Key Takeaways

💰 Ecolab offers a forward dividend yield of 0.88% with a payout ratio under 37%, supported by over 30 years of consecutive dividend increases and consistent mid-to-high single-digit growth.

📊 Operating cash flow reached $2.95 billion over the trailing 12 months, generating $1.64 billion in free cash flow, comfortably covering capital needs and dividend commitments.

📈 Analyst sentiment is firmly positive with a Buy consensus across 21 analysts and an average price target of $321.86, suggesting modest additional upside from current levels near the 52-week high.

🧾 Ecolab raised its quarterly dividend to $0.73 per share in December 2025, representing a meaningful step up from the prior $0.65 rate and continuing a track record of uninterrupted annual increases.

Updated 2/25/26

Ecolab Inc. (ECL) is a global leader in water, hygiene, and infection prevention solutions, serving industries from healthcare to hospitality. With over a century of operating history and a presence in more than 170 countries, the company has built a reputation for consistent performance, strong margins, and dependable dividend growth. Its services are foundational to the safety and efficiency of businesses worldwide.

The company’s leadership, anchored by CEO Christophe Beck, continues to execute with discipline, focusing on high-margin segments and sustainable innovation. Despite macro headwinds and valuation premiums, Ecolab has maintained steady earnings growth, expanded margins, and delivered reliable shareholder returns.

Recent Events

Ecolab has had considerable momentum heading into early 2026. The stock is trading at $308.16, just a dollar below its 52-week high of $309.15, reflecting sustained investor confidence in the company’s operational execution and long-term positioning. Over the past year, ECL has climbed from a low of $221.62, representing a gain of nearly 40% from trough to recent peak, a run that has meaningfully outpaced the broader market and validated the company’s earnings trajectory.

The company raised its quarterly dividend to $0.73 per share in December 2025, up from $0.65, marking another year of consecutive increases and reaffirming management’s confidence in the cash generation profile of the business. The new annualized rate of $2.76 per share represents a roughly 12.3% increase over the prior annual rate of $2.60, which is well above the company’s historical mid-single-digit average and signals a notably accelerated pace of shareholder returns.

On the financial front, Ecolab reported full-year revenue of approximately $16.1 billion alongside net income of $2.08 billion and earnings per share of $7.27. Return on equity stands at 22.52%, and the company’s profit margin of 12.91% reflects continued pricing discipline and operational efficiency across its global platform. With a market capitalization now above $87 billion, Ecolab has grown into one of the largest specialty chemicals companies in the world.

Key Dividend Metrics 📊

💵 Forward Dividend Rate: $2.76

📈 Forward Dividend Yield: 0.88%

📊 5-Year Average Dividend Yield: 1.04%

🔄 Last Quarterly Dividend Paid: $0.73

💡 Payout Ratio: 36.81%

📅 Last Dividend Payment: December 16, 2025

⛔ Prior Ex-Dividend Date: December 16, 2025

🏁 Last Split: 2-for-1 in June 2003

Dividend Overview

At first glance, Ecolab’s dividend yield of 0.88% doesn’t exactly jump off the page. It currently sits below the company’s own five-year average yield of 1.04%, which is largely a reflection of how much the stock price has appreciated over the past twelve months rather than any pullback in dividend commitment. This isn’t a stock for someone chasing quick income. It’s for someone who values durability and compounding.

What gives that modest yield real value is the foundation supporting it. Ecolab is not straining to pay its dividend. The payout ratio of 36.81% leaves ample room to continue growing the dividend even through an earnings slowdown, and the company’s services in water treatment, food safety, and infection prevention remain essential regardless of the economic cycle. That built-in demand underpins both revenue stability and dividend reliability.

The December 2025 increase to $0.73 per quarter was a particularly strong move, lifting the annualized rate to $2.76 and delivering a year-over-year increase of roughly 12% on the dividend alone. For income investors willing to accept a lower starting yield in exchange for consistent and accelerating growth, Ecolab continues to make a compelling case.

Dividend Growth and Safety

Ecolab has one of the steadiest dividend track records in the specialty chemicals space. The company has raised its dividend for more than 30 consecutive years, placing it firmly among the Dividend Aristocrats. The pace of growth has historically run in the mid-to-high single-digit range, but the most recent increase broke above that pattern in a meaningful way.

Looking at the dividend history, the quarterly rate held at $0.53 through most of 2023 before stepping up to $0.57 in December of that year, then to $0.65 in December 2024, and most recently to $0.73 in December 2025. Each annual increase has been larger in absolute dollar terms than the last, reflecting growing earnings power and management’s willingness to share that growth with shareholders. The current annualized rate of $2.76 represents a cumulative increase of more than 38% from the $2.12 annualized rate in early 2023.

The numbers supporting dividend safety are strong. Earnings per share of $7.27 cover the $2.76 annual dividend more than 2.6 times over. Operating cash flow of $2.95 billion dwarfs total dividend obligations, and free cash flow of $1.64 billion provides additional cushion. Return on equity of 22.52% demonstrates that Ecolab continues to deploy capital efficiently, and a payout ratio below 37% means there is meaningful room to keep raising the dividend even if earnings growth moderates temporarily.

For long-term dividend investors, Ecolab offers something rare: a dependable stream of income wrapped inside a resilient, global business model that quietly powers industries behind the scenes.

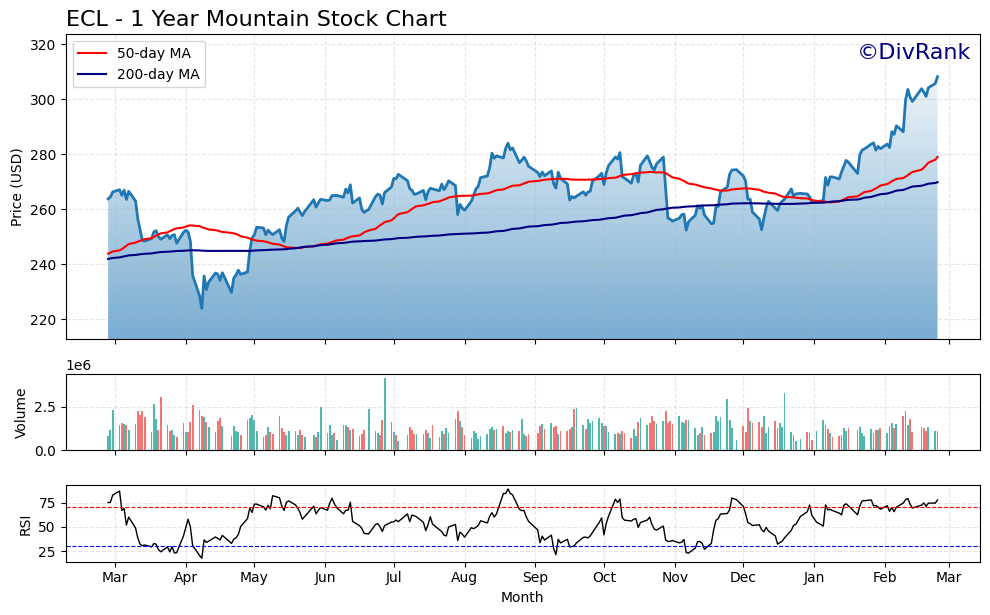

Chart Analysis

Ecolab’s price action over the past year tells a compelling story of sustained recovery and accelerating momentum. Shares bottomed out at $223.93 on the 52-week low before embarking on a rally that has now carried the stock all the way to $308.16, representing a gain of roughly 37.6% from trough to peak. That kind of move in a large-cap industrial compounder reflects genuine re-rating, not just broad market drift, and the fact that ECL is sitting precisely at its 52-week high as of the current reading confirms that buyers have been in full control throughout the climb.

The moving average picture reinforces that bullish read. The 50-day moving average currently sits at $279.02 and the 200-day moving average at $269.81, and ECL is trading meaningfully above both lines. Equally important, the 50-day has crossed above the 200-day, producing the classic golden cross formation that technical analysts treat as a signal of durable intermediate-term trend strength. When price, the near-term average, and the long-term average are all stacked in ascending order, the path of least resistance is clearly upward, and dividend investors can take some comfort in the fact that the technical structure supports the fundamental thesis rather than working against it.

The one area that warrants measured attention is the RSI reading of 77.75, which is firmly in overbought territory. A reading above 70 does not mean a reversal is imminent, but it does indicate that short-term buying enthusiasm has run well ahead of any historical baseline for this stock. Investors who are considering initiating or adding to a position should be aware that periods of consolidation or modest pullbacks are a normal and healthy feature of strong uptrends, and an RSI at this level historically precedes at least some near-term digestion of gains before the next leg higher.

For dividend-focused investors, the technical backdrop is largely constructive. ECL is in a confirmed uptrend with strong moving average support roughly 10% below current levels, which provides a meaningful cushion before any technical damage would occur. The immediate caution is simply one of entry timing: chasing a stock that is simultaneously at a 52-week high and deeply overbought on RSI introduces short-term price risk that patient investors can often avoid by waiting for a modest retracement toward the 50-day moving average. The trend itself is healthy, and the chart structure does nothing to undermine the long-term income thesis.

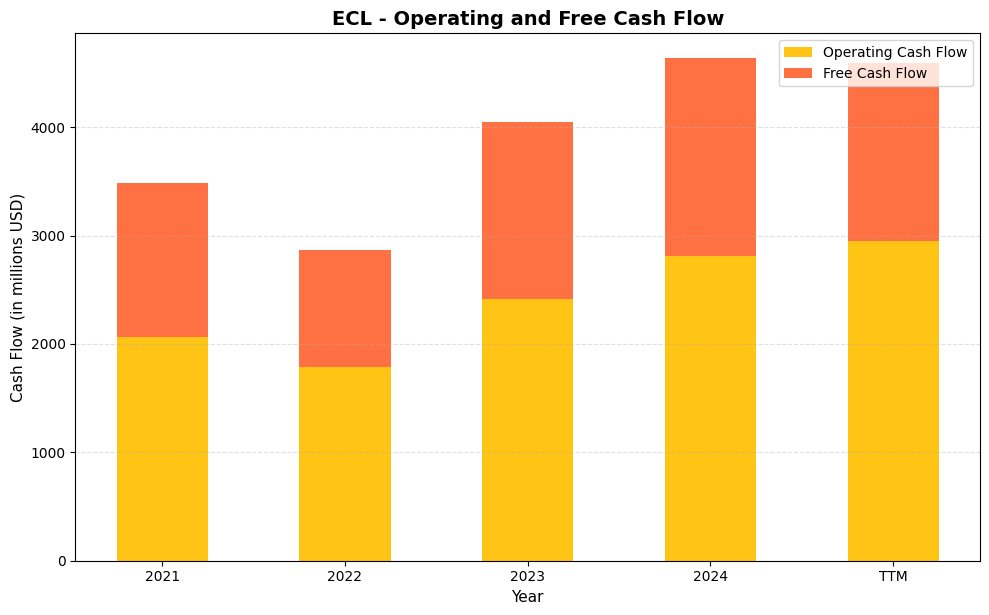

Cash Flow Statement

Ecolab’s cash flow profile has strengthened considerably over the four-year span shown, and the trajectory carries real significance for dividend investors. Operating cash flow climbed from $2,061.9 million in 2021 to $2,813.9 million in 2024, a gain of roughly 36%, before reaching a trailing twelve-month figure of $2,952.6 million. Free cash flow followed a similar arc, recovering sharply from a 2022 dip to $1,075.6 million and pushing to $1,819.4 million in 2024. The 2022 compression was largely a function of elevated working capital needs and input cost pressures tied to the post-pandemic inflationary environment, and the subsequent rebound to record levels through 2023 and 2024 confirms that the underlying business generates durable, repeatable cash. With trailing free cash flow of $1,642.4 million sitting comfortably above the company’s annual dividend obligation, the payout rests on a very solid foundation.

The broader trend across this period reveals a business that has become meaningfully more capital efficient even as it continues to invest in its operations. Capital expenditures, implied by the gap between operating and free cash flow, have remained relatively stable in absolute terms, which means the improvement in free cash flow largely reflects genuine earnings-quality improvement rather than capex suppression. For shareholders, that distinction matters because it suggests ECL is not sacrificing future capacity to make today’s dividend look better. The 2023 and 2024 figures in particular, with free cash flow conversion running above 60% of operating cash flow in both years, point to a company that has regained pricing power and operational leverage after a difficult stretch. Income investors can take reasonable comfort in a free cash flow base that has nearly doubled from trough to peak within just three years.

Analyst Ratings

Analyst sentiment on Ecolab is broadly constructive as shares approach their 52-week high. The current consensus stands at Buy across a group of 21 analysts, with an average 12-month price target of $321.86. That target sits roughly 4.4% above the current price of $308.16, suggesting analysts see continued but measured upside from here rather than a deep discount opportunity. The range of targets spans from a low of $270.00 to a high of $352.00, reflecting a spread of views on how aggressively earnings can grow from current levels given the stock’s elevated valuation.

The price target distribution tells an interesting story. With the stock already near the top of its 52-week range and trading within reach of the mean analyst target, the bull case now rests primarily with the upper end of coverage, where price targets in the $340 to $352 range imply faith in continued margin expansion, strong volume growth across Ecolab’s water and hygiene segments, and the company’s ability to sustain double-digit earnings growth. The $270 floor target likely reflects caution around the premium valuation and the possibility of multiple compression if earnings momentum slows. For income investors already holding the stock, the analyst community’s Buy consensus and positive target range support continued confidence in the position.

Earning Report Summary

Full-Year Results Reflect Sustained Execution

Ecolab closed out its most recent full fiscal year with results that reinforced the company’s standing as one of the more consistent earnings growers in the specialty chemicals space. Revenue reached $16.1 billion, reflecting meaningful top-line scale across its global platform. Net income of $2.08 billion translated to earnings per share of $7.27, representing continued growth from prior periods and comfortably ahead of the dividend obligation. Profit margins of 12.91% reflect a business that has successfully managed input costs while maintaining pricing discipline across its customer base.

Leadership Perspective and Looking Ahead

CEO Christophe Beck has consistently framed Ecolab’s growth story around operational execution, customer retention, and long-term sustainability trends. The company’s focus on water efficiency, infection prevention, and food safety positions it in markets where demand is structurally supported rather than purely cyclical. Beck has pointed to digital tools and data-driven service delivery as key differentiators, areas where Ecolab has been quietly investing for several years and where the returns are beginning to show up in margins and customer stickiness.

With earnings per share of $7.27 for the most recently reported period, the company appears well-positioned to continue growing into the upper end of analyst expectations. The management team has not signaled any retreat from its long-standing commitment to annual dividend increases, and the pace of the most recent raise, at roughly 12%, suggests confidence in the earnings outlook heading into 2026.

Business Segment Performance

Ecolab’s diversified segment structure continues to provide stability across varying demand environments. The Institutional and Specialty segment, serving hotels, restaurants, and food service operations, has benefited from sustained recovery in those end markets. Water treatment remains a core growth driver as industrial customers face increasing regulatory and operational pressure around water use and quality. Life Sciences and Pest Elimination have each contributed solid organic growth, supported by new customer wins and product innovation. The company’s ability to generate consistent performance across segments, rather than relying on any single vertical, is a key element of what makes its earnings and dividend profile so durable.

Management Team

Ecolab’s leadership team has been marked by stability and strategic clarity, with Christophe Beck serving as CEO since 2021. He has been with the company for over a decade and previously held various senior roles, including president and COO, which gives him a deep understanding of the business from the ground up. His background in engineering and operational efficiency has shown up clearly in Ecolab’s consistent push toward productivity improvements, digital transformation, and sustainable innovation.

Beck’s communication style has remained direct and pragmatic. He is not one to overpromise. Instead, he tends to frame goals in terms of operational execution and long-term growth. Under his guidance, the company has doubled down on core areas like water efficiency and infection prevention while pruning non-core operations, such as the prior sale of the surgical solutions business. That type of portfolio discipline tends to appeal to investors looking for steady, compounding growth.

Supporting Beck is a seasoned executive team that blends long-term Ecolab veterans with outside hires who bring fresh thinking. This balance shows in the company’s willingness to evolve its go-to-market strategy and lean more into digital tools, all while maintaining a deeply customer-centric culture.

Valuation and Stock Performance

Ecolab has historically traded at a premium to the broader market, and that premium has expanded meaningfully as shares have climbed toward new highs. At a current price of $308.16 and a P/E ratio of 42.39, the stock is pricing in continued strong earnings growth and a degree of defensiveness that the market consistently rewards in Ecolab’s category. The price-to-book ratio of 13.14 against a book value per share of just $23.46 underscores how much of the company’s value is intangible, residing in its brand, customer relationships, and recurring service model rather than hard assets.

The stock’s 52-week range of $221.62 to $309.15 tells a powerful story. Shares have nearly doubled from their trough to peak over the trailing year, and the current price sits essentially at the top of that range. That kind of performance reflects a genuine rerating of the stock as earnings have grown and margin expansion has become more visible to the market. Beta of 0.99 places ECL roughly in line with the broader market on a volatility basis, which is somewhat lower than its premium valuation might suggest and reflects the defensive nature of its end markets.

The company’s return on equity of 22.52%, combined with a profit margin approaching 13% and operating cash flow above $2.95 billion, provides a fundamental basis for the elevated multiple. While the yield of 0.88% is below the stock’s historical average, the total return potential, combining continued dividend growth with a business trading near all-time highs on genuine earnings momentum, remains compelling for investors with a long time horizon.

Risks and Considerations

Even a strong, diversified business like Ecolab carries meaningful risks that income investors should understand. The most immediate valuation risk is simply how much good news is already reflected in the stock price. At a P/E of 42.39 and a price near its 52-week high, any earnings disappointment, guidance reduction, or macro deterioration could result in a sharp multiple contraction even if the underlying business remains sound. Investors buying at current levels are paying a significant premium for Ecolab’s consistency, and that premium leaves little margin for error.

Currency exposure remains a structural risk given the company’s operations in more than 170 countries. With over $16 billion in annual revenue generated globally, swings in the dollar against major trading currencies can create meaningful headwinds to reported earnings even when local-currency performance is solid. While the company employs hedging strategies, the exposure can never be fully eliminated and has historically been a source of earnings noise.

Input cost sensitivity is another ongoing consideration. Ecolab’s cleaning and chemical solutions businesses rely on raw materials whose prices can shift with commodity cycles, supply chain disruptions, or geopolitical events. The company has demonstrated an ability to offset these pressures through pricing and operational efficiency, but periods of rapid cost inflation can compress margins before pricing actions fully take hold.

Regulatory environments across healthcare, food safety, and water treatment are tightly governed and subject to change. Shifts in environmental policy, chemical safety standards, or trade regulations in key markets could require costly reformulations or operational adjustments. Finally, while Ecolab’s leverage is not alarming by industry standards, carrying meaningful long-term debt in an environment where interest rates remain elevated requires ongoing attention. A sustained tightening of credit conditions or a period of weaker-than-expected cash flow could limit the company’s financial flexibility and complicate its capital allocation priorities.

Final Thoughts

Ecolab continues to stand out as a well-run, globally diversified business that focuses on areas of persistent demand. From clean water to infection prevention, its services are deeply embedded in how businesses operate safely and efficiently. That’s a compelling story for long-term investors who prioritize stability and steady income over short-term thrills.

The management team has proven it can deliver under a range of conditions, including global disruptions, inflationary waves, and shifting regulatory tides. Their steady hand, combined with an agile operational approach, has allowed Ecolab to deliver earnings growth and dividend increases year after year. The December 2025 dividend raise to $0.73 per quarter was a particularly strong signal, lifting the annualized rate to $2.76 and representing one of the more aggressive increases in recent memory for this company.

While the valuation at 42 times earnings is the most significant risk on the table, that has long been the trade-off for a company with Ecolab’s consistency and market position. Risks like currency exposure and raw material costs are real, but they are balanced by a business model that generates nearly $3 billion in annual operating cash flow and serves customers for whom these services are non-negotiable.

With its long runway in water technology, health and hygiene solutions, and sustainability-focused growth, Ecolab looks well-positioned to keep rewarding those who value reliability and compounding over noise and speculation.