Key Takeaways

📈 Essent’s dividend yield sits at 2.10% with a recent raise to $0.31 per share quarterly, backed by an exceptionally low 17.97% payout ratio that leaves substantial room for continued growth.

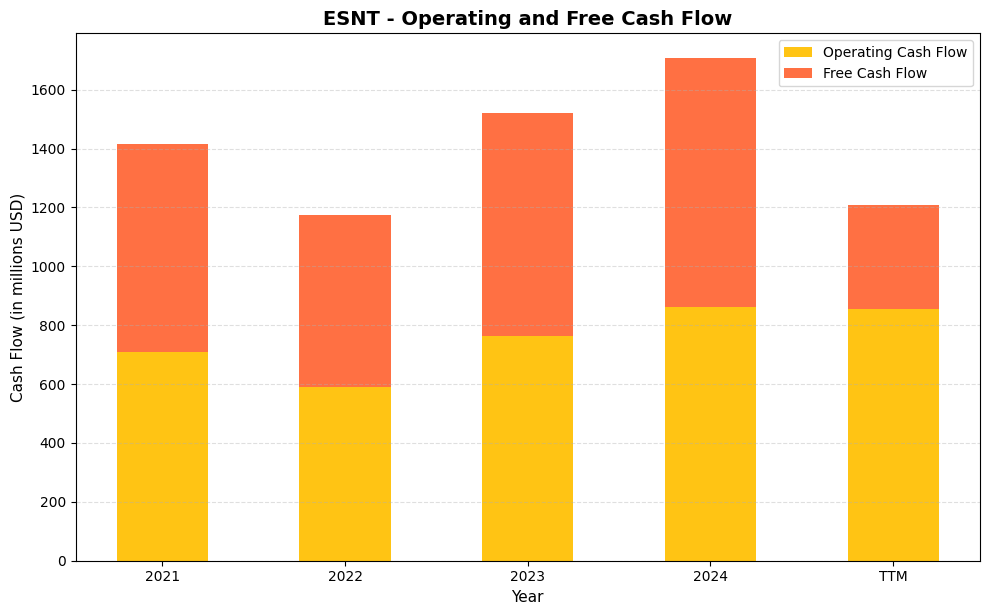

💰 Operating cash flow reached $856.1 million over the trailing twelve months, with free cash flow of $351.3 million, reflecting strong core earnings and ongoing capital flexibility.

🧐 Analysts maintain a constructive outlook with a consensus buy rating and a mean price target of $68.31, implying meaningful upside from current levels near $59.58.

📊 Essent trades at just 8.63 times earnings and essentially at book value, presenting an undemanding valuation for a business generating profit margins above 54%.

Updated 2/25/26

Essent Group Ltd. (ESNT) operates a focused and profitable business providing mortgage insurance and reinsurance solutions across the U.S. With a steady underwriting approach, strong capital position, and consistent free cash flow, the company has quietly built a reputation for disciplined growth and shareholder returns. Its leadership team, led by CEO Mark Casale, has remained committed to long-term value over short-term gains, guiding the company through varying housing and rate environments.

Shares of ESNT offer a modest yield with a growing dividend, supported by a low payout ratio and a clean balance sheet. The stock trades at attractive valuation levels relative to its earnings and book value, with room for upside as earnings continue to grow. The consensus analyst price target of $68.31 sits well above the current price of $59.58, suggesting the market has yet to fully price in the company’s earnings power and capital strength.

Recent Events

Essent has continued to execute its focused mortgage insurance strategy heading into 2026, with the company’s most recent public disclosures pointing to ongoing strength in credit performance and underwriting discipline. Management has maintained its conservative posture in new insurance written, prioritizing margin quality over volume, which has been a consistent theme under CEO Mark Casale’s leadership. The company’s reinsurance arrangements, including quota share agreements established in prior periods to cover a portion of new insurance written, remain a structural part of how Essent manages its capital and risk exposure across cycles.

On the capital return front, the dividend was raised to $0.31 per share quarterly beginning with the March 2025 payment, up from the $0.28 per share rate that had been in place through the second half of 2024. That represents a roughly 10.7% increase and continues a track record of consistent annual dividend growth since the company initiated its payout in 2020. The company’s buyback program has also remained active, providing an additional lever for capital return alongside the growing dividend.

The broader mortgage insurance environment remains tied to the trajectory of interest rates and housing affordability. Elevated rates have kept refinancing activity subdued and limited new origination volumes, but Essent’s persistency on its existing book of insurance in force has helped support earned premiums. Management has shown a steady hand in navigating these conditions, and the company’s profitability metrics remain well above industry norms.

Key Dividend Metrics 🧾

📈 Forward Dividend Yield: 2.10%

💵 Annual Dividend Rate: $1.40

💰 Most Recent Quarterly Dividend: $0.31

📊 5-Year Average Yield: 1.80%

🛡️ Payout Ratio: 17.97%

📅 Last Dividend Paid: May 30, 2025

📆 Most Recent Ex-Dividend Date: March 14, 2025

For dividend investors, these numbers paint a picture of a company that’s not just paying out cash, but doing so from a position of real strength.

Dividend Overview

On the surface, Essent’s 2.10% yield might seem modest, especially in a world where higher yields are easily found elsewhere. But the payout ratio of just under 18% is the real headline. It means this dividend isn’t just safe, it has significant room to grow even if the economy softens materially. With earnings per share of $6.90 supporting a $1.40 annual dividend, the coverage is exceptionally comfortable by any standard.

The company is highly profitable, with a return on equity of 12.15% and return on assets of 7.34%, alongside a profit margin above 54%. Those figures tell you Essent knows how to deploy capital effectively. Rather than stretching to juice the yield, management is balancing payouts with smart reinvestment and share repurchases. That kind of approach tends to produce better total returns over time than a company prioritizing a high headline yield over financial discipline.

One of the more impressive aspects of the company’s strategy is how consistent it has been. Even in uncertain housing and rate environments, they’ve kept the dividend intact and growing. For investors building a reliable income stream, that kind of steadiness matters more than chasing an extra point or two of yield from a less financially sound business.

Dividend Growth and Safety

Essent began paying a dividend in early 2020 and has raised the payout every single year since. That’s not just a gesture toward shareholder friendliness, it’s a sign of a business maturing in the right way. The raises have come because the fundamentals support them, not as a marketing exercise.

The most recent increase brought the quarterly payout to $0.31 per share, or $1.24 annualized at the time, with the current annual rate now standing at $1.40 per share. Tracing the dividend history makes the progression clear: from $0.22 per quarter in mid-2022 to $0.23, then $0.25, then $0.28, and now $0.31, each step reflects a business generating more cash than it needs to sustain operations. What’s notable is how these raises have come with virtually no strain on the balance sheet, and the payout ratio has remained well below 20% throughout this entire growth arc.

The dividend is well covered not just by earnings but by operating cash flow of $856.1 million, which compares very favorably to the total annual dividend obligation on a per-share basis. Free cash flow came in at $351.3 million for the trailing period, and while that figure is lower than operating cash flow due to investing activity, it still provides ample coverage for the dividend at current levels. Combine that with a management team clearly focused on maintaining a conservative payout strategy, and the income stream looks durable and likely to keep expanding.

Essent may not be on every dividend investor’s radar yet, but between its strong cash generation, disciplined management, and a growing payout backed by real earnings power, this is the kind of company that quietly delivers the returns long-term income investors are seeking.

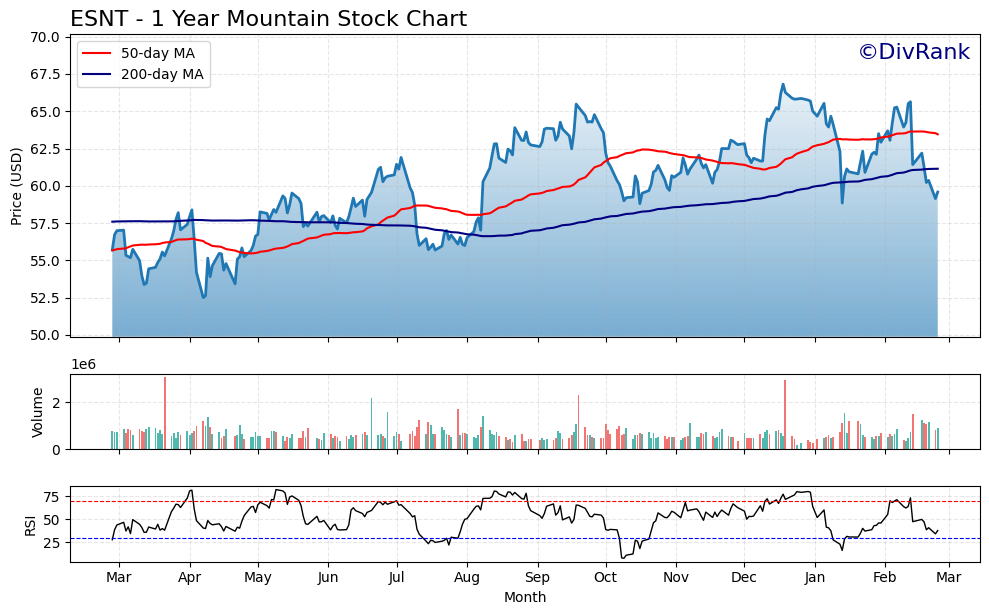

Chart Analysis

Essent Group has had a range-bound but volatile twelve months, trading between $52.50 and $66.82 before settling at $59.58 as of the most recent session. That current price sits roughly 10.8% below the 52-week high, which tells a story of a stock that found real buying interest in the mid-$50s but has struggled to sustain momentum on any push toward the upper end of its range. The broader price action reflects the uncertainty that has followed private mortgage insurers as housing affordability concerns and macroeconomic noise weigh on sentiment, even as ESNT’s underlying fundamentals have remained relatively stable.

The moving average picture is mixed but not without a constructive element. ESNT is currently trading below both its 50-day moving average of $63.45 and its 200-day moving average of $61.14, which places the stock in technically challenged territory in the near term. The silver lining is that the 50-day remains above the 200-day, a configuration known as a golden cross, which reflects the trend improvement that occurred earlier in the year. The concern for chart-focused investors is that price has now undercut the 200-day, turning what was a support level into potential overhead resistance. A sustained recovery back above $61.14 would be an encouraging first step toward reestablishing a healthier technical posture.

The RSI reading of 37.63 places ESNT in oversold territory, approaching but not yet breaching the conventional 30-level threshold that often signals exhausted selling pressure. Momentum is clearly negative in the short run, and there is no obvious technical catalyst yet to suggest a reversal is imminent. Historically, RSI readings in this zone can precede mean-reversion bounces, particularly in fundamentally sound companies where the selloff has been sentiment-driven rather than earnings-driven, but confirmation through price stabilization near current levels would be important before reading too much into that signal alone.

For dividend investors, the current setup presents a familiar tension between price weakness and improving yield. The pullback has pushed ESNT closer to a more attractive entry valuation, and the stock’s distance of roughly 13.5% above its 52-week low suggests downside has been at least partially absorbed. Income-focused investors with a multi-year horizon may view the current price as a reasonable accumulation zone, particularly given ESNT’s history of returning capital through both its regular dividend and special dividend distributions. Those watching from the sidelines would want to see the stock reclaim and hold the $61 area before treating the technical picture as anything more than a work in progress.

Cash Flow Statement

Essent Group’s cash generation has been a standout feature of its financial profile, and the numbers here leave little room for doubt about dividend sustainability. Operating cash flow climbed from $709.3 million in 2021 to $861.5 million in 2024, a gain of more than 21% over that three-year stretch, with free cash flow tracking almost identically given the company’s minimal capital expenditure requirements. The near-perfect conversion of operating cash into free cash flow is a reflection of the asset-light nature of private mortgage insurance, where the business does not need to sink capital into factories, equipment, or heavy infrastructure to grow. The TTM free cash flow figure of $351.3 million represents a meaningful departure from the full-year 2024 reading of $844.8 million, and investors should monitor whether that gap reflects timing differences in investment activity or a more structural shift in how cash is being deployed. For dividend coverage purposes, the underlying operating cash flow stream of $856.1 million on a TTM basis remains more than sufficient to service Essent’s current dividend obligations by a wide margin.

Stepping back across the full timeline, the 2022 dip to $588.8 million in operating cash flow stands out as the one soft patch in an otherwise consistent upward trend, and it coincided with the broader mortgage market contraction as rising interest rates compressed origination volumes and slowed new insurance written. The recovery to $763.0 million in 2023 and the subsequent push to $861.5 million in 2024 demonstrated that Essent’s in-force book of business generates durable, recurring premium income that can offset cyclical pressure on new business volumes. Capital efficiency across this period has been exceptional, with free cash flow conversion rates consistently above 98% of operating cash flow in each full calendar year shown. For shareholders focused on long-term dividend growth, that level of capital efficiency means management has substantial flexibility to simultaneously fund dividend increases, support share repurchases, and build the investment portfolio that underpins Essent’s regulatory capital position, all without stretching the balance sheet.

Analyst Ratings

Analyst sentiment on Essent is broadly constructive heading into 2026, with a consensus buy rating across eight covering analysts. The mean twelve-month price target stands at $68.31, which represents roughly 14.6% upside from the current price of $59.58. Price targets range from a low of $63.00 to a high of $75.00, and the fact that even the most conservative target sits above the current price suggests analysts broadly view the stock as undervalued at present levels.

The constructive consensus reflects confidence in Essent’s underwriting discipline, its consistent earnings generation, and its ability to manage credit performance through a prolonged period of elevated rates and constrained housing activity. Analysts covering the stock appear to appreciate the company’s conservative capital management approach and the durability of its earnings, which have held up well despite headwinds in the broader mortgage origination market.

With the stock trading at $59.58 against a mean target of $68.31 and a low target of $63.00, the current price appears to offer a margin of safety relative to the analyst community’s view of fair value. That gap, combined with the buy consensus, suggests the market is pricing in more risk than analysts believe is warranted given the company’s financial profile and track record.

Earning Report Summary

Solid Finish to the Year

Essent Group posted earnings per share of $6.90 for the trailing period, with net income of approximately $690 million on revenue of $1.26 billion. The profit margin of 54.72% reflects the company’s highly efficient operating model and the earnings leverage inherent in a well-seasoned book of mortgage insurance in force. Return on equity came in at 12.15%, a level that, while modestly below prior-year figures, remains strong in the context of a financial services business managing capital conservatively.

CEO Comments and Strategic Moves

CEO Mark Casale has consistently emphasized credit discipline and underwriting quality as the foundations of Essent’s operating approach. Management has highlighted the company’s reinsurance arrangements as an important tool for capital flexibility, with quota share agreements providing structured risk distribution on new insurance written. The tone from leadership has remained measured and focused on long-term profitability rather than volume growth, a posture that has served shareholders well through the rate cycle of the past few years.

Book Value, Investment Income, and Shareholder Returns

Book value per share stands at $60.31, and with the stock trading at $59.58, ESNT is currently priced at essentially one times book, a level that historically has represented fair to attractive entry for this business. Investment income has continued to benefit from the higher rate environment, contributing meaningfully to the bottom line and reinforcing the company’s ability to sustain and grow its dividend. The quarterly payout of $0.31 per share reflects management’s confidence in the ongoing earnings trajectory, and the active buyback program provides additional capital return for shareholders.

Looking Ahead

Essent enters 2026 with a lean payout ratio, a strong balance sheet, and a management team that has demonstrated the ability to navigate a challenging mortgage environment without compromising the company’s financial integrity. The primary variables to watch are the trajectory of interest rates and their effect on new insurance written volumes, as well as credit performance across the existing portfolio. Based on current trends, the setup appears favorable for continued earnings stability and ongoing dividend growth.

Management Team

Essent Group’s leadership brings a steady hand and deep industry knowledge, which shows up clearly in how the company operates. Mark A. Casale, the founder, continues to serve as Chairman and CEO, providing long-term stability at the top. His leadership has guided the company from its early days into a mature, profitable business without losing sight of its disciplined underwriting and risk-focused culture.

Supporting him is a team of experienced executives with strong backgrounds in insurance, finance, and risk management. CFO Lawrence V. McAlee has played a key role in maintaining the company’s financial health, ensuring the balance sheet stays flexible while supporting capital returns. Other executives in operations and analytics have also stayed with the firm for many years, creating consistency across departments. This continuity has helped Essent avoid the common pitfalls of turnover and strategic drift.

The overall tone from leadership is pragmatic and grounded. They don’t chase headlines or make aggressive moves just to meet short-term goals. Instead, they manage the business with an eye on long-term performance, steady returns, and sustainable growth, which is reflected in the company’s solid financials and conservative balance sheet.

Valuation and Stock Performance

Essent currently trades at a price-to-earnings ratio of 8.63, which is modest by almost any standard for a business generating profit margins above 54% and returns on equity above 12%. The price-to-book ratio of 0.99 means investors are acquiring the stock at essentially the accounting value of its net assets, a level that has historically been an attractive entry point for well-run financial services companies with strong earnings power. With book value per share at $60.31 and the current price at $59.58, the stock is trading at a slight discount to book, which is unusual for a business of Essent’s quality.

Over the past year, the stock has traded in a range of $51.61 to $67.09, and the current price of $59.58 sits roughly in the middle of that band. The beta of 0.90 reflects somewhat lower volatility than the broader market, which is consistent with the company’s stable earnings profile and limited exposure to speculative activity. Short interest of approximately 1.69 million shares is not elevated, suggesting no significant bearish conviction from institutional players.

Essent doesn’t need a surge in valuation multiples to deliver shareholder value. It generates consistent cash flow, pays a growing dividend, and has committed to a meaningful buyback program. If the market begins to assign a more normal earnings multiple to a business of this quality, the re-rating potential from current levels is meaningful, and the analyst consensus target of $68.31 reflects exactly that view.

Risks and Considerations

Like any company tied to the housing sector, Essent is exposed to macroeconomic shifts. Rising interest rates or a prolonged slowdown in mortgage originations can directly affect the volume of new insurance written. If home prices were to fall meaningfully from current levels, that could also impact credit performance and increase claim activity across the existing book of insurance in force.

There is also a layer of regulatory risk that comes with operating in the mortgage insurance space. Essent operates under guidelines set in part by the GSEs and federal housing regulators, and any changes to capital requirements, underwriting standards, or eligibility rules could influence the company’s operating model and competitive positioning.

The business is also somewhat concentrated in a single product category and geography. Essent focuses primarily on U.S. private mortgage insurance, with limited diversification across insurance types or international markets. That singular focus carries advantages in terms of expertise and efficiency, but it also means the company has less insulation from shocks specific to the domestic housing and mortgage market.

Competition in the private mortgage insurance space remains intense, with several well-capitalized players often competing on price to maintain or grow market share. While Essent has historically prioritized margin quality over volume, that discipline could face pressure if competitors become more aggressive on pricing during periods of lower origination activity.

Final Thoughts

Essent Group has quietly built a business defined by consistency, profitability, and careful risk management. It doesn’t grab headlines, but it delivers results. The management team knows the industry deeply and has shown a willingness to stay disciplined through cycles rather than overreact to market pressures or chase growth at the expense of quality.

The current valuation at 8.63 times earnings and essentially one times book reflects a level of market caution that doesn’t appear fully aligned with the company’s actual performance. With a growing dividend now at $1.40 per share annually, a payout ratio under 18%, and a consensus analyst price target of $68.31 sitting well above the current price of $59.58, the building blocks for meaningful shareholder value are clearly in place.

While risks remain tied to the housing market and broader economic conditions, Essent has demonstrated the ability to navigate those challenges with conservative underwriting and a strong capital base. The company’s focus on core profitability, disciplined risk management, and consistent capital return provides a solid foundation to build on.

This isn’t a company built for the short term. It’s structured for resilience, long-term value creation, and steady returns, all qualities that can compound meaningfully over time for patient income investors.