Key Takeaways

📈 Dividend Yield and Growth: Colgate-Palmolive offers a steady 2.10% yield, extending its remarkable dividend growth streak to 62 consecutive years.

💰 Cash Flow: Operating cash flow of $4.2 billion and free cash flow of $3.1 billion continue to underpin dividend reliability.

📊 Analyst Ratings: The consensus among 19 analysts is a buy, with price targets ranging from $87 to $105 and a mean target of $96.68.

📝 Earnings Report Summary: Full-year EPS of $2.63 reflects steady profitability, supported by pricing discipline and resilient demand across core categories.

👥 Management Team: CEO Noel Wallace continues to lead with a focus on innovation, sustainability, and disciplined capital allocation.

Updated 2/25/26

Colgate-Palmolive (CL) has spent decades earning its reputation as one of the most dependable names in consumer staples, and that reputation remains intact heading into 2026. With a brand portfolio spanning oral care, personal care, home care, and pet nutrition through Hill’s, the company generates steady demand across economic cycles and geographies. Management continues to prioritize operational efficiency and long-term brand investment while returning capital to shareholders with remarkable consistency.

The stock currently trades at $96.67, near the top of its 52-week range of $74.55 to $100.18, and carries a forward dividend yield of 2.10% backed by an annual payment of $2.08 per share. The 62-year dividend growth streak, combined with $4.2 billion in operating cash flow, makes this a name that income investors have long favored for its ability to quietly compound through market volatility. The analyst consensus has shifted to a buy, with a mean price target of $96.68 sitting almost precisely at the current price.

Recent Events

Colgate-Palmolive has been navigating a global operating environment that continues to test consumer staples companies broadly, with currency headwinds, input cost pressures, and shifting consumer behavior in key international markets all demanding management attention. The company has responded by leaning into pricing discipline and cost efficiency, and those efforts are showing up in improved cash generation relative to recent years. Operating cash flow climbed to $4.2 billion on a trailing basis, a meaningful step up from prior periods and a sign that the underlying business model is performing well despite the noise.

On the product front, Colgate has continued investing in its oral care innovation pipeline, with premium products under the Colgate and Elmex brands gaining traction in key markets. Hill’s Pet Nutrition has remained a standout performer, benefiting from the durable consumer trend toward premium pet food, and management has signaled continued investment in that segment’s capacity and product development. The company has also been navigating potential tariff implications on cross-border manufacturing, particularly regarding production activity tied to Mexico, and leadership has indicated contingency planning is underway to manage those exposures should conditions change. Return on assets came in at 16.36%, and the profit margin of 10.46% reflects a business that is still working through some cost normalization while maintaining its core earnings power.

Key Dividend Metrics

📈 Forward Dividend Yield: 2.10%

💸 Annual Dividend Rate: $2.08 per share

📅 Last Ex-Dividend Date: January 21, 2026

📊 Payout Ratio: 78.33%

📉 5-Year Average Dividend Yield: 2.29%

🔁 Dividend Growth Streak: 62 years and counting

💵 Most Recent Quarterly Payment: $0.52 per share

Dividend Overview

For income investors who prize reliability above all else, Colgate-Palmolive remains one of the most compelling names available. The company extended its dividend growth streak to 62 consecutive years in 2025, when it raised its quarterly payment from $0.50 to $0.52, pushing the annualized rate to $2.08 per share. That increase, modest as it may appear, is a continuation of a pattern that has rewarded patient shareholders through recessions, market crashes, and global disruptions alike.

At the current price of $96.67, the forward yield sits at 2.10%, which is modestly below the five-year average of 2.29%. That compression reflects a stock price that has moved meaningfully higher from the lower end of its 52-week range at $74.55, rather than any deterioration in the dividend itself. For investors who initiated positions at lower prices over the past year, the yield on cost is considerably more attractive.

The payout ratio has risen to 78.33% based on trailing EPS of $2.63, which is higher than levels seen in prior years. That warrants monitoring, but it should be viewed in context. Colgate’s free cash flow of $3.1 billion provides substantial coverage for the roughly $1.7 billion in annual dividend obligations, and the company’s non-capital-intensive business model means that free cash flow consistently runs well above reported net income. The dividend is well-supported on a cash basis even if the earnings-based payout ratio looks elevated.

Dividend Growth and Safety

Colgate’s approach to dividend growth has always been measured rather than aggressive, and that deliberate pace is a feature rather than a limitation. The raise from $0.50 to $0.52 per quarter in April 2025 represented a 4% increase, consistent with the low-to-mid single digit growth rates the company has delivered over many years. For investors compounding dividends over decades, that steady cadence builds meaningful income streams over time.

The safety of the dividend rests on a foundation of strong and growing cash flow. Operating cash flow of $4.2 billion for the trailing twelve months is an improvement over prior periods, and free cash flow of $3.1 billion comfortably exceeds the annual dividend outlay by a wide margin. Even accounting for debt service and capital expenditure commitments, Colgate retains substantial financial flexibility. The company does carry a significant debt load, but its ability to generate cash consistently has historically allowed it to manage that leverage without compromising shareholder returns.

The stock’s beta of 0.29 is one of the lowest among large-cap consumer staples names, reflecting the defensive nature of Colgate’s product categories. Toothpaste, soap, and pet food are not discretionary purchases, and demand for these products holds up in economic downturns in ways that cyclical businesses cannot match. That low-volatility characteristic is particularly valuable for income investors who rely on their portfolios for current income and cannot afford large drawdowns. When equity markets experience the kinds of sharp corrections that have become increasingly common, Colgate tends to provide the portfolio ballast that defensive allocations are meant to deliver.

Chart Analysis

Colgate-Palmolive has staged an impressive recovery over the past twelve months, climbing from a 52-week low of $74.52 to its current price of $96.67, a gain of nearly 30% from trough to present. That kind of price appreciation in a consumer staples name reflects a meaningful shift in investor sentiment, and the stock now sits just 1.47% below its 52-week high of $98.11. For a defensive dividend grower, that proximity to a yearly peak signals that the market has been consistently rewarding buyers rather than punishing them, and the overall trend across the past year reads as a steady, orderly advance rather than a volatile spike.

The moving average picture reinforces that constructive view. CL is trading above both its 50-day moving average of $85.97 and its 200-day moving average of $83.71, with the 50-day now sitting above the 200-day in what technicians call a golden cross formation. That alignment is broadly bullish, indicating that shorter-term momentum is running in the same direction as the longer-term trend. The spread between the current price and the 200-day average is roughly $13, or about 15%, which suggests the stock has moved meaningfully off its base without the kind of parabolic extension that would raise concerns about an overheated chart.

The Relative Strength Index currently reads 59.23, placing CL in a constructive middle zone that is neither overbought nor neutral to the point of suggesting stalled momentum. Readings above 70 would flag potential exhaustion, while readings below 40 would indicate selling pressure. At 59, the stock retains room to continue its advance toward that 52-week high without immediately triggering overbought signals. Momentum at this level tends to favor continuation rather than reversal, particularly in a low-volatility sector where price moves are typically measured and gradual.

For dividend investors, the technical setup here is genuinely supportive. Buying a dividend grower when it is trending above both major moving averages, carrying moderate RSI, and trading near a yearly high reduces the risk of purchasing into a deteriorating price trend that erodes total return while you wait to collect income. CL’s chart does not suggest a screaming entry at a discounted price, but it does suggest a stock in good technical health, which is exactly the kind of environment where a long-term income position can be initiated or added to with reasonable confidence in near-term price stability.

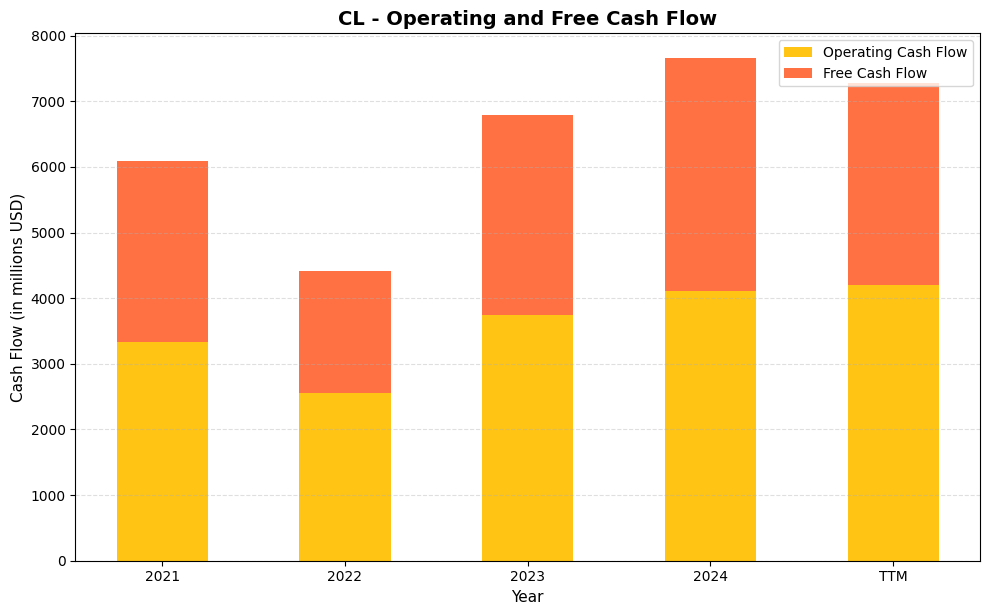

Cash Flow Statement

Colgate-Palmolive’s cash generation has strengthened considerably over the past two years, and the numbers make a compelling case for dividend sustainability. Operating cash flow climbed from a trough of $2,556.0M in 2022 to $3,745.0M in 2023 and then to $4,107.0M in 2024, with the trailing twelve months pushing even higher to $4,198.0M. Free cash flow followed the same trajectory, recovering from $1,860.0M in 2022 to $3,040.0M in 2023 and $3,546.0M in 2024. With CL’s annual dividend obligation running well below its free cash flow generation, the payout is covered with meaningful room to spare, which is precisely the kind of cushion long-term income investors should want to see.

Stepping back across the full five-year window, the 2022 dip now reads as a temporary compression rather than a structural deterioration, driven largely by working capital headwinds and cost inflation that pressured margins at the time. The subsequent recovery was sharp and sustained, with free cash flow in 2024 running approximately 28% above the 2021 level of $2,758.0M. The gap between operating cash flow and free cash flow, which reflects capital expenditures, has remained relatively stable, suggesting CL is not sacrificing reinvestment to manufacture better headline numbers. For shareholders, the combination of rising absolute cash generation and disciplined capital spending points to a business that can continue funding both its dividend growth commitment and its ongoing brand investment without straining its balance sheet.

Analyst Ratings

The analyst community has moved to a more constructive stance on Colgate-Palmolive, with the consensus among 19 covering analysts currently sitting at a buy. That represents a more positive collective view than was evident in prior periods, when hold ratings dominated the landscape. The mean price target of $96.68 lands almost exactly at the current trading price of $96.67, which suggests analysts see the stock as fairly valued at current levels rather than meaningfully undervalued or overvalued relative to their models.

The range of price targets spans from a low of $87 to a high of $105, reflecting genuine dispersion in views about near-term earnings power and the trajectory of margins as input cost pressures evolve. The $87 floor implies limited downside risk is being priced in by the most cautious analysts, while the $105 ceiling from the most optimistic targets suggests approximately 9% upside if Colgate executes well on its cost efficiency and pricing initiatives through 2026. With the stock trading so close to the consensus mean target, investors considering new positions at current prices should weigh that the near-term price appreciation potential implied by analyst models is modest, though the income component and long-term compounding thesis remain intact regardless of short-term target proximity.

Earning Report Summary

Colgate-Palmolive delivered full-year results that reflected steady execution in a challenging global operating environment. Revenue for the trailing twelve-month period came in at approximately $20.4 billion, with earnings per share of $2.63 demonstrating the company’s ability to convert revenue into bottom-line results through disciplined cost management and pricing strategy. Net income of $2.13 billion represented a solid outcome given the currency headwinds and input cost normalization pressures that have been a consistent feature of the operating backdrop.

Segment Dynamics and Revenue Drivers

Oral care continues to anchor Colgate’s revenue base, with premium product innovation helping to sustain pricing power across developed and emerging markets. The company has been focused on trading consumers up within its oral care lineup, and while volume trends in certain markets have been softer due to affordability constraints, the mix shift toward higher-margin products has helped protect profitability. Hill’s Pet Nutrition has been a consistent bright spot, benefiting from secular tailwinds in pet humanization and the willingness of pet owners to maintain premium spending on animal health products even when overall household budgets are under pressure. That segment has contributed meaningfully to both revenue growth and margin improvement.

Profitability and Margins

The profit margin of 10.46% is below where Colgate has operated historically, and management has acknowledged the ongoing work required to restore margins toward prior peaks as raw material costs stabilize and pricing actions earn through. Return on assets of 16.36% remains healthy for the business model, while the extraordinary return on equity figure reflects the company’s capital-light approach and the mathematical effect of a very lean book value rather than anything unusual about the underlying business performance. Operating cash flow of $4.2 billion confirms that the core cash generation engine is running well, and free cash flow conversion remains strong relative to reported earnings.

Outlook and Management Commentary

CEO Noel Wallace has maintained a consistent message around investing in brand strength and innovation while managing costs with discipline. The company has flagged potential tariff-related impacts on its manufacturing cost structure, particularly around cross-border production, and management has indicated that contingency plans are in place to mitigate those risks through supply chain adjustments and domestic manufacturing alternatives if needed. CFO Stanley Sutula has emphasized that the company enters 2026 with flexibility on its balance sheet and confidence in its ability to sustain dividend growth, even if the macro environment remains unsettled. The overall tone from leadership is one of cautious confidence, acknowledging real-world challenges while reaffirming the long-term earnings power of the franchise.

Management Team

Colgate-Palmolive continues to operate under the leadership of Noel Wallace, who has served as Chairman, President, and Chief Executive Officer since 2018. Wallace has built a track record of steady execution, emphasizing brand investment, sustainability, digital transformation, and operational efficiency as the pillars of his strategic framework. His communication style has been consistent and measured, which tends to suit a company whose investor base prioritizes dependability over dramatic transformation. Under his tenure, Colgate has navigated significant macro disruptions while maintaining its dividend growth streak and improving cash flow generation.

Stanley Sutula continues as Chief Financial Officer, providing financial rigor and clarity around capital allocation priorities. The broader executive team brings deep experience in international operations, supply chain management, legal and regulatory affairs, and marketing, reflecting the complexity of running a consumer products business across more than 200 countries and territories. The team has demonstrated alignment around shareholder return priorities while balancing reinvestment in the brands and capabilities that support long-term competitiveness. That consistency of leadership and strategy is itself a form of risk management for investors evaluating the durability of the dividend and the business.

Valuation and Stock Performance

Colgate-Palmolive trades at $96.67, sitting near the upper portion of its 52-week range of $74.55 to $100.18. The stock has recovered substantially from its 52-week low, a move that reflects both improved investor sentiment toward defensive consumer staples names and confidence in Colgate’s cash flow resilience. The trailing P/E ratio of 36.76 is elevated relative to the broader market and above where Colgate has historically traded, which reflects in part the compression in EPS from margin pressures and in part the premium that investors have been willing to assign to highly predictable, dividend-growing businesses in an uncertain economic climate.

For investors accustomed to evaluating Colgate on an earnings multiple basis, the current P/E may give pause. However, the more relevant lens for income investors is cash flow valuation, and on that basis the picture is more reasonable given the $3.1 billion in free cash flow the business generates against a market capitalization of approximately $78 billion. The mean analyst price target of $96.68 suggests the stock is fairly valued at current prices by the covering analyst community, which means the investment case here rests primarily on the income stream and dividend growth rather than on near-term price appreciation. For investors who purchased shares earlier in the 52-week range, the position looks considerably more attractive on both a yield and total return basis, and that dynamic highlights why building positions in quality dividend growers during periods of price weakness tends to reward patience over time.

Risks and Considerations

Currency volatility remains one of the most persistent and difficult-to-control risks for Colgate given its exposure to more than 200 markets globally. A strengthening U.S. dollar directly erodes the reported value of overseas earnings and cash flows, and while the company uses hedging strategies to partially offset these impacts, a sustained period of dollar strength can meaningfully weigh on reported results. Emerging market currencies in particular have shown volatility in recent years that has created headwinds in regions where Colgate has significant revenue exposure.

The payout ratio of 78.33% based on trailing earnings deserves ongoing attention. While free cash flow coverage of the dividend remains comfortable, any material deterioration in earnings from cost pressures, volume declines, or currency headwinds could bring the earnings-based payout ratio into a range that prompts investor concern, even if the cash flow reality remains sound. Dividend growth investors should monitor the trajectory of EPS recovery and margin restoration as a key variable in assessing the company’s capacity for continued annual raises.

Input cost dynamics, including raw materials such as palm oil, resins, and packaging materials, remain a variable that management does not fully control. While pricing actions have helped recover some of these costs, competitive dynamics in certain categories limit the degree to which Colgate can continuously pass through higher costs without sacrificing volume. The balance between protecting margin and maintaining market share is an ongoing tension that has shown up in recent results.

Geopolitical risk, including potential tariffs on goods manufactured in Mexico and other cross-border supply chain exposures, adds a layer of uncertainty to the cost outlook for 2026. Management has indicated contingency planning is underway, but the actual impact will depend on policy decisions that remain outside the company’s control. Regulatory and legal risks around product ingredients and labeling requirements across different jurisdictions also represent ongoing background risk for a company that sells consumer health and hygiene products at global scale.

Final Thoughts

Colgate-Palmolive enters 2026 as what it has always been: a steady, cash-generative, globally diversified consumer brands business with an unmatched dividend growth track record. Sixty-two consecutive years of dividend increases is not an accident. It reflects the durability of the underlying business, the discipline of successive management teams, and the enduring demand for the kinds of everyday products that Colgate sells regardless of what the economic cycle is doing.

The stock is not obviously cheap at current prices, with the P/E at 36.76 and the mean analyst target essentially at the current trading level. Investors entering here are paying a fair price for a high-quality franchise rather than getting a bargain, and the near-term upside from price appreciation alone is limited according to current analyst models. The investment case is therefore most compelling for income-focused investors who value the 2.10% yield, the annual dividend growth, and the low-beta stability that Colgate brings to a diversified portfolio.

For those investors, Colgate continues to do what it has always done: generate reliable cash flows, return capital consistently, and navigate global complexity with operational discipline. That combination may not generate excitement, but it has produced decades of compounding income and capital preservation, which is exactly what dividend growth investing is designed to deliver.