Updated 2/25/26

Comfort Systems USA (NYSE: FIX) is a national leader in mechanical and electrical contracting, serving commercial, industrial, and institutional clients across the country. The company has built a reputation for consistent execution, strong cash flow, and disciplined capital allocation. Backed by a growing project backlog and a return on equity now exceeding 49%, FIX continues to deliver both earnings growth and operational strength. Its dividend, while modest in yield, has seen extraordinary growth over the past two years, with a payout ratio of just 7.2%, leaving substantial room for continued increases. The stock has surged dramatically, trading near $1,450 as of late February 2026, and the company’s financials reflect record profitability, with management maintaining a constructive outlook. Supported by a seasoned leadership team and exceptional financial footing, FIX has positioned itself as a resilient, income-generating industrial name with compelling long-term potential.

Recent Events

Comfort Systems USA has continued to generate significant attention across the industrial and engineering sectors heading into early 2026. The company’s revenue has climbed to over $9.1 billion on a trailing basis, reflecting a business that has scaled meaningfully over the past several years. Operating cash flow has reached nearly $1.19 billion, and free cash flow stands at approximately $774 million, reinforcing the financial strength that has made FIX one of the more closely watched names in industrial contracting.

The stock itself has been one of the more remarkable performers in the market, rising from a 52-week low near $276 to an all-time high approaching $1,500. That kind of range reflects both the market’s repricing of the company’s earnings power and growing conviction among institutional investors that FIX’s exposure to data center construction, advanced manufacturing, and infrastructure modernization is genuinely durable rather than cyclical. Short interest remains low at roughly 732,000 shares, suggesting the skeptic camp has largely stepped aside.

The company’s profit margin has expanded to 11.23%, and net income has crossed $1 billion on a trailing twelve-month basis, a milestone that underscores just how much the business has matured operationally. With a return on equity of 49.24% and a return on assets of 14.71%, FIX is generating exceptional results relative to the capital it deploys, and the market capitalization has now eclipsed $51 billion, placing it firmly among the largest names in its sector.

Key Dividend Metrics 📊

💰 Forward Annual Dividend: $2.25

📈 Most Recent Quarterly Payment: $0.60 per share

📆 Last Dividend Payment Date: November 13, 2025

📉 Payout Ratio: 7.20%

📅 Trailing Dividend Growth (2023 to 2025): Over 240% cumulative increase

🔁 Recent Dividend Growth: $0.35 to $0.60 per quarter, a 71% increase year over year

Dividend Overview

At a yield that rounds to roughly 0.15% at current prices, FIX is not the stock you buy when you need income today. But the dividend story here is not about the current yield. It is about the trajectory, and that trajectory has been exceptional. The company paid $0.175 per quarter in early 2023 and has since raised the dividend to $0.60 per quarter as of November 2025, representing a cumulative increase of more than 240% in less than three years. Very few companies of any size, in any sector, can point to dividend growth at that pace.

The payout ratio of just 7.2% is the other key data point. With earnings per share at $23.64 and the annualized dividend at $2.25, Comfort Systems is returning only a small fraction of what it earns to shareholders through the dividend. That is not stinginess. That is a company with enormous confidence in its future earnings power, choosing to reinvest aggressively while still signaling commitment to shareholders through consistent and rapidly growing distributions.

For investors building a dividend growth portfolio with a long time horizon, FIX represents a model of how compounding dividend increases can eventually produce meaningful yield on cost, even when the starting yield appears modest. Those who bought shares three years ago are earning a substantially higher effective yield today than the headline number suggests for new buyers.

Dividend Growth and Safety

The dividend history for FIX reads like a master class in confident capital allocation. From $0.175 per quarter in March 2023 through eight consecutive increases to $0.60 per quarter in November 2025, management has demonstrated a willingness to share the company’s expanding earnings in a meaningful and accelerating way. The move from $0.35 in the fourth quarter of 2024 to $0.60 in the fourth quarter of 2025 alone represents a 71% year-over-year increase in the quarterly payment, which is a remarkable figure for a company with a $51 billion market cap.

Safety is equally compelling. With a payout ratio of 7.2% and free cash flow of $774 million against an annual dividend obligation that is a fraction of that figure, Comfort Systems could absorb a severe and prolonged earnings contraction and still comfortably fund its dividend. The company’s operating cash flow of nearly $1.19 billion provides an additional cushion, as the dividend is covered many times over by cash generated from the business rather than relying on balance sheet maneuvers.

The nature of the underlying business adds another layer of durability. Comfort Systems serves clients in sectors like data center construction, advanced manufacturing, and institutional facilities, where demand for mechanical, electrical, and plumbing systems is tied to long-term infrastructure buildout rather than discretionary spending. These are projects that get funded through multi-year capital programs, which provides a degree of revenue visibility that pure-play construction companies often lack. Return on equity at 49.24% and return on assets at 14.71% confirm that the business model is generating outstanding results at the operating level, and that operational strength is what ultimately underlies dividend safety.

Chart Analysis

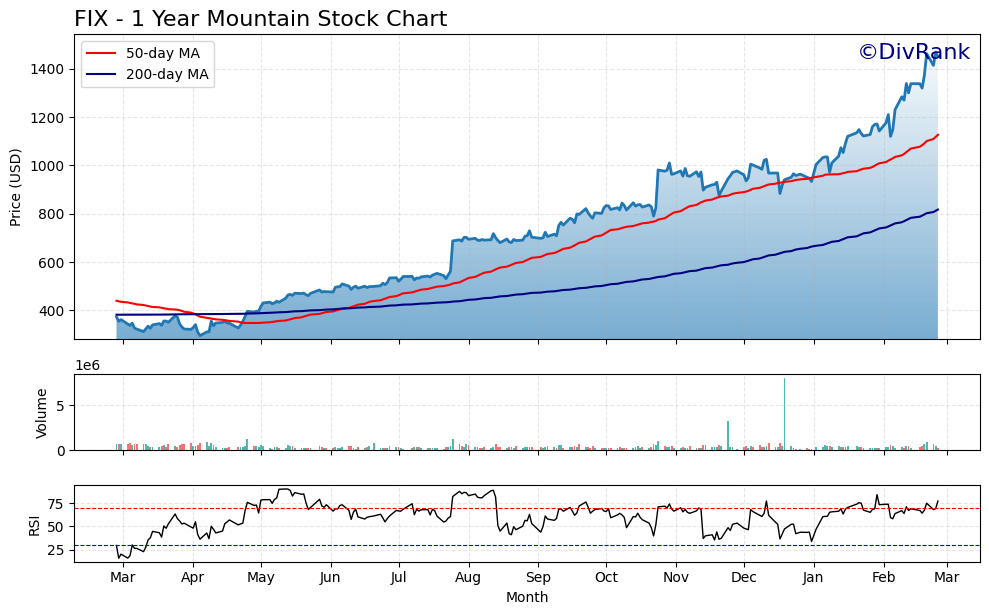

FIX has delivered a remarkable price run over the past year, climbing from a 52-week low of $295.83 to its current level of $1,450.03, a gain of roughly 390% from trough to present. That kind of price appreciation is unusual for a mechanical services contractor and reflects a dramatic rerating of the business by the market. The stock is now trading within 1.26% of its 52-week high of $1,468.58, which means buyers have remained aggressive right up to the most recent sessions with virtually no meaningful pullback from peak levels.

The moving average picture is unambiguously constructive. FIX is trading well above both its 50-day moving average of $1,126.52 and its 200-day moving average of $817.38, and the 50-day has crossed above the 200-day to form a golden cross, a technical configuration that typically signals a sustained uptrend rather than a short-term bounce. The spread between the current price and the 200-day average is exceptionally wide at roughly 77%, which tells you this rally has been steep and fast rather than a slow grind higher. That kind of distance from the long-term average can be a sign of strength, but it also means the stock would have significant room to correct before any technical damage would appear on the longer-term trend.

The RSI reading of 77.21 places FIX firmly in overbought territory, above the conventional threshold of 70 that many traders use as a caution signal. Momentum is clearly strong, but an RSI at this level historically increases the probability of a consolidation period or a modest pullback as the price digests its gains. This does not imply a trend reversal, but investors adding a new position at current levels should be aware that buying into an overbought condition often means enduring some short-term choppiness before the next leg higher materializes.

For dividend investors, the technical setup presents a nuanced picture. The underlying trend is solidly bullish, and the golden cross confirms that institutional buying has been persistent and broad-based. However, the combination of an RSI above 77 and a price sitting less than 2% from a 52-week high suggests that patience may be rewarded here. Investors who prioritize entry price and yield-on-cost would be well served by monitoring for any pullback toward the $1,126 area near the 50-day average, which would represent a more favorable risk-adjusted entry without abandoning the bullish thesis the chart otherwise supports.

Cash Flow Statement

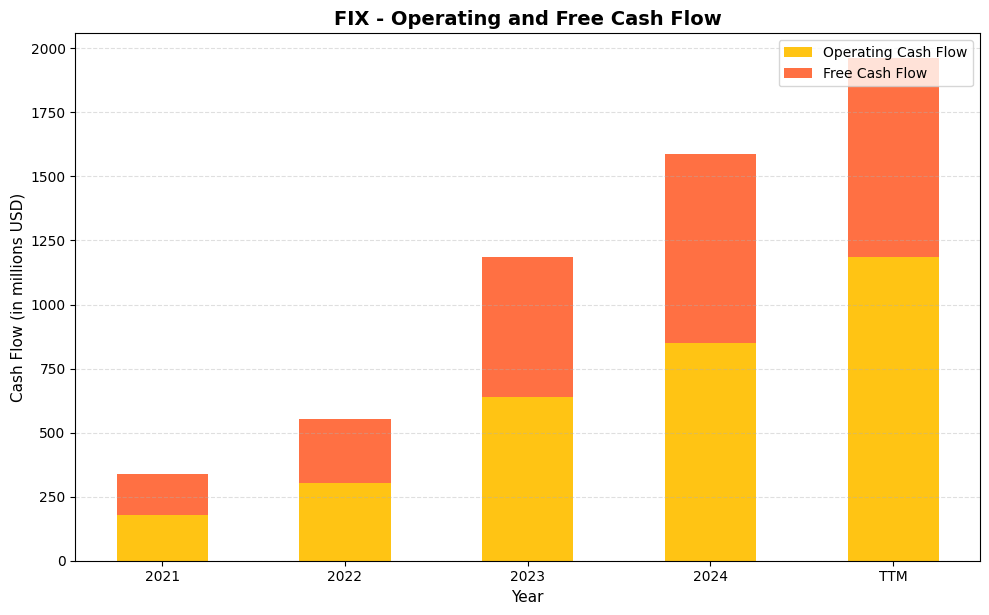

Comfort Systems USA has generated a remarkable surge in cash production over the past four years, with operating cash flow climbing from $180.2 million in 2021 to $849.1 million in 2024, and trailing twelve months figures now sitting at $1,186.4 million. Free cash flow has followed the same trajectory, rising from $157.8 million in 2021 to $738.0 million in 2024 before reaching $774.2 million on a TTM basis. For dividend investors, these numbers tell a compelling story about sustainability. The company’s current dividend obligation consumes a small fraction of the free cash flow being generated, leaving substantial room for continued dividend growth, share repurchases, and opportunistic acquisitions without any meaningful strain on the balance sheet.

What makes this trend particularly impressive is the consistency and acceleration of the improvement. From 2021 to 2024, free cash flow grew at a compounded rate that reflects not just revenue expansion but genuine operating leverage, with the conversion from operating cash flow to free cash flow remaining highly efficient throughout the period. Capital expenditures have stayed disciplined relative to the cash being produced, as evidenced by the narrow gap between operating and free cash flow in every year shown. The jump between 2022 and 2023 alone, where free cash flow nearly doubled from $253.2 million to $544.7 million, signals a business that hit an inflection point in its earnings model. Shareholders are the clear beneficiaries of this dynamic, as a company generating nearly $775 million in annual free cash flow has considerable flexibility to reward income investors while simultaneously funding the organic and acquisition-driven growth that has powered this cash flow expansion in the first place.

Analyst Ratings

The analyst community has maintained a strong buy consensus on Comfort Systems USA as of late February 2026, with five analysts covering the stock and a mean price target of $1,696.20. That consensus target implies meaningful upside from the current trading price near $1,450, and the range of estimates from $1,611 on the low end to $1,800 at the high end suggests that even the more conservative voices in the group see room for appreciation from current levels.

The breadth of the price target range, spanning nearly $190 from floor to ceiling, reflects some divergence in assumptions around the pace of the company’s backlog conversion, margin sustainability, and the duration of the data center and manufacturing construction cycle that has driven much of FIX’s recent growth. However, the fact that all targets sit above the current price, and that the consensus is the highest available rating, indicates broad conviction in the company’s near-term earnings trajectory. With EPS at $23.64 and the stock trading at a P/E of approximately 61, analysts are clearly pricing in continued earnings growth to justify current and higher valuations. The strong buy consensus, combined with a mean target roughly 17% above current prices, suggests the analyst community believes that growth is achievable.

Earnings Report Summary

Strong Start to the Year

Comfort Systems USA delivered record financial results over the trailing twelve-month period, with revenue climbing to over $9.1 billion, net income exceeding $1 billion, and earnings per share reaching $23.64. These figures represent a dramatic expansion from prior periods and reflect the company’s deepening involvement in large-scale data center, semiconductor fabrication, and advanced manufacturing projects, which have driven both volume and margin improvement simultaneously. Gross margins and operating margins have expanded alongside revenue, a combination that rarely persists for long in contracting businesses and that speaks to the quality of FIX’s project selection and execution capabilities.

Backlog Tells the Real Story

The company’s project backlog has remained a central driver of investor confidence. Comfort Systems has consistently reported backlog figures that point to strong visibility into future revenue, and the composition of that backlog, weighted toward technology infrastructure and manufacturing rather than general commercial construction, carries higher margins and longer contract durations than the historical mix. Management has signaled continued demand from customers planning large capital expenditure programs, particularly in areas tied to artificial intelligence infrastructure and domestic manufacturing expansion, both of which require extensive mechanical and electrical systems work.

Operational Efficiency Drives Profitability

Profit margins at 11.23% represent a notable achievement for a contracting business, where single-digit margins are the norm. Return on equity at 49.24% is exceptional by any measure and reflects the company’s ability to generate earnings well in excess of the capital base required to run the business. Operating cash flow of nearly $1.19 billion confirms that profitability is translating into real cash generation rather than accounting-driven results. These figures collectively describe a business operating at a high level of efficiency, and they provide the financial foundation for continued dividend growth and capital reinvestment.

Management’s Outlook

Brian Lane and the leadership team have maintained a constructive tone regarding the demand environment heading into 2026, pointing to the strength of customer relationships and the scale of the company’s backlog as indicators that the current growth phase has duration. Management has also acknowledged the importance of workforce capacity and project execution as the business operates at elevated volumes, and the company’s investment in training and retention has been a consistent theme in leadership commentary. The overall message from the executive team has been one of disciplined optimism, grounded in specific project wins and customer commitments rather than general macroeconomic enthusiasm.

Management Team

Comfort Systems USA is led by a highly experienced and stable leadership group. Brian E. Lane, who has served as CEO and President since 2011, brings more than 30 years of experience in engineering and construction. Before joining the company, Lane held leadership roles in business development and strategic planning at firms like Halliburton and Capstone Turbine. Under his direction, Comfort Systems has transformed from a regional contracting business into one of the largest and most profitable mechanical and electrical contractors in the United States, with revenue now exceeding $9 billion and a market capitalization above $51 billion.

The board of directors complements management with a wide range of expertise, including legal, financial, real estate, and engineering backgrounds. Individuals like Franklin Myers and Herman E. Bulls contribute oversight grounded in decades of corporate and financial experience. The diversity in thought and industry knowledge within the boardroom helps guide long-term strategy and ensures thoughtful risk management across the business. The consistency of the leadership team over many years has been a meaningful contributor to the company’s operational culture and its track record of execution through varying market conditions.

Valuation and Stock Performance

Comfort Systems USA is trading near $1,450 as of late February 2026, just below its 52-week high of approximately $1,500 and well above the 52-week low near $276. The scale of that range, more than a fivefold move within a single year, reflects the market’s dramatic reassessment of the company’s earnings power and competitive positioning as the data center and advanced manufacturing construction cycle has accelerated. The stock’s long-term performance is even more striking, with gains that have compounded far beyond what most industrial names have delivered over the same period.

The current P/E ratio of 61.34 is elevated by historical standards for a contracting company, and it demands continued earnings growth to remain justifiable on a fundamental basis. Price-to-book at 20.80 against a book value of $69.73 per share similarly reflects a premium that the market has assigned based on the company’s exceptional return on equity and the perceived durability of its growth drivers. Analysts see the current valuation as reasonable given the trajectory, with a consensus price target of $1,696.20 implying roughly 17% upside from current levels. The low end of analyst targets at $1,611 still sits above the current price, which provides a degree of support for the view that the stock is not dramatically overvalued relative to near-term expectations, even at elevated multiples.

Risks and Considerations

The most significant risk facing Comfort Systems at current valuation levels is the cyclicality of its end markets. The company’s recent revenue and earnings growth has been heavily influenced by a surge in data center construction and advanced manufacturing projects, both of which are tied to capital spending decisions by a relatively concentrated group of large technology and industrial companies. If those customers slow their buildout programs, whether due to changes in AI investment timelines, financing costs, or broader economic conditions, FIX’s backlog and revenue could face meaningful pressure that the current stock price does not reflect.

Labor availability and cost inflation remain persistent operational challenges across the contracting industry. Comfort Systems has managed these factors well relative to peers, but the company is operating at elevated volumes and the ability to recruit, train, and retain skilled tradespeople at scale is not unlimited. Any deterioration in workforce availability or unexpected wage inflation could compress margins in ways that would be difficult to offset quickly through pricing adjustments on existing contracts.

The valuation itself represents a form of risk. At a P/E above 61 and a price-to-book above 20, the stock is priced for continued exceptional performance. Any earnings miss, guidance reduction, or shift in market sentiment toward industrial cyclicals could produce significant price volatility given the beta of 1.67. Investors entering at current prices are accepting meaningful downside exposure in a scenario where growth merely moderates rather than accelerates further.

The company’s decentralized operating model, while a source of flexibility and local expertise, introduces consistency and oversight challenges as the business continues to scale rapidly. Regulatory risk tied to energy efficiency standards, environmental requirements, and building codes also warrants attention, as changes in these areas can affect project economics and delivery timelines in ways that are difficult to anticipate or price into long-term contracts.

Final Thoughts

Comfort Systems USA has evolved into one of the most compelling growth and income stories in the industrial sector, a combination that is genuinely rare. The leadership team has navigated an extended period of rapid expansion with operational discipline, and the financial results, including over $1 billion in net income, nearly $1.2 billion in operating cash flow, and a return on equity approaching 50%, reflect a business operating at an exceptionally high level. The dividend growth story, with quarterly payments rising from $0.175 to $0.60 in under three years, is among the most impressive in the contracting space, and the 7.2% payout ratio ensures that further increases are well within reach.

The risks are real, particularly the valuation premium and the concentration of recent growth in a handful of end markets that could prove more cyclical than current sentiment suggests. But for investors with a long time horizon and an appreciation for compounding dividend growth rather than current yield, FIX remains one of the more interesting names available in the industrials universe. The company continues to demonstrate why it has earned its place as a core holding among investors who value operational excellence, financial strength, and a management team with a demonstrated commitment to growing shareholder returns over time.