Key Takeaways

📈 Eaton’s dividend yield currently stands at 1.15%, with the quarterly dividend raised to $1.04 per share in early 2025, continuing the company’s long track record of annual increases.

💵 Eaton generated $27.45 billion in revenue over the trailing twelve months, with net income reaching $4.09 billion and EPS of $10.45, reflecting continued earnings growth across its core industrial segments.

📊 Analysts maintain a buy consensus on ETN, with a mean price target of $407.52 across 26 analysts, suggesting moderate upside from the current price of $374.56.

📋 Eaton’s payout ratio of 39.81% and return on equity of 21.53% underscore the financial discipline that has made its dividend program one of the more reliable in the industrials sector.

Updated 2/25/26

Eaton Corporation (ETN) is a global leader in intelligent power management with operations spanning electrical, aerospace, and mechanical sectors. The company has steadily reshaped its business over the past decade, focusing on high-growth, high-margin markets tied to electrification, digital infrastructure, and energy efficiency. With a solid foundation in industrial systems and a forward-facing strategy, Eaton continues to deliver consistent earnings growth and increasing dividends.

The company’s performance is backed by experienced leadership, disciplined capital allocation, and a long-term approach to innovation and operational efficiency. Recent results have reflected strong demand across core segments, a record backlog of infrastructure projects, and growing momentum in data center investments. Eaton’s valuation reflects its improved fundamentals, while its dividend track record and reliable cash generation make it a compelling option for income-focused strategies with a growth orientation.

🔑 Key Dividend Metrics (as of February 25, 2026)

📈 Forward Dividend Yield: 1.15%

💵 Annual Dividend Rate: $4.16 per share

📆 Last Dividend Payment: $1.04 per share

💰 Payout Ratio: 39.81%

📊 5-Year Average Yield: 1.88%

📈 5-Year Dividend Growth: Solid and steady

🧾 Dividend Safety Score: High

Recent Events

Eaton has remained an active presence in industrial and infrastructure conversations heading into early 2026, as the broader push toward grid modernization, data center buildout, and electrification of commercial and industrial facilities continues to generate sustained demand for the company’s power management solutions. The company’s Electrical Americas segment has been a consistent focal point for investors, given the scale of North American infrastructure spending programs that continue to funnel work toward Eaton’s product lines and project services.

The stock has pulled back from its 52-week high of $408.45 and currently trades at $374.56, sitting comfortably above its 52-week low of $231.85. That wide range reflects the volatility that industrials experienced over the past year amid shifting interest rate expectations and concerns about the pace of large-scale infrastructure project execution. At current levels, ETN has recovered meaningfully and trades in line with analyst expectations, with the consensus price target of $407.52 suggesting the stock still has room to reclaim its recent highs.

Eaton raised its quarterly dividend to $1.04 per share in March 2025, up from $0.94 in the prior year, representing an increase of approximately 10.6%. That raise was consistent with the company’s pattern of annual dividend growth and was supported by the continued expansion of net income, which reached $4.09 billion over the trailing twelve months. With 26 analysts currently covering the stock at a buy consensus and a beta of 1.18, investor attention on ETN remains elevated as infrastructure spending themes stay prominent in 2026.

Dividend Overview

For investors focused on income, Eaton’s yield of 1.15% may appear modest at first glance, but the yield compression is largely a function of price appreciation rather than any slowdown in dividend growth. The company now pays $4.16 annually per share on a quarterly cadence of $1.04, and that figure has climbed steadily over the past several years. The quarterly payment was $0.81 in late 2022, $0.86 through most of 2023, $0.94 throughout 2024, and stepped up again to $1.04 in early 2025, a sequence that illustrates consistent, uninterrupted growth.

The payout ratio of 39.81% is conservative relative to earnings per share of $10.45, meaning the company retains the majority of its profits for reinvestment and capital flexibility. That cushion is meaningful because it signals the dividend is not only well-covered today but has room to grow further without requiring earnings to dramatically outperform expectations. Eaton’s profit margin of 14.89% and return on equity of 21.53% provide the underlying earnings quality to sustain that trajectory.

Eaton’s current yield sits below its five-year average of 1.88%, largely because the share price has appreciated considerably over that period. Investors entering the stock today are accepting a lower starting yield in exchange for the expectation that both the dividend and the share price will continue to grow from here. For those with a long time horizon, that trade-off has historically proven worthwhile with ETN.

Dividend Growth and Safety

Where Eaton truly distinguishes itself is in the reliability and consistency of its dividend growth. The company has raised its dividend every year, and the pace of those increases has accelerated as earnings have expanded. Moving from $0.86 per quarter in 2023 to $0.94 in 2024 and then to $1.04 in 2025 represents a growth rate of roughly 10% annually, a pace that meaningfully outpaces inflation and rewards long-term holders.

The safety of that dividend is anchored in the company’s financial discipline. A payout ratio just under 40% means that even a meaningful decline in earnings would leave the dividend well-supported. Return on equity of 21.53% and return on assets of 8.28% reflect a business that generates strong returns on the capital it deploys, which is the foundation for sustaining long-term income growth. Net income of $4.09 billion against an annual dividend obligation that represents a fraction of that figure reinforces the low-risk profile of the payout.

Eaton’s management team has not overextended the company in pursuit of short-term earnings. Their focus on electrification, intelligent power management, and grid infrastructure positions the business in markets where long-term demand remains structurally supported. That strategic clarity reduces the likelihood of a sudden pivot that might disrupt dividend growth, and it creates a self-reinforcing cycle where strong project pipelines support earnings, which in turn support continued dividend increases.

While the yield is lower than what some pure income investors prefer, the combination of a conservative payout ratio, strong earnings quality, and a demonstrated commitment to annual increases makes Eaton’s dividend one of the more dependable in the industrials universe.

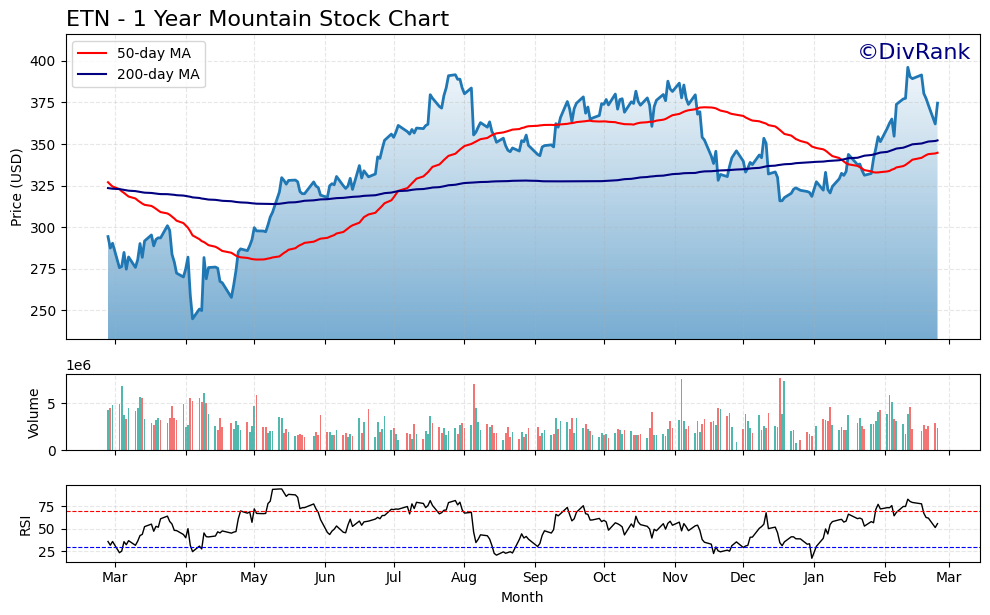

Chart Analysis

Eaton’s price action over the past year tells a story of dramatic recovery and renewed momentum. The stock carved out a 52-week low of $244.95 before staging an impressive rally that has carried shares to $374.56 at the time of writing, a gain of roughly 53% off that trough. That kind of range, spanning nearly $151 from low to high, reflects how significantly sentiment shifted as industrial and electrification demand narratives reasserted themselves. The current price sits just 5.4% below the 52-week high of $396.09, which signals that the recovery is mature and that the stock is now navigating the upper end of its recent trading band rather than chasing an early-stage breakout.

The moving average picture is mixed but leans constructive in the near term. ETN trades above both its 50-day moving average of $344.75 and its 200-day moving average of $352.17, which confirms that price momentum is positive on both intermediate and longer-term timeframes. However, the 50-day moving average currently sits below the 200-day moving average, a configuration technically classified as a death cross. That cross reflects the period earlier in the year when the stock was under meaningful pressure, and while the label sounds alarming, the more relevant observation for dividend investors is that price itself has already reclaimed both averages convincingly. The averages will likely resolve into a golden cross in the coming weeks if the current price level holds, which would remove that residual bearish technical overhang.

The RSI reading of 55.71 is one of the more reassuring data points in this setup. It places ETN in a neutral-to-constructive zone, well clear of oversold territory and equally clear of the overbought readings above 70 that tend to precede short-term pullbacks. That balance suggests the rally from the lows was not simply a panic-driven snapback but has been absorbed gradually enough that momentum is not stretched. Investors entering a position at current levels are not chasing an exhausted move, which matters when the investment case is built around collecting and compounding dividends over years rather than trading short-term swings.

For dividend investors, the chart presents a stock in recovery mode that has already done most of its heavy lifting. The proximity to the 52-week high means some near-term resistance is a realistic possibility, and patient investors may find opportunities to build positions on any modest pullback toward the $352 to $355 range where the 200-day moving average provides a logical support zone. The combination of above-average price recovery, neutral momentum readings, and improving moving average alignment suggests the technical backdrop is supportive of the long-term income thesis, even if the most aggressive price gains from the cycle low are likely behind it.

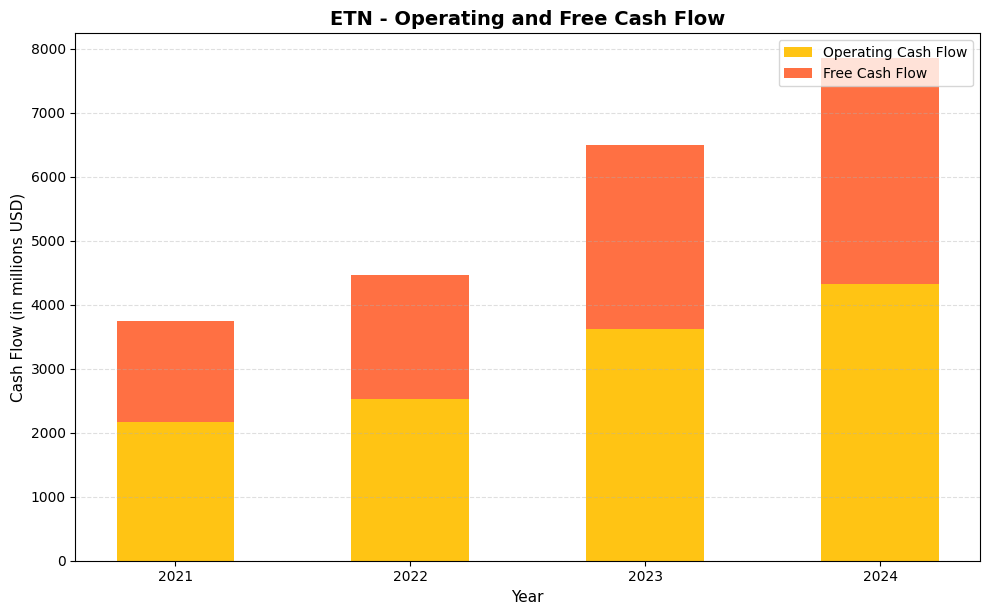

Cash Flow Statement

Eaton’s cash generation profile has transformed meaningfully over the past four years, and the numbers make a compelling case for dividend sustainability. Operating cash flow climbed from $2,163.0 million in 2021 to $4,327.0 million in 2024, a near-doubling in just three years. Free cash flow followed an equally impressive trajectory, rising from $1,588.0 million in 2021 to $3,519.0 million in 2024. That $3,519.0 million in free cash flow dwarfs Eaton’s annual dividend obligation by a comfortable margin, which means the company is retaining substantial cash after paying shareholders, leaving plenty of room for future dividend increases without straining the balance sheet.

The trend across this four-year window reveals more than just growth — it reflects genuine capital efficiency improvements. The spread between operating cash flow and free cash flow, which captures capital expenditure intensity, has remained relatively consistent even as absolute figures surged, suggesting Eaton is scaling earnings power without a proportional increase in reinvestment requirements. Free cash flow conversion from operating cash flow held near 73% in both 2021 and 2024, meaning the business is not becoming more capital-hungry as it grows. For dividend investors, a company that can nearly double its free cash flow generation over three years while maintaining that conversion ratio is precisely the kind of compounder that supports not just dividend safety today, but accelerating dividend growth well into the future.

Analyst Ratings

Eaton carries a buy consensus among the 26 analysts currently covering the stock, reflecting broad confidence in the company’s positioning within power management and industrial electrification. The mean price target of $407.52 sits above the current price of $374.56, implying upside of roughly 8.8% from current levels. The range of targets is wide, spanning from a low of $321.00 to a high of $545.00, which reflects differences in how aggressively analysts are modeling the pace of data center and grid infrastructure spending over the next several years.

The $407.52 mean target suggests that the analyst community collectively views Eaton as fairly valued to modestly undervalued at current prices, rather than pricing in an extreme premium or discount. The elevated high-end target of $545.00 likely reflects scenarios where large-scale electrification spending accelerates beyond current expectations and Eaton captures a disproportionate share of that demand through its Electrical Americas and Global segments.

Concerns that emerged in early 2025 around AI-related power demand assumptions, particularly following the emergence of more energy-efficient AI architectures, have not materially shifted the overall analyst stance. The buy consensus has held, and the mean price target remains above current trading levels. With short interest at approximately 7.5 million shares, the stock does not face significant technical headwinds from bearish positioning. Overall, the analyst community remains constructively aligned with Eaton’s long-term growth narrative, with price targets pointing to continued appreciation from current levels.

Earnings Report Summary

Solid Start to the Year

Eaton’s most recent full-year results demonstrated the continued strength of its core industrial and electrical operations. The company reported revenue of $27.45 billion and net income of $4.09 billion, with earnings per share of $10.45. Profit margins of 14.89% reflect disciplined cost management alongside strong revenue growth, and the return on equity of 21.53% confirms that the business is generating meaningful returns on the capital it employs. These metrics collectively illustrate a company executing at a high level across its segments.

The Electrical Americas segment has remained the primary growth engine, with demand driven by data center construction, utility-scale grid upgrades, and the ongoing electrification of commercial and industrial facilities. The Aerospace segment has continued to contribute steadily, benefiting from both commercial aviation recovery and defense-related demand. Eaton’s ability to expand margins alongside top-line growth reflects favorably on its operational discipline and pricing strategy in a competitive environment.

Leadership’s Take on What’s Ahead

Craig Arnold and his leadership team have maintained a consistent message around disciplined execution and long-term positioning in high-demand markets. The company’s pipeline of North American megaprojects, which management has previously described as representing a multi-trillion-dollar addressable opportunity, continues to provide a long runway for revenue growth. Only a fraction of those projects have moved to active construction phases, meaning the backlog supports confidence in future revenue even as near-term quarter-to-quarter results may vary with project timing.

Management has emphasized staying ahead of the technology curve in power management and grid modernization, investing in areas where Eaton can maintain a leadership position and generate consistent returns. The tone from leadership has remained measured but optimistic, with the focus firmly on sustainable earnings growth and shareholder value creation over multi-year horizons rather than short-term maximization. That approach has consistently resonated with investors and analysts alike, and there is little indication the strategy is shifting as the company moves through 2026.

Management Team

Eaton’s leadership has guided the company through meaningful transformation over the years. Craig Arnold, who serves as Chairman and CEO, has been a steady hand at the wheel. Under his leadership, Eaton has leaned into sectors that offer stronger growth and better margins, shifting focus toward electrification, intelligent power systems, and digital infrastructure. These changes haven’t just improved the numbers; they’ve reshaped how the company operates and how investors view it.

Arnold’s approach emphasizes disciplined execution and long-term planning over short-term hype. He is backed by a management team with deep industrial experience and clear alignment around Eaton’s priorities. Their strategy is methodical, with an eye on delivering consistent results while navigating the transition to more sustainable and tech-driven markets. Eaton’s board adds another layer of stability, made up of leaders with diverse expertise across finance, global manufacturing, and operations. Together, this group has built a framework that prioritizes long-term resilience and shareholder value, and the consistency of that approach is visible in both the financial results and the dividend growth record.

Valuation and Stock Performance

ETN has had a dynamic twelve months, trading in a range from $231.85 to $408.45. The stock currently sits at $374.56, well above its annual low and within striking distance of its high, reflecting the recovery in investor confidence after a period of broader industrial sector volatility. The 52-week low suggests the stock experienced meaningful selling pressure at some point during the year, likely tied to macro concerns around interest rates and the pace of large infrastructure project execution, but the subsequent recovery to current levels indicates those concerns have largely been absorbed.

Valuation-wise, Eaton trades at a P/E ratio of 35.84 and a price-to-book of 7.49, both of which reflect a premium to traditional industrial peers. That premium is earned through the company’s exposure to secular growth themes in electrification and power infrastructure, its consistent margin expansion, and the quality of its earnings stream. A book value per share of $50.04 against a share price of $374.56 speaks to the market’s confidence in Eaton’s ability to compound returns well above its asset base. Return on equity of 21.53% justifies a meaningful price-to-book premium, as the company is generating strong returns on the equity it holds.

The beta of 1.18 suggests slightly above-average market sensitivity, which is reasonable for a company with meaningful exposure to industrial capital spending cycles. Over the long term, shareholders have benefited from both price appreciation and a growing dividend, and with the analyst consensus pointing to a mean target of $407.52, the stock continues to offer what appears to be a reasonable risk-reward profile for investors with a multi-year perspective.

Risks and Considerations

Slowing growth in core end markets such as construction, utilities, and commercial real estate could lead to project delays and softer equipment demand. Even with a healthy backlog supporting near-term visibility, extended project timelines or reduced capital investment from large customers could create choppiness in quarterly results. The company’s strong backlog provides insulation, but it is not a complete buffer against a prolonged period of reduced infrastructure spending.

Cost inflation and supply chain pressures remain latent risks. Eaton has navigated these challenges effectively in recent cycles, but margin pressure can reemerge if input costs rise faster than the company’s ability to pass them through to customers. Pricing power is real but has limits, particularly if demand softens in any of the major end markets the company serves.

Eaton’s strategic concentration in electrification and digital power infrastructure means its long-term performance is closely tied to the pace and scale of the energy transition and AI-driven infrastructure buildout. These are large, durable trends, but they are also subject to shifts in technology direction, government policy, and capital allocation decisions by large hyperscale customers. The emergence of more power-efficient AI architectures, for example, could moderate some of the demand assumptions that support higher price targets in the analyst community.

Global operations add currency and geopolitical complexity to the financial picture. Eaton generates revenue across multiple regions, and fluctuations in foreign exchange rates or disruptions in international trade policy can affect reported results in ways that are largely outside management’s control. At a P/E of 35.84, the valuation leaves limited margin for error if earnings growth were to disappoint relative to current expectations.

Final Thoughts

Eaton stands out as a company that has done the hard work of evolving its business for a changing world. Its focus on electrification, smart energy solutions, and infrastructure positions it in front of long-term demand trends, and the financial results continue to reflect that positioning. Revenue of $27.45 billion, net income of $4.09 billion, and EPS of $10.45 represent a business firing on most cylinders, and the consistent pattern of dividend increases, most recently to $1.04 per quarter, reinforces the company’s commitment to returning capital to shareholders in a sustainable and growing manner.

The leadership team continues to drive the company with discipline rather than flash. That measured approach has earned trust, and it shows up in the premium valuation the market is willing to assign to ETN. A buy consensus from 26 analysts and a mean price target of $407.52 suggest the investment community sees the current price as a reasonable entry point with upside remaining.

While risks around valuation, end-market cyclicality, and technology substitution are real and worth monitoring, Eaton brings the kind of balance that is difficult to ignore. It is building for the future while delivering in the present, with a clear strategic vision and a proven track record of execution. That combination of long-term positioning, earnings quality, and a growing dividend makes it a name that continues to earn its place in dividend growth portfolios.