Key Takeaways

📈 eBay offers a forward dividend yield of 1.38% with a consistent growth track record, raising its quarterly dividend to $0.29 per share in early 2025 and maintaining a conservative 25% payout ratio.

💰 The company generated $1.96 billion in operating cash flow and $741 million in free cash flow over the trailing twelve months, with net income of nearly $2 billion supporting the dividend comfortably.

🧐 Analyst consensus sits at Hold with a mean price target of $98.57 across 30 analysts, though the current price of $85.30 sits roughly 13% below that average, suggesting limited near-term downside in analyst expectations.

📊 Full-year revenue reached $11.1 billion with a profit margin of 18.3% and EPS of $4.51, reflecting a mature but steadily profitable marketplace business executing on its niche vertical strategy.

Updated 2/25/26

eBay has continued to evolve as a disciplined e-commerce platform with a strong emphasis on niche verticals, consistent cash generation, and shareholder-friendly capital allocation. The stock has pulled back from its 52-week high of $101.15 and now trades at $85.30, creating what some income investors may view as a more attractive entry point relative to both the analyst consensus target and the company’s underlying earnings power. With growing dividends, active buybacks, and a sub-30% payout ratio, eBay remains a compelling choice for investors who prioritize dividend safety and incremental income growth.

The management team has settled into its configuration following leadership transitions completed in prior periods, and the strategic direction remains focused on AI-powered platform tools, international expansion, and category-specific enhancements. Revenue has scaled to $11.1 billion on a trailing basis, and with net income approaching $2 billion, the financial profile supports continued capital returns without stretching the balance sheet.

Recent Events

eBay has been active on several fronts heading into early 2026. The company’s AI-driven listing and discovery tools have continued to gain traction on the platform, with management pointing to measurable improvements in seller conversion rates and buyer engagement. These enhancements, first introduced in earnest during 2024, have become a core part of eBay’s pitch to both new and returning users as it works to differentiate itself from generalist e-commerce rivals.

On the international side, eBay’s Authenticity Guarantee program has expanded further into key markets, reinforcing the platform’s credibility in high-value categories like sneakers, luxury handbags, and collectibles. The program has been a meaningful driver of gross merchandise volume in verticals where trust is a prerequisite for buyer participation. eBay Motors has also remained a focus area, with the Caramel acquisition from 2025 continuing to be integrated into the vehicle transaction workflow.

The stock has experienced notable volatility over the past year, trading in a wide range between $58.71 and $101.15. After reaching triple digits earlier in the period, shares have retreated to the mid-$80s, which has reignited conversations among income investors about whether the current price represents a better risk-reward setup than the highs suggested. With a beta of 1.38, eBay trades with more sensitivity to broader market swings than a typical defensive income name, and that dynamic has been visible in the price action.

Short interest stands at roughly 12.3 million shares, a figure that reflects some skepticism among market participants but is not at a level that would signal acute concern. The broader e-commerce environment remains competitive, and macroeconomic uncertainty around consumer discretionary spending continues to be a factor that analysts are weighing in their outlooks.

Key Dividend Metrics

📈 Forward Dividend Yield: 1.38%

💰 Forward Annual Dividend Rate: $1.24

📅 Most Recent Dividend Payment: $0.29 per share (November 28, 2025)

🔁 Most Recent Dividend Increase: To $0.29 from $0.27, effective March 2025

📊 Payout Ratio: 25.28%

🕰️ Dividend Growth Since 2019: Consecutive annual increases every year

🔥 Most Recent Dividend Growth Step: $0.27 to $0.29 per quarter, approximately 7.4%

🔐 Free Cash Flow: $741 million trailing twelve months

💼 Return on Equity: 40.85%

Dividend Overview

eBay’s dividend yield of 1.38% is not going to turn heads on a yield-screening tool, but the quality and safety behind that payment tell a more interesting story for income investors focused on the long game. The company is paying out just 25% of earnings as dividends, which is among the more conservative payout ratios in the internet retail space. That restraint leaves substantial room for continued dividend growth without putting any pressure on the balance sheet or cash flow profile.

The annual dividend rate of $1.24 per share reflects the most recent quarterly payment of $0.29, which was raised from $0.27 earlier in 2025. That increase, roughly 7.4%, continues eBay’s pattern of meaningful annual hikes rather than token adjustments. Net income came in at nearly $2 billion on a trailing basis, and even with free cash flow at $741 million due to capital allocation decisions, the dividend payout itself is well within reach on both an earnings and cash flow basis.

eBay has also continued its buyback program, which incrementally reduces the share count and amplifies earnings per share over time. For dividend reinvestment investors, that combination of growing per-share dividends and a declining share base creates a compounding dynamic that the headline yield alone does not fully capture.

Dividend Growth and Safety

eBay’s dividend history since initiating the payment in 2019 has been one of uninterrupted annual increases, and 2025 maintained that streak with the step up to $0.29 per quarter. Going back through the recent payment history, the progression is clear: $0.25 per quarter throughout 2023, $0.27 per quarter throughout 2024, and $0.29 per quarter throughout 2025. That steady cadence of 7 to 8 percent annual increases reflects a management team that treats the dividend as a serious and growing commitment rather than a secondary consideration.

The safety profile of the dividend is strong. A payout ratio of 25% against earnings of $4.51 per share means the company would need to experience a dramatic and sustained earnings decline before the dividend came under any real pressure. Operating cash flow of $1.96 billion on a trailing basis provides additional confirmation that the business generates more than enough internal cash to cover the dividend many times over, even after accounting for capital expenditures and other obligations.

Return on equity of 40.85% is a standout figure that speaks to the underlying quality of eBay’s asset-light marketplace model. When a business earns at that rate on its equity base while paying out only a quarter of earnings, the compounding math works in shareholders’ favor. The dividend is not being supported by financial engineering or one-time items. It is the output of a genuinely profitable business with consistent cash generation. For income investors with a multi-year horizon, that combination of low payout ratio, high returns on equity, and a demonstrated willingness to raise the dividend annually is exactly the profile worth owning.

Chart Analysis

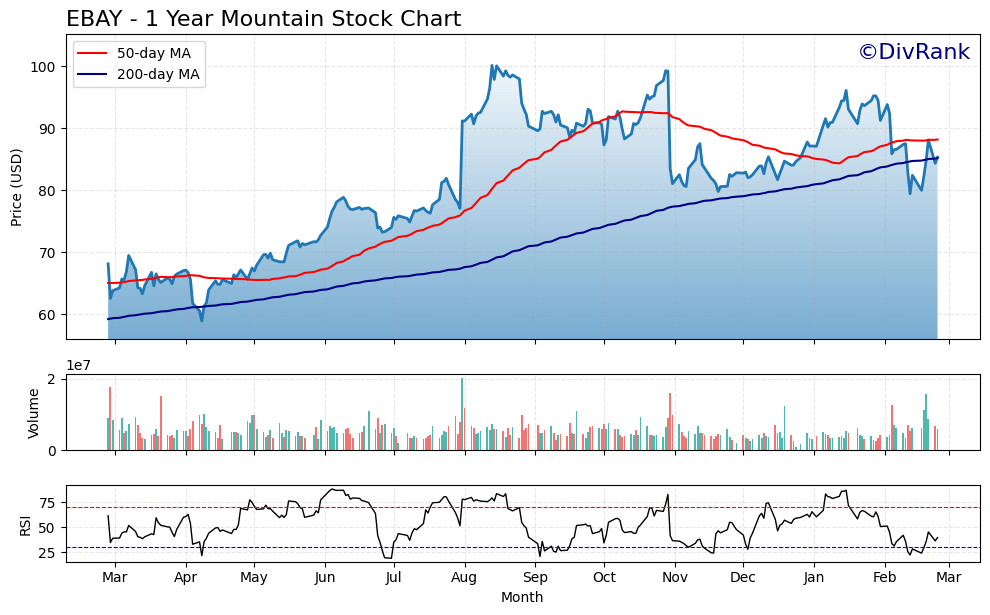

eBay’s chart tells a story of genuine recovery over the past twelve months, with the stock climbing from a 52-week low of $58.89 to its current price of $85.30, a gain of nearly 45% from the trough. That low marked a point of maximum pessimism, and the subsequent rally carried shares all the way to $100.10 earlier in the year before sellers reasserted control. The pullback from that peak, now sitting at roughly 14.8% off the high, has brought the stock back toward a more reasonable entry zone, and the broader trend still looks constructive when viewed across the full twelve-month window rather than just the recent softness.

The moving average picture offers a nuanced read for patient investors. The 200-day moving average sits at $85.16, which is almost exactly where shares are trading right now, meaning the stock is effectively sitting on this long-term trend line and testing it as support. That level has real significance. The 50-day moving average at $88.15 remains above the current price, so eBay is technically in a short-term downtrend relative to that shorter timeframe measure. Importantly, the 50-day remains above the 200-day, which confirms a golden cross formation, a broadly bullish structural signal that reflects the strength of the prior uptrend and suggests the long-term momentum backdrop has not fully deteriorated.

The RSI reading of 39.75 places eBay in oversold territory, approaching but not yet breaching the traditional 30-level threshold that often precedes mean-reversion bounces. This kind of momentum compression, where price has been sold down to a degree that reflects more fear than fundamental deterioration, can be an interesting setup. It does not guarantee an immediate reversal, but it does suggest that much of the near-term selling pressure may already be priced in. Dividend investors who have been waiting for a better entry point than the $100 peak are now looking at a materially different risk-reward setup than existed a few months ago.

For income-focused shareholders, the technical picture reads as cautiously constructive. The stock is holding near critical long-term support at the 200-day moving average, the golden cross remains intact, and the RSI suggests the recent pullback is more of an exhaustion signal than the beginning of a new downtrend. A confirmed hold above the $85 area would reinforce the bullish structure, while a breakdown below it would argue for patience before adding exposure. At current levels, the chart is offering dividend investors a chance to revisit the name at prices roughly 15% below the yearly high, with a technical foundation that has not yet been broken.

Cash Flow Statement

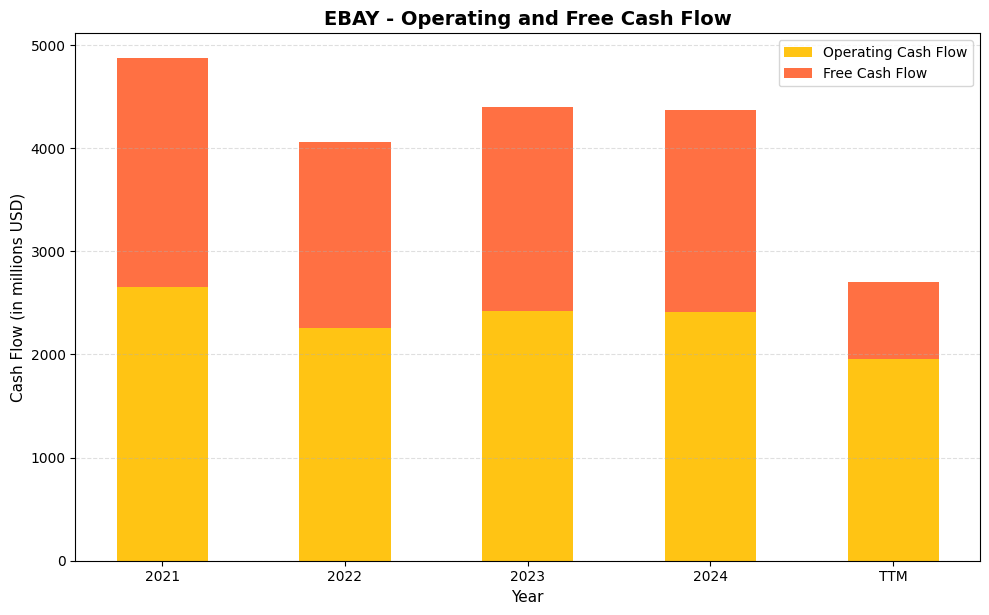

eBay’s operating cash flow has held in a remarkably tight band over the past four fiscal years, ranging from $2,254.0M in 2022 to $2,657.0M in 2021, and settling at $2,414.0M in 2024. That consistency is exactly what dividend investors want to see underneath a payout program, because it signals that the business generates real cash regardless of short-term earnings noise. Free cash flow has tracked closely, coming in at $1,956.0M in 2024 versus $1,970.0M in 2023, which means capital expenditures are modest and disciplined. Against an annual dividend outlay that has grown steadily alongside the company’s buyback program, that level of free cash flow provides a comfortable coverage cushion and leaves room for continued payout increases without straining the balance sheet.

The TTM figures introduce a wrinkle worth examining carefully. Operating cash flow has dipped to $1,959.0M on a trailing basis, which still looks acceptable in isolation, but free cash flow has dropped sharply to $741.1M, a meaningful departure from the $1,800.0M to $2,200.0M range the company posted in each of the prior four full years. That compression suggests either a temporary spike in capital spending, a working capital timing shift, or both, and investors should watch whether the next full-year print normalizes back toward the historical range. eBay’s longer-term record does demonstrate solid capital efficiency, converting a high percentage of operating cash into freely distributable cash in most periods, and the underlying marketplace model carries low physical asset intensity. As long as the TTM free cash flow dip proves transitory, the dividend remains on sound footing, though the divergence between operating and free cash flow in the most recent trailing period is a data point that warrants monitoring in coming quarters.

Analyst Ratings

The analyst community has settled into a Hold consensus on eBay across 30 covering analysts, with a mean price target of $98.57 that sits roughly 15.6% above the current price of $85.30. That gap between the consensus target and the trading price is worth paying attention to, as it suggests analysts broadly see value above current levels even if the collective view is not bullish enough to warrant a Buy rating. The range of expectations is wide, with the low-end target at $60.00 and the high-end reaching $122.00, reflecting genuine disagreement about eBay’s trajectory in a competitive e-commerce landscape.

The low-end target of $60.00 represents a meaningful discount to current prices and likely reflects analysts who are most concerned about slowing gross merchandise volume growth, competitive pressure from Amazon and specialized vertical platforms, and macroeconomic sensitivity given eBay’s discretionary-heavy product mix. The high-end target of $122.00 reflects a more optimistic view on AI-driven platform improvements, international expansion, and the company’s ability to grow earnings per share through a combination of margin discipline and buybacks.

With no specific analyst actions available in the current data, the consensus Hold rating and the $98.57 mean target are the most useful anchors for evaluating where the Street stands. For income investors, the more relevant observation is that at $85.30, eBay is trading below what the average analyst considers fair value, which provides a modest margin of safety even in the context of a mixed fundamental outlook. The 25% payout ratio and consistent dividend growth record give income-focused investors a reason to hold through any near-term volatility while collecting and compounding a growing payment.

Earning Report Summary

Full-Year Performance Reflects a Mature, Profitable Marketplace

eBay’s trailing twelve-month financials through the most recently available reporting period show a business that has reached meaningful scale while maintaining the profitability that defines its marketplace model. Revenue came in at $11.1 billion, and net income reached $1.996 billion, translating to a profit margin of 18.3% and earnings per share of $4.51. These are not the growth metrics of an early-stage platform, but they reflect a company that has carved out a durable and highly profitable niche in global e-commerce.

Operating cash flow of $1.96 billion confirms that the earnings figures are supported by real cash generation rather than accounting adjustments. The spread between revenue and net income, combined with a return on equity north of 40%, tells investors that eBay’s asset-light model continues to work well. The company does not require heavy physical infrastructure to serve its marketplace participants, and that structural advantage shows up consistently in the margin profile.

Platform Strategy and Capital Allocation

Management has continued to execute on the strategy articulated in prior periods, centering on AI-enhanced listing and discovery tools, category-specific trust programs like Authenticity Guarantee, and vertical expansion through initiatives like eBay Motors. The integration of Caramel into the vehicle transaction experience represents a concrete example of eBay deploying capital toward defensible competitive advantages rather than chasing broad market share.

On capital allocation, eBay has remained consistent in its approach of combining buybacks with dividend growth. The dividend was raised again in early 2025 to $0.29 per quarter, and the buyback program has continued to reduce the share count, which amplifies per-share metrics over time. With EPS at $4.51 and the annual dividend at $1.24, the coverage ratio is strong and leaves ample room for another increase in early 2026 if the business continues to perform at current levels.

Looking Ahead

The key variables for eBay heading through 2026 are gross merchandise volume trends, the pace of international expansion, and the degree to which AI-driven tools translate into measurable gains in buyer and seller activity. Management has consistently framed the AI investment as a long-cycle initiative rather than a near-term catalyst, which sets realistic expectations but also means the payoff horizon requires patience. For income investors, the more immediate consideration is whether the earnings and cash flow base remains stable enough to support another annual dividend increase, and on that question, the current financial profile provides a confident answer.

Management Team

eBay’s management team has stabilized following the leadership transitions completed in 2025. Peggy Alford assumed the Chief Financial Officer role after Steve Priest’s departure, bringing with her a background that includes senior financial leadership at PayPal. Her tenure so far has been characterized by continued discipline on capital allocation and a focus on integrating financial planning more tightly with the company’s technology and product initiatives.

CEO Jamie Iannone has maintained the strategic direction he set when he joined the company, with AI platform tools, category verticalization, and international expansion remaining the three pillars of the operational agenda. Jordan Sweetnam continues in his role overseeing Global Markets and Product as Chief Commercial Officer, and Mazen Rawashdeh leads engineering as Chief Technology Officer. The current configuration reflects a structure designed to reduce the distance between commercial strategy and technology execution, which is appropriate for a marketplace business where the product experience and the revenue model are inseparable. The team has now had enough time together to move from transition to execution, and the financial results suggest that coordination is functioning as intended.

Valuation and Stock Performance

eBay shares are trading at $85.30 as of February 25, 2026, which puts the stock at a price-to-earnings ratio of 18.91 based on trailing EPS of $4.51. That is a reasonable multiple for a business with the profitability profile eBay has demonstrated, particularly when the 25% payout ratio and 40.85% return on equity are factored in alongside the earnings figure. The stock reached a 52-week high of $101.15 before pulling back to its current level, a decline of roughly 16% from peak that has brought the valuation back to a more grounded range.

The mean analyst price target of $98.57 implies approximately 15.6% upside from current levels, and the price-to-book ratio of 8.30 against a book value per share of $10.28 reflects the asset-light nature of the marketplace model where intrinsic value is not well captured by balance sheet metrics alone. For income investors, the current entry point offers a 1.38% yield on a dividend that has grown every year since 2019, with a payout ratio that leaves substantial runway for continued increases. Market cap stands at roughly $39 billion, placing eBay among the larger mid-to-large cap names in the internet retail category. The combination of below-peak pricing, a conservative payout ratio, and a demonstrated dividend growth track record makes the current setup worth consideration for income-oriented portfolios.

Risks and Considerations

The most persistent risk for eBay is its exposure to discretionary consumer spending. A meaningful portion of what trades on the platform, including collectibles, refurbished electronics, fashion, and vehicles, represents purchases that consumers can delay or forgo when economic conditions tighten. eBay has navigated past slowdowns with reasonable resilience, but with a beta of 1.38, the stock itself tends to amplify broader market moves, which can create volatility even when the underlying business holds steady.

Competition from Amazon and from specialized vertical platforms remains a structural challenge. Amazon’s logistics infrastructure and Prime ecosystem give it a significant advantage in new goods, while category-specific platforms for sneakers, luxury goods, and collectibles continue to attract buyers and sellers who might otherwise transact on eBay. The company’s response has been to deepen its focus on trust mechanisms like Authenticity Guarantee and to improve the platform experience through AI tools, but these efforts require consistent investment and face execution risk if the pace of platform improvement slows.

The company’s debt level, while manageable given its cash flow generation, represents an ongoing consideration in a higher interest rate environment. The price-to-book ratio of 8.30 is elevated relative to tangible assets, meaning the stock’s valuation rests heavily on continued earnings power rather than hard asset backing. If growth stalls or margins compress materially, the multiple could compress in ways that affect total return even if the dividend itself remains secure. Investors should also note that free cash flow of $741 million, while sufficient to cover the dividend, is meaningfully lower than operating cash flow due to capital expenditure levels, and any acceleration in capital spending could further narrow that coverage in the near term.

Final Thoughts

eBay is not a high-octane growth story, and it does not need to be. What it offers income investors is a combination of consistent dividend growth, a conservative payout ratio, strong earnings power, and a management team that has demonstrated discipline in returning capital to shareholders year after year. The dividend has been raised every year since 2019, the most recent increase bringing the quarterly payment to $0.29, and with a payout ratio of just 25%, there is no fundamental reason that streak cannot continue into 2026 and beyond.

The current price of $85.30 represents a notable discount to both the 52-week high and the analyst consensus target, which creates a more attractive entry point for new investors than existed when the stock was trading above $100. The risks around consumer spending sensitivity, competitive pressure, and valuation multiple are real and deserve attention, but they are also well-understood and largely priced into the current consensus. For investors who appreciate a growing income stream backed by a genuinely profitable business, eBay at current levels offers a sensible combination of yield, safety, and long-term compounding potential.