Key Takeaways

🚂 CSX operates a robust 20,000-mile railroad network crucial to the U.S. economy.

📈 Shares have surged toward 52-week highs, trading at $42.20 with a P/E of 27.41.

💰 Dividend yield of 1.22% is supported by a conservative 33.77% payout ratio and strong operating cash flow.

⚠️ The stock now trades above the consensus analyst price target of $39.98, warranting valuation discipline.

👔 Experienced management continues to prioritize operational efficiency and consistent dividend growth.

Updated 2/25/26

CSX Corporation has long been one of the key players in the American railroad industry. Based out of Jacksonville, Florida, the company operates an impressive 20,000-mile rail network that connects major markets across the eastern United States. From moving coal and chemicals to transporting consumer goods and agricultural products, CSX plays a crucial behind-the-scenes role in the country’s economy.

The beauty of CSX’s business is in its simplicity and scale. No matter how much the world leans into technology, goods still need to move physically from one place to another. CSX makes sure that happens efficiently. Even when economic headwinds blow strong, the company’s focus on operational efficiency and steady capital returns keeps it attractive, especially for dividend-focused investors.

Let’s dig into how things are shaping up recently and what dividend investors should keep an eye on.

Recent Events

CSX has been generating renewed investor interest as shares have climbed sharply over the past several months, approaching the upper end of the 52-week range of $26.22 to $42.68. The stock’s move from its lows reflects improving sentiment around freight demand and broader industrial activity, with investors rotating back into transportation names as the economic backdrop has steadied. The rally has pushed CSX’s market capitalization to approximately $78.5 billion, a meaningful recovery from where the stock was trading earlier in the range.

On the operational front, CSX President and CEO Joe Hinrichs has continued pressing forward with network reliability initiatives and service improvement programs across the 20,000-mile system. Management has kept its messaging focused on execution and cost discipline, themes that resonate with investors who watched the company navigate through softer freight conditions in prior quarters. The emphasis on improving service metrics has been a consistent refrain from leadership, and there are signs those efforts are beginning to show up in the numbers.

Revenue for the trailing twelve months came in at $14.09 billion, and net income reached $2.89 billion with earnings per share of $1.54. Profit margins held at a solid 20.50%, and return on equity came in at 22.51%, reflecting the underlying quality of the franchise even as the revenue base has moderated from peak levels. The company’s operating cash flow of $4.61 billion continues to demonstrate the cash-generative nature of the rail business, giving management ample flexibility to fund capital programs and return cash to shareholders.

Key Dividend Metrics

📈 Forward Dividend Yield: 1.22%

💵 Annual Dividend: $0.52

📅 Last Dividend Payment: $0.13 per share

🚂 Payout Ratio: 33.77%

📈 5-Year Dividend Growth: Positive and consistent

🔄 Most Recent Raise: From $0.12 to $0.13 per quarter (effective February 2025)

🛡️ Dividend Safety: Strong, backed by $4.61 billion in operating cash flow

Dividend Overview

CSX doesn’t compete on yield alone, but the consistency and growth trajectory of the dividend are what make it compelling for income-oriented investors. The current annual dividend of $0.52 per share translates to a forward yield of 1.22% at today’s price of $42.20. That yield is relatively modest in absolute terms, but the payout ratio of 33.77% signals that there is meaningful room for continued dividend growth without putting any stress on the balance sheet.

The most recent dividend increase, which moved the quarterly payment from $0.12 to $0.13 per share beginning in February 2025, represented an 8.3% raise, a healthy step up that reflects management’s confidence in the durability of the company’s cash flows. With operating cash flow running at $4.61 billion over the trailing twelve months and free cash flow at $970 million after capital expenditures, the dividend is extremely well covered. Total annual dividend payments on the current share base represent a fraction of what the business generates in cash, leaving plenty of capacity for buybacks and reinvestment simultaneously.

The five-year dividend history tells a clear story of steady, deliberate growth. CSX moved from $0.11 per quarter in 2023 to $0.12 in early 2024 and then to $0.13 in early 2025, a trajectory that dividend growth investors can appreciate for its predictability. The company has not wavered in its commitment to growing the payout, even through periods of softer freight volumes, which speaks to the durability of the underlying cash flow model.

Dividend Growth and Safety

When it comes to dividend investing, reliability often matters more than size. CSX gets that. Over the past several years, the company has steadily grown its quarterly payment from $0.11 to $0.13, representing an annualized growth rate that meaningfully outpaces inflation. Each increase has been measured and consistent, reflecting a management team that takes the dividend seriously as a capital allocation commitment rather than an afterthought.

With a payout ratio of 33.77%, CSX maintains a wide safety margin. Even if earnings were to soften materially in a given period, the dividend would remain well protected. Earnings per share of $1.54 cover the $0.52 annual dividend by a factor of nearly three times, and the cash flow coverage is even more comfortable. Operating cash flow alone exceeds the annual dividend obligation by a substantial multiple, which is the kind of cushion that lets long-term investors sleep soundly.

The structural advantages of the railroad business are worth keeping in mind here. CSX operates an irreplaceable network that cannot be replicated by a competitor. That physical moat translates into pricing power over time and a level of cash flow predictability that most businesses simply cannot match. Those qualities underpin the safety of the dividend across different points in the economic cycle.

One additional positive for dividend investors is that CSX has demonstrated its willingness to raise the dividend even during periods when the stock has underperformed. The February 2025 increase came after a stretch of softer freight results, signaling that management’s commitment to growing shareholder income is not contingent on perfect operating conditions. That kind of discipline is exactly what long-term income investors need to see from a core holding.

The long-term case for CSX’s dividend strength remains firmly intact. A wide economic moat, dependable cash generation, and a conservative payout philosophy are powerful allies for patient investors building a steady income stream over time.

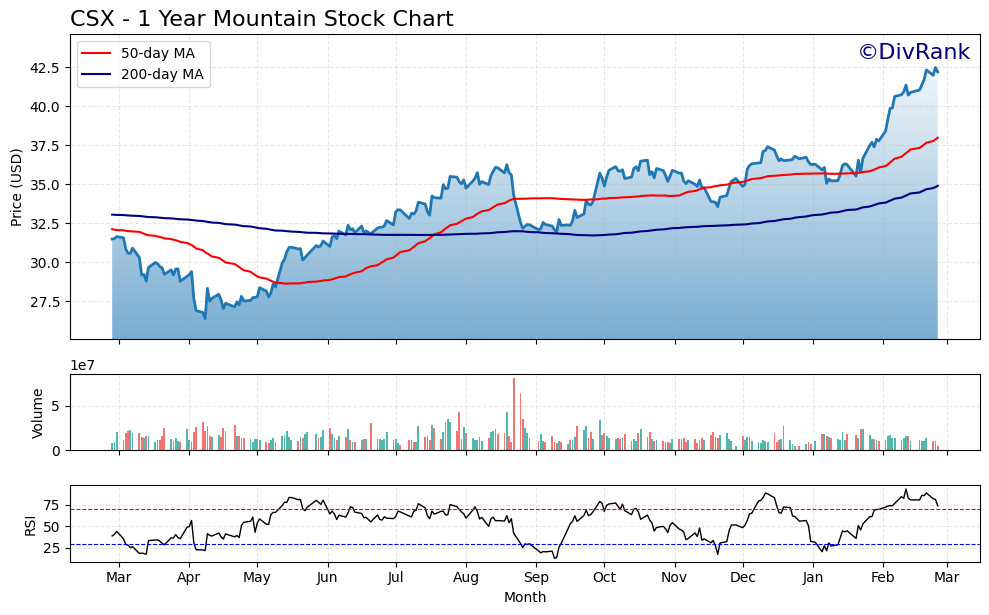

Chart Analysis

CSX has staged a remarkable recovery over the past year, climbing from a 52-week low of $26.38 to its current price of $42.19, a gain of nearly 60% from trough to present. That kind of price appreciation is unusual for a mature railroad operator, and it reflects a meaningful shift in market sentiment toward the name. The stock is now within a fraction of a percent of its 52-week high of $42.47, which tells you that buyers have been in firm control of the tape and that the recovery was not a brief overshooting event but a sustained, broadening advance.

The moving average picture is unambiguously constructive. CSX is trading well above both its 50-day moving average of $37.97 and its 200-day moving average of $34.88, and the 50-day has crossed above the 200-day to form what technicians call a golden cross. That configuration typically signals that intermediate-term momentum has aligned with the longer-term trend, and it is generally viewed as a confirming indicator rather than a leading one. The roughly $7 spread between the current price and the 50-day average also suggests the stock has built a meaningful cushion of support beneath it should any near-term selling pressure emerge.

The RSI reading of 74.0 is the one area that warrants measured attention. A reading above 70 places CSX in technically overbought territory by conventional standards, meaning the stock has moved a significant distance in a short period without a meaningful pullback to consolidate gains. For dividend investors adding to a position at current levels, this does not signal a fundamental problem with the thesis, but it does suggest that patient buyers may find a better entry point if the stock digests some of its recent gains over the coming weeks.

On balance, the technical setup for CSX reflects a stock in genuine recovery mode rather than one that has simply drifted higher on low volume. The golden cross, the proximity to 52-week highs, and the distance traveled from the lows all point to a name that the market is actively rerating upward. Income investors focused on CSX’s growing dividend stream should feel reasonably comfortable with the long-term trend structure here, while those with flexibility to wait may benefit from letting the RSI cool before committing new capital.

Cash Flow Statement

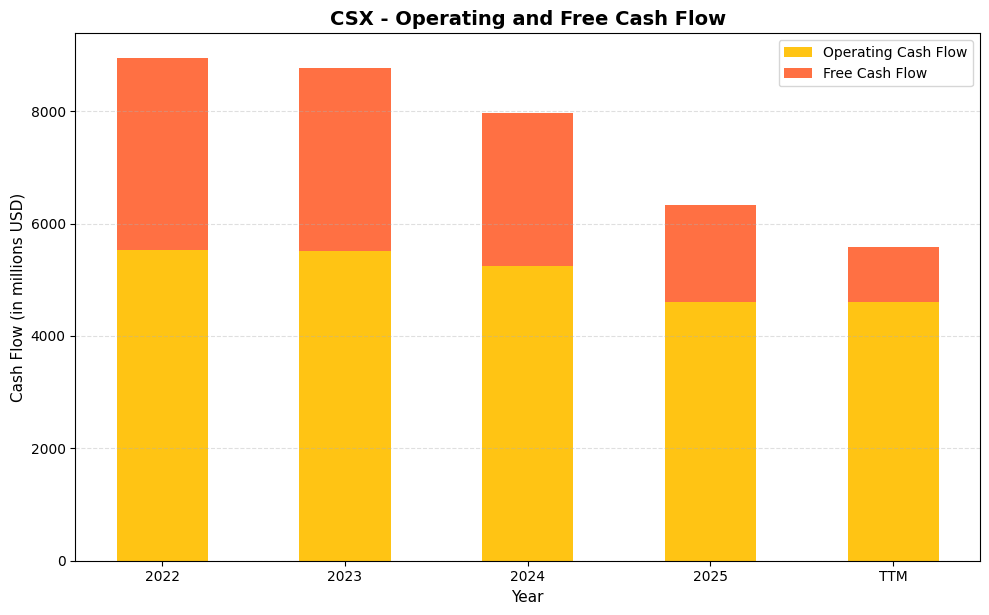

CSX’s cash flow profile has been under steady pressure over the measured period, and the trend demands attention from income-focused investors. Operating cash flow peaked at $5,526.0 million in 2022 and has declined in each subsequent year, reaching $4,613.0 million in both 2024 and full-year 2025. Free cash flow tells an even more pointed story, falling from $3,413.0 million in 2022 to $2,718.0 million in 2024 and then compressing sharply to $1,711.0 million in 2025. On a trailing twelve-month basis, free cash flow has narrowed further to just $970.5 million, a figure that warrants scrutiny when measured against the company’s dividend obligations and share repurchase commitments. The dividend itself remains covered at current payout levels, but the cushion that once made CSX a straightforward income holding has thinned considerably, and investors should monitor whether capital expenditure normalization or volume recovery can begin reversing this trajectory.

Zooming out across the full four-year window, CSX has shed roughly $2,400.0 million in annual free cash flow from its 2022 peak, a contraction of more than 70% on a free cash flow basis even as operating cash flow declined a comparatively modest 17%. That gap between the two metrics reflects a meaningful step-up in capital spending, which has consumed an increasing share of operating cash generation. For dividend growth investors, the concern is not imminent dividend risk but rather the reduced financial flexibility to simultaneously grow the dividend, fund buybacks, and invest in the network. If capital intensity begins to ease as infrastructure projects mature, free cash flow should recover and restore some of that flexibility. Until then, CSX is a case where the income thesis rests more heavily on earnings trajectory and less on the free cash flow abundance that characterized the stock just a few years ago.

Analyst Ratings

The analyst community holds a consensus buy rating on CSX, with 24 analysts covering the stock. The mean price target sits at $39.98, which is actually below the current trading price of $42.20, a dynamic that deserves attention from investors considering a new position today. The range of targets runs from a low of $30.00 to a high of $45.00, with the upper end of that range only marginally above where shares are currently trading.

The fact that CSX is trading above the consensus price target of $39.98 is a notable development. It suggests that the recent rally has outpaced analyst expectations, and that the stock may need earnings revisions higher or continued volume momentum to justify further appreciation from current levels. The $45.00 high target from the most optimistic analyst on the Street represents only about 6.6% upside from today’s price, a relatively narrow ceiling for a stock carrying a beta of 1.29.

Despite the valuation overhang relative to consensus targets, the buy rating itself reflects genuine confidence in CSX’s franchise quality, cash flow durability, and management execution. Analysts broadly recognize that the railroad business model generates superior returns through the cycle, and the 22.51% return on equity supports that view. For dividend investors, the key takeaway from the analyst community is that the business fundamentals are sound, even if the stock’s near-term upside from current prices appears limited relative to where targets are currently set.

Earning Report Summary

Full Year and Trailing Twelve Month Performance

CSX Corporation’s trailing twelve month results show a business generating $14.09 billion in revenue with net income of $2.89 billion. Earnings per share came in at $1.54, and the profit margin held at a solid 20.50%. Return on equity reached 22.51% and return on assets came in at 6.86%, both metrics reflecting the quality and efficiency of the underlying railroad franchise. Operating cash flow of $4.61 billion over the same period reinforces the view that CSX’s earnings are backed by real cash generation rather than accounting constructs.

The revenue figure of $14.09 billion represents a modest step down from the $14.28 billion reported in the prior comparable period, reflecting ongoing normalization in certain freight categories, particularly coal and intermodal. However, the company’s ability to maintain a 20.50% profit margin through that volume softness speaks to management’s cost discipline and the pricing leverage inherent in the rail model. These are not the results of a business under structural pressure but rather one navigating a cyclical freight environment with its margins largely intact.

Leadership’s Take on the Quarter

CSX President and CEO Joe Hinrichs has maintained a forward-looking tone throughout the recent operating period, emphasizing network reliability, service quality, and customer satisfaction as the primary levers for driving long-term revenue growth. His focus on fixing operational challenges that emerged in prior periods has been consistent, and the margin resilience visible in the numbers suggests those efforts are bearing fruit. Leadership has been candid about the freight market environment while expressing confidence in the company’s ability to grow volumes as conditions improve.

Management has also continued to highlight the importance of disciplined capital allocation, balancing ongoing infrastructure investment with meaningful returns to shareholders through dividends and repurchases. The tone from the executive team suggests a group that is neither complacent about the challenges ahead nor distracted from the operational priorities that drive long-term performance. For dividend investors, that combination of candor and operational focus is exactly what you want to see from the team managing a core income holding.

Management Team

CSX is led by a seasoned executive group with strong backgrounds in transportation and large-scale operations. At the top is Joe Hinrichs, who serves as President and CEO. Since taking over, he has focused on improving performance across the network and enhancing customer service through better execution. Hinrichs brings a leadership style that emphasizes reliability, efficiency, and people-first operations. His past experience managing massive industrial operations shows in the way CSX has responded to service challenges and worked to build a more consistent operating profile.

The rest of the executive team includes leaders across operations, finance, and technology who have worked in rail and infrastructure for years. Their approach to managing CSX has remained consistent: tight cost control, a focus on long-term value, and maintaining safety and service standards across the network. This kind of leadership continuity and deep industry knowledge tends to serve well in navigating both growth cycles and periods of freight softness, and it provides an important source of confidence for investors counting on the dividend to grow over time.

Valuation and Stock Performance

Shares of CSX currently trade at $42.20, near the top of the 52-week range of $26.22 to $42.68. The trailing P/E ratio of 27.41 represents a meaningful premium to where the stock was trading earlier in the past year, and it is also above the levels that most analysts have baked into their price targets. The price-to-book ratio of 5.97 on a book value per share of $7.07 reflects the market’s willingness to pay up for the quality and durability of CSX’s cash flows, though it also leaves limited room for multiple expansion from here.

The stock’s performance over the trailing twelve months has been exceptional, with shares nearly doubling off their 52-week low of $26.22. That kind of move reflects a significant re-rating, and it naturally raises the bar for continued appreciation. At 27 times trailing earnings, the market is pricing in a recovery in freight volumes and sustained margin performance. If those expectations are met, the valuation is defensible. If volumes disappoint or costs rise faster than anticipated, there is more downside risk embedded in the current price than was the case a year ago.

For dividend investors, the math at current prices is straightforward. The 1.22% yield is real and growing, but investors initiating a position today are accepting a lower starting yield than those who bought closer to the 52-week lows. The total return case depends increasingly on earnings growth rather than multiple expansion, which puts a premium on CSX continuing to execute on its operational improvement agenda. Patient investors with a long time horizon can still build a case for owning the stock, but the margin of safety is narrower at $42 than it was at $28.

Risks and Considerations

CSX’s business remains highly sensitive to the overall health of the U.S. economy. When industrial production slows, coal shipments decline, or consumer spending softens, freight volumes across the network can fall quickly. The company’s revenue base of $14.09 billion is diversified across commodity types, but no railroad is immune to a broad economic slowdown, and any deterioration in manufacturing activity or energy demand could pressure both volumes and pricing in the near term.

The current valuation represents a meaningful risk in its own right. Trading at a P/E of 27.41 and above the consensus analyst price target of $39.98, the stock has limited room for error. If earnings growth disappoints or the freight cycle turns lower again, the market could reprice shares quickly given the premium multiple. Investors buying at today’s levels are accepting more valuation risk than has been the case at various points over the past year.

Labor costs and union relations remain a persistent background consideration for CSX. The company operates under collective bargaining agreements, and while relations have been relatively stable in recent years, any disruption or acceleration in wage inflation could compress margins. The capital-intensive nature of the railroad business also means that maintenance and infrastructure spending are non-negotiable, putting ongoing pressure on free cash flow even as operating earnings remain healthy.

Environmental regulations continue to evolve, and increased compliance requirements around emissions and fuel efficiency could raise costs over the medium term. CSX has invested in modernizing its fleet and improving fuel efficiency, but this remains an ongoing effort with uncertain long-term cost implications. Finally, competition from trucking and alternative logistics networks is a structural consideration. While rail has clear advantages on fuel efficiency and cost per ton-mile over long distances, shifts in freight patterns or technology-driven logistics innovations could gradually erode certain volume categories over time.

Final Thoughts

CSX has had a strong run over the past year, and the business fundamentals that underpin the investment case remain intact. Revenue of $14.09 billion, a 20.50% profit margin, and operating cash flow of $4.61 billion paint a picture of a company that continues to perform well as a cash-generating machine. The dividend growth story is compelling, with the quarterly payment having risen from $0.11 to $0.13 over the past two years, and the 33.77% payout ratio leaves ample room for further increases ahead.

The primary consideration for investors today is valuation. At $42.20, shares are trading above the consensus analyst price target and near the top of the 52-week range. That doesn’t mean the stock can’t go higher, but it does mean that the risk-reward is more balanced than it was when shares were trading in the high twenties. Investors who own CSX have been well rewarded and have good reason to hold a well-run business with a durable competitive moat and a growing dividend.

For those considering a new position, the quality of the franchise is not in question. What matters is the entry point, and at current prices, patience may be rewarded if the market offers a more attractive starting yield. The long-term case for CSX as a dividend growth holding remains solid, grounded in an irreplaceable infrastructure network, experienced management, and a capital allocation philosophy that consistently prioritizes shareholders. The rails keep running, and for patient income investors, that’s ultimately what counts.