Key Takeaways

💸 DTE’s dividend yield is currently 3.04% with a sustained history of annual increases and a healthy 63.09% payout ratio, reflecting continued financial discipline.

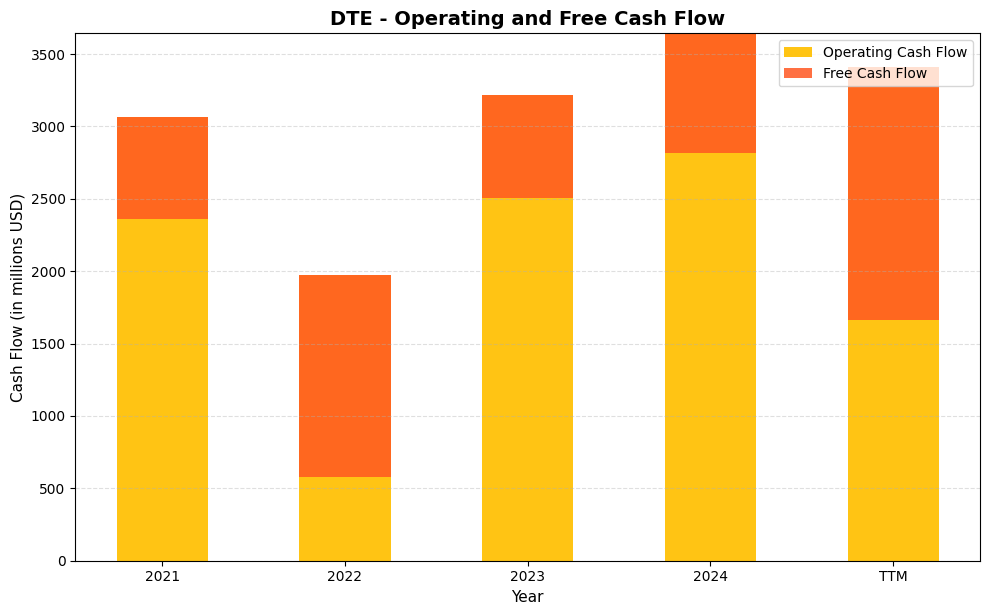

💰 Operating cash flow reached $3.41 billion over the trailing twelve months, comfortably covering dividend obligations even as capital investment keeps free cash flow negative.

📊 Analyst consensus sits at a buy rating across 13 covering analysts, with a mean 12-month price target of $151.50 against a current price of $146.09.

📈 With shares trading near the upper end of their 52-week range, DTE continues to reward income investors through consistent dividend growth, including a raise to $1.165 per share in December 2025.

Updated 2/25/26

DTE Energy (DTE) has built a consistent track record of financial discipline, infrastructure investment, and dependable shareholder returns. The company operates a regulated utility business across Michigan, delivering electricity and natural gas to millions of customers. With leadership focused on both grid reliability and clean energy expansion, DTE continues to execute a long-term strategy centered on stable operations and steady capital deployment.

Over the past year, the stock has traded between $123.69 and $154.63, and at the current price of $146.09 it sits in the upper half of that range. DTE’s dividend yield stands at 3.04 percent with a manageable payout ratio, and the company maintains a beta of just 0.48, reflecting its characteristically low volatility profile. Backed by confident leadership, consistent operating cash flow, and a disciplined transition toward renewable energy, DTE remains a name defined by operational strength and forward-looking capital planning.

Recent Events

DTE Energy has remained active on multiple fronts heading into early 2026. The company has continued to advance its grid modernization program across Michigan, directing capital toward power line upgrades and infrastructure hardening designed to reduce the impact of severe weather events that have historically pressured operational results. This investment push is part of a broader multi-year capital plan that management has communicated consistently to both regulators and investors.

On the regulatory front, DTE has been working through rate proceedings in Michigan, seeking cost recovery that would support its ongoing capital spending. Michigan’s regulatory environment has historically been constructive for DTE, and any positive outcome in pending cases would provide additional financial visibility heading into the second half of 2026. These approvals are central to the company’s ability to fund its clean energy transition without straining dividend coverage.

DTE also raised its quarterly dividend to $1.165 per share in December 2025, up from $1.09, representing another step in its pattern of annual increases. The company declared the most recent payment on that schedule, continuing a long-term commitment to growing shareholder distributions. With the annual dividend now running at $4.51 per share, this latest raise reinforces that management remains confident in the earnings trajectory going forward.

Short interest in the stock stands at roughly 3.9 million shares, a modest figure relative to total float that suggests the broader market is not positioning heavily against DTE’s near-term prospects.

📊 Key Dividend Metrics

💸 Forward Dividend Yield: 3.04%

📈 5-Year Average Yield: 3.32%

💰 Annual Dividend Payout: $4.51 per share

🧮 Payout Ratio: 63.09%

🗓 Last Dividend Payment: $1.17 per share

✅ Dividend Safety: Reasonably Strong

🏛 Dividend Track Record: Long-Term, No Cuts

Dividend Overview

DTE’s forward yield of 3.04 percent places it in a reasonable range for income investors seeking a regulated utility with consistent payout growth. The yield has compressed slightly relative to its five-year average of 3.32 percent, but that reflects a stock that has appreciated meaningfully rather than a dividend that has stalled. At $4.51 per share annually, the payout is well-supported by earnings of $7.03 per share, leaving room for reinvestment in infrastructure while still rewarding shareholders.

The payout ratio of 63.09 percent is appropriate for a utility operating in a capital-intensive environment. It reflects a management team that takes both growth and income obligations seriously, calibrating distributions to earnings without overextending. Given the predictability of DTE’s regulated revenue base, there is little to suggest that this balance will be disrupted in the near term.

What continues to distinguish DTE as a dividend holding is the combination of yield, stability, and incremental growth. The company raised its quarterly payment from $1.09 to $1.165 in December 2025, extending a pattern of annual increases that goes back many years. For investors who value consistency over splashy payouts, DTE’s dividend policy reflects exactly the kind of measured, long-term thinking that keeps income streams growing reliably.

Dividend Growth and Safety

DTE’s dividend history over the past several years tells a straightforward story of steady annual increases. The quarterly payment moved from $0.953 per share through most of 2023, stepped up to $1.02 at the end of that year, rose again to $1.09 entering 2025, and most recently increased to $1.165 in December 2025. That progression reflects a compounding rate roughly in the 5 to 6 percent range annually, which is consistent with what management has communicated as a long-term target.

With a payout ratio just above 63 percent and operating cash flow of $3.41 billion over the trailing twelve months, the dividend is well-covered from an earnings and cash perspective. Free cash flow is currently negative at approximately $1.75 billion, but that figure reflects the scale of DTE’s capital expenditure program rather than any underlying operational deterioration. Utilities routinely carry negative free cash flow during intensive grid upgrade cycles, and the operating cash flow generation more than offsets concerns about payout sustainability.

Volatility remains low, with DTE carrying a beta of just 0.48. For income investors, that kind of price stability provides a smoother holding experience, particularly during periods of broader market turbulence. The stock has traded in a relatively defined range over the past year, reinforcing its character as a defensive income name rather than a high-growth trade.

Looking ahead, dividend growth in the 4 to 6 percent range annually remains the most reasonable expectation. The company is not positioned for aggressive payout acceleration, but it does not need to be. Incremental, reliable growth compounded over many years is the model, and DTE has executed that model without interruption.

Valuation sits at a P/E of 20.78, a slight step up from historical norms for the sector but not unreasonable given the company’s earnings consistency and dividend track record. A price-to-book ratio of 2.47 against a book value of $59.22 per share is in line with well-capitalized utilities and reflects the premium investors are willing to pay for regulated earnings stability.

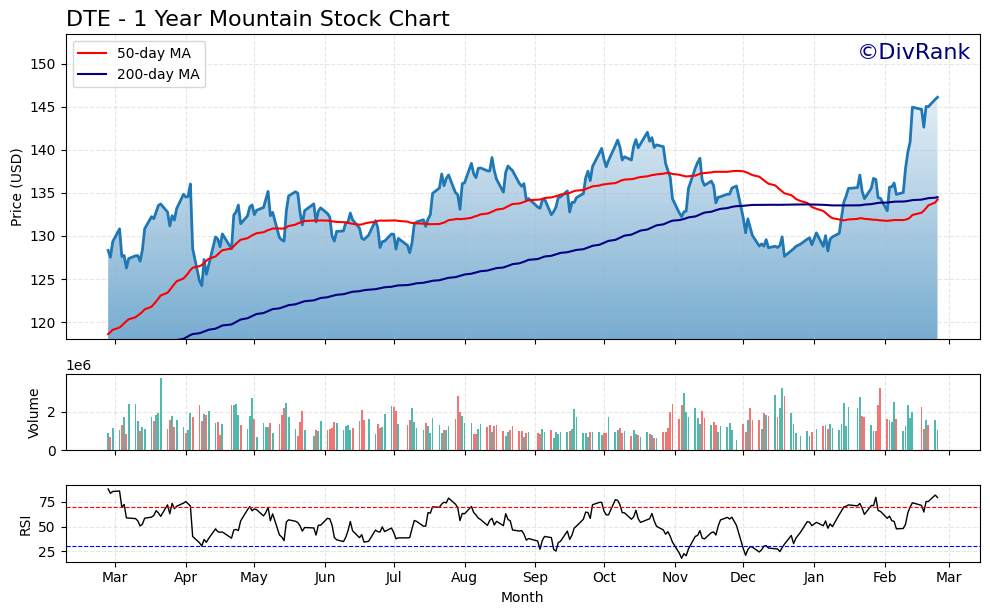

Chart Analysis

DTE Energy has put together an impressive run over the past year, climbing from a 52-week low of $124.23 to its current price of $146.09, which also happens to be the 52-week high. That 17.6% advance from trough to peak reflects a stock that has steadily recovered and then accelerated, with recent momentum carrying shares right up to the top of their annual range. For dividend investors, a stock trading at its 52-week high is a double-edged signal: it confirms underlying fundamental confidence, but it also means there is no technical cushion built in from recent consolidation.

The moving average picture is more nuanced. DTE currently trades well above both its 50-day moving average of $134.23 and its 200-day moving average of $134.50, which on the surface looks constructive. However, the 50-day moving average sits fractionally below the 200-day, a configuration technically classified as a death cross. That bearish crossover suggests the intermediate trend was weakening before this latest price surge, and the rapid climb above both averages looks more like a sharp rally than a sustained, orderly uptrend. The gap between the current price of $146.09 and both moving averages, which sit roughly $12 below current levels, is wide enough to warrant some caution about near-term mean reversion.

The RSI reading of 79.34 reinforces that caution. A reading above 70 is generally considered overbought territory, and DTE is sitting meaningfully above that threshold. Momentum of this magnitude, while impressive in the short run, historically increases the probability of a pullback or at minimum a period of sideways consolidation as the stock digests its gains. Investors chasing shares at this level are buying into a name with very little technical breathing room.

For dividend investors, the core thesis on DTE remains intact from a fundamental standpoint, but the chart is flashing a clear message about timing. Those already holding shares can take comfort in the price appreciation padding their total return, but initiating a new position at the 52-week high with an RSI near 80 introduces short-term price risk that income-focused buyers typically prefer to avoid. A pullback toward the $134 to $138 range, where both moving averages currently reside, would offer a far more attractive entry point and a more favorable yield on cost for anyone building a long-term dividend position.

Cash Flow Statement

DTE Energy’s operating cash flow has shown a generally positive trajectory over the review period, climbing from $3,067.0M in 2021 to $3,643.0M in 2024, with TTM coming in at $3,409.0M. That underlying operational cash generation is a genuine strength for dividend sustainability, as it confirms the core utility business continues to convert earnings into real cash at scale. The complication, as with most capital-intensive regulated utilities, is that free cash flow has been persistently and deeply negative across every year in the dataset, ranging from -$705.0M in 2021 to a TTM figure of -$1,746.6M. For dividend sustainability purposes, this means DTE funds its dividend through a combination of operating cash flow, debt financing, and equity issuance rather than free cash flow alone, which is a standard structural feature of large regulated utilities but one that investors should understand clearly before drawing comfort from the operating cash line.

The widening gap between operating cash flow and free cash flow in the TTM period, where free cash flow deteriorated to -$1,746.6M despite solid operating cash of $3,409.0M, signals an acceleration in capital expenditure intensity rather than any erosion in the business itself. DTE has been investing heavily in grid modernization, renewable energy transition, and infrastructure upgrades required under its regulated framework, all of which consume capital well in excess of depreciation charges in the near term. From a shareholder perspective, this level of reinvestment is a double-edged reality: it pressures near-term financial flexibility and keeps the company reliant on external capital markets, but it also underpins the rate base growth that drives future regulated earnings and, by extension, future dividend increases. As long as DTE continues to secure constructive rate case outcomes from Michigan regulators, the capex burden today is building the earnings foundation that supports dividend growth tomorrow.

Analyst Ratings

Analyst sentiment toward DTE Energy is broadly positive heading into early 2026. Across 13 covering analysts, the consensus sits at a buy rating, reflecting confidence in the company’s regulated earnings base, dividend reliability, and long-term capital strategy. The mean 12-month price target of $151.50 implies modest upside from the current price of $146.09, while the high-end target of $168.00 reflects a more optimistic scenario tied to favorable regulatory outcomes and continued earnings growth. The low-end target of $139.00 represents the more cautious end of the range, suggesting limited downside risk even for those with a conservative view.

The distribution of targets around the current price is telling. With shares at $146.09 sitting between the mean target of $151.50 and the low of $139.00, analysts collectively view DTE as fairly valued to modestly undervalued. That positioning is consistent with a stock that has already appreciated meaningfully over the past year but retains room to move higher as earnings and regulatory developments unfold through 2026.

For a utility of DTE’s profile, a buy consensus among 13 analysts is a strong endorsement. The sector does not typically generate the kind of aggressive price target upgrades seen in growth names, but the consistency and breadth of coverage here reflects a market that views DTE as a well-managed, reliable compounder rather than a speculative hold. Income investors can take some comfort in the fact that analyst views on the name have remained constructive even as the stock has moved higher.

Earning Report Summary

Consistent Execution Across the Business

DTE Energy’s most recent financial results reinforce a familiar narrative of steady, regulated utility performance. Revenue for the trailing twelve months came in at $15.81 billion, and net income reached $1.46 billion, producing earnings per share of $7.03. Those figures reflect a business that continues to generate reliable income from its core Michigan electric and natural gas operations, even as capital spending remains elevated. Profit margins of 9.25 percent are in line with what regulated utilities typically produce, and return on equity of 12.18 percent suggests the company is generating acceptable returns on the capital shareholders have entrusted to it.

Investment and Infrastructure in Focus

Capital expenditure remains the defining feature of DTE’s recent financial story. The company is in the midst of a sustained infrastructure investment cycle, directing billions of dollars toward grid hardening, reliability improvements, and clean energy capacity additions. That spending is the primary reason free cash flow is deeply negative, and management has been consistent in communicating that this is an intentional strategic posture rather than a financial constraint. The operating cash flow of $3.41 billion demonstrates that the underlying business is generating real cash, even if much of it flows back into capital projects.

Looking Ahead

Management has maintained a forward posture centered on long-term earnings growth and dividend sustainability. The December 2025 dividend increase to $1.165 per quarter signals confidence in the earnings outlook for 2026, and ongoing rate proceedings in Michigan are expected to provide additional cost recovery as the capital program continues. Leadership has consistently framed the company’s investment cycle as a long-term value creation effort, with the expectation that infrastructure spending today will support rate base growth and earnings per share growth over the coming years. From the tone and financial results available, DTE appears to be executing in line with its stated plan.

Management Team

DTE Energy’s leadership remains focused on long-term execution and operational discipline. Chairman and CEO Jerry Norcia has kept the company on a steady path, emphasizing investments in clean energy while ensuring the traditional utility infrastructure remains reliable. Under his watch, DTE has expanded its presence in renewables and pushed forward on its carbon reduction roadmap, all while maintaining consistent earnings and dividend growth.

CFO David Ruud and the broader executive team have maintained a conservative financial posture. They have balanced significant capital expenditures with steady operating cash flow and manageable debt servicing. The tone from leadership continues to reflect confidence in the business, particularly in their ability to navigate weather challenges, regulatory changes, and shifting energy demand without compromising financial goals. The management approach is focused more on execution than promises, and that has supported the company’s credibility with investors over many years.

Valuation and Stock Performance

DTE’s share price of $146.09 places it in the upper portion of its 52-week range of $123.69 to $154.63, reflecting a stock that has seen meaningful appreciation while stopping just short of a new high. The roughly 18 percent rally from the low earlier in the year has been supported by improving earnings visibility, constructive regulatory developments in Michigan, and sustained investor appetite for low-volatility income names in an uncertain market environment.

At a P/E of 20.78, DTE is priced at a slight premium to the broader utility sector average, but that premium is defensible given the company’s earnings consistency, payout growth track record, and the relative stability of Michigan’s regulatory framework. The price-to-book ratio of 2.47 against a book value of $59.22 per share is consistent with other well-capitalized regulated utilities and reflects the value investors assign to predictable, rate-base-driven earnings streams.

The dividend yield of 3.04 percent remains competitive for a regulated utility, particularly one with a demonstrated commitment to annual increases. Combined with a beta of 0.48, DTE continues to offer the combination of income and low volatility that has historically attracted long-term institutional holders. With the mean analyst price target of $151.50 sitting above the current price, the stock retains modest upside potential even after its recent run, and the low-end target of $139.00 provides a reasonable downside reference for those assessing entry points.

Risks and Considerations

Regulatory risk remains the most consequential variable in DTE’s long-term outlook. The company’s business model depends on recovering capital costs and earning an allowed return through Michigan’s rate-setting process. That process has historically been constructive, but any shift in regulatory posture, whether driven by political changes, consumer advocacy, or economic conditions, could affect the pace of cost recovery and put pressure on earnings projections. A less favorable rate environment would also complicate the financial case for DTE’s ongoing capital program.

The company’s debt load is substantial, as is typical for capital-intensive regulated utilities, and changes in the interest rate environment can affect financing costs over time. While DTE’s debt is primarily long-dated, ongoing capital expenditure requirements mean the company regularly accesses credit markets, and elevated rates translate into higher costs on new issuances. This dynamic bears watching, particularly in a period where infrastructure spending shows no sign of decelerating.

Severe weather continues to represent a real operational and financial risk. Ice storms, high winds, and extreme precipitation events can cause meaningful infrastructure damage across DTE’s Michigan service territory, driving up maintenance costs and creating customer service pressures that invite regulatory and public scrutiny. The company has invested significantly in grid hardening and vegetation management to reduce these impacts, but the underlying weather risk cannot be fully engineered away, and climate trends suggest these events may become more frequent.

The transition toward cleaner energy sources introduces its own set of execution risks. Balancing carbon reduction commitments with service reliability and cost management requires precise capital allocation and regulatory alignment. The scale of investment required for the clean energy shift must be financed and managed in a way that does not erode dividend coverage or compromise the financial flexibility that underpins DTE’s income investor appeal.

Final Thoughts

DTE Energy continues to present a picture of steady, measured growth. The company raised its quarterly dividend to $1.165 per share in December 2025, extending a track record of annual increases that reflects management’s confidence in the earnings trajectory ahead. At a yield of 3.04 percent and a payout ratio just above 63 percent, the income profile remains attractive without showing signs of overextension.

The company’s leadership has demonstrated a clear commitment to balancing infrastructure investment with financial discipline, directing capital into grid modernization and clean energy while sustaining operating cash flow that comfortably covers dividend obligations. That balance has earned DTE a buy consensus from 13 analysts and a mean price target of $151.50, implying that the market still sees room to run from current levels.

While regulatory risk, weather exposure, and an elevated debt load are genuine considerations, none of them represent new or unexpected challenges for a company that has navigated this operating environment for decades. For investors who favor a slow-and-steady approach built on regulated earnings, disciplined capital deployment, and reliable income growth, DTE continues to deliver exactly what it has always promised. In a market that frequently rewards noise over substance, that kind of consistency carries real value.