Key Takeaways

📈 Coca-Cola offers a reliable 2.53% dividend yield, backed by a remarkable 63-year streak of dividend increases and steady annual growth.

💰 Operating cash flow came in at $7.41 billion for the trailing twelve months, supporting continued dividend security and operational flexibility.

🔍 Analysts rate KO as a “Buy,” with a consensus price target of $82.63 and a high target of $89.00, reflecting confidence in the company’s resilient business model.

📊 Coca-Cola’s full-year financials show revenue of $47.94 billion and net income of $13.11 billion, with a profit margin of 27.34% that ranks among the best in consumer staples.

👥 Under CEO James Quincey’s leadership, Coca-Cola continues to emphasize global expansion, portfolio innovation, and operational efficiency as the company heads deeper into 2026.

Updated 2/25/26

Coca-Cola (KO) continues to stand out as a dependable force in the consumer staples sector. With a 63-year streak of dividend increases, solid global revenue, and strong leadership at the helm, the company remains a consistent performer. Shares have climbed steadily through early 2026, approaching their 52-week high of $80.69 and currently trading at $80.47, reflecting growing investor confidence in the company’s earnings power and brand durability.

The leadership team, guided by CEO James Quincey, has continued to lean into global expansion, innovation, and operational efficiency. A consensus buy rating from 23 analysts, a forward dividend yield of 2.53%, and a profit margin above 27% reflect the market’s appreciation for Coca-Cola’s long-term compounding story. Whether it’s pricing strength, strategic portfolio management, or brand execution, KO continues to offer a stable mix of income and growth potential backed by one of the most recognizable consumer franchises in the world.

Recent Events

Coca-Cola has continued to generate headlines in early 2026 as the company navigates a global beverage landscape that remains both competitive and full of opportunity. The company’s push into premium and health-oriented categories has stayed front and center, with brands like Fairlife and Topo Chico maintaining momentum as consumers increasingly reach for alternatives to traditional carbonated soft drinks. Coca-Cola Zero Sugar has remained one of the portfolio’s most discussed growth drivers, with volume trends supporting continued marketing investment behind the brand.

On the pricing front, Coca-Cola has continued to demonstrate its ability to pass cost increases through to the end consumer without significant volume erosion, a dynamic that has impressed analysts watching the company’s margin trajectory. The company also remains active on the sustainability front, facing ongoing public and regulatory scrutiny around packaging and water usage practices that management has addressed through a series of environmental commitments. Meanwhile, the long-running IRS transfer pricing dispute continues to linger in the background, with the $6 billion tax deposit still unresolved and representing a notable overhang for investors tracking the company’s balance sheet. Shares are trading near their 52-week high, suggesting the market has largely priced in a favorable operating outlook heading into the rest of 2026.

Key Dividend Metrics

📈 Forward Dividend Yield: 2.53%

💸 Forward Annual Dividend: $2.06 per share

📆 Dividend Growth Streak: 63 consecutive years

📊 Payout Ratio: 67.11%

🕒 5-Year Average Yield: 3.01%

📉 Most Recent Quarterly Dividend: $0.51 per share

⚖️ Last Dividend Payment: December 1, 2025

Dividend Overview

There’s a reason Coca-Cola remains on every dividend investor’s radar. It’s not just about the current yield or the size of the checks — it’s the dependability. When a company has raised its dividend for 63 straight years, that consistency becomes a trust factor in its own right, and Coca-Cola has more than earned that trust through recessions, inflation cycles, and global disruptions alike.

The current forward yield of 2.53% may not grab headlines on its own, but when you consider that it’s backed by one of the strongest brand portfolios in the world and a business that generates cash across virtually every economic environment, it starts to look considerably more attractive. The quarterly dividend now stands at $0.51 per share, up from $0.485 in 2024 and $0.46 in 2023, reflecting a consistent upward trajectory that income investors can plan around.

The payout ratio of 67.11% represents a notable improvement from the nearly 79% reported in prior periods, giving Coca-Cola more financial flexibility than it has had in recent years. This tighter ratio reflects the combination of a modestly higher dividend and meaningfully stronger earnings per share of $3.04. For a mature consumer staples company with highly recurring revenue, a payout ratio in this range is well within a comfortable zone, and it provides a broader buffer for future increases even if earnings growth moderates.

Dividend Growth and Safety

Coca-Cola’s dividend history over the past several years tells a clear story of deliberate, inflation-conscious growth. The quarterly payment moved from $0.46 throughout 2023 to $0.485 in 2024 and then stepped up again to $0.51 in 2025, putting the annualized rate at $2.06. That progression represents a roughly 5.4% increase from the 2024 rate and an even larger jump from where dividends stood two years ago. For a company of this size, that pace is meaningfully above the low-single-digit raises investors have historically received from KO.

The safety of the dividend is supported by several layers of financial strength. Net income of $13.11 billion on revenue of $47.94 billion produced a profit margin of 27.34%, which is exceptional for a company operating at this scale across global markets. A return on equity of 43.32% and a return on assets of 9.15% confirm that Coca-Cola continues to extract strong value from its asset base, even while carrying a significant debt load. Operating cash flow of $7.41 billion covers the annual dividend obligation with room to spare, though the negative free cash flow figure of $1.46 billion warrants attention and likely reflects elevated capital expenditure during the period rather than a structural deterioration in cash generation.

Coca-Cola’s continued share repurchase program provides an additional tailwind for dividend sustainability. By gradually reducing the share count, the company lowers the total annual dividend payout while simultaneously improving earnings per share, a dual benefit that creates incremental headroom for future increases. Combined with the brand’s global pricing power and the sticky demand patterns that define the non-alcoholic beverage category, the dividend’s long-term trajectory looks well-supported heading into the back half of the decade.

Chart Analysis

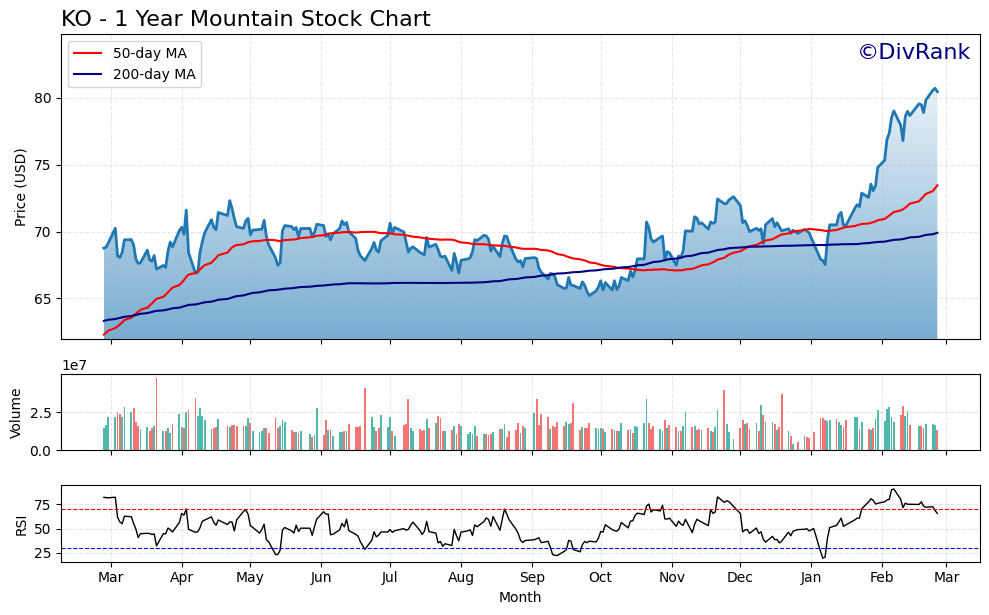

Coca-Cola’s price action over the past year tells a compelling recovery story. Shares bottomed near $65.21 before staging a sustained advance that has carried the stock to within a fraction of its 52-week high of $80.72. At the current price of $80.47, KO has gained roughly 23.4% from that trough, a meaningful move for a large-cap consumer staples name that most investors hold primarily for its income. The trajectory has been orderly rather than parabolic, which tends to be a healthier sign for long-term holders who care more about price stability than momentum chasing.

The moving average picture is constructive. KO is trading comfortably above both its 50-day moving average of $73.46 and its 200-day moving average of $69.91, and the 50-day has crossed above the 200-day to form what technicians call a golden cross. That configuration signals that shorter-term buying pressure has meaningfully outpaced the longer-term trend, and it historically corresponds to periods of sustained price strength rather than brief countertrend rallies. The roughly $10.50 gap between the current price and the 200-day average also provides a reasonable cushion, suggesting the longer-term trend would need to deteriorate significantly before the broader uptrend came into question.

The Relative Strength Index sits at 65.6, which places KO in firm uptrend territory without yet crossing into the overbought zone above 70. That distinction matters for dividend investors evaluating entry points. A reading this close to 70 warrants some patience, particularly with the stock sitting just 0.31% below its 52-week high. A pullback toward the $75 to $76 range, which would bring KO closer to its 50-day moving average, would offer a more attractive entry while keeping the broader bullish structure fully intact.

For dividend-focused investors, the technical setup reinforces rather than complicates the income thesis. The trend is clearly positive, the stock is not in distressed or broken-chart territory, and the proximity to a 52-week high reflects genuine institutional demand for the name. The main practical consideration is timing. Investors already holding KO for its dividend can view this chart with confidence, while those looking to initiate a position may find it reasonable to wait for a modest consolidation before committing new capital at prices this close to a year-to-date peak.

Cash Flow Statement

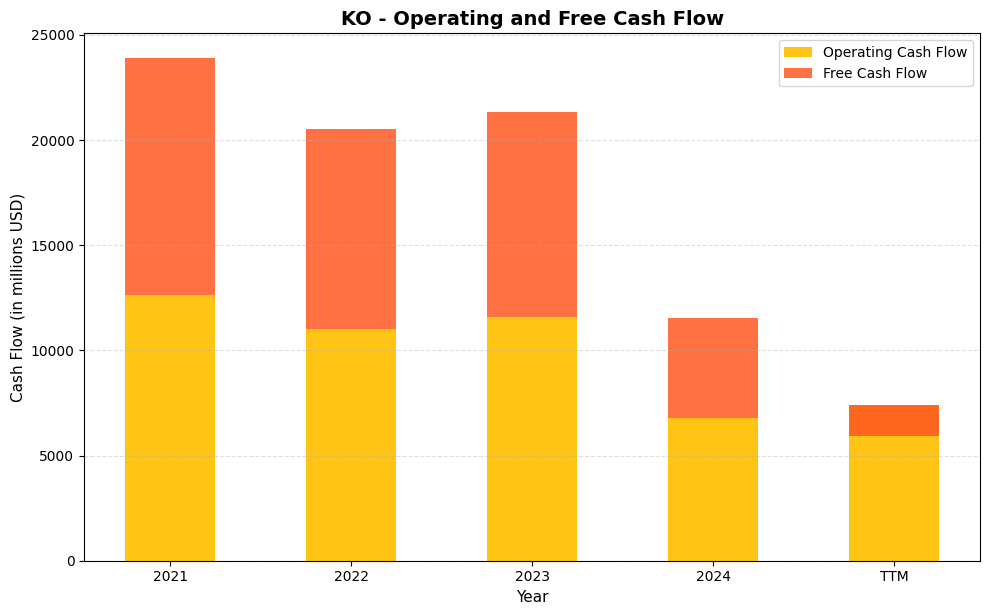

Coca-Cola’s operating cash flow held in a relatively tight band between $11.0 billion and $12.6 billion from 2021 through 2023, which provided a comfortable cushion above the company’s annual dividend obligations of roughly $7.6 billion to $8.0 billion over that same stretch. The picture shifted meaningfully in 2024, when operating cash flow dropped to $6.8 billion and free cash flow fell to $4.7 billion, levels that no longer covered the dividend with the same margin investors had come to expect. On a trailing twelve month basis, the situation looks more acute, with operating cash flow of $7.4 billion and free cash flow turning negative at approximately $1.5 billion. That negative free cash flow figure is a direct consequence of elevated capital expenditures and legal accruals related to the IRS tax dispute rather than a structural deterioration in the underlying business, but it is a number dividend investors need to monitor closely as the company works through those one-time charges.

Stepping back across the full four-year picture, the 2021 peak of $12.6 billion in operating cash flow and $11.3 billion in free cash flow represented KO operating near the top of its cash generation range, supported by post-pandemic volume recovery and disciplined capital spending that averaged roughly $1.4 billion annually. Capital efficiency was strong through 2023, with free cash flow conversion remaining above 80 percent of operating cash flow in each of those three years. The 2024 and TTM compression is a departure from that efficiency profile, and the degree to which KO restores free cash flow toward the $9 billion to $10 billion range in 2025 will be the most important variable for assessing whether the dividend, which has grown for 62 consecutive years, can continue compounding at its historical pace of 4 to 5 percent annually without leaning on the balance sheet.

Analyst Ratings

The analyst community remains broadly constructive on Coca-Cola heading into 2026. Among the 23 analysts covering the stock, the consensus stands at a buy rating, reflecting confidence in the company’s ability to sustain earnings growth and continue returning capital to shareholders. The mean price target of $82.63 sits just above the current trading price of $80.47, implying modest near-term upside from current levels. The high target of $89.00 suggests that the more bullish analysts see room for meaningful appreciation if earnings execution remains strong, while the low target of $71.38 reflects a more cautious view centered on valuation risk and macro headwinds.

Given that shares are trading close to the consensus mean target, the market appears to have already priced in much of the near-term fundamental story. That dynamic is consistent with Coca-Cola trading near its 52-week high of $80.69 as of late February 2026. Analysts who have assigned higher targets are likely pointing to the company’s improving payout ratio, the continued strength of its international volume trends, and the long-term optionality embedded in its non-soda portfolio. For income-focused investors, the analyst consensus adds a layer of comfort, confirming that the professional community broadly views KO as a well-managed company operating from a position of competitive strength.

Earning Report Summary

Coca-Cola delivered a strong full-year financial performance through the trailing twelve-month period, posting revenue of $47.94 billion and net income of $13.11 billion. The profit margin of 27.34% stands out as one of the most impressive in the entire consumer staples sector, reflecting both the premium positioning of Coca-Cola’s core brands and the operating leverage the company has built through years of disciplined cost management. Earnings per share of $3.04 provide the foundation for the company’s continued dividend growth, with the payout ratio improving to a more comfortable 67.11%.

Volume and Pricing Dynamics

Coca-Cola’s revenue performance has continued to be shaped by a combination of pricing initiatives and gradual volume recovery across its global markets. The company’s ability to implement price increases without triggering significant consumer pushback has been a defining characteristic of the business over the past several years, and that dynamic has remained largely intact. Coca-Cola Zero Sugar has continued to serve as one of the portfolio’s most visible growth contributors, attracting consumers who are moving away from full-sugar variants while remaining within the Coca-Cola ecosystem. Sparkling soft drinks overall have held their ground, while still beverages and premium categories have added diversification to the revenue base.

Leadership’s Take

CEO James Quincey has continued to frame Coca-Cola’s strategy around what he has called an “all-weather” operating model, one that balances the company’s global reach with disciplined local market execution. He has repeatedly pointed to the company’s category diversification and the growing contribution from brands like Fairlife and Topo Chico as evidence that Coca-Cola is successfully attracting consumers beyond its traditional core. The operational philosophy under Quincey emphasizes agility and margin discipline, two priorities that are reflected in the improvement in profitability metrics over the most recent reporting period.

Looking Ahead

Management has maintained an optimistic tone heading into the remainder of 2026, pointing to organic revenue growth targets and continued investment in marketing and innovation as the primary levers for sustaining momentum. Currency fluctuations remain a manageable but persistent headwind given the company’s extensive international exposure, and the unresolved IRS tax matter continues to command attention from investors focused on the balance sheet. That said, Coca-Cola’s underlying business fundamentals, anchored by a globally recognized brand portfolio and decades of consumer loyalty, provide a durable platform from which management can execute its long-term growth plan.

Management Team

At the helm of Coca-Cola is James Quincey, who has served as Chairman and CEO since 2017. Quincey has been instrumental in steering the company through major shifts, placing emphasis on innovation, portfolio diversification, and digital transformation. He has helped shape a more agile Coca-Cola, one that is better positioned to respond to consumer trends and global disruptions while maintaining the operational discipline that has defined the company for decades.

Supporting him is John Murphy, the company’s President and Chief Financial Officer. Murphy has played a key role in managing capital structure and driving cost efficiencies, and his steady stewardship has helped maintain Coca-Cola’s profitability even in challenging economic climates. Henrique Braun serves as Chief Operating Officer, bringing over two decades of experience within Coca-Cola, particularly across Latin America and Asia, and his role underscores the company’s continued emphasis on international growth as a primary driver of long-term value. Other members of the executive team, including Lisa Chang as Chief People Officer and Manuel Arroyo as Chief Marketing Officer, have each contributed to enhancing Coca-Cola’s internal culture and brand relevance on a global scale. Altogether, the leadership team reflects both stability and strategic vision, two qualities that matter enormously when navigating a rapidly changing consumer landscape.

Valuation and Stock Performance

Coca-Cola’s stock has performed well over the past year, climbing from a 52-week low of $65.35 to its current price of $80.47, just a hair below the 52-week high of $80.69. That move represents a gain of roughly 23% from the trough and places KO in a position of meaningful technical strength heading into the spring of 2026. The stock’s beta of 0.36 continues to make it one of the lower-volatility names in the large-cap universe, reinforcing its appeal to investors who prioritize capital preservation alongside income generation.

From a valuation standpoint, Coca-Cola is not inexpensive. The stock trades at 26.47 times earnings and carries a price-to-book ratio of 10.76 against a book value per share of just $7.48, a reflection of the company’s asset-light model and the enormous intangible value embedded in its brand portfolio. These multiples are above the broader market average, but they have historically commanded a premium given Coca-Cola’s consistency, global distribution network, and unmatched pricing power in the non-alcoholic beverage category. The consensus analyst price target of $82.63 implies limited near-term upside from current levels, which is a reasonable observation given how close the stock is trading to that figure. However, for investors with a multi-year time horizon, the combination of a growing dividend, improving earnings quality, and a business model that has proven resilient across cycles continues to make a compelling case for ownership.

Risks and Considerations

Despite its global footprint and diversified portfolio, Coca-Cola faces a set of risks that income investors should monitor carefully. Currency headwinds remain a recurring challenge, particularly in emerging markets where exchange rate volatility can meaningfully erode the value of overseas revenues when translated back into U.S. dollars. Given that a substantial portion of Coca-Cola’s business is conducted outside North America, this is not a peripheral concern but a structural feature of the investment that investors must accept as part of the long-term trade-off.

The unresolved IRS transfer pricing litigation, which prompted the company to deposit $6 billion with the tax authority, continues to represent an overhang on the balance sheet. While management has indicated it does not expect a near-term material operational impact, the ultimate resolution of this matter remains uncertain and could affect capital allocation decisions going forward.

The company’s negative free cash flow of $1.46 billion over the trailing twelve months also deserves attention. If elevated capital expenditure levels persist rather than normalize in coming periods, Coca-Cola’s ability to self-fund dividend increases and share repurchases from internal cash generation could come under pressure, potentially increasing reliance on debt markets.

Regulatory scrutiny around sugar content, plastic packaging, and water usage continues to intensify in key markets across Europe, Asia, and Latin America. These pressures require ongoing investment in product reformulation and sustainability infrastructure, adding to the cost burden even as they protect the company’s social license to operate. Finally, shifts in consumer preferences toward functional beverages, reduced-sugar options, and hydration products outside Coca-Cola’s core portfolio represent a long-term competitive challenge that management has addressed but not yet fully resolved.

Final Thoughts

Coca-Cola isn’t about chasing the next big thing. It’s about staying relevant, consistent, and efficient, and that’s exactly what the company has managed to do across more than six decades of uninterrupted dividend growth. Under strong leadership, it has evolved beyond soda into a broader beverage empire that includes water, coffee, premium milk, energy drinks, and more. The progression hasn’t been flashy, but it has been remarkably steady.

With shares trading near all-time highs, a payout ratio that has improved meaningfully to 67%, earnings per share of $3.04, and a dividend that has now reached $2.06 annually, the fundamental picture entering 2026 is as solid as it has been in years. Risks remain, as they always do, but Coca-Cola’s scale, brand strength, and operational discipline give it the tools to navigate whatever the global economic environment delivers next. For long-term income investors seeking a combination of predictable cash returns and defensive resilience, KO continues to make a quiet but compelling case for a permanent place in a dividend-focused portfolio.