Updated 2/25/26

Cass Information Systems (CASS) delivers payment and information processing services to some of the largest corporations in the country, with a business model built around precision, consistency, and cash flow stability. The company supports a dividend yield of 2.82% and maintains a conservative payout ratio of 54%, reflecting a more earnings-covered distribution profile than in prior years. Under CEO Martin Resch, Cass continues to sharpen its focus on core verticals following the divestiture of non-core operations, while generating steady returns on equity and sustaining a low-volatility profile that suits income-oriented portfolios.

Recent Events

Cass Information Systems has been operating quietly but effectively in recent months, consistent with the low-drama character that long-term shareholders have come to expect. The company completed its exit from the Telecom Expense Management business, a strategic move that management signaled was aimed at concentrating resources on the payment processing and data services segments where Cass has the deepest competitive positioning. That sharpened focus appears to be bearing fruit at the margin level, with the company posting a profit margin of 16.93% on revenues of approximately $207.4 million, a meaningful improvement over the 9.5% margin reported in the prior period.

The broader small-cap industrials space has been mixed heading into early 2026, but Cass has held its own. Market capitalization currently stands near $587 million, reflecting a recovery in the share price from the lows seen earlier in the 52-week range. The company’s return on equity of 13.18% reflects continued operational discipline, and with a beta of just 0.45, the stock continues to sit well below market volatility levels. Short interest remains modest at approximately 210,100 shares, suggesting limited conviction among bearish traders that the current valuation is overstretched.

The most recent dividend payment of $0.32 per share, paid in December 2025, marked a step up from the $0.31 quarterly rate that had been in place since early 2025, continuing the company’s unbroken pattern of incremental annual increases.

Key Dividend Metrics

📈 Forward Dividend Yield: 2.82%

💰 Annual Dividend: $1.28 per share

📆 Last Dividend Payment: $0.32 per share (December 2025)

🧮 Payout Ratio: 54.11%

📊 EPS: $2.31

📉 Beta: 0.45

🔁 Dividend Frequency: Quarterly

💵 Book Value Per Share: $18.88

📎 Price/Book: 2.38

🔁 Last Stock Split: 6-for-5 on December 3, 2018

Dividend Overview

Cass pays a dividend that prioritizes reliability over headline size, and with a current yield of 2.82%, it sits in a reasonable range for income investors seeking steady returns without excessive risk. At $1.28 annually, the dividend is well covered by earnings of $2.31 per share, producing a payout ratio of 54.11% that is notably more conservative than the 81% ratio reported in the prior year. That improvement reflects both stronger net income and a management team that appears comfortable letting earnings grow faster than the dividend in the near term.

The lower payout ratio is actually a positive development for long-term holders. It creates additional headroom for future increases and reduces the vulnerability of the dividend to an earnings softer patch. Cass does not need to stretch to fund its distribution, and that kind of built-in cushion is exactly what income investors should want from a specialty services company operating in a niche that can be sensitive to macroeconomic volumes in freight and utilities payments.

The quarterly cadence has been steady for years, and the most recent raise to $0.32 per share continues a pattern of modest but dependable annual step-ups that reflect the measured capital allocation philosophy of the current management team.

Dividend Growth and Safety

Reviewing the recent dividend history tells a clear story of slow, consistent progression. Cass paid $0.29 per quarter throughout most of 2023, moved to $0.30 in late 2023 and held that rate through most of 2024, then stepped to $0.31 in early 2025 before closing the year at $0.32 in December. That trajectory, while modest in dollar terms, represents an unbroken string of annual increases that long-term shareholders can track with confidence.

The safety profile of the dividend has arguably improved compared to a year ago. With a payout ratio now at 54%, the dividend is covered by earnings with significant margin to spare. Net income of $31.1 million against a modest market cap and disciplined cost structure means the company is generating real earnings power relative to its size. The profit margin expansion to nearly 17% from the single-digit levels of the prior period is a material shift that strengthens the foundation under the dividend.

The company’s low beta of 0.45 is an underappreciated element of dividend safety. When the stock does not move violently with the broader market, income investors are less likely to face the kind of sentiment-driven drawdowns that tempt dividend-focused holders to sell at inopportune times. Cass is not the kind of stock that generates exciting headlines, but it is exactly the kind of stock that allows investors to collect quarterly payments without losing sleep. With earnings growing faster than the dividend and the payout ratio declining, there is reasonable basis for expecting further incremental raises in the quarters ahead.

Chart Analysis

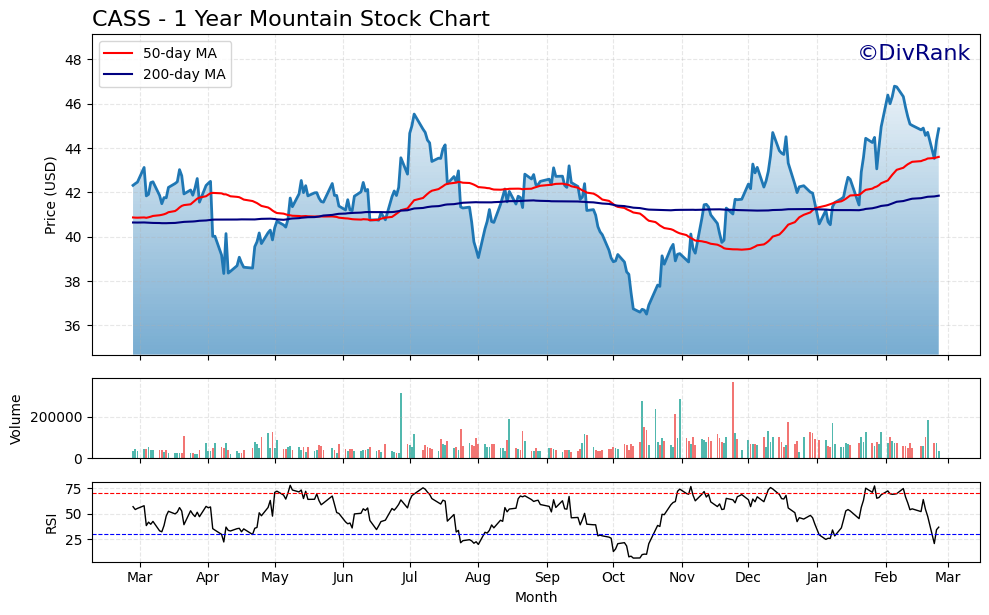

Cass Information Systems has staged a meaningful recovery over the past year, climbing from a 52-week low of $36.51 to its current price of $44.87, a gain of nearly 23% from the trough. The stock reached a peak of $46.79 earlier in the trailing twelve-month window, and at the current quote it sits just 4.1% below that high-water mark. That kind of range compression near the top of a year-long advance typically reflects a stock that has done the hard work of trend repair and is consolidating rather than rolling over, which is an encouraging backdrop for long-term income investors sizing up an entry.

The moving average picture reinforces that constructive read. Cass is trading above both its 50-day moving average of $43.60 and its 200-day moving average of $41.85, and critically, the 50-day has crossed above the 200-day to form what technicians call a golden cross. That configuration signals that shorter-term momentum has aligned with the longer-term trend, a condition that has historically been associated with sustained upward price action rather than one-off bounces. The roughly $1.27 cushion between the current price and the 50-day, and the wider $3.02 gap above the 200-day, suggest the trend has enough underlying support to absorb normal day-to-day volatility without immediately threatening the bullish structure.

The one area that warrants attention is the RSI reading of 36.84, which is sitting in the lower end of the neutral zone and approaching oversold territory below 30. For a stock near the top of its 52-week range, a softening RSI tells you that near-term selling pressure has been absorbing recent strength, and a further pullback toward the 50-day moving average around $43.60 would not be out of character. Importantly, that kind of modest retracement would still leave the golden cross intact and the broader uptrend undisturbed, so it represents process rather than a red flag.

For dividend investors, the technical setup for Cass reads as constructive with a patient posture warranted. The trend is up, the moving averages are positively aligned, and the stock is within striking distance of new 52-week highs. The cooling RSI actually offers a more attractive risk-reward entry point than chasing the stock at its recent peak, and investors looking to build or add to a position may find that a minor pullback toward the $43 to $44 range provides a better cost basis without any meaningful deterioration in the underlying trend.

Cash Flow Statement

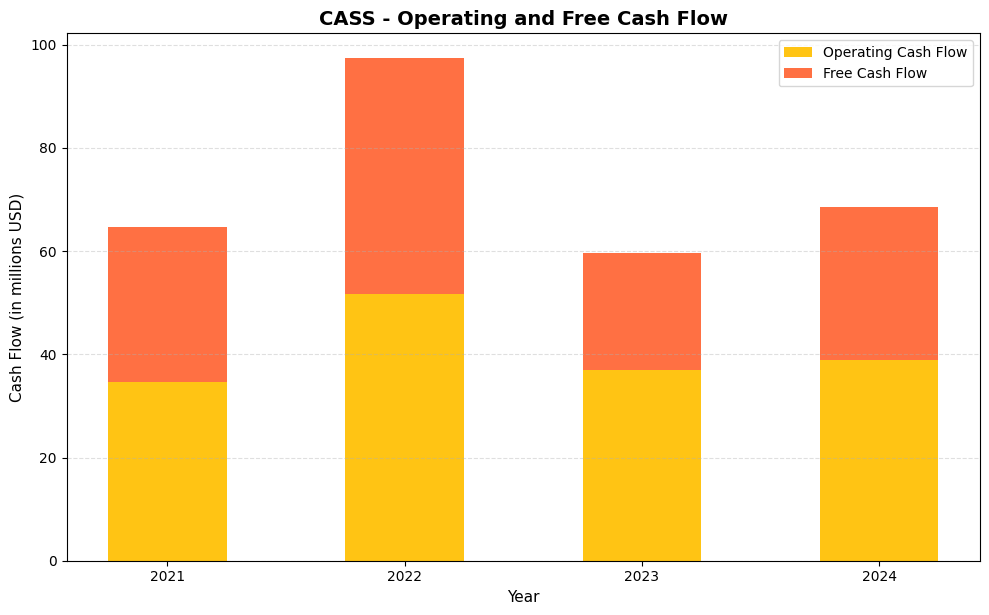

Cass Information Systems has generated positive operating cash flow in each of the four years shown, ranging from $34.5 million in 2021 to a peak of $51.6 million in 2022, then settling back to $38.9 million in 2024. Free cash flow followed a similar arc, reaching $45.7 million in 2022 before compressing to $22.6 million in 2023 and recovering to $29.6 million in 2024. Against an annual dividend obligation that runs well below $20 million at current payout levels, the free cash flow figures consistently provide meaningful coverage, which speaks directly to the sustainability of the dividend. Even in the softer years, the company retained enough cash generation to fund distributions without stretching the balance sheet.

The 2022 results stand out as a high-water mark, likely reflecting a favorable mix of transaction volume and float income during a period of rising interest rates, a key revenue driver for Cass given its banking operations. The retreat in 2023 free cash flow to $22.6 million owed partly to elevated capital expenditures relative to prior years, which compressed the conversion of operating cash into free cash, yet operating cash flow itself held reasonably firm at $36.9 million. The partial recovery in 2024, with free cash flow climbing back to $29.6 million on operating cash of $38.9 million, suggests capital spending is normalizing and efficiency is improving. For income investors, the consistent positive free cash flow across all four periods reinforces confidence that the dividend is being funded from genuine business operations rather than from borrowing or asset sales.

Analyst Ratings

Analyst coverage of Cass Information Systems remains sparse, which is typical for a small-cap specialty services company with a market cap below $600 million. With one analyst actively covering the name, the lone price target on record stands at $50.00, representing approximately 11.4% upside from the current price of $44.87. That target, while reflecting a single data point rather than a broad consensus, is nonetheless meaningful in that it sits above current trading levels and suggests the covering analyst views the stock as modestly undervalued relative to its earnings and dividend profile.

The absence of a formal consensus rating does not diminish the investment case for income-focused holders. Cass tends to attract patient, fundamentals-driven investors rather than momentum traders, and limited analyst coverage can itself be a source of pricing inefficiency that benefits those willing to do independent research. The stock’s current P/E of 19.42 and its improving margin profile provide a reasonable basis for the $50 price target, particularly if the company continues to grow net income at a pace that allows for ongoing dividend increases and potential share repurchase activity.

Earning Report Summary

Cass Information Systems has delivered a materially stronger earnings profile over the most recent reporting period, with EPS of $2.31 and net income of $31.1 million representing a significant improvement from prior-year figures. The profit margin of 16.93% is one of the more compelling data points in the current report, as it reflects not just top-line stability but genuine improvement in the cost and revenue mix of the business.

Stronger Margins, Better Earnings

The most notable development in the recent financial results is the dramatic improvement in profitability relative to the 9.5% profit margin reported in the prior year. At nearly 17%, the current margin suggests that the combination of the Telecom Expense Management divestiture and continued operational discipline has meaningfully changed the earnings quality of the business. Return on equity of 13.18% is solid for a company operating in a niche services model, and it suggests that management is deploying the equity base productively.

Focused on the Core

The strategic exit from the Telecom Expense Management segment has clarified the company’s focus on payment processing and information services for large enterprises in transportation and facility expense verticals. That focus appears to be paying off in margin terms. Revenue of $207.4 million is the base from which a leaner, higher-margin business is now operating, and the company’s ability to convert that revenue into $31.1 million of net income reflects well on the management team’s execution over the past year.

Capital Allocation and Shareholder Returns

Consistent with prior periods, Cass has continued to return capital to shareholders through its quarterly dividend. The most recent raise to $0.32 per share in December 2025 was incremental but meaningful, and the payout ratio of 54% leaves substantial room for the company to sustain and grow the dividend even if earnings were to pull back modestly. Share repurchase activity has historically been a supplemental component of the capital return program, and with a current P/E below 20, any buyback activity at current prices would be accretive to per-share earnings.

Looking Ahead

The company enters 2026 with a cleaner business model, stronger margins, and a dividend that is better covered by earnings than it has been in recent years. Management’s conservative approach to capital allocation and its focus on operational precision in the core processing segments provide a reasonable foundation for continued steady performance. The macro environment for freight and utilities payment volumes will remain a key variable, but the internal improvements visible in the income statement suggest Cass is not relying on volume tailwinds to deliver results.

Management Team

Cass Information Systems is led by Martin Resch, who stepped into the CEO role in early 2023. With a strong background in financial technology, enterprise risk, and operational efficiency, Resch brings a measured and strategic approach to the business. Before joining Cass, he held senior positions at Bank of the West, where he was responsible for areas like strategy, digital banking, and operations. That blend of experience is well suited for a company like Cass, which straddles both the financial services and data-processing worlds. The divestiture of the Telecom Expense Management segment and the resulting margin improvement reflect the kind of focused strategic decision-making that Resch has brought to the leadership role.

The executive team around him reflects deep institutional knowledge. Tony Urban, who leads the Transportation Information Services segment, has been with the company for decades, giving him a firm grasp of the client base and the nuanced nature of this business. Jim Cavellier, the CIO, oversees the company’s technology strategy, ensuring systems remain secure and scalable. The board is composed of seasoned professionals across finance, technology, and audit, people who understand the regulatory landscape and the importance of risk oversight. Collectively, leadership at Cass leans conservative, prioritizing sustainable growth over short-term gains, and the financial results of the past year suggest that approach is delivering.

Valuation and Stock Performance

Shares of CASS are currently trading at $44.87, near the upper portion of the 52-week range of $36.07 to $47.43. The stock has recovered meaningfully from its lows and is within reach of its 52-week high, reflecting the market’s recognition of the improved earnings profile. At a trailing P/E of 19.42 and a price-to-book of 2.38, the valuation is not stretched for a company with a 16.93% profit margin, a clean balance sheet, and a track record of consistent dividend growth.

The $50.00 analyst price target implies roughly 11% upside from current levels, and when combined with a 2.82% dividend yield, the total return potential over the next 12 months is modest but meaningful for a low-beta holding. With a beta of 0.45, Cass continues to offer well below average price volatility relative to the broader market, which makes the current valuation feel more reasonable on a risk-adjusted basis than raw P/E comparisons might suggest.

The stock’s positioning near the top of its 52-week range reflects genuine fundamental improvement rather than speculative enthusiasm. Small-cap specialty services companies like Cass rarely attract the kind of institutional momentum that drives sharp re-ratings, but the current setup, improving margins, a covered dividend, and a single analyst target above the current price, provides a reasonable case for continued participation at current levels for income-focused investors.

Risks and Considerations

Cass operates in a segment of the economy that is sensitive to transaction volumes in freight, transportation, and facility services. A slowdown in industrial activity or a contraction in shipping volumes could pressure the number of invoices processed and reduce fee-based revenue. While the company’s margin improvement has been impressive, a meaningful volume decline would test whether that efficiency can be sustained without top-line support.

The interest rate environment is a dual-edged factor for Cass. The company benefits from rate-sensitive assets on its balance sheet, similar to a bank, and prior periods demonstrated that rising net interest margin contributed positively to net income. A sustained decline in interest rates could reduce that tailwind and put pressure on the revenue components tied to float and investment income, making the interest rate outlook an important variable to monitor in 2026.

Technology and cybersecurity risk is inherent to any business processing large volumes of financial transactions and sensitive enterprise data. Cass handles payment and information flows for major corporations, and any disruption to system availability or a data security incident could damage client relationships and trigger regulatory scrutiny. The company has avoided high-profile issues to date, but the threat landscape continues to evolve and requires ongoing investment to manage effectively.

Client concentration is another factor worth understanding. A relatively small number of large enterprise clients contribute meaningfully to Cass’s overall processing volumes. If any of those clients were to bring payment processing in-house, switch to a competitor, or renegotiate pricing terms, the impact on revenue and margins could be disproportionate to the size of that individual relationship. This is a common structural feature of specialized B2B service businesses, but it is a risk that does not disappear simply because it is familiar.

Final Thoughts

Cass Information Systems enters 2026 with arguably its strongest earnings foundation in recent memory. The profit margin improvement to nearly 17%, the decline in the payout ratio to 54%, and the continued quarterly dividend increases all point to a business that is executing well on its core mission. The divestiture of the Telecom Expense Management segment has clarified the strategic picture, and the financial results suggest the trade-off was well worth it.

At $44.87, the stock is not a deep value play, but it does not need to be. For income investors, the appeal of Cass lies in what it consistently does rather than what it might do. The dividend is safe, the balance sheet is clean, the volatility profile is low, and the management team has demonstrated a willingness to make difficult decisions in service of long-term shareholder value. The lone analyst covering the name sees $50 as fair value, providing a reasonable margin of appreciation above the current price. Cass will never top the performance charts, but for patient investors who value precision over excitement, it continues to make a compelling case for a place in an income-focused portfolio.