standpoint, EQIX does not come cheap, nor should it. The price-to-earnings ratio of 68.98 is well above the average for the REIT sector, but it reflects the company’s unique positioning as a digital infrastructure platform with consistent growth, pricing power, and strong recurring revenue. Price-to-book stands at 6.61 against a book value per share of $144.12, a premium that the market is willing to pay for Equinix’s ability to generate returns far above the value of its physical assets alone.

The market cap of approximately $93.5 billion places Equinix among the largest REITs in the world, and the average analyst price target of $1,019.42 suggests the stock has room to approach and potentially exceed its 52-week high if the company continues executing on its expansion pipeline. With beta at 1.07, the stock moves roughly in line with the broader market, offering growth-oriented income investors a balance of upside participation and relative stability compared to more volatile sectors.

Risks and Considerations

Equinix operates in a capital-intensive space where expansion, maintenance, and modernization of data centers require significant ongoing investment. While the company has demonstrated its ability to manage these expenses effectively, and free cash flow has improved substantially, elevated borrowing costs could still weigh on future funding flexibility if the interest rate environment shifts unfavorably during refinancing cycles.

The competitive landscape deserves attention as well. While Equinix has carved out a dominant global position, hyperscalers like Amazon, Microsoft, and Google continue to invest heavily in their own infrastructure. Although many still rely on Equinix for neutral interconnection services, increased vertical integration by these large players could gradually shift certain workloads away from third-party colocation over time.

Geopolitical and regulatory developments present another layer of complexity. As Equinix deepens its presence across more than two dozen countries, it faces varying compliance requirements, data sovereignty rules, and infrastructure constraints. These are not new challenges for the company, but they require constant adaptation and could potentially slow specific expansion initiatives in sensitive regions.

Currency fluctuations represent a meaningful variable given the company’s global revenue base. Changes in exchange rates or local economic conditions can impact both revenue and cost structures in ways that are difficult to hedge fully. Additionally, as AI infrastructure demands evolve, customer requirements around power density, cooling, and connectivity may shift at a pace that requires more rapid and capital-intensive responses than historical expansion cycles have demanded.

Final Thoughts

Equinix continues to stand out in the REIT universe by offering a rare combination of digital infrastructure exposure, steady dividend growth, and long-term capital appreciation potential. It is a business deeply woven into the fabric of the internet and enterprise cloud ecosystems, and that positioning is hard to replicate at scale.

The management team brings a steady hand and a proven record of navigating complexity, whether financial cycles, regulatory challenges, or shifts in global tech demand. They have built a company that generates strong and growing operating cash flow and reinvests it smartly, while also returning capital to shareholders through a dividend that has now grown for a full decade without interruption. The step-up to $4.69 per quarter in 2025, a 10.1% increase, signals that management’s confidence in the cash flow outlook is increasing.

The stock is not cheap by conventional valuation metrics, but investors are not paying for convention. They are paying for consistency, global scale, and a front-row seat to the future of digital infrastructure. The recovery from the 52-week low of $701.41 to near $951.90 reflects a market that is re-rating the business based on its improving free cash flow profile and its strategic relevance to the AI infrastructure buildout.

While the capital-intensive nature of the business and global operating risks remain real considerations, Equinix has consistently shown it can manage them well. As enterprises continue investing in cloud, AI, and network resilience, the company is well-positioned to benefit. For those looking to pair long-term growth with income, it remains one of the more compelling stories in its space.