Updated 2/25/26

Church & Dwight Co., Inc. (CHD) has built a dependable business around a portfolio of well-known consumer brands like Arm & Hammer, OxiClean, and TheraBreath. With consistent earnings, disciplined cash flow management, and nearly three decades of uninterrupted dividend growth, it remains a steady player in the household and personal care sector. The stock currently trades around $103.63, supported by strong free cash flow and a conservative payout ratio.

While its valuation remains elevated, the 19-analyst consensus price target of $103.58 sits nearly in line with the current price, reflecting a market that views CHD as fairly valued at present levels. The leadership transition to CEO Richard Dierker, formerly the company’s long-tenured CFO, has settled in, and the organization appears focused on executing its brand-driven growth strategy. Backed by stable revenue, a solid balance sheet, and a commitment to long-term shareholder return, Church & Dwight continues to offer investors a foundation of operational strength and strategic clarity.

Recent Events

Church & Dwight has continued advancing its product innovation agenda into early 2026, building on the brand momentum it established throughout 2025. The company has remained active in the e-commerce channel, where online sales have become an increasingly meaningful portion of total consumer revenue, and management has emphasized targeted marketing investments designed to support volume growth across its core categories. The ARM & HAMMER franchise continues to serve as a cornerstone of the portfolio, with newer product formats helping the brand reach health-conscious and value-oriented consumers alike.

On the operational front, the company has benefited from moderating input cost pressures compared to the peak inflation environment of prior years, which has helped support margin stability. Supply chain efficiency gains have also contributed to stronger cash conversion, with operating cash flow reaching approximately $1.22 billion on a trailing twelve-month basis. Revenue for the period came in at $6.20 billion, a modest step up from the $6.11 billion reported for full-year 2024, reflecting continued organic growth across its domestic and international segments.

Richard Dierker’s tenure as CEO, following his transition from CFO, has been characterized by a steady-as-it-goes approach that long-term CHD shareholders tend to appreciate. The market has responded with relative calm, as the stock has traded within a fairly defined range and maintained its reputation as a lower-volatility consumer staples name. With a beta of just 0.47, CHD continues to behave like the defensive anchor it has historically been for income-oriented portfolios.

Key Dividend Metrics

📈 Forward Yield: 1.12%

💰 Annual Dividend: $1.23 per share

🔁 Payout Ratio: 39.07%

🕰️ 5-Year Average Yield: 1.13%

📅 Last Dividend Payment: $0.308 per share (February 13, 2026)

🧮 Ex-Dividend Date: February 13, 2026

🔧 Dividend Growth Streak: 29 years

🧾 Free Cash Flow Coverage: Strong (FCF: ~$1.14B)

Dividend Overview

CHD isn’t about headline-grabbing yields. At just over 1%, the current forward yield won’t excite investors looking for immediate income. But dig a little deeper, and you see what makes this dividend different — it’s built on a foundation of consistency and prudence.

The payout ratio has improved considerably, now sitting at approximately 39%, down from the nearly 48% reported in the prior period. That means the company is paying out well under half of its earnings as dividends, which leaves significant room to reinvest in the business, handle debt obligations, and still reward shareholders. It reflects a more comfortable cushion than CHD has carried in recent years.

The most recent quarterly dividend payment of $0.308 per share, paid on February 13, 2026, represents a step up from the $0.295 quarterly rate that was in place throughout most of 2025. That increase brings the annualized dividend to $1.23 per share and extends the company’s dividend growth streak to 29 consecutive years, a milestone that speaks to the durability of this income stream across multiple economic cycles.

CHD also tends to be a steady stock. With a beta of 0.47, it moves far less than the broader market, which is another meaningful consideration for income investors looking to reduce portfolio volatility without sacrificing dividend consistency.

Dividend Growth and Safety

Church & Dwight has now increased its dividend for 29 consecutive years, a record that places it firmly in the territory of elite dividend compounders. The most recent increase, reflected in the $0.308 quarterly payment made in February 2026, represents a raise of approximately 4.4% from the prior rate of $0.295. That aligns well with the company’s historical cadence of low-to-mid single-digit annual increases, which, while not spectacular in isolation, compound meaningfully for investors who hold over the long term.

The safety of this dividend is well-supported by the underlying cash flow profile. Operating cash flow reached approximately $1.22 billion on a trailing basis, and free cash flow came in near $1.14 billion after accounting for capital expenditures. Against an annualized dividend obligation that represents a fraction of that figure, the coverage ratio is comfortable by any reasonable measure. Even in a scenario where earnings soften temporarily, CHD has the financial flexibility to sustain its payout without strain.

The payout ratio of 39% is one of the more reassuring data points in this profile. Relative to earnings per share of $3.02, the $1.23 annual dividend is well within what the business generates without any extraordinary effort. That conservatism is a deliberate management choice and one of the reasons the dividend has never been at risk even during periods of macroeconomic stress.

For dividend-focused investors, the current share price near $103.63 sits noticeably below the 52-week high of $116.46, which means investors entering at this level are locking in a modestly better yield-on-cost than those who bought at the top. Church & Dwight isn’t trying to be flashy, and in this case, that’s exactly what makes it a worthwhile consideration for investors who appreciate steady hands, dependable income, and brands that don’t go out of style.

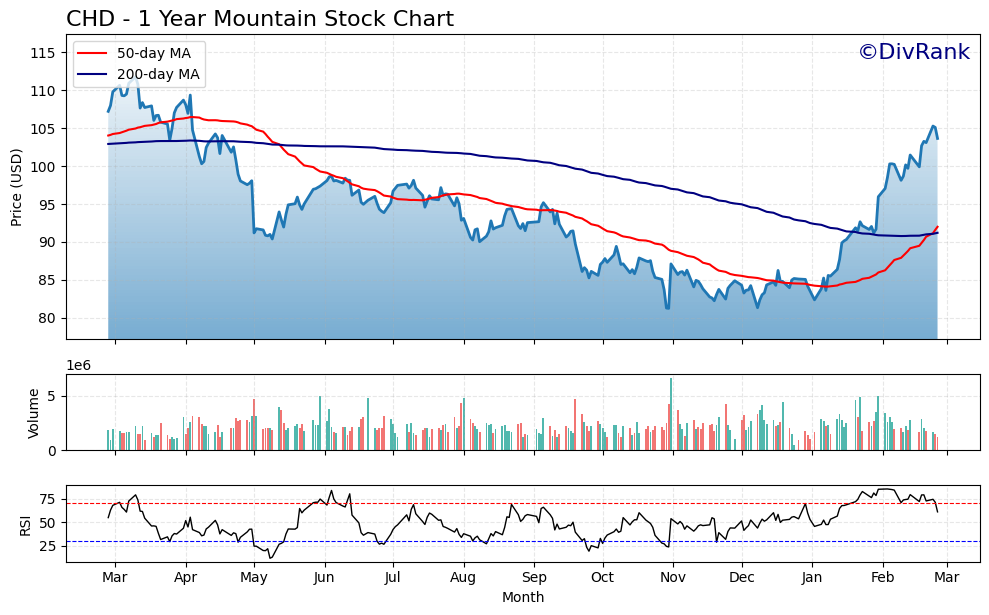

Chart Analysis

Church & Dwight has staged an impressive recovery over the past twelve months, climbing from a 52-week low of $81.26 to its current price of $103.63, a gain of roughly 27.5% from trough to present. The stock reached a peak of $111.75 over that same period, and at today’s price it sits about 7.3% below that high water mark. That kind of constructive base-to-current trajectory tells a clear story: after whatever selling pressure drove CHD into the low $80s, buyers stepped in with conviction and have held the line through a sustained advance. For dividend investors, that price stability and recovery capacity matters almost as much as the yield itself, because a stock that can defend its floor tends to protect the long-term compounder story that makes consumer staples names worth holding through volatility.

The moving average picture is about as constructive as it gets for a steady-growth name like this. CHD is trading at $103.63, which places it comfortably above both its 50-day moving average of $92.00 and its 200-day moving average of $91.21. The fact that those two averages are so close together, and that price has pulled well clear of both, confirms that the recent advance has been broad-based rather than a short-term spike. More importantly, the 50-day has crossed above the 200-day, forming what technical analysts call a golden cross, which is generally interpreted as a medium-term bullish signal. For an income investor who is less focused on short-term trading and more concerned with entry timing on a long-term hold, seeing the stock above both averages with the trend aligned in the same direction is a reassuring backdrop.

The RSI reading of 60.92 sits in a range that is firm without being alarming. A reading above 70 would traditionally signal overbought conditions and raise the risk of a near-term pullback, but at roughly 61, CHD has meaningful momentum behind it while still leaving room to run before the technicals become stretched. This is often considered a sweet spot for quality names, where price strength is confirmed but the stock has not yet attracted the kind of speculative froth that typically precedes a sharp correction. Dividend investors who have been waiting for a cleaner entry should be aware that this momentum reading suggests the market is pricing in continued positive sentiment, and dips toward the moving averages in the low $90s would represent a more attractive risk-reward setup if patience allows for it.

Taken together, the technical picture for CHD is broadly supportive for income-focused investors with a multi-year time horizon. The trend is up, the moving averages are properly aligned, and momentum is constructive without being euphoric. The stock is not screaming cheap from a chart perspective, trading nearly 13% above its 200-day average, but nothing in this setup suggests deterioration of the underlying trend. Investors who already own CHD have little reason to feel technically exposed. Those looking to initiate a position may prefer to be patient and watch for any consolidation back toward the $95 to $98 range, which would offer a tighter entry relative to key support while keeping the dividend growth thesis fully intact.

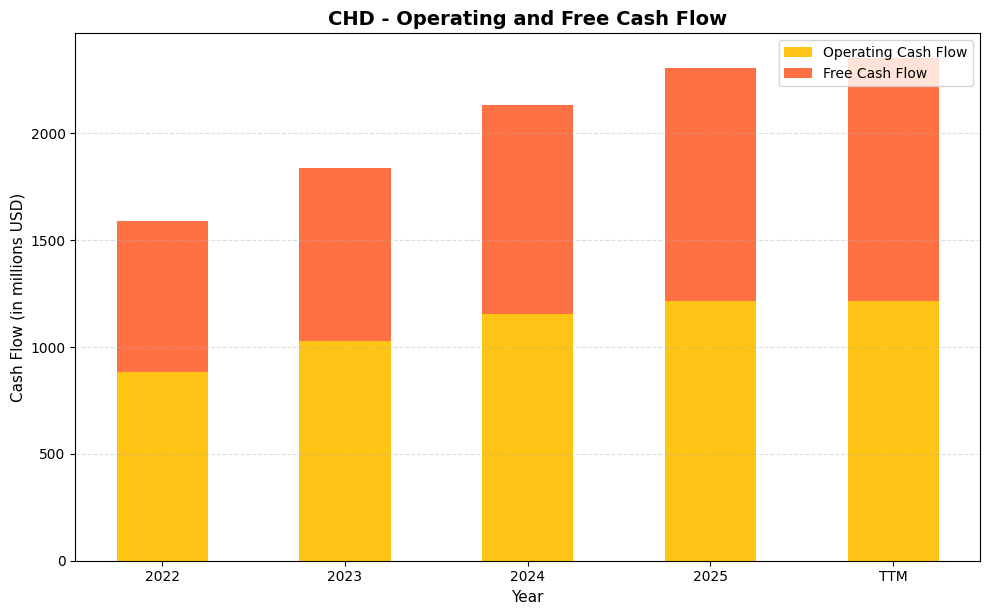

Cash Flow Statement

Church & Dwight’s cash generation story is one of the more compelling in the consumer staples space. Operating cash flow has climbed from $885.2 million in 2022 to $1,215.4 million in 2025, a gain of roughly 37% over just three years, and the TTM figure holds steady at that same $1,215.4 million level. Free cash flow tells an even more encouraging story for dividend investors, rising from $706.4 million in 2022 to $1,093.0 million in 2025, with the TTM reading pushing further to $1,135.9 million. That kind of free cash flow expansion gives the company substantial headroom above its annual dividend obligation, and it means the payout is backed by real cash generation rather than accounting earnings alone.

The multi-year trajectory here reflects genuine improvement in capital efficiency, not just revenue growth. The gap between operating cash flow and free cash flow has narrowed meaningfully over this period, which signals that capital expenditures are being managed with discipline even as the business scales. In 2022, capex consumed roughly $179 million of operating cash flow; by the TTM period, that figure had compressed to approximately $79.5 million, freeing up an increasingly large share of earnings for shareholders. For dividend growth investors, this trend matters because it suggests CHD has more financial flexibility today than it did three years ago, whether that means accelerating dividend increases, pursuing bolt-on acquisitions, or building a buffer against any cyclical softness in consumer demand.

Analyst Ratings

The current analyst consensus on Church & Dwight is a buy, based on the collective views of 19 analysts covering the stock. The mean price target of $103.58 sits almost exactly in line with the current share price of $103.63, which tells you the Street broadly views CHD as fairly valued at current levels rather than deeply discounted or overextended. The range of targets is notable, however, stretching from a bearish low of $74.00 to a bullish high of $115.00, reflecting genuine disagreement about how much premium the market should assign to CHD’s predictable cash flows and brand strength.

The bears in that range are likely focused on valuation, as a trailing P/E of 34.31 and a price-to-book of 6.13 are not cheap for a consumer staples company growing at a low-to-mid single-digit organic rate. The $74 low target implies meaningful downside if sentiment shifts or if earnings disappoint relative to current expectations. The more constructive analysts, those with targets near the $115 high, are presumably leaning on the quality of CHD’s cash flow generation, its defensive characteristics, and the durability of its brand portfolio as justification for a sustained premium multiple.

With no recent analyst actions to highlight, the current consensus represents a stable, if unexciting, assessment of the stock. A buy rating with a mean target that essentially mirrors the current price is the market’s way of saying CHD is a quality business trading at a fair price — not a screaming buy, but not a name to exit either for investors who already own it and value its income consistency.

Earning Report Summary

Church & Dwight has continued to demonstrate the kind of steady, brand-driven performance that has defined its track record over many years. With trailing twelve-month revenue of $6.20 billion and net income of $736.8 million, the business is generating meaningful profits at an 11.88% margin, a level that reflects both pricing discipline and ongoing efficiency work across the supply chain.

Solid Top-Line Growth

Revenue of $6.20 billion represents a step forward from the $6.11 billion reported for full-year 2024, continuing the pattern of steady organic growth that has characterized CHD for years. The gains are being driven by a combination of volume improvement and selective pricing, with e-commerce remaining a particularly active channel. Management has noted that online sales now account for a meaningful and growing share of total consumer revenue, and the company has leaned into digital marketing to support that momentum.

Healthy Margins and Cash Flow

Earnings per share of $3.02 on a trailing basis reflects the improved earnings quality of the business. Operating cash flow of approximately $1.22 billion and free cash flow near $1.14 billion represent standout figures that give CHD substantial financial flexibility. The payout ratio of 39.07% is well below where it has been in recent years, suggesting the earnings recovery has outpaced dividend growth, which is a healthy dynamic for long-term dividend sustainability. Return on equity of 17.62% and return on assets of 8.20% round out a picture of a company using its capital effectively.

Leadership’s Take

CEO Richard Dierker, who assumed the top role following Matthew Farrell’s transition to Chairman, has maintained the company’s focus on brand investment, innovation-led growth, and operating efficiency. His background as a long-tenured CFO has brought a financially disciplined lens to capital allocation decisions, and the cash flow improvement in the most recent period reflects that orientation. Management has continued to highlight the importance of product development and targeted marketing as the primary levers for sustaining organic growth across its portfolio of household and personal care brands.

What’s Next

Looking ahead, Church & Dwight remains focused on innovation within its existing brand architecture, with newer product formats and line extensions aimed at capturing demand from health-conscious consumers and those seeking value. The company also continues to monitor the competitive landscape carefully, as the household and personal care category remains contested by both legacy national brands and private label alternatives. The balance between investment spending and margin management will be a key theme as CHD navigates the next phase of its growth trajectory.

Management Team

Church & Dwight completed its planned leadership transition with Richard Dierker stepping into the CEO role following Matthew Farrell’s move to Executive Chairman. Dierker spent 15 years at the company as CFO before taking the top job, and his deep institutional knowledge of the business, its financial structure, and its brand portfolio has made the transition feel far more like a promotion than a disruption. Farrell’s continued presence as Chairman ensures that the strategic continuity the market has long valued at CHD remains intact.

The broader executive team continues to be led by experienced operators across key functions. Patrick de Maynadier serves as Executive Vice President and General Counsel, Carlos Linares oversees global research and development, and Britta Bomhard leads marketing strategy. Their combined tenure and familiarity with the business reinforce the culture of operational discipline that has allowed CHD to grow its dividend without interruption for 29 consecutive years. It is a management group that understands both the pace and the priorities of a consumer brands company built for the long run.

Valuation and Stock Performance

As of February 25, 2026, CHD is trading at $103.63, sitting comfortably in the middle of its 52-week range of $81.33 to $116.46. The trailing P/E ratio of 34.31 is high relative to the broader consumer staples sector, but it reflects the premium the market consistently assigns to CHD’s combination of predictable cash flows, low volatility, and a nearly three-decade dividend growth track record. The price-to-book ratio of 6.13 against a book value per share of $16.92 similarly reflects that investors are paying up for quality.

The market cap stands at approximately $24.9 billion, and the stock’s beta of 0.47 continues to make CHD one of the more defensive names in the consumer staples universe. For investors prioritizing stability over momentum, that low sensitivity to broader market swings is a feature rather than a limitation. The analyst consensus mean price target of $103.58 essentially mirrors the current stock price, which implies the Street views CHD as fairly priced rather than offering a clear margin of safety at current levels. Investors looking for a more attractive entry point may find that pullbacks toward the lower end of the 52-week range offer a better risk-reward setup, particularly given the durable cash flow profile and the 29-year dividend growth streak that underpins the total return case.

Risks and Considerations

Church & Dwight’s domestic concentration remains a meaningful consideration. The company generates the large majority of its revenue from the U.S. market, which limits its ability to offset weakness in one geography with strength in another. Changes in U.S. consumer spending behavior, shifts in retail channel dynamics, or domestic regulatory developments can have a more direct and immediate impact on CHD than on more globally diversified peers.

The competitive environment in household and personal care is persistent and intensifying in some categories. CHD’s brands face pressure from both national brand competitors with larger marketing budgets and private label alternatives that have grown more sophisticated in quality and presentation. A misstep in product development, a quality issue affecting consumer trust, or a loss of shelf space at a major retailer could meaningfully affect revenue trends in ways that are difficult to reverse quickly.

The current valuation level introduces its own category of risk. A trailing P/E of 34.31 leaves little room for earnings disappointment. If organic growth slows, margins compress from rising input costs, or management guidance comes in below market expectations, the stock could reprice sharply lower even if the underlying business remains fundamentally sound. Investors paying a premium for predictability need that predictability to actually materialize, and any deviation tends to be punished more severely at elevated multiples. Short interest of nearly 10 million shares suggests a meaningful contingent of investors is positioned for exactly that kind of downside scenario.

Final Thoughts

Church & Dwight continues to do what it has always done — grow steadily, manage its brands well, and convert revenue into reliable free cash flow. The February 2026 dividend increase to $0.308 per quarter extends the growth streak to 29 consecutive years and underscores the company’s commitment to returning capital to shareholders in a measured, sustainable way. The payout ratio of 39% is one of the lowest it has been in years, which means the dividend has room to keep growing even if earnings growth moderates.

The valuation is not cheap, and the analyst consensus price target sitting almost exactly at the current share price suggests limited near-term upside. But CHD has never really been about near-term upside. It’s a compounder, a business that quietly builds shareholder value through consistent execution, brand investment, and disciplined cash flow management. For investors who value that kind of predictability, sound management continuity, and a dividend they can count on through multiple market cycles, Church & Dwight continues to stand out as a core holding worth owning.