Updated 2/25/26

Community Bank System, Inc. (CBU), the parent company of Community Bank, N.A., has built a strong presence in the Northeast through a disciplined approach to banking and a consistent commitment to returning value to shareholders. With a dividend yield of 2.96% and a five-year average yield of 2.95%, CBU continues to attract long-term investors focused on income and stability. The company has delivered solid revenue and earnings growth, supported by strong leadership, expanding financial services, and a steady balance sheet. A consensus hold rating from analysts and a healthy payout ratio further highlight its ongoing dependability as an income holding.

Recent Events

Community Bank System has continued advancing its leadership structure following the appointment of Marya Burgio Wlos as Executive Vice President and Chief Financial Officer, a move that brought fresh operational depth to a management team already anchored by CEO Dimitar Karaivanov. Wlos, who brings prior experience from M&T Bank, has been integrating into the bank’s financial strategy as CBU works to sustain the earnings momentum built through 2024 and into 2025. Meanwhile, the bank’s ongoing expansion of fee-based services, including wealth management and insurance, has continued to diversify revenue beyond traditional net interest income, a strategic priority that has become increasingly important as the rate environment evolves.

On the business front, CBU has maintained its disciplined posture in the regional banking space, avoiding the kind of aggressive loan book expansion that has created credit quality problems for some peers. The bank’s markets across upstate New York and surrounding Northeast communities remain relatively stable, and deposit growth has continued to provide a reliable funding base. With short interest sitting at approximately 1.6 million shares, there is no meaningful bearish pressure building against the stock, and the technical picture heading into early 2026 reflects a name that has held up well in a rate-sensitive environment.

💰 Key Dividend Metrics

📅 Ex-Dividend Date: December 12, 2025

📥 Dividend Date: January 2026

🏦 Forward Dividend Yield: 2.96%

📈 5-Year Average Yield: 2.95%

💵 Annual Dividend Rate: $1.87

🧮 Payout Ratio: 46.85%

📊 Trailing 12-Month EPS: $3.97

💬 Dividend Overview

CBU’s current dividend yield of 2.96% sits right in line with its five-year average of 2.95%, which tells you something meaningful about where the stock is priced relative to its income history. This is not a yield that has been artificially inflated by a declining share price. Shares are trading at $63.48 as of this update, well within the upper portion of their 52-week range of $49.44 to $67.50, reflecting genuine investor confidence in the underlying business rather than a distressed entry point.

The payout ratio of 46.85% is one of the most reassuring figures in the CBU dividend profile. It has come down meaningfully from the 52.91% reported in the prior update, a direct result of earnings growth outpacing dividend increases. That compression in the payout ratio creates additional headroom for future dividend raises without straining the bank’s finances, and it signals that management is running the payout conservatively relative to what the earnings stream can support.

For income investors, a sub-50% payout ratio at a well-capitalized regional bank represents a durable setup. You are not reaching for yield here and taking on hidden risk. The dividend at $1.87 annually is well-covered by $3.97 in trailing EPS, and that margin of safety is what keeps the payout credible through varying economic conditions.

🔍 Dividend Growth and Safety

CBU has delivered another incremental dividend increase since the prior report. The per-share quarterly payment moved from $0.46 to $0.47 beginning with the September 2025 payment, bringing the annualized rate to $1.88 on a run-rate basis. That raise, while modest in percentage terms, continues a pattern of consistent upward movement that has defined CBU’s dividend history for years. Investors who have held this name for a decade have watched steady, quiet compounding work in their favor without dramatic headline moments in either direction.

Looking at the full recent dividend history, the cadence is clear: $0.44 per quarter in early 2023, rising to $0.45 by mid-2023, then $0.46 in late 2024 and into early 2025, and now $0.47 through the end of 2025. Each step is deliberate and measured. CBU is not trying to buy investor loyalty with aggressive hikes it cannot sustain. Instead, it is building a long-term record that income investors can count on.

The safety profile of the dividend is reinforced by an EPS of $3.97 and a payout ratio under 47%. Return on equity of 11.17% and return on assets of 1.25% both reflect a bank that is generating real earnings from its capital base rather than relying on leverage or accounting maneuvers. With a profit margin of 26.41% on $796.9 million in revenue, the earnings engine behind this dividend is operating with genuine efficiency. There are no red flags in the numbers that suggest the payout is at risk, and the trend in both earnings and dividends points in the same direction.

Chart Analysis

Community Bank System has put together a strong recovery over the past year, climbing roughly 27.6% off its 52-week low of $49.68 to trade at $63.41 as of the most recent session. That kind of sustained move off a trough reflects genuine buying interest rather than a short-lived bounce, and the price action along the way has been orderly enough to suggest institutional accumulation rather than speculative momentum. The stock remains within striking distance of its 52-week high of $66.77, sitting just 5% below that level, which tells income investors that CBU is operating near the top of its recent range without having overextended itself.

The moving average picture is constructive. CBU is trading above both its 50-day moving average of $62.12 and its 200-day moving average of $57.90, and the 50-day has crossed above the 200-day to form what technicians call a golden cross. That configuration is generally interpreted as a medium-term bullish signal, indicating that recent price momentum is outpacing the longer-term trend rather than lagging behind it. The roughly $4.22 spread between the two averages gives the trend some room to breathe before either would be at risk of flipping negative, which is a reasonable cushion for a stock in CBU’s price range.

The one area that warrants attention is the current RSI reading of 39.6, which sits in the lower portion of neutral territory and is approaching oversold conditions. For a stock that has been trending upward over the past year, an RSI drifting toward 40 typically signals a consolidation phase or a modest pullback in progress rather than a fundamental deterioration. It is not an alarm bell, but it does suggest that near-term price momentum has cooled, and buyers have not been as aggressive recently as they were during the earlier stages of the recovery.

For dividend investors, the overall setup is encouraging. The bullish trend structure confirmed by the golden cross, combined with a price sitting comfortably above both key moving averages, suggests the path of least resistance remains to the upside over a multi-month horizon. The softening RSI could present a more attractive entry point if the stock pulls back toward the $61 to $62 range near the 50-day average, giving income-focused buyers a chance to lock in a slightly higher yield before any renewed push toward the 52-week high.

Cash Flow Statement

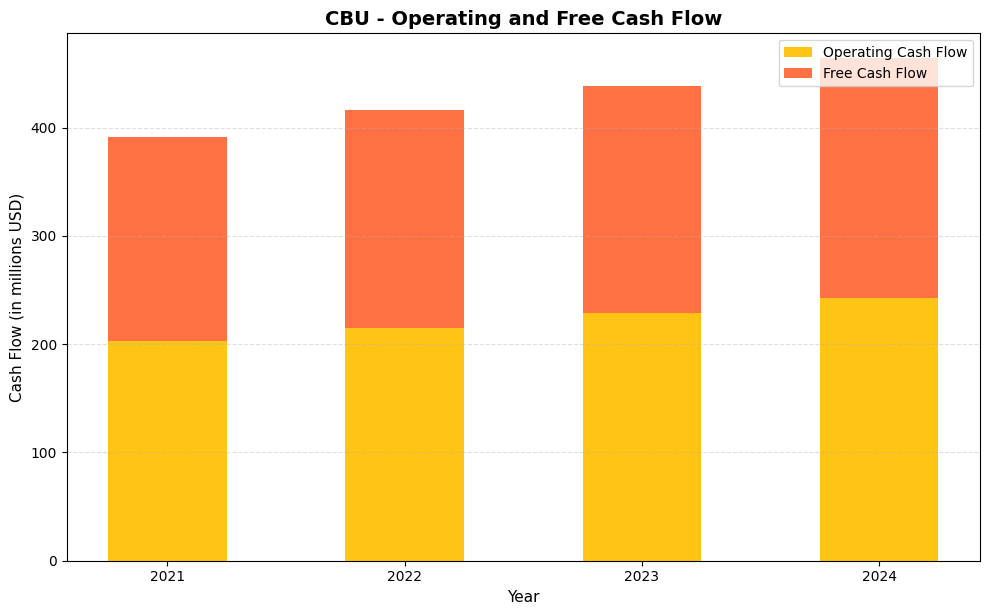

Community Bank System has delivered a steady and encouraging pattern of cash generation over the past four years, with operating cash flow climbing from $202.5 million in 2021 to $242.3 million in 2024, a gain of roughly 20% over that span. Free cash flow has tracked in close parallel, rising from $189.2 million to $221.6 million across the same period, which tells you that capital expenditure requirements remain modest and are not meaningfully consuming the cash the business produces. For dividend investors, that spread between operating and free cash flow is the number that matters most, and CBU’s consistent ability to convert nearly all of its operating cash into free cash flow provides a durable foundation for its dividend obligations. A bank that can grow its distributable cash at a low-to-mid single-digit annual rate while keeping capex disciplined is exactly the kind of profile that supports uninterrupted and growing dividend payments over a full economic cycle.

Zooming out across the full four-year window, CBU has added approximately $39.8 million in annual operating cash flow and $32.4 million in annual free cash flow without any sudden jumps or worrying reversals, which reflects genuine operational consistency rather than a one-year anomaly. The year-over-year increments are measured and predictable, with each year building modestly on the last, and that kind of cadence tends to reduce the risk of dividend cuts caused by cash flow volatility. Capital efficiency here is genuinely attractive, as the gap between operating and free cash flow has stayed narrow and relatively stable, hovering around $20 million annually, suggesting the company is not being forced to reinvest heavily just to maintain its earnings power. For shareholders collecting the dividend, that combination of growing free cash flow and restrained reinvestment needs means CBU is generating an expanding pool of capital that management can allocate toward dividend increases, opportunistic acquisitions, or balance sheet strength.

Analyst Ratings

Six analysts currently cover Community Bank System, and the consensus has settled at a hold rating as of this update. No specific named analyst actions are available in the current data, but the price target distribution provides a useful read on where professional sentiment sits. The mean 12-month price target of $68.33 represents roughly 7.6% upside from the current price of $63.48, while the high target of $73.00 implies potential appreciation of nearly 15%. The low target of $62.00 sits just below the current price, suggesting the most cautious analyst on the coverage list sees limited near-term catalysts but is not concerned about meaningful downside.

That spread from $62.00 to $73.00 reflects a community of analysts who are generally supportive of CBU’s fundamentals but are waiting for clearer signals before turning more constructive. At a P/E of 15.99 and a price-to-book of 1.67, the stock is trading at a modest premium to many regional bank peers, which may account for some of the hesitation to move to a buy rating despite solid underlying numbers. For dividend-focused investors, however, the hold consensus paired with a mean target above the current price is a reasonable setup. It suggests limited downside risk while preserving meaningful participation in any re-rating as earnings continue to grow.

Earning Report Summary

Community Bank System, Inc. has continued to build on the strong earnings momentum established through 2024, with trailing twelve-month EPS of $3.97 representing a notable step up from the $3.47 reported in the prior update. Net income of $210.5 million on $796.9 million in revenue reflects a business that is growing its top line while also expanding its margin profile, with the profit margin improving to 26.41% from approximately 25% in the comparable prior period.

Revenue and Lending Growth

Total revenue of $796.9 million on a trailing basis marks continued expansion for a bank that has grown steadily through a combination of organic loan growth and strategic investment in fee-based services. Net interest income remains the core driver of results, supported by the bank’s deposit base and loan book positioning. Noninterest income from insurance, wealth management, and other financial services has continued to provide diversification that smooths out the revenue line relative to pure-play lenders more exposed to rate cycle volatility.

Leadership’s Take on the Quarter

CEO Dimitar Karaivanov has maintained a consistent message focused on operational efficiency, disciplined credit standards, and sustainable earnings growth. His emphasis on growing pre-tax, pre-provision net revenue per share as a core performance metric reflects an approach that prioritizes quality of earnings over short-term headline growth. The integration of CFO Marya Burgio Wlos into the executive team has added financial depth, and the bank’s capital ratios continue to reflect a well-managed institution operating with appropriate buffers above regulatory minimums.

Strong Capital and Forward Outlook

Return on equity of 11.17% and return on assets of 1.25% both represent improvements over the prior reporting period, confirming that the earnings improvement is translating into better capital efficiency. With a book value per share of $38.08 and a price-to-book of 1.67 times, the market is ascribing a reasonable premium to the franchise value that CBU has built in its core Northeast markets. The forward outlook remains centered on steady loan growth, continued fee income expansion, and incremental dividend increases backed by a payout ratio that provides ample room for future raises without pressuring the balance sheet.

Management Team

Community Bank System, Inc. (NYSE: CBU) is guided by an experienced leadership team that has shown steady hands in navigating growth and industry shifts. At the top is President and CEO Dimitar A. Karaivanov, who took over the role in early 2024. His background includes key roles within the company and the broader financial services sector, giving him a deep understanding of both internal operations and external market dynamics. Since stepping in, Karaivanov has focused on enhancing operating efficiency and maintaining the company’s steady financial trajectory.

The financial reins are in the hands of Marya Burgio Wlos, who was appointed Executive Vice President and Chief Financial Officer in March 2025. She brings a strong operational background in banking, including leadership experience at M&T Bank. Her skill set is expected to complement the current strategy and strengthen the bank’s focus on financial discipline as CBU continues to grow its earnings base and manage capital allocation decisions.

Also playing a central role is Jeffrey Levy, who was promoted to Chief Banking Officer at the start of 2024. With a long tenure at CBU and hands-on operational experience, Levy is seen as a critical driver in the company’s core banking expansion. Together, this leadership team blends continuity with fresh perspective, aiming to guide the bank through its next phase of growth with a firm focus on quality and service.

Valuation and Stock Performance

CBU shares are trading at $63.48 as of this update, within a 52-week range of $49.44 to $67.50. The stock has recovered meaningfully from the lower end of that range and is now trading in the upper quartile, reflecting sustained investor confidence in the bank’s earnings trajectory and dividend reliability. At a market capitalization of approximately $3.34 billion, CBU remains a mid-sized regional bank with enough scale to support diversified revenue but enough focus to maintain the operational efficiency that distinguishes it from larger, more complex institutions.

From a valuation perspective, the P/E ratio of 15.99 is a modest premium to many regional banking peers but is well-supported by the earnings growth CBU has delivered. EPS of $3.97 represents a meaningful improvement over the prior period’s $3.47, which means the multiple expansion in the stock price has been accompanied by actual earnings growth rather than multiple expansion alone. The price-to-book of 1.67 times, against a book value of $38.08 per share, similarly reflects a franchise premium that the market has consistently been willing to assign to CBU given its track record of stable returns and conservative balance sheet management.

The analyst consensus mean target of $68.33 suggests moderate upside from current levels, and with a beta of 0.81, CBU trades with less volatility than the broader market, making it a suitable holding for risk-conscious income investors who want equity participation without the swings that come with higher-beta financial names. The valuation picture is not cheap, but it is fair for what CBU delivers, and the combination of earnings growth, dividend increases, and capital strength provides a reasonable basis for the current price level.

Risks and Considerations

Interest rate sensitivity remains the most persistent risk for CBU and for regional banks broadly. Net interest income, which drives the majority of the bank’s revenue, is directly influenced by the shape of the yield curve and the level of short-term rates. If rates decline faster than expected or the curve flattens again for an extended period, margin compression could slow the earnings growth that has supported recent dividend increases and stock performance.

Competition in CBU’s core markets is another factor that income investors should monitor. Larger national banks have been investing heavily in digital capabilities and branch expansion in regional markets, while fintech lenders continue to compete for consumer and small business loan originations. Holding deposit costs low while growing the loan book at acceptable spreads requires ongoing discipline, and that task is unlikely to become easier as the competitive landscape evolves.

Regulatory complexity grows alongside CBU’s financial services footprint. As the bank expands in areas like insurance and wealth management, the compliance burden increases in scope. Managing that complexity without allowing it to erode margins requires continued investment in risk and compliance infrastructure, and any missteps in that area could attract regulatory attention that distracts management from core growth priorities.

The broader economic sensitivity of CBU’s Northeast markets also warrants attention. While the region has been relatively stable, a meaningful deterioration in employment, housing, or local business conditions could affect loan performance and demand for financial services. Credit quality metrics have been clean in recent periods, but that picture can shift if economic conditions in the bank’s footprint weaken more than current expectations suggest.

Final Thoughts

CBU presents a compelling story of consistent execution, solid leadership, and a conservative approach to balance sheet management. The stock is not trying to win attention with dramatic growth numbers or transformational deals. Instead, it leans into what it does best: delivering steady earnings, maintaining a strong capital position, and growing the dividend at a pace the business can genuinely support. The move from a $0.46 to $0.47 quarterly payout may not generate headlines, but it is exactly the kind of incremental, sustainable progress that dividend growth investors build long-term wealth around.

Management appears focused and aligned with shareholder interests. Financial performance has improved meaningfully, with EPS rising to $3.97 and net income crossing $210 million, and the payout ratio compression to 46.85% leaves more room for future dividend growth than existed in prior periods. The valuation at roughly 16 times earnings and 1.67 times book is not a bargain, but it is appropriate for a bank with CBU’s track record and the quality of its earnings stream.

For income-oriented investors looking for a regional bank that can hold its ground through changing economic cycles, CBU continues to be a name worth owning. It is not flashy, and the yield at 2.96% will not satisfy investors chasing maximum income. But for those who value dividend safety, consistent growth, and a management team that has earned trust over time, CBU checks the right boxes and remains a solid core holding in a dividend growth portfolio.