Updated 2/25/26

Cogent Communications Holdings, Inc. (CCOI) delivers high-speed internet and data services across a global IP network, targeting businesses, ISPs, and government agencies. With a network footprint that spans multiple continents, the company has built its business around recurring revenue, operational efficiency, and consistent shareholder returns.

Over the past year, CCOI has experienced a dramatic repricing, with shares falling from a 52-week high near $80.45 to the current level around $18.49. The company continues to carry significant debt from the Sprint wireline integration, and its dividend history took a notable turn in late 2025 when the quarterly payout was cut sharply. Free cash flow has turned deeply negative, and operating cash flow has followed suit. CEO Dave Schaeffer and CFO Thaddeus Weed remain at the helm, and the management team’s commitment to long-term network strategy has not wavered, but income investors are navigating a materially different landscape than just a year ago.

Recent Events

The most significant development for Cogent investors in recent months has been the dramatic reduction in the quarterly dividend. After maintaining a consistent streak of quarterly increases that stretched back years, the company slashed its quarterly payout from $0.995 in November 2024 to $1.005 in March 2025, then $1.01 in May 2025, and $1.015 in August 2025, before cutting it to just $0.02 in November 2025. That represents a reduction of roughly 98% on a quarterly basis, a seismic shift for a company that had built much of its investor identity around dividend growth. The cut signals that management has concluded the prior payout level was no longer sustainable given the trajectory of cash flow.

Compounding the dividend story, the stock has shed most of its value over the past twelve months, falling from the low $80s to under $19 at current levels. The 52-week range of $15.96 to $80.45 captures just how severe the repricing has been. Institutions that once held the majority of the float are likely reassessing their positions as the income thesis has fundamentally changed. Meanwhile, the Sprint wireline integration continues to consume capital, and the company is working through a period of elevated capital expenditures and negative free cash flow as it attempts to stabilize the combined network and find its next phase of operational leverage.

With short interest sitting at approximately 5.5 million shares, there is a meaningful contingent of market participants positioned for further downside, though the stock has already absorbed an extraordinary drawdown from its highs.

Key Dividend Metrics

🟡 Forward Dividend Yield: 16.10%

🔵 Annual Dividend: $2.07

🟢 Last Quarterly Payment: $0.02

🟣 Prior Quarterly Payments (2025): $1.005, $1.01, $1.015

🟠 Payout Ratio: 562.32%

🔴 Last Dividend Date: November 21, 2025

⚫ Beta: 0.78

The headline yield of 16.10% is misleading in the most important sense: it is calculated using an annualized figure that includes the legacy higher payments, not the $0.02 payout that was made most recently. Investors should not interpret this yield as a reliable income signal going forward. The payout ratio of 562.32% reflects how far earnings have fallen below even a reduced dividend level, and the dramatic step-down in the November 2025 payment is the central fact any income investor must confront before evaluating this stock.

Dividend Overview

For years, Cogent’s dividend was one of the more distinctive income stories in the telecom services space. The company made quarterly increases a near-religious commitment, raising its payout incrementally every quarter for an extended streak that management openly celebrated. That history is now complicated by the November 2025 payment of just $0.02 per share, down from $1.015 the prior quarter.

Looking at the dividend history in sequence, the progression from $0.925 in March 2023 through $1.015 in August 2025 was steady and deliberate. The collapse to $0.02 was anything but gradual. At $2.07 in total annual dividend per share as reported, the forward income picture is deeply uncertain. Management has not yet publicly articulated a new dividend framework or growth target following the cut, and investors are effectively waiting to understand what the new baseline looks like. For income-focused portfolios, the current situation demands caution rather than confidence in the yield figure at face value.

Dividend Growth and Safety

The dividend growth story that once defined Cogent’s shareholder return strategy has been interrupted in a meaningful way. The November 2025 payment of $0.02 represents a near-total elimination of the cash return that income investors had come to rely on, and it raises serious questions about when and whether a sustained payout can be reestablished at any meaningful level.

On a safety basis, the numbers are difficult to defend. Operating cash flow for the trailing period came in at negative $10.6 million, and free cash flow was negative $90 million. With earnings per share at negative $4.06 and a net loss of $182 million, there is no traditional coverage ratio framework under which this dividend could be called safe. The company’s negative book value of $1.34 per share and negative return on equity of 229.15% further illustrate the degree of balance sheet stress. The cash on hand and the company’s ability to service debt remain important variables, but from a pure dividend safety standpoint, there is very little cushion at current operating levels.

Investors who held Cogent specifically for the income stream should reassess the thesis entirely. The question now is whether management can stabilize free cash flow through the back half of the Sprint integration and eventually restore a more modest but sustainable payout. That outcome is possible but far from certain at this stage.

Chart Analysis

Cogent Communications has endured a brutal twelve months on the price chart, with shares collapsing from a 52-week high of $75.05 to a current price of $18.49, a decline of more than 75% from peak to trough. The stock is now trading just 10.98% above its 52-week low of $16.66, which means it is scraping along the floor of its annual range with very little technical cushion beneath it. That kind of price destruction is not noise. It reflects a sustained and broad-based shift in sentiment that has persisted across multiple quarters, and dividend investors need to understand they are looking at a stock in confirmed long-term distress rather than a temporary pullback.

The moving average picture reinforces that concern at every level. CCOI is trading well below both its 50-day moving average of $23.13 and its 200-day moving average of $35.04, meaning the stock sits roughly 20% beneath its near-term trend and nearly 47% beneath its longer-term baseline. Critically, the 50-day average has crossed below the 200-day average, forming what technicians call a death cross, a configuration that historically signals entrenched downward momentum rather than a bottoming process. Until the 50-day average begins to flatten and curl upward toward the 200-day, the path of least resistance remains lower.

Momentum readings are not offering much comfort either. The Relative Strength Index currently sits at 34.73, which places the stock just outside oversold territory without yet triggering the kind of deeply washed-out reading that sometimes precedes a technical bounce. An RSI in the mid-30s on a stock that has already fallen 75% from its high is actually a cautionary signal, because it suggests selling pressure remains active rather than exhausted. Buyers have not yet stepped in with enough conviction to push momentum metrics into territory that would hint at accumulation.

For dividend investors, the chart presents a straightforward but uncomfortable message. The combination of a confirmed death cross, a price sitting near annual lows, and an RSI that has not yet reached oversold extremes suggests that technical support has not been established. Income-focused investors who rely on price stability to complement yield generation should treat this chart as a yellow flag at minimum. Watching for a sustained close above the 50-day moving average of $23.13 would be the most reasonable first signal that the downtrend is beginning to stabilize, and that threshold is still more than 25% above where shares are trading today.

Cash Flow Statement

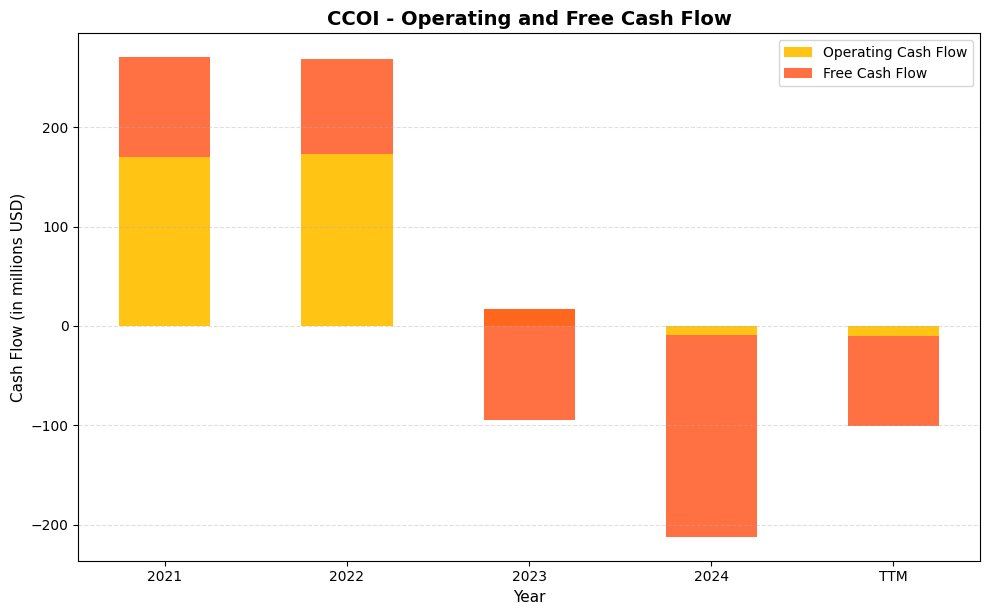

Cogent Communications’ cash flow profile has deteriorated sharply over the trailing measurement periods, and that deterioration sits at the center of any honest dividend sustainability analysis. Operating cash flow ran a healthy $170.3 million in 2021 and held roughly flat at $173.7 million in 2022, generating free cash flow of $100.3 million and $94.7 million respectively. Those were the years when the dividend looked well-supported on a pure cash generation basis. The picture changed dramatically in 2023, when operating cash flow collapsed to $17.3 million and free cash flow swung to negative $112.3 million. By 2024, operating cash flow turned negative at $8.6 million and free cash flow deepened further into the red at negative $203.6 million. The TTM figures offer no meaningful recovery signal, with operating cash flow still negative at $10.6 million and free cash flow at negative $90.0 million. A company paying a dividend while generating negative free cash flow is, by definition, funding that distribution through debt or asset sales rather than organic cash generation, and income investors need to weigh that reality carefully.

The trajectory here is not a temporary dip caused by a single capital project. It reflects the integration costs and network build-out obligations tied to Cogent’s 2023 acquisition of Sprint’s wireline business from T-Mobile, a transaction that fundamentally reshaped the company’s capital intensity profile. Capital expenditures scaled up precisely as operating cash flow was shrinking, which produced the compounding free cash flow losses visible across 2023 and 2024. Management has framed the spending as an investment in long-term revenue synergies, particularly in the wavelength and IP transit markets where the Sprint assets give Cogent meaningful new reach. That thesis may prove correct over time, but shareholders sitting in the dividend today are effectively betting on a future cash flow recovery that has not yet materialized in the reported numbers. Until operating cash flow returns to a level that covers both capex and the dividend obligation, the distribution relies on financial engineering rather than the self-funding model that dividend growth investors typically require as a baseline for holding conviction.

Analyst Ratings

The analyst community maintains a consensus buy rating on CCOI based on 11 analysts, though that consensus was almost certainly established or last updated before the most dramatic phase of the stock’s decline and the dividend cut. The mean price target of $26.64 implies upside of roughly 44% from the current price of $18.49, while the low target of $17.00 sits just below current trading levels and the high target of $43.00 represents more than double the current price. The wide dispersion between the low and high targets reflects genuine disagreement about where the stock finds its floor and whether the underlying network assets justify a meaningful premium to current levels.

Given the absence of recent named analyst actions in the data, the most useful read on Wall Street sentiment is the price target range itself. The $17.00 floor suggests at least one analyst believes the stock is fairly valued or slightly rich at current prices, while the $43.00 high implies a scenario where the Sprint integration delivers on its cost savings promises and free cash flow recovers materially. At $18.49, the stock is trading well below the mean target, which typically signals either an overlooked opportunity or a situation where the consensus has not yet been updated to reflect deteriorating fundamentals. Investors should monitor for target revisions as analysts incorporate the November 2025 dividend cut and the most recent operating cash flow data into their models.

Earning Report Summary

Cogent Communications reported trailing twelve-month revenue of approximately $896.6 million, reflecting continued pressure on top-line results as the company integrates the Sprint wireline assets and works through a transitional period in its business mix. Net income came in at a loss of $182.2 million, producing an EPS of negative $4.06 and a profit margin of negative 20.32%. These are not the numbers of a company firing on all cylinders, but they do need to be understood in the context of a multi-year integration effort that has front-loaded costs and capital spending.

Profitability and Margins

Return on equity came in at negative 229.15% and return on assets at negative 2.07%, both reflecting the combination of net losses and the heavily leveraged balance sheet. The negative book value per share of $1.34 illustrates how accumulated losses and debt have eroded the equity base. Operating margins are under sustained pressure, and the path to profitability runs directly through the completion of the Sprint integration, the realization of planned cost synergies, and a recovery in free cash flow generation. Management has previously expressed confidence in exceeding the $220 million annual synergy target from the Sprint deal, and progress on that front will be a key indicator for investors watching the next few quarters.

Cash Flow and Capital Allocation

The November 2025 dividend cut to $0.02 per share was the most direct signal from management that the prior capital allocation strategy had become untenable given current cash flow realities. Operating cash flow of negative $10.6 million and free cash flow of negative $90 million left no credible path to sustaining a quarterly payout above $1.00 per share. The company’s capital allocation priority has effectively shifted from shareholder distributions to preserving liquidity and funding the network investments necessary to complete the integration. How quickly that balance shifts back toward income distribution will depend heavily on when the operating business returns to sustainably positive free cash flow.

Looking Ahead

The forward outlook for Cogent hinges on a few critical variables: the pace of Sprint integration cost savings, the trajectory of capital expenditure normalization, and the recovery of operating cash flow. Management has historically been direct about its financial targets and its commitment to shareholder returns, and it would be surprising if the $0.02 quarterly dividend became a permanent baseline. A more realistic scenario is that the company uses the near-term period to stabilize its cash position, complete the heaviest phase of capital spending, and then rebuild the dividend at a more conservative and sustainable level. Investors buying at current prices are effectively making a bet on that recovery timeline.

Management Team

Dave Schaeffer, the founder and CEO who has led Cogent since 1999, remains the defining figure of the company’s strategic identity. His emphasis on lean operations, network simplicity, and capital returns has been consistent across more than two decades of business cycles, and the Sprint wireline acquisition represented his most ambitious strategic bet yet on the long-term value of Cogent’s network footprint. The dividend cut of late 2025 is a departure from the shareholder return script he had followed for years, but it also reflects the kind of pragmatic adjustment that a founder-led management team is often better positioned to make than one constrained by short-term optics.

CFO Thaddeus Weed continues to oversee the financial mechanics of a complex balance sheet, managing the company’s debt obligations and cash allocation through a demanding period. Chief Legal Officer John Chang handles the regulatory and compliance dimensions that come with operating a global network. The management team’s long tenure and collective institutional knowledge of the business remain genuine assets as the company navigates its most challenging stretch in recent memory. Their credibility with investors will be tested and rebuilt through execution rather than narrative over the coming quarters.

Valuation and Stock Performance

At $18.49, CCOI is trading near the lower end of its 52-week range of $15.96 to $80.45, a staggering compression that has wiped out the majority of the stock’s market value in under twelve months. The market capitalization of approximately $909 million now represents a fraction of what it was at the stock’s highs, and the enterprise value relative to any reasonable EBITDA estimate has contracted sharply. With a negative book value per share and no P/E ratio calculable given the net loss, traditional valuation frameworks offer limited utility here.

The price-to-book ratio of negative 13.82 is a mathematical artifact of the accumulated deficit on the balance sheet rather than a meaningful valuation signal. What does carry weight is the relationship between the current enterprise value and the company’s network assets, which represent real infrastructure with long-term replacement value. Some analysts arguing for price targets in the $40s range are likely anchoring to that asset value and a recovery in cash generation, while those with targets near $17.00 are taking a more conservative view on execution risk and the debt burden. The beta of 0.78 suggests the stock has historically moved with less volatility than the broader market, though the past twelve months have certainly tested that characterization. For investors considering entry at current levels, the risk-reward is asymmetric in both directions, with meaningful upside if the integration delivers and meaningful downside if cash flow does not recover on a reasonable timeline.

Risks and Considerations

The most immediate risk facing Cogent investors is the sustainability of even the reduced dividend level. With operating cash flow negative and free cash flow at negative $90 million, the company is not currently generating the cash needed to support distributions at any material level. If capital expenditures remain elevated and the Sprint integration continues to consume resources, the $0.02 quarterly payment could remain the ceiling rather than a floor for income recovery.

The company’s debt load is a persistent concern that amplifies every operational challenge. Interest expense at current levels consumes a significant portion of whatever cash the business generates, and refinancing risk becomes a real consideration if credit conditions tighten or the company’s financial metrics do not improve on a timeline that satisfies debt covenants. The negative return on equity of 229.15% and negative book value are symptoms of a balance sheet that has been stretched to fund the Sprint deal, and unwinding that stress will take time and consistent operational execution.

Competition in enterprise connectivity and bandwidth services remains intense. Cogent competes against larger, better-capitalized players with broader product portfolios, and pricing pressure in core markets can erode the revenue consistency that the dividend strategy depends on. The company has historically differentiated on network efficiency and simplicity, but sustaining that edge while digesting a major acquisition and managing costs is genuinely difficult.

Finally, the execution risk around the Sprint integration remains real even as management has expressed confidence in exceeding synergy targets. Integrating legacy network infrastructure, retaining customers through a transition, and achieving cost savings simultaneously is a complex undertaking. Any meaningful shortfall in synergy realization or customer retention could delay the free cash flow recovery that the entire investment thesis now depends on.

Final Thoughts

Cogent Communications today is a fundamentally different income proposition than it was twelve months ago. The quarterly dividend has been cut to near zero, free cash flow is deeply negative, and the stock has lost roughly 75% of its value from its 52-week high. For investors who owned CCOI for its yield, the past year has been a painful lesson in the limits of payout sustainability when cash flow deteriorates faster than expected.

That said, the underlying network infrastructure retains real long-term value, and the Sprint integration does create a pathway to a larger, more capable business if management can execute on its cost savings targets and return operating cash flow to positive territory. The analyst consensus of buy with a mean target of $26.64 suggests that at least a majority of Wall Street coverage sees more upside than downside from current levels. For investors with a higher risk tolerance and a long time horizon, the current price may eventually look like an attractive entry point. But for income investors specifically, CCOI no longer fits the profile of a reliable dividend grower, and any position taken here should be sized and monitored accordingly with a clear-eyed view of the cash flow recovery timeline ahead.