Key Takeaways

📈 EOG carries a forward dividend yield of 3.30% with a 43% payout ratio and continued growth, including a recent raise to $1.02 per share per quarter.

💰 Operating cash flow reached $10.2 billion over the trailing twelve months, with free cash flow of $2.9 billion supporting dividends and ongoing capital returns.

📊 Twenty-nine analysts maintain a buy consensus on EOG with a mean price target of $132.93, suggesting modest upside from the current price of $123.70.

🛢️ EOG generated $9.12 in earnings per share over the trailing twelve months, supported by a 24.4% profit margin and an 18.5% return on equity.

Updated 2/25/26

EOG Resources (EOG) is a major independent oil and gas producer with a long-standing reputation for capital discipline, efficient operations, and shareholder-focused strategy. With operations concentrated in prolific U.S. basins like the Delaware, Utica, and Eagle Ford, the company consistently generates strong free cash flow while maintaining one of the lowest cost structures in the sector.

In recent quarters, EOG has continued to grow oil production, reduce well costs, and return significant capital through dividends and share repurchases. The balance sheet remains healthy, with a conservative payout ratio that supports both income and flexibility, and the company has once again demonstrated its willingness to grow the dividend as conditions allow.

Recent Events

EOG Resources has been navigating a moderately challenging stretch in the energy market as we head through the first quarter of 2026. Crude oil prices have remained under pressure from a combination of elevated OPEC+ output and softer global demand signals, creating headwinds across the E&P space. Despite this backdrop, EOG has remained operationally focused, continuing to execute on its cost reduction programs and maintaining discipline around capital spending, which has been a consistent theme under CEO Ezra Yacob’s leadership.

The company raised its quarterly base dividend to $1.02 per share in the fourth quarter of 2025, up from $0.975, marking another step in EOG’s pattern of steady base dividend growth. That increase took effect with the October 2025 payment and was reaffirmed with the January 2026 distribution, signaling management’s continued confidence in the underlying cash flow profile of the business even in a softer commodity environment.

On the operational front, EOG has continued to expand activity in the Utica and Dorado basins while keeping the Delaware Basin as its primary production engine. The company’s internal drilling motor program and ongoing completion efficiency efforts have kept per-well costs moving in the right direction, a key competitive advantage as the broader industry deals with lingering cost inflation. Investors heading into the next earnings cycle will be watching production volumes and updated capital guidance closely.

Key Dividend Metrics

📈 Forward Yield: 3.30%

💰 Annual Dividend Rate: $4.08 per share

📆 Dividend Payout Ratio: 43.26%

🔁 Last Dividend Payment: $1.02 per share (January 16, 2026)

📊 Recent Dividend Growth: Raised from $0.975 to $1.02 in Q4 2025

💼 Payout Coverage: Operating cash flow of $10.2 billion and free cash flow of $2.9 billion provide strong support

Dividend Overview

EOG’s current annualized dividend of $4.08 per share translates to a forward yield of roughly 3.30% at the current price of $123.70. That yield sits comfortably above the typical S&P 500 payout and is particularly attractive given the conservative way it is funded. A payout ratio of 43% against trailing earnings of $9.12 per share leaves meaningful room for continued growth or special distributions during periods of stronger commodity pricing.

Beyond the regular quarterly base dividend, EOG has historically used special dividends as a core component of its capital return strategy. Rather than permanently committing to a higher base payout that might become unsustainable in a downcycle, the company has been willing to supplement base distributions in strong cash flow years, rewarding shareholders without sacrificing balance sheet flexibility. That model has proven durable across multiple commodity cycles and continues to distinguish EOG from peers that have overextended their dividend commitments.

The most recent dividend increase, from $0.975 to $1.02 per quarter, represents a roughly 4.6% raise and reflects management’s measured but consistent approach to growing the income stream. Income investors can reasonably expect that pattern to continue as long as free cash flow remains supportive, which the current operational profile suggests it will.

Dividend Growth and Safety

EOG’s dividend history over the past several years tells a clear story of deliberate, sustained growth. Starting from $0.825 per quarter in mid-2023, the company has moved the base payout up in a series of incremental steps, reaching $1.02 per quarter as of October 2025. That represents a cumulative increase of roughly 24% over approximately two and a half years, a meaningful pace of growth for an energy producer operating in a volatile pricing environment.

The safety of that dividend rests on a cash flow foundation that remains genuinely impressive. Over the trailing twelve months, EOG generated $10.2 billion in operating cash flow. Even with capital expenditures running at elevated levels to support production growth, free cash flow came in at $2.9 billion, more than sufficient to cover the total dividend outlay. With $9.12 in earnings per share and a payout ratio sitting just above 43%, there is no credible near-term threat to the dividend even if commodity prices soften further from current levels.

The company’s return metrics reinforce this picture. A return on equity of 18.5% and a return on assets of 9.1% reflect a business that allocates capital efficiently and generates above-average profitability relative to its asset base. A profit margin of 24.4% on revenues of $22.7 billion is a strong result by any measure, and it underscores why EOG has been able to grow its dividend consistently without stretching its financial resources.

Institutional ownership in EOG remains high, as large sophisticated investors continue to treat it as a core holding within the energy sector. That constituency values dividend consistency and balance sheet prudence, and EOG’s management has made it clear that maintaining that trust is a central priority. The result is a dividend that is not just attractive today but supported by a business model built to sustain and grow income payments over time.

Chart Analysis

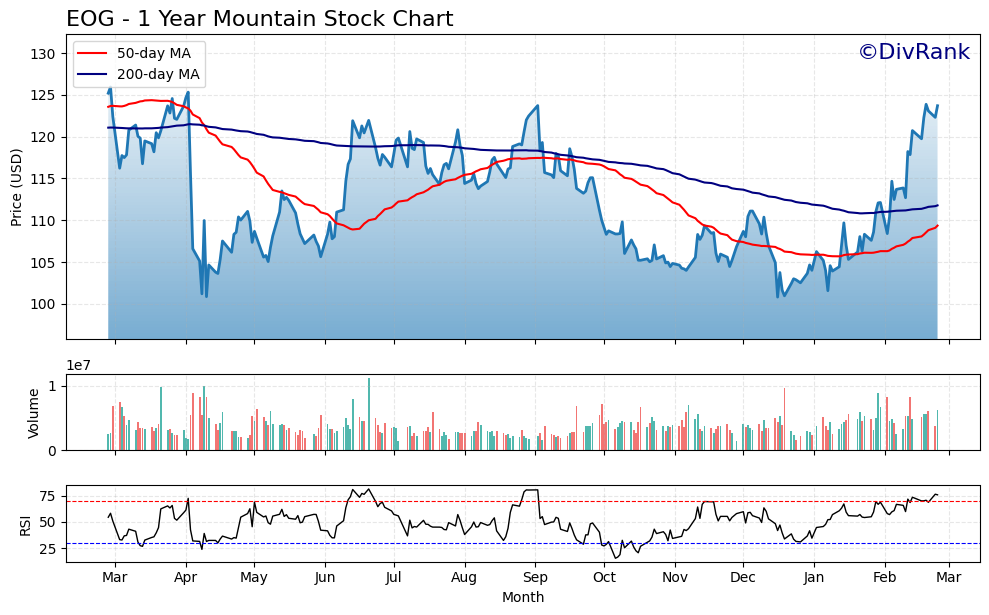

EOG Resources has staged a strong recovery over the past year, climbing from a 52-week low of $100.82 to its current price of $123.70, a gain of roughly 22.7% from trough to present. That move has carried the stock to within striking distance of its 52-week high of $125.94, sitting just 1.78% below that level as of the most recent close. The price action over this period reflects a broadly constructive trend, with buyers consistently defending pullbacks and the most recent leg of the advance showing genuine momentum rather than a slow grind higher.

The moving average picture tells a more nuanced story. EOG is trading comfortably above both its 50-day moving average of $109.36 and its 200-day moving average of $111.78, which in isolation is a bullish configuration. However, the 50-day remains below the 200-day, a setup technically classified as a death cross, suggesting the intermediate trend had been weakening before the recent surge began. The current price strength has pulled the stock well clear of both averages, but dividend investors should recognize that the moving averages have not yet realigned in a traditional golden cross formation, meaning the longer-term trend has not fully confirmed the recent recovery.

The RSI reading of 75.73 places EOG firmly in overbought territory, above the conventional threshold of 70. Momentum is clearly running hot, and while strong RSI readings can persist during genuine breakouts, a reading at this level does raise the probability of a near-term consolidation or modest pullback. For investors looking to initiate or add to a position, patience here is likely to be rewarded, as even a brief digestion of the recent gains could offer a more favorable entry point relative to the 50-day moving average around $109.

From a dividend investor’s perspective, the technical setup is a mixed but ultimately constructive read. The proximity to the 52-week high and elevated RSI argue against chasing the stock at current levels, but the underlying price recovery and strong positioning above both key moving averages reflect a market that is giving EOG’s fundamentals real credit. Investors focused on long-term income generation may find the current setup more suitable for building a watchlist price target than for immediate deployment of capital, with a pullback toward the $110 to $113 range offering a more attractive risk-reward entry into what remains a high-quality energy dividend grower.

Cash Flow Statement

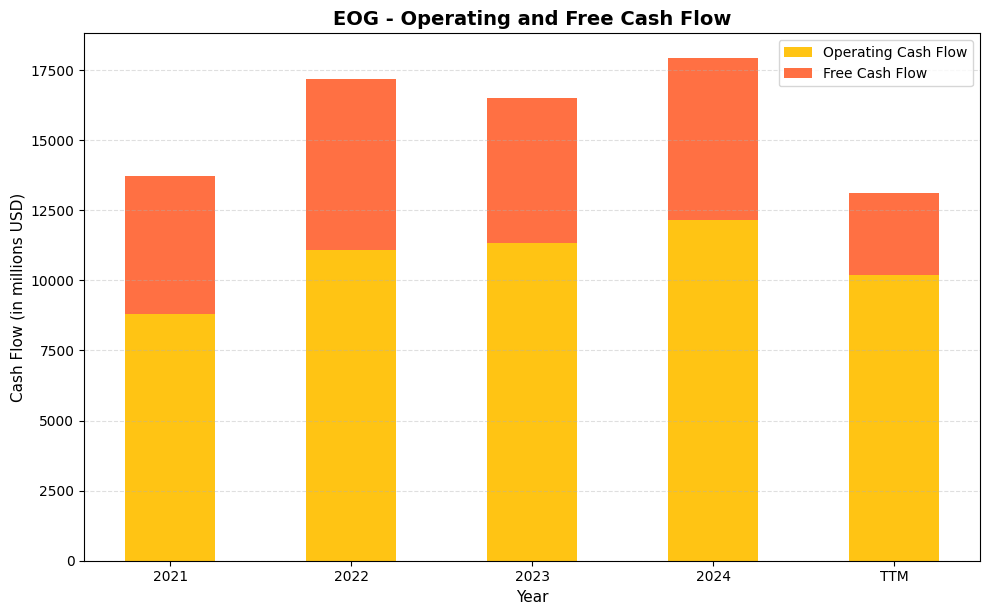

EOG’s cash generation has been one of the most compelling parts of its dividend story over the past several years. Operating cash flow climbed from $8,791.0 million in 2021 to $12,143.0 million in 2024, a gain of roughly 38% over that stretch, reflecting the company’s ability to convert higher realized prices and disciplined well costs into real cash rather than just accounting earnings. Free cash flow followed a similar arc, rising from $4,941.0 million in 2021 to a peak of $6,093.0 million in 2022 before settling back to $5,155.0 million in 2023 and recovering to $5,771.0 million in 2024. The TTM figures show operating cash flow at $10,195.0 million and free cash flow at $2,926.7 million, a notable step down that reflects both elevated capital spending cycles and the commodity price environment in recent quarters. Even so, $2.9 billion in trailing free cash flow is a substantial cushion for a company paying a regular dividend supplemented by special distributions, and it does not signal any structural impairment to dividend coverage.

Stepping back across the full four-year picture, what stands out is how consistently EOG has kept its capital reinvestment disciplined enough to preserve meaningful free cash flow in every year shown. The spread between operating cash flow and free cash flow, representing capital expenditures, has generally run in the $5.0 billion to $6.2 billion range, which reflects a company investing seriously in its premium drilling inventory without letting spending creep undermine shareholder returns. The 2022 free cash flow peak of $6,093.0 million funded a surge in special dividends that income investors will remember well, and the more modest but still healthy readings since then have supported continued regular dividend growth. For dividend investors, the key takeaway is that EOG generates enough operating cash to fund its capital program, its regular dividend, and its special distributions with room to spare in most commodity environments, making the payout far more durable than what a simple earnings-based payout ratio would suggest.

Analyst Ratings

The analyst community remains constructive on EOG Resources, with 29 analysts currently covering the stock and a consensus buy rating reflecting broad confidence in the company’s fundamentals. The mean 12-month price target of $132.93 implies roughly 7.5% upside from the current price of $123.70, a modest but meaningful premium that suggests the market has not fully priced in the company’s operational strengths and cash flow generation capacity.

The range of price targets among analysts spans from a low of $108.00 to a high of $157.00, indicating a meaningful spread in views on how commodity pricing and production growth will play out over the next year. The lower end of that range reflects a more cautious macro view on crude oil prices, while the upper end captures the potential for a recovery in energy demand and EOG’s ability to grow volumes efficiently. At the current price of $123.70, EOG is trading below the analyst consensus target, which historically has been a reasonable entry signal for patient income investors.

The buy consensus also reflects analyst appreciation for EOG’s balance sheet strength, its consistent free cash flow generation, and its track record of disciplined capital allocation. In an E&P peer group where financial leverage and cost structures vary widely, EOG’s conservative approach continues to earn premium standing among institutional research desks.

Earning Report Summary

Strong Profitability on Substantial Revenue Base

EOG Resources posted trailing twelve-month earnings per share of $9.12 on revenues of $22.7 billion, reflecting a business that continues to generate substantial profits even as commodity prices have softened from their peaks. Net income of $5.53 billion represents a profit margin of 24.4%, which is a high-quality result for an E&P company operating in the current environment and compares favorably to most of the company’s publicly traded peers.

Operating cash flow of $10.2 billion underscores the fact that EOG’s earnings quality is high, with cash generation closely tracking reported income. That alignment between accounting profits and actual cash flow is a meaningful indicator of business quality and gives dividend investors confidence that payouts are backed by real economic performance rather than accounting-driven figures.

Production and Cost Discipline Remain Central Themes

EOG’s operational execution continues to be the core driver of its financial results. The company’s focus on reducing per-well costs through internal technology programs, including its in-house drilling motor initiative, has kept the cost structure competitive even as the industry broadly dealt with inflationary pressure on equipment and labor. Management has consistently guided toward further efficiency gains, and the results in recent periods suggest those targets are being met.

The Delaware Basin remains the company’s primary production hub, but activity in the Utica and Dorado basins is contributing meaningfully to the overall growth story. This geographic diversification within the U.S. provides some operational flexibility and reduces concentration risk in any single producing region.

Capital Allocation Continues to Favor Shareholders

EOG raised its quarterly dividend to $1.02 per share in October 2025 and maintained that level through the January 2026 payment, signaling management’s confidence in the sustainability of the current payout. The company’s buyback authorization remains active, providing an additional tool for capital return when valuation and cash flow conditions are favorable. The combination of a growing base dividend, the potential for special distributions in stronger years, and an active repurchase program reflects a shareholder return framework that is comprehensive and well-funded.

Outlook Remains Grounded in Operational Discipline

Looking ahead, EOG’s capital spending plans remain disciplined, with management emphasizing efficiency and returns over volume growth for its own sake. The company continues to target a balance between reinvestment and shareholder returns that is appropriate for the current commodity price environment, and guidance has consistently reflected a conservative approach to planning assumptions. While oil price volatility will always introduce uncertainty into forward projections, EOG’s cost structure and balance sheet give it meaningful downside protection relative to less disciplined peers.

Management Team

EOG Resources has long been respected for its disciplined and consistent leadership. The management team is known not for bold, risky bets, but for operational efficiency and capital restraint, traits that tend to matter more as market cycles stretch out. Ezra Yacob, who took on the CEO role in 2021, has continued to build on the company’s legacy of thoughtful execution. His tenure has been marked by a steady hand, even in a choppy commodity environment, and the series of dividend increases approved under his leadership reflect genuine confidence in the company’s cash generation capacity.

Under Yacob’s direction, EOG has remained committed to generating value through low-cost production and strategic reinvestment. The executive team has maintained a strong balance sheet and stayed conservative in its guidance. While some peers have jumped aggressively into acquisitions or expanded spending in pursuit of top-line growth, EOG has stuck with a focused plan built around efficient operations, cost control, and responsible shareholder returns.

The culture inside EOG leans heavily into data and innovation, and it shows. Internal programs such as the in-house drilling motor initiative continue to reduce costs and improve well performance. Management doesn’t chase headlines, it chases margins. That mindset has helped the company consistently outperform in difficult environments and preserve flexibility when others have been forced to retreat. For income investors, a management team with this orientation is exactly what you want standing behind a dividend commitment.

Valuation and Stock Performance

At $123.70, EOG trades at a trailing price-to-earnings ratio of 13.56 and a price-to-book ratio of 2.22 against a book value of $55.69 per share. The P/E multiple is modest by broader market standards and reflects the market’s tendency to discount energy sector earnings as cyclical and potentially mean-reverting. For investors who believe EOG’s current earnings power is sustainable rather than cyclical peak, that valuation represents a reasonable entry point with a solid dividend yield attached.

The stock’s 52-week range of $101.59 to $134.49 places the current price near the upper half of that band, suggesting the market has partially recovered from earlier lows but has not yet pushed through to new highs. With the analyst consensus target at $132.93 and the high-end target at $157.00, there is a credible case for meaningful appreciation from current levels if commodity prices stabilize and production growth continues on its current trajectory.

EOG’s beta of 0.47 is notably low for an energy producer, which means the stock has historically moved less than half as much as the broader market in either direction. That characteristic makes it a more comfortable holding for income-oriented investors who want energy exposure without the extreme volatility that often accompanies smaller or more leveraged E&P names. A market cap of approximately $67.5 billion confirms EOG’s status as one of the largest independent oil and gas companies in the United States, with the liquidity and institutional following that comes with that scale.

The return on equity of 18.5% and the profit margin of 24.4% are both metrics that reflect genuine earnings quality, not financial engineering. For a stock trading at roughly 13.5 times trailing earnings with a 3.3% dividend yield and a buy consensus from 29 analysts, EOG’s current valuation looks attractive to investors willing to hold through the inevitable near-term fluctuations that come with any commodity-linked business.

Risks and Considerations

Like any company tied to commodities, EOG’s fortunes will always be partly at the mercy of market pricing. Volatility in crude oil and natural gas can have a direct impact on revenue, earnings, and ultimately free cash flow. While EOG has done a commendable job managing these cycles through a disciplined cost structure, it cannot completely insulate itself from global supply and demand shifts, OPEC+ production decisions, or geopolitical disruptions that move prices unpredictably. The decline in free cash flow from $5.77 billion in the prior comparable period to $2.9 billion in the trailing twelve months is a concrete reminder of how quickly commodity price changes can affect the financial profile of even a well-run producer.

Hedging strategies can help smooth results, but they also come with opportunity costs. In strong pricing environments, hedges can limit upside, and when volatility hits hard, even carefully constructed protection programs do not always prevent earnings drawdowns. Investors should approach EOG with a clear-eyed understanding that the income stream, while well-covered and growing, exists within a commodity business framework that does not offer the same predictability as a utility or consumer staples dividend.

Regulatory and environmental pressures also represent a continuing risk for the E&P sector broadly and EOG specifically. The political and policy environment around domestic oil and gas production can shift with administrations, and any significant tightening of permitting, emissions standards, or royalty structures could affect the company’s cost profile or operational flexibility. EOG has made meaningful progress on emissions reduction and water usage efficiency, but it operates in an industry that remains subject to ongoing policy scrutiny.

Labor and supply chain dynamics continue to be worth monitoring. The energy sector has dealt with cost inflation across equipment, personnel, and services, and while EOG’s internal technology programs have helped offset some of those pressures, they remain part of the operating backdrop. Any sustained increase in service costs or well completion expenses could compress margins and reduce the free cash flow available for dividends and buybacks.

Finally, short interest of approximately 14.3 million shares represents a modest but real overhang on the stock. While not alarmingly high for a company of EOG’s size, it does indicate that some market participants have a bearish view on near-term prospects, most likely tied to oil price expectations. That positioning could create additional volatility around earnings announcements or significant commodity price moves.

Final Thoughts

EOG Resources is the kind of company that quietly builds long-term value while letting others chase headlines. Its consistent execution, conservative financial management, and shareholder-focused approach set it apart in a sector known for its dramatic highs and painful lows. The recent raise to $1.02 per quarter is the latest demonstration that management is serious about growing income payments over time, and the 43% payout ratio leaves plenty of room to continue doing so.

The leadership team under Ezra Yacob is not likely to make big moves just to keep up with faster-growing peers, and that restraint is a feature rather than a flaw. What EOG offers is a stable, cash-rich model with a proven track record of managing through downcycles and capitalizing during periods of strength. For investors with a long view, it is a business that rewards patience, operational focus, and clarity of purpose.

At $123.70 with a 3.3% yield, a P/E of 13.56, and a buy consensus from 29 analysts, EOG sits in a reasonable valuation range with a competitive income profile. The energy market will always have its swings, and EOG is not immune to them. But its ability to maintain high margins, generate meaningful free cash flow, and keep costs under control positions it well to navigate uncertainty and continue growing the dividend that income investors have come to rely on.