Updated 4/14/25

Cable One (CABO) is a broadband-focused communications provider serving smaller markets across the U.S., with a business model centered on consistent cash flow and infrastructure-driven service. Over the past year, the stock has seen a sharp decline from over $425 to around $263, driven by revenue pressure, increased competition, and shifts in customer trends. Despite these challenges, the company remains focused on long-term sustainability, supported by stable operating cash flow, disciplined capital spending, and a 4.45% dividend yield. With a leadership team emphasizing efficient execution and a business that still generates strong free cash flow, Cable One is navigating its reset phase with a measured, operationally grounded approach.

Recent Events

The past year hasn’t been easy for Cable One shareholders. The stock has lost more than 30% over the last 12 months and is now trading around $262, well below its 52-week high of $437. That decline reflects broader concerns around subscriber retention, price sensitivity, and increased competition—even in the rural strongholds where Cable One usually operates with limited disruption.

In the most recent quarter, revenue declined by 6% year-over-year, a clear signal that growth has hit a few roadblocks. Profit margins have thinned out, too, with net income for the trailing twelve months landing at just $14.5 million—resulting in a profit margin under 1%. Not exactly a high-margin business right now.

Debt is another red flag. The company has racked up $3.6 billion in total debt, with a debt-to-equity ratio over 200%. That’s high by any standard, and with interest rates still elevated, it adds pressure to future cash flow.

Yet despite all these headwinds, the dividend has held up—and even grown. That’s not something every company in this sector can claim.

Key Dividend Metrics

💸 Forward Dividend Yield: 4.45%

📈 5-Year Average Yield: 1.55%

📆 Dividend Payout Ratio: 457.36%

🔁 Dividend Growth: Consistent in recent years

📊 Free Cash Flow Coverage: Supported by $305M in levered FCF

📍 Latest Dividend Date: March 7, 2025

📍 Ex-Dividend Date: February 18, 2025

Dividend Overview

At today’s share price, Cable One’s annual dividend of $11.80 works out to a 4.45% yield. That’s a big step up from the 1.55% average yield over the last five years. In a market where yield is getting harder to come by, that number alone will draw attention from income-focused investors.

However, on an earnings basis, the dividend looks stretched. The payout ratio is over 450%, based on trailing twelve-month earnings per share of just $2.57. That’s not a typo. EPS doesn’t come close to covering the dividend right now.

But earnings don’t always tell the whole story. In businesses like Cable One—heavy on infrastructure and capital investment—cash flow can paint a very different picture. And here, the picture looks a lot better. The company produced $664 million in operating cash flow and $305 million in levered free cash flow over the past year. That’s more than enough to cover the dividend, which costs the company roughly $66 million annually given the current share count.

So while the payout looks risky if you only glance at earnings, the cash coming in tells us the dividend is still on solid ground—at least for now.

Dividend Growth and Safety

Cable One’s dividend hasn’t just held steady—it’s been growing. That sends a strong message to shareholders that returning capital remains a top priority for management. In a sector where others have taken a step back or frozen payouts, CABO has kept moving forward.

That said, the path isn’t without risk. The heavy debt load, shrinking revenue, and changing consumer preferences all raise questions about the long-term sustainability of current payout levels. If cash flow starts to slip, the cushion between free cash and dividend obligations could shrink quickly.

Debt remains the elephant in the room. The company’s debt-to-equity ratio north of 200% isn’t something to overlook. If EBITDA weakens further, interest payments could eat into cash reserves and force tough decisions on capital returns.

Ownership dynamics also come into play here. Institutions hold over 105% of the float, a sign of both confidence and potential volatility. With over 22% of the float sold short, this is a stock that can move sharply in either direction based on news or earnings.

But for now, Cable One’s dividend is backed by cash—even if earnings and headline numbers suggest otherwise. If the company can stabilize revenue and continue to manage debt effectively, it has a shot at keeping those dividend checks flowing for a while longer.

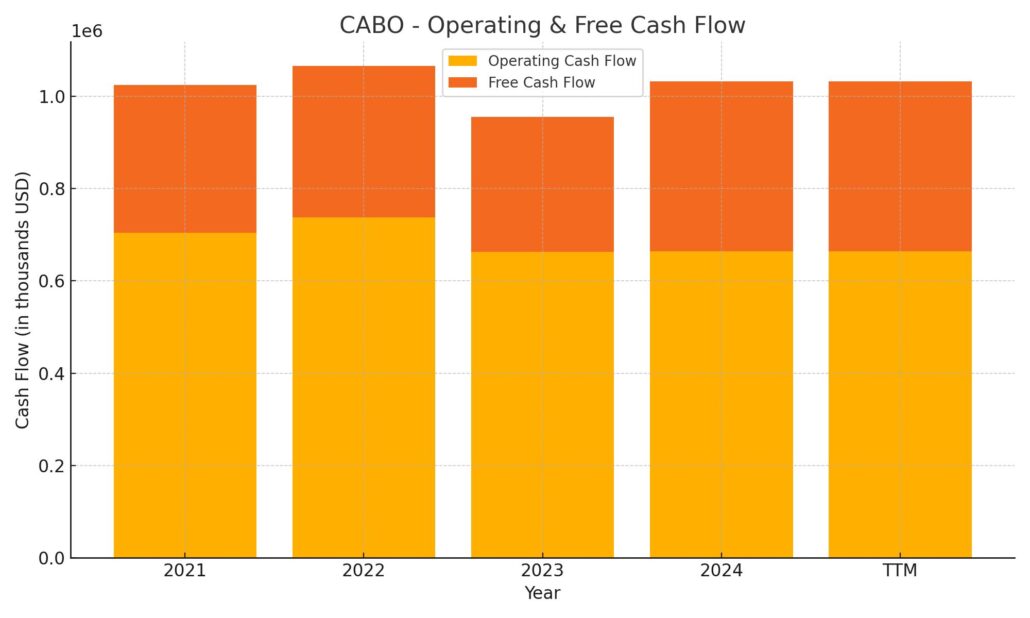

Cash Flow Statement

Over the trailing twelve months, Cable One generated $664 million in operating cash flow, maintaining a consistent performance compared to previous years. This stability suggests that despite revenue pressure, the company’s core business still produces dependable cash. Free cash flow came in at $368 million—healthy coverage for dividends and a positive signal for shareholders looking for ongoing returns. Capital expenditures were trimmed to $296 million, a decline from the $370 million spent the prior year, showing some tightening in spending while preserving essential investments.

On the investing side, cash outflows reached $564 million, significantly higher than in 2023 but still well below the extraordinary $2.4 billion figure seen in 2021. Financing activity also leaned negative, with $136 million in outflows. Debt management appears active, with $175 million in new issuance offset by nearly $239 million in repayments. Interest costs remain elevated at $149 million, but the current strategy reflects a balanced approach—funding operations, covering obligations, and protecting the dividend despite a declining end cash position of $154 million.

Analyst Ratings

🔍 Cable One (CABO) has seen a mix of sentiment from analysts recently, reflecting both the hurdles it faces and the long-term possibilities. The consensus rating currently stands at “Hold,” based on the views of four analysts. Among them, one has issued a “Buy” rating, two are on “Hold,” and one has rated the stock a “Sell.”

🎯 The average 12-month price target sits at $417.75, which points to a potential upside of nearly 57% from where the stock is currently trading. Analyst expectations are spread out, with targets ranging from a low of $240 to a high of $650, signaling uncertainty but also room for optimism if fundamentals stabilize.

📉 Some of the recent downgrades have stemmed from concerns over shrinking top-line revenue, the company’s high debt load, and uncertainty surrounding returns from infrastructure upgrades like DOCSIS 4.0. There’s also growing competitive pressure from fiber and fixed wireless providers moving into Cable One’s traditionally protected rural markets.

📈 On the flip side, there’s still support from certain analysts who appreciate Cable One’s focus on broadband over legacy cable services and its position in less saturated areas. The company’s reliable cash flow and continued dividend payouts are seen as positives that could help anchor its valuation even as growth slows.

Earning Report Summary

A Tough Quarter With Some Bright Spots

Cable One’s latest earnings report shows a company facing some real headwinds, but also making moves to keep things steady where it matters most. For the fourth quarter, the company posted a net loss of $105.2 million, which stands in sharp contrast to the $103.5 million profit from the same period a year earlier. That swing mainly came from some big non-cash hits tied to its investment in Mega Broadband Investments (MBI). A $195.7 million downward adjustment and a $111.7 million impairment charge hit hard, although a $71.5 million gain from amending the MBI agreement helped offset some of the damage.

Revenue for the quarter came in at $387.2 million, about 6% lower than last year. Residential internet revenues dropped 5.4%, mostly because of lower average revenue per user and fewer subscribers—some of that tied to the end of the government’s Affordable Connectivity Program. On the plus side, the business internet side showed some life with a modest 2.3% gain, thanks to more small business customers signing on.

Cash Flow Stays Strong, Spending Comes Down

Despite the earnings loss, the cash flow story looked more stable. Adjusted EBITDA was $211 million for the quarter, down 7% from a year ago, and the margin landed at 54.5%, still a solid number. Operating cash flow actually improved, rising to $167.6 million from $151.7 million the previous year. That’s thanks in part to better working capital management and less cash going out the door for interest and taxes. Capital spending was pulled back in a big way, too—$71.9 million this quarter compared to $115.6 million a year ago.

For the full year, revenue was down about 6%, totaling $1.58 billion. Net income for all of 2024 came in at just $14.5 million, a sharp drop from the $224.6 million the company earned in 2023. Adjusted EBITDA was $854 million, down nearly 7%, but operating cash flow held steady at $664 million. Capital expenditures for the year dropped almost 23%, signaling a more cautious approach to investment.

Looking Ahead

In terms of returning value to shareholders, Cable One paid out $16.9 million in dividends in Q4 and $67.9 million across the year. It also made moves to improve its financial flexibility, including increasing its credit line by $250 million. Additionally, the company reworked its agreement with MBI in a way that should ease some balance sheet pressure and help manage leverage going forward.

CEO Julie Laulis offered a bit of optimism, pointing out that residential internet revenue per user stabilized in the second half of the year. She also noted that if you strip out the end of the ACP and one small acquisition, the company actually added about 2,200 residential broadband customers. According to Laulis, the company is taking the right steps to lay the groundwork for more sustainable, long-term growth—even if the short term remains bumpy.

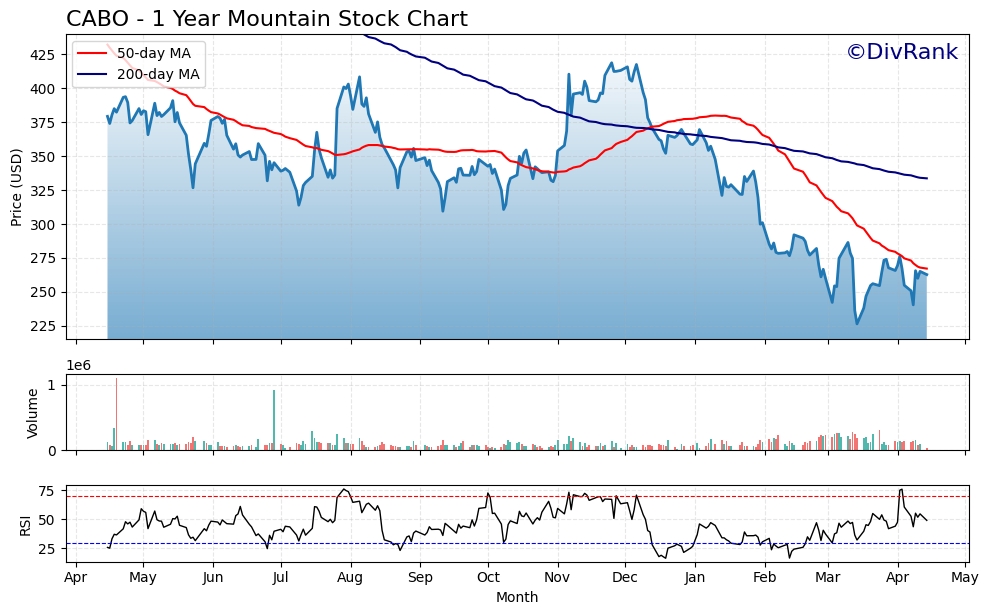

Chart Analysis

Price Action and Moving Averages

CABO has been on a clear downtrend over the past year. The price peaked around the $425 range last summer but has steadily lost ground since then. The 50-day moving average (red line) started rolling over in late November and has been trending lower ever since, now sitting well below the 200-day moving average (blue line). That crossover, which occurred back in December, typically reflects a longer-term bearish tone and has played out just that way in the months since.

More recently, the stock has found some footing around the $250–$260 level, with a few failed attempts to break higher. Every push toward the 50-day line has met resistance, showing that sellers are still in control of the short-term trend. For a stock that once held comfortably above $400, this is a sizable reset.

Volume and Participation

Volume has stayed relatively muted for most of the year, aside from a few spikes during sharp price moves, particularly in April and again back in July. These surges in volume, especially on down days, can suggest institutional activity—potentially some funds rotating out or trimming their positions. The more recent activity looks like a mix of weak hands exiting and bargain hunting stepping in.

That said, there hasn’t been any strong, sustained volume to confirm a reversal. Most of the action has occurred in low-volume environments, which makes any upward movement less convincing. Without heavier buying coming in to support the price, it’s tough to say the worst is over just yet.

Relative Strength Index (RSI)

The RSI spent much of the first quarter of the year below the midpoint of 50, hanging near oversold territory. A few brief rallies pushed it closer to 70—especially in early April—but those were short-lived. The latest bounce pulled the RSI up, but not with much conviction. It remains in a range that doesn’t indicate either exhaustion from sellers or a fresh wave of buyers stepping in.

Overall, momentum appears weak and somewhat directionless. The stock isn’t deeply oversold right now, but it’s certainly not in a position of strength either. Until RSI can hold above 50 for an extended period, rallies may continue to fizzle out quickly.

Overall Takeaway

The broader technical setup for CABO remains soft. The stock continues to struggle below both its key moving averages, volume hasn’t confirmed any true buying interest, and momentum indicators aren’t flashing any urgency on the upside. It looks like the price is trying to base around current levels, but without stronger signals, that process could take time. For now, the chart is still showing signs of caution rather than recovery.

Management Team

Cable One’s leadership brings a steady, long-term mindset to the table, marked by a commitment to operational discipline and thoughtful capital allocation. Julie Laulis, who serves as both CEO and Chair of the Board, has been with the company for more than 20 years and has led it as CEO since 2017. Her focus has been on pivoting the company away from its legacy cable roots and toward a broadband-first model that targets smaller, less competitive markets.

Throughout her tenure, Cable One has made a series of acquisitions and strategic investments aimed at expanding its broadband footprint while maintaining financial flexibility. The company has consistently emphasized cash flow generation, network quality, and shareholder returns over headline growth. That’s been reflected in its dividend policy and its cautious stance on new capital expenditures.

Other members of the leadership team bring deep backgrounds in finance, network operations, and regional service delivery. Their collective experience shows in the way the company handles leverage, infrastructure planning, and customer service in markets often overlooked by larger providers. The executive team’s tone has stayed pragmatic, focused on sustainability and efficient operations over high-risk expansion.

Valuation and Stock Performance

Cable One’s share price has been on a sharp decline over the last year. Trading near $263 today, the stock has fallen significantly from its highs above $425 just a year ago. While the drop reflects growing concerns around revenue pressure and subscriber trends, it’s also led to a more favorable valuation for long-term investors looking beyond the headlines.

At first glance, the stock looks expensive, with a trailing P/E ratio well above 100. But that number is skewed by non-cash charges and temporary earnings impacts. When looking at enterprise value to EBITDA, a more reliable measure for a capital-heavy business like this one, Cable One trades at around 6.8 times EBITDA—much more reasonable and in line with industry peers.

The price-to-book ratio is now under 1.0, which means the stock is trading below the value of its net assets. This can often indicate market pessimism but also potential value for those willing to wait out the current cycle. The price-to-sales ratio is also sitting around 1.0, reflecting a business that’s generating steady top-line revenue but not being rewarded for it by the market—at least not yet.

A major part of the valuation story is the dividend. With a yield of 4.45%, it’s not only significantly above the company’s five-year average, but it’s also supported by strong free cash flow rather than net income. That distinction is important, as it shows the business is still producing real money that can be returned to shareholders, even during periods of earnings compression.

Risks and Considerations

Cable One isn’t without its share of risks, and anyone following the story needs to stay aware of the potential pitfalls.

The most obvious issue is leverage. The company carries over $3.6 billion in total debt, and its debt-to-equity ratio sits above 200%. That’s high by any measure and leaves limited room for error. While cash flow currently supports debt payments, any decline in EBITDA or unexpected increase in borrowing costs could put that balance under pressure.

Customer churn is another concern. The company experienced subscriber losses following the expiration of the Affordable Connectivity Program, and its average revenue per user has slipped as well. While the company still operates in less crowded markets, those areas are starting to attract competition from wireless and regional fiber players.

Execution also remains a variable. Cable One is in the middle of network upgrades, including its rollout of DOCSIS 4.0, and these projects come with both costs and uncertainty. If those investments don’t deliver the expected returns or operational efficiencies, they could weigh on margins and slow down progress on deleveraging.

There are broader market risks, too. Regulatory changes in broadband access or infrastructure funding could shift the landscape, and with such a concentrated operating model, any disruption in customer behavior could have an outsized impact. The stock’s high short interest and relatively low average trading volume also raise the risk of outsized volatility on both good and bad news.

Final Thoughts

Cable One finds itself at a turning point. Once a quiet, high-performing stock, it’s now in the process of resetting expectations. The market has adjusted, and the share price reflects current headwinds. But what hasn’t changed is the company’s steady hand, its cash-generating core, and its ability to support a reliable dividend.

While growth has slowed, and the market environment is more competitive, the business continues to do what it’s been built to do: serve less contested regions with consistent broadband access and dependable service. The company is not chasing growth at all costs, but instead leaning on its long-standing strengths—network reliability, careful financial management, and a slow-but-steady operating approach.

The current valuation suggests the market may be overlooking these strengths. Trading at levels that imply minimal future upside, Cable One is now in a spot where even modest stabilization in subscriber trends or operating margins could shift sentiment. Add in a dividend yield that’s more than just window dressing, and the total return picture starts to look more balanced.

This isn’t a momentum stock or a rapid turnaround story. But for those who value consistency, a disciplined approach to growth, and an emphasis on real cash flow, Cable One still brings meaningful elements to the table. The road ahead might be slower than it once was, but it’s not without direction.