Key Takeaways

💵 The regular dividend yield stands at just 0.20% on an annualized basis of $1.20, but a payout ratio of only 2.85% leaves enormous room for the special dividends that have defined Dillard’s capital return story.

💡 Free cash flow remains healthy at approximately $502 million, supported by $717 million in operating cash flow and restrained capital spending.

📊 The analyst consensus sits at underperform across just three covering firms, with a mean price target of $561.33, modestly below the current price of $595.88.

📈 Dillard’s delivered $570 million in net income on $6.56 billion in revenue, generating EPS of $36.77 and sustaining a return on equity of nearly 32%.

Updated 2/25/26

Dillard’s, Inc. (DDS) continues to operate as one of the most financially disciplined retailers in the country, prioritizing cash generation, shareholder returns, and balance sheet strength over expansion or trend-chasing. The company reported solid full-year results with net income of $570 million and EPS of $36.77, metrics that reflect genuine operational efficiency rather than financial engineering. The regular quarterly dividend was raised from $0.25 to $0.30 in the third quarter of 2025, and the company once again delivered a large special dividend in December, underscoring the flexible capital return model that long-term shareholders have come to expect. With a current price of $595.88 and a P/E of just 16.21, the valuation picture is more nuanced than a casual glance suggests.

Recent Events

Dillard’s capped fiscal 2025 in a manner consistent with its reputation for quiet execution. In December 2025, the company paid another large special dividend of $30.00 per share, following a similar $25.00 special dividend in December 2024 and a $20.00 special in December 2023. This recurring pattern of year-end special distributions has become a defining feature of how management returns excess capital, and the December 2025 payout marked an increase over the prior year’s special, reflecting confidence in the underlying cash position.

Separately, the company raised its regular quarterly dividend from $0.25 to $0.30 beginning with the September 2025 payment, a 20% increase in the base payout. While the regular dividend remains small in absolute terms relative to EPS, the directional move signals that management is willing to nudge the recurring income stream upward as the business supports it.

On the operational front, Dillard’s has maintained its characteristic discipline in store management and inventory control. There have been no major acquisition announcements or store expansion programs, which is consistent with the company’s long-standing preference for organic efficiency over growth at any cost. The retail environment has remained uneven, with consumer spending on apparel and home goods facing pressure from broader macroeconomic uncertainty, but Dillard’s profit margin of 8.69% continues to outperform most brick-and-mortar peers.

Key Dividend Metrics

📅 Next Dividend Date: March 31, 2026 (estimated)

🔻 Ex-Dividend Date: March 2026 (estimated)

💵 Regular Annual Dividend: $1.20

📈 Dividend Yield (Regular): 0.20%

🧮 Payout Ratio: 2.85%

📊 5-Year Average Yield: 0.49%

🎁 Most Recent Special Dividend: $30.00 (December 2025)

💡 Free Cash Flow (ttm): $501.9 million

📉 Operating Cash Flow (ttm): $717 million

Dividend Overview

A 0.20% regular dividend yield is not going to attract income investors scanning for yield. That number, taken in isolation, tells almost none of the actual story at Dillard’s. The regular quarterly dividend of $0.30 per share, or $1.20 annualized, is intentionally modest, and management has made no secret of the reasoning: they prefer to retain flexibility and deploy capital where it generates the most value for shareholders, which often means buybacks and special dividends rather than an elevated base payout.

The payout ratio of 2.85% against EPS of $36.77 illustrates just how much room exists. Dillard’s is generating far more earnings per share than it distributes through the regular dividend, which means the base payout is essentially immune to any near-term earnings softness. The real income event for DDS shareholders has become the December special dividend, which totaled $30.00 per share in 2025, up from $25.00 in 2024. Investors who hold through year-end are rewarded with a cash distribution that dwarfs the regular quarterly income.

This model requires a different frame of reference than a traditional dividend growth stock. Rather than evaluating Dillard’s on consecutive annual dividend increases to the regular payment, the more relevant measure is total capital returned per share across both channels. On that basis, the company has been consistently generous, and the trend is moving in the right direction.

Dividend Growth and Safety

The September 2025 increase in the regular quarterly dividend from $0.25 to $0.30 represents a 20% step-up in the base payout and signals a modest but meaningful shift toward growing the recurring income stream. That change, combined with the larger December 2025 special of $30.00 versus $25.00 in December 2024, suggests that management felt comfortable accelerating shareholder returns heading into 2026.

The safety of the dividend is about as well-supported as it gets in the retail sector. Operating cash flow of $717 million and free cash flow of approximately $502 million leave a wide margin of coverage over both the regular dividend and even a generous special. With EPS of $36.77 and a payout ratio of 2.85%, there is no realistic scenario in which the regular dividend faces a cut unless the business suffers a catastrophic and sustained earnings collapse, which the current balance sheet is specifically designed to prevent.

Insider ownership remains one of the most compelling aspects of the Dillard’s story. With roughly a third of shares held by insiders, the people deciding how much cash to return are the same people receiving those distributions. That alignment consistently produces decisions oriented toward long-term value preservation rather than short-term optics. Return on equity of 31.90% and return on assets of 12.23% confirm that management is deploying capital productively, not just sitting on it.

Share repurchases continue to complement the dividend program by shrinking the denominator and naturally lifting EPS over time. This mechanical support for earnings per share is part of why the dividend, even at a low nominal level, is structurally secure. The company is not leveraging its balance sheet to fund returns; it is funding them from genuine operating cash flow, which is the most durable foundation possible.

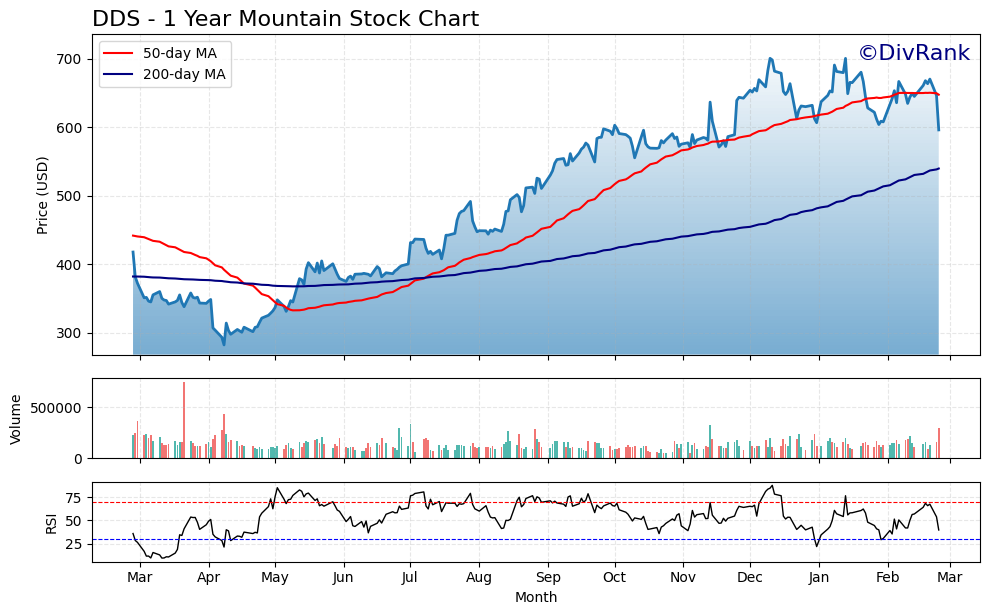

Chart Analysis

Dillard’s has delivered a remarkable run over the past year, with shares climbing from a 52-week low of $282.18 to a current price of $595.88, representing a gain of more than 111% from the trough. That kind of price appreciation is unusual for a traditional department store retailer, and it reflects both the company’s aggressive share buyback program and a broader rerating of the stock by the market. The more recent picture is less euphoric, however. Shares have pulled back roughly 15% from their 52-week high of $700.28, and the stock has been consolidating in a range well below that peak, suggesting that the most aggressive phase of the upward move may be behind us for now.

The moving average picture tells a nuanced story. The 200-day moving average sits at $539.53, comfortably below the current price of $595.88, which confirms that the longer-term trend remains constructively bullish. The 50-day moving average, at $647.26, has crossed above the 200-day, producing what technicians call a golden cross, a configuration that has historically been associated with sustained upward momentum. The complication is that the current price is sitting beneath that 50-day average by a meaningful margin. That positioning typically indicates that near-term selling pressure has been sufficient to drag the stock below its intermediate trend line, and DDS will need to reclaim the $647 area to restore full technical conviction.

The RSI reading of 39.61 reinforces the sense that momentum has cooled considerably. At this level the stock is approaching oversold territory without having crossed the conventional 30 threshold that would signal an extreme reading. What it does communicate clearly is that sellers have been in control during the recent pullback phase, and the stock has not yet found the kind of buying interest that would stabilize momentum indicators. Readings in the high 30s can sometimes precede a reversal, particularly when the longer-term trend is still intact, but they can also linger if broader market conditions or sector sentiment remain soft.

For dividend investors, the technical setup presents a classic tension between an improving long-term trend and a choppy near-term picture. The golden cross on the moving averages and the substantial distance from the 52-week low are encouraging structural signals for investors with a multi-year time horizon. The pullback from the highs, combined with an RSI that has not yet bottomed out convincingly, suggests that patience may be rewarded with a better entry point in the weeks ahead. Income-focused investors watching DDS should treat the $540 area, near the 200-day moving average, as a meaningful technical floor, and any sustained move back above $647 would be a meaningful signal that the intermediate trend has reasserted itself.

Cash Flow Statement

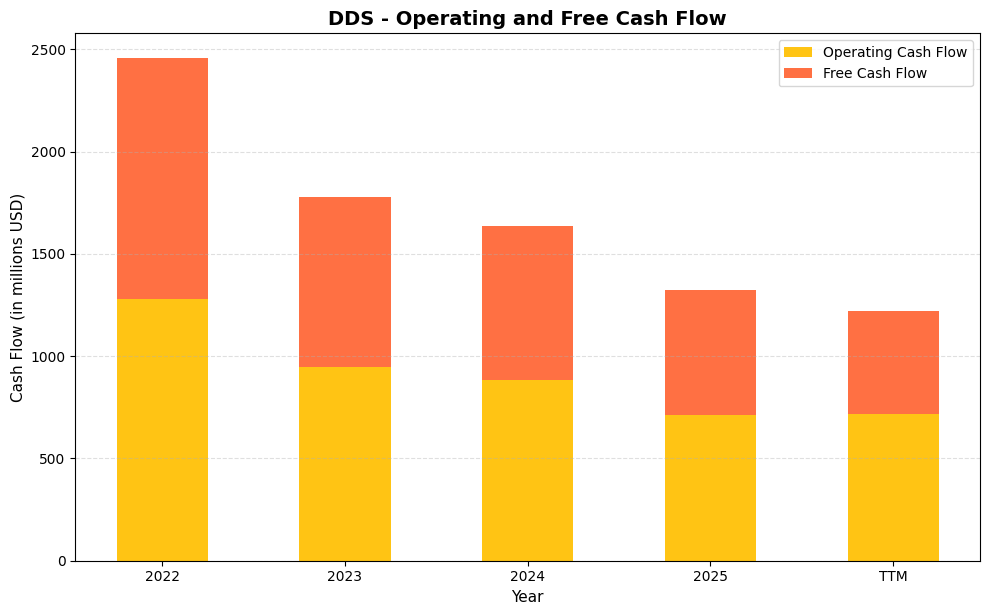

Dillard’s cash generation has followed a clear downward trajectory since its peak in 2022, when the company produced $1.28 billion in operating cash flow and $1.176 billion in free cash flow, figures that reflected an extraordinary post-pandemic retail environment. By fiscal 2025, operating cash flow had declined to $714.1 million and free cash flow to $609.6 million, with the trailing twelve months showing further compression to $717.0 million in operating cash flow and $501.9 million in free cash flow. Despite that compression, the dividend remains well covered. DDS pays a modest regular dividend that consumes a small fraction of annual free cash flow, and the company has consistently supplemented that with special dividends and aggressive share repurchases funded directly from operating cash generation. Even at the TTM free cash flow figure of $501.9 million, the company retains substantial capacity to sustain and grow its dividend program without straining the balance sheet.

The broader trend here deserves context rather than alarm. The 2022 cash flow numbers were exceptional, driven by inventory liquidation tailwinds, pent-up consumer demand, and margin expansion that was always unlikely to hold permanently. The step-down from $1.175 billion in free cash flow to roughly $502 million over three years reflects normalization more than structural deterioration, and Dillard’s capital expenditure discipline has remained consistent throughout, with capex running in the $100 million to $130 million range annually. That restraint keeps free cash flow conversion high relative to peers and signals that management is not chasing growth spending at the expense of shareholder returns. For income investors, the key takeaway is that even a normalized Dillard’s generates enough free cash flow to fund its dividend many times over, leaving ample room for continued buybacks that reduce the share count, support earnings per share growth, and ultimately make each remaining dividend dollar more valuable over time.

Analyst Ratings

Analyst coverage of Dillard’s remains thin, with only three firms actively publishing ratings on the stock. The consensus sits at underperform, which stands in some tension with the company’s actual financial performance and the continued appreciation in the share price over recent years. The mean price target among the three analysts is $561.33, which is modestly below the current price of $595.88, suggesting that the covering community as a whole views the stock as slightly stretched at current levels.

The range of price targets tells a more complete story. The high target of $700.00 implies roughly 17% upside from current levels, reflecting a constructive view on Dillard’s earnings power and capital return potential. The low target of $460.00, representing more than 20% downside, captures the bear case centered on sector headwinds, limited growth prospects, and what some analysts view as a valuation that exceeds fair value for a traditional department store operator. With just three analysts covering the stock, any single rating change carries outsized influence on the consensus designation.

The underperform consensus should be evaluated in context. Dillard’s has consistently outperformed the expectations embedded in cautious analyst ratings over the past several years, and the company’s financial metrics, including a 31.90% return on equity and a profit margin of 8.69%, are well above what the consensus designation might imply. For dividend growth investors, the analyst community’s conservatism is less relevant than the trajectory of cash flow and the company’s demonstrated commitment to returning capital.

Earning Report Summary

A Solid Finish, Even With Some Slippage

Dillard’s delivered full-year results that reinforced the company’s reputation for operational discipline. Net income of $570 million and EPS of $36.77 represent genuine profitability rather than a managed outcome, and a profit margin of 8.69% remains well above what most brick-and-mortar retail operators can sustain. Revenue of $6.56 billion reflects a consumer environment that has remained selective with discretionary spending, but Dillard’s has demonstrated that it can maintain strong margins even when top-line growth is limited.

Return on equity of 31.90% is a figure that stands out across virtually any sector, and in the context of retail it is exceptional. That metric reflects both the strength of earnings relative to book value and the impact of the company’s ongoing share repurchase program, which reduces equity over time and mathematically elevates ROE. Return on assets of 12.23% confirms that the earnings quality is genuine and not simply a leverage-driven result.

What Management Had to Say

CEO William T. Dillard, II maintained the measured, direct communication style that long-term observers of this company have come to expect. Management acknowledged the pressures facing the broader retail environment while emphasizing that Dillard’s operational focus on expense discipline and inventory management has allowed the company to protect its margin structure. The decision to raise the regular quarterly dividend to $0.30 and deliver a $30.00 special dividend in December reflects confidence in the durability of the cash flow model.

There were no dramatic strategic announcements, no pivot to e-commerce grand plans, and no acquisition targets flagged. The message from leadership was consistent with prior years: run the business well, protect the balance sheet, and return capital to shareholders when earnings support it. That posture may frustrate growth-oriented investors, but it remains exactly what income-focused shareholders should want from this management team.

Looking Ahead

Dillard’s does not provide formal forward guidance, which is consistent with its conservative communication approach and reflects a management team that prefers to let results speak rather than set expectations that could distort short-term decision-making. The directional signals from the 2025 results suggest a business that is managing through a softer consumer spending cycle without compromising its financial foundation. Free cash flow of $502 million provides ample capacity to sustain the current dividend structure and continue buybacks, and the balance sheet remains a source of strategic optionality. The question heading into 2026 is whether consumer spending on apparel and home goods recovers, which would provide a top-line tailwind that the company is operationally well-positioned to convert into earnings.

Management Team

Dillard’s remains a family-led business in the most meaningful sense of the phrase. CEO William T. Dillard, II has spent decades guiding the company with a philosophy built on financial conservatism, operational discipline, and a preference for long-term value over short-term performance. His leadership style is deliberate and low-profile, which mirrors the company’s overall approach to communication and strategy. There are no bold pivots or headline-grabbing announcements, just steady execution of a model that has proven durable across multiple retail cycles.

The approximately one-third insider ownership stake is one of the most structurally important facts about this company. Management and the founding family own enough of the business that their financial interests are genuinely aligned with outside shareholders. This alignment consistently produces capital allocation decisions that prioritize sustainability, and it is a key reason why the special dividend program has been maintained and grown rather than abandoned during periods of sector pressure.

The team communicates in a factual, understated manner that some investors find frustrating but that reflects a genuine focus on operating the business rather than managing perceptions. For dividend growth investors who value alignment and long-term consistency over public relations, Dillard’s leadership represents one of the more trustworthy management setups in the retail sector.

Valuation and Stock Performance

At $595.88 per share, Dillard’s trades at a P/E of 16.21 against trailing EPS of $36.77. For a brick-and-mortar retailer operating in a sector that often commands single-digit multiples, that valuation requires some justification, and the company’s financial metrics largely provide it. A return on equity of 31.90%, a profit margin of 8.69%, and free cash flow of $502 million are the kinds of numbers that support a premium to traditional retail peers. The price-to-book ratio of 5.23 against book value of $114.04 per share reflects both the earnings power of the franchise and the impact of years of share repurchases reducing book value.

The 52-week range of $282.24 to $741.98 tells the story of a stock that has experienced significant volatility over the past year. Shares have pulled back considerably from the $741.98 high, and at $595.88 the stock sits roughly in the middle of that range. The mean analyst price target of $561.33 implies that the consensus view sees modest downside from current levels, while the high target of $700.00 suggests that the bull case remains intact for investors who believe in the company’s cash generation and capital return trajectory.

The market cap of approximately $9.3 billion against free cash flow of $502 million represents a free cash flow yield of roughly 5.4%, which is a meaningful return when combined with the special dividend program. For investors who evaluate Dillard’s on total capital returned rather than the nominal dividend yield, the valuation case is considerably more compelling than the headline P/E or yield figures might suggest. The stock is not obviously cheap, but neither is it obviously expensive given the quality of the underlying business.

Risks and Considerations

The most persistent risk facing Dillard’s is the structural shift in how consumers shop. The ongoing migration toward e-commerce and the changing preferences of younger consumer cohorts continue to pressure traditional department store traffic. Dillard’s has made incremental investments in its digital capabilities, but it has not positioned itself as an omnichannel leader, and the gap between its online presence and that of larger competitors remains meaningful. This is a slow-moving risk rather than an immediate crisis, but it is one that income investors need to hold in their awareness over a multi-year horizon.

The concentration of the dividend return story in the annual special distribution creates a different kind of risk than investors face with traditional dividend growth stocks. If operating cash flow were to decline significantly due to a prolonged consumer spending downturn, management would likely reduce or eliminate the special dividend before touching the regular payout. Investors who have incorporated the special dividend into their income planning should recognize that it is discretionary rather than contractually committed, even if the track record of paying it has been consistent.

Thin analyst coverage introduces a structural risk to the stock’s price discovery process. With only three analysts following DDS, the stock is more susceptible to outsized price moves on any individual rating change or earnings surprise. This can work in both directions, but the lack of broad institutional research coverage means that information about the company reaches the market less efficiently than it would for a more widely followed name.

The elevated price-to-book ratio of 5.23 and the stock’s position well above the mean analyst price target suggest that much of the optimism around Dillard’s capital return program is already reflected in the current valuation. If the December 2026 special dividend disappoints relative to the $30.00 paid in 2025, or if earnings compress meaningfully, the stock could face a sharper correction than the modest beta would imply. Investors entering at current prices are paying for a continuation of strong execution, which adds execution risk to the thesis.

Final Thoughts

Dillard’s is a genuinely unusual company in the retail sector, and that unusualness is precisely what makes it interesting for a certain kind of income investor. The regular dividend yield of 0.20% is not the point. The point is a business generating $717 million in operating cash flow, run by insiders who own roughly a third of the company, with a payout ratio of 2.85% that leaves almost unlimited room for the kind of capital return flexibility that produced a $30.00 special dividend in December 2025.

The recent raise in the regular quarterly dividend to $0.30 and the increase in the December special from $25.00 to $30.00 both point in the same direction: management is comfortable with the trajectory of cash generation and is willing to share more of it as the business supports that decision. That is exactly the kind of signal dividend growth investors want to see, even if the mechanism looks different from a traditional annual dividend increase.

The risks are real. The retail environment is structurally challenging, the stock is not cheap by conventional metrics, and analyst sentiment is cautious. But Dillard’s has navigated retail headwinds for decades by refusing to overextend, staying disciplined on the balance sheet, and treating capital allocation as a long-term responsibility rather than a quarterly performance tool. In a market full of companies that say those things, Dillard’s is one that actually does them. For investors who can appreciate that distinction, the thesis here is straightforward even if the dividend structure is unconventional.