Updated 2/25/26

Broadcom Inc. (AVGO) has grown into one of the most consequential technology companies in the world, combining dominant semiconductor franchises with a rapidly expanding infrastructure software business. Under CEO Hock Tan, the company has executed a disciplined strategy built around cash generation, focused acquisitions, and a relentless push into artificial intelligence infrastructure. The VMware integration has added meaningful recurring revenue, and Broadcom’s custom AI accelerator business continues to attract the largest hyperscaler customers on the planet. With operating cash flow of $27.5 billion, a 13-year dividend growth streak, and a market capitalization approaching $1.6 trillion, Broadcom occupies rare air among income-generating technology companies. Risks remain, from a stretched valuation to integration complexity, but the operational consistency and strategic clarity that define this management team continue to make AVGO a compelling holding for dividend growth investors with a long horizon.

Recent Events

Broadcom has been at the center of the AI infrastructure conversation heading into early 2026, with hyperscaler customers including Alphabet, Meta, and Apple increasingly relying on Broadcom’s custom application-specific integrated circuits, known as XPUs, to build out next-generation AI training and inference clusters. The company’s AI revenue has scaled dramatically over the past several quarters, and Broadcom has guided for continued acceleration in that segment as its three largest XPU customers expand their custom silicon programs. These design wins represent multi-year commitments that give the company unusual revenue visibility in a business that can otherwise be cyclical.

On the software side, the VMware integration has progressed ahead of many early expectations. Broadcom has successfully migrated a significant portion of VMware’s customer base onto subscription arrangements, replacing perpetual licenses with annual contracts that produce more predictable revenue. That shift has contributed meaningfully to margin expansion across the infrastructure software division. The transition has not been without friction, as some VMware customers have pushed back publicly on pricing changes, but the financial results have validated Broadcom’s approach.

Broadcom also continued its disciplined approach to capital allocation over the trailing twelve months, repurchasing shares and sustaining its dividend growth cadence. The company raised its quarterly dividend to $0.65 per share beginning with the December 2025 payment, up from $0.59 in the prior three quarters, extending its consecutive annual dividend increase streak to 14 years.

Key Dividend Metrics

📈 Forward Dividend Yield: 0.74%

💵 Annual Dividend Rate: $2.60

📅 Last Dividend Payment: $0.65 per share (December 22, 2025)

📊 Payout Ratio: 49.48%

📈 5-Year Average Yield: 2.50%

🔁 Dividend Growth Streak: 14 consecutive years

💰 Operating Cash Flow: $27.54 billion (TTM)

🔍 Free Cash Flow: $25.04 billion (TTM)

Dividend Overview

Broadcom’s current yield of 0.74% will not attract investors who screen for high income first. But that number alone tells an incomplete story. The yield is low primarily because the stock price has compounded so dramatically over the past several years, outrunning even Broadcom’s aggressive pace of dividend increases. The annual payout of $2.60 per share represents a genuinely well-covered dividend, supported by $25 billion in free cash flow against a total annual dividend obligation that represents a small fraction of that figure.

The payout ratio of 49.48% is a significant improvement from prior periods when GAAP-based ratios exceeded 100%, a distortion caused by acquisition-related amortization and other non-cash charges. As those charges normalize and earnings have grown, the reported payout ratio now reflects a much healthier picture. Cash flow coverage was already strong, and the GAAP picture has caught up. Broadcom pays its dividend on a consistent quarterly schedule, and the rhythm has been reliable for well over a decade. Income investors who prioritize growth of the dividend over starting yield have been rewarded handsomely here.

The five-year average yield of 2.50% is a useful reference point. Investors who purchased shares when that yield was available have seen both their income stream and their capital appreciate substantially. Today’s entry yield is lower, but the same dynamic, where the dividend grows and the stock price follows, remains intact for patient buyers.

Dividend Growth and Safety

Broadcom’s dividend history over the past three years illustrates a company that treats its payout as a serious commitment rather than an afterthought. Quarterly payments moved from $0.46 in early 2023 to $0.525 by the end of that year, then to $0.53 in September 2024, $0.59 in December 2024, and most recently to $0.65 per share in December 2025. That progression represents a cumulative increase of more than 41% in just under three years, a pace that far exceeds inflation and most traditional income alternatives.

The safety of the dividend is underpinned by one of the strongest free cash flow profiles in technology. With $25 billion in free cash flow against an annual dividend obligation that remains well below $5 billion based on current share count, Broadcom has enormous headroom. The payout ratio of 49.48% on a GAAP earnings basis confirms that even after years of heavy acquisition spending, the business generates enough reported profit to cover the dividend nearly twice over. The software transition underway through VMware adds another layer of safety, as subscription revenue is structurally more stable than transactional hardware cycles.

Return on equity of 31.05% and a profit margin of 36.20% signal a business operating with real pricing power and cost discipline. These are not the metrics of a company that needs to stretch to fund its dividend. Broadcom’s 14-year growth streak is not an accident, and the financial architecture supporting future increases remains firmly in place.

Chart Analysis

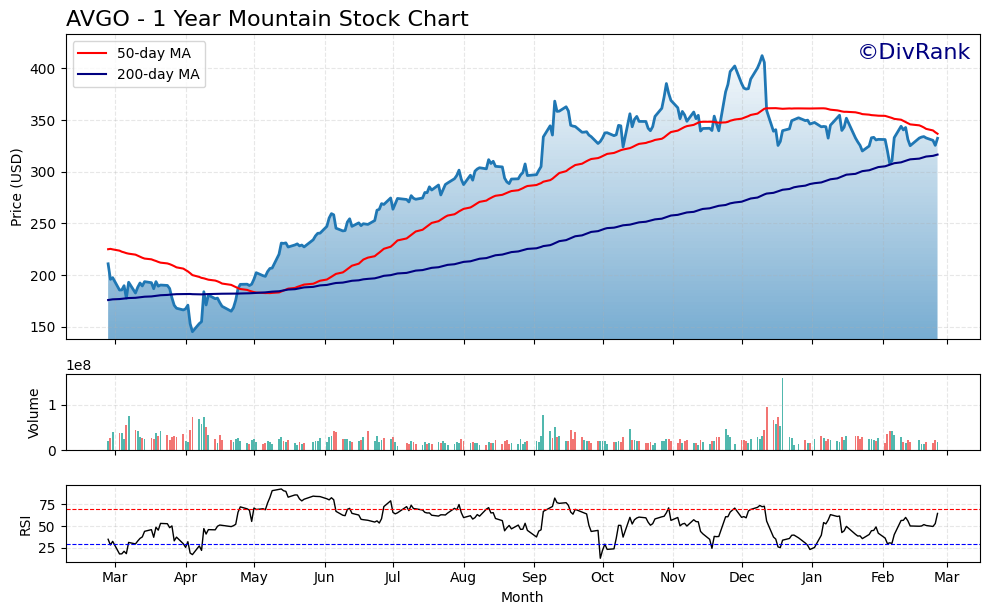

Broadcom’s price chart tells a compelling story of recovery and resilience over the past twelve months. The stock carved out a 52-week low of $145.42 before staging a dramatic reversal, ultimately reaching a peak of $412.18 before pulling back to its current level of $332.31. That round-trip represents a gain of more than 128% from trough to present, which speaks to the extraordinary demand that has accumulated in AVGO shares as investors repriced the company’s AI infrastructure opportunity. The current price sits about 19% below the 52-week high, which is not unusual for a stock that appreciated this aggressively in a compressed timeframe, and long-term dividend investors who held through the volatility have been richly rewarded.

The moving average picture is constructive on balance. The 200-day moving average currently sits at $316.59, and AVGO is trading above it at $332.31, confirming that the longer-term trend remains intact and that buyers have defended the stock at structurally meaningful levels. The 50-day moving average at $336.72 is a modest headwind, as price is currently trading just below it by roughly $4.40. Importantly, the 50-day remains above the 200-day, a configuration known as a golden cross that typically reflects sustained bullish momentum. This alignment suggests the recent softness in price is a consolidation episode within a broader uptrend rather than a meaningful breakdown in trend structure.

The Relative Strength Index reading of 64.54 lands in a sweet spot for dividend investors assessing entry timing. The stock is neither overbought nor oversold, sitting comfortably below the 70-level threshold that often precedes short-term mean reversion. An RSI in the mid-60s on a stock that has more than doubled from its lows is a signal that momentum has normalized in a healthy way, with buyers maintaining control without the frothy excess that invites sharp corrections. This kind of momentum profile tends to support a stable dividend collection environment, as it reduces the probability of a sentiment-driven selloff forcing the stock meaningfully back toward its longer-term support levels.

For dividend investors, the technical setup offers a reasonable backdrop for initiating or adding to a position. The confirmed golden cross, a price above the 200-day moving average, and a non-extended RSI collectively point to a stock in a constructive intermediate-term trend. The gap between the current price and the 52-week high does introduce some near-term overhead resistance as the stock works back toward $412, and the slight dip below the 50-day moving average is worth watching for confirmation of continued support. That said, income-focused investors who prioritize the growing dividend stream over short-term price precision will find the current chart conditions far more favorable than threatening.

Cash Flow Statement

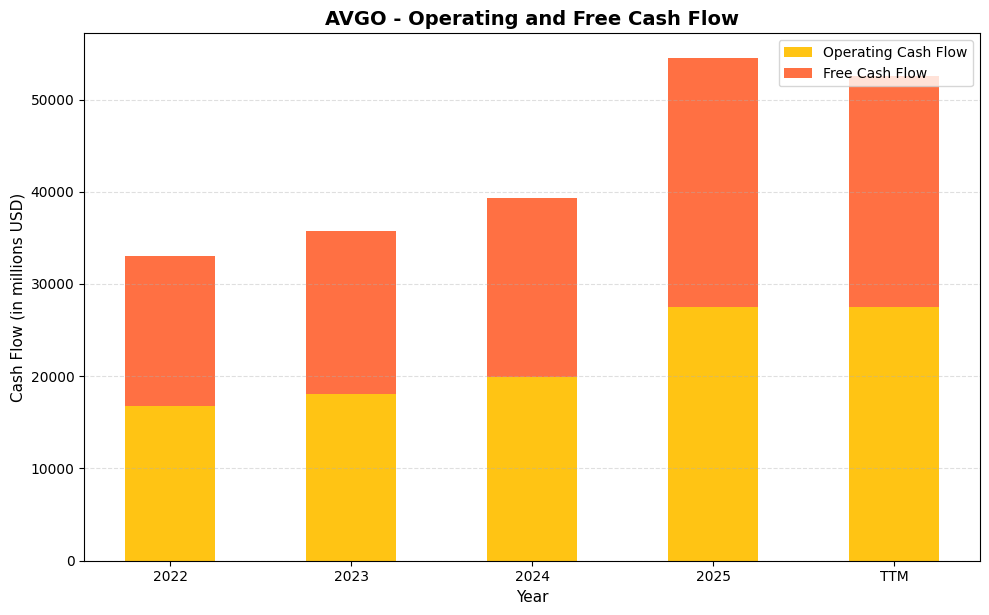

Broadcom’s cash generation machine has shifted into a higher gear following the VMware acquisition, with operating cash flow climbing from $16.7 billion in fiscal 2022 to $27.5 billion in fiscal 2025, a gain of roughly 64% over three years. Free cash flow tracked almost in lockstep, rising from $16.3 billion to $26.9 billion over the same period, which tells you that capital expenditure requirements remain modest relative to the revenue base. The TTM free cash flow of $25.0 billion, slightly below the fiscal 2025 figure, reflects normal timing differences rather than any structural deterioration. For dividend investors, the critical takeaway is that Broadcom generated enough free cash flow in fiscal 2025 alone to cover its annualized dividend commitment several times over, leaving substantial room for continued payout growth without pressuring the balance sheet.

The trajectory here is what separates Broadcom from most dividend growers in the semiconductor space. The company converted operating cash flow into free cash flow at a conversion rate above 97% in fiscal 2023 and fiscal 2024, reflecting a capital-light model where incremental revenue drops to free cash flow with minimal reinvestment drag. Even in fiscal 2025, after absorbing the VMware integration costs and scaling a much larger combined business, the free cash flow conversion remained above 97%. That level of capital efficiency means shareholders are not watching earnings get consumed by heavy equipment spending or facility buildouts. The consistent and widening spread between reported earnings and actual cash generation gives management the flexibility to grow the dividend, reduce debt taken on for the VMware deal, and still pursue opportunistic buybacks, all from a single year’s cash production.

Analyst Ratings

Broadcom commands one of the most enthusiastic analyst followings in the technology sector. Forty-five analysts currently cover the stock, and the consensus sits at strong buy, reflecting broad conviction in the company’s positioning across AI semiconductors and enterprise software. The mean price target of $455.10 implies upside of approximately 37% from the current price of $332.31, a gap that suggests the market may not be fully pricing in the trajectory analysts expect from the AI revenue ramp and continued VMware monetization.

The range of targets is wide, spanning from a low of $335.00 to a high of $535.00, which reflects genuine disagreement about the pace of AI infrastructure spending and how aggressively hyperscalers will expand their custom silicon programs. The low end of the range barely clears the current price, indicating that even the most cautious analysts covering the name see limited downside at these levels. The high end of $535.00 would represent a market capitalization well above $2 trillion, a figure that requires sustained execution on both the semiconductor and software fronts but is not considered unreasonable given the growth rates Broadcom has demonstrated. With the stock trading below the low end of the analyst target range, the current setup is one that the majority of covering analysts view as an attractive entry point for long-term investors.

Earning Report Summary

Broadcom’s most recently reported fiscal results reflected the compounding benefits of its dual-engine strategy in semiconductors and software. Revenue for the trailing twelve months reached $63.9 billion, representing a dramatic acceleration from prior periods and confirming that the VMware integration is contributing at scale. Net income of $23.1 billion and earnings per share of $4.78 demonstrated that this revenue growth is flowing through to the bottom line with impressive efficiency. Profit margins of 36.20% at the net level are exceptional for a company of this size and complexity.

AI Driving Semiconductor Growth

The semiconductor segment continues to be propelled by demand for Broadcom’s custom AI accelerators. The company’s XPU business has scaled rapidly as its largest hyperscaler customers deepen their commitment to custom silicon over merchant solutions. Networking revenue has also benefited from AI cluster buildouts, as the interconnect fabric linking thousands of accelerators requires sophisticated switching and routing solutions that Broadcom supplies. This combination of compute and networking exposure creates a more complete participation in AI infrastructure spending than chip suppliers focused on a single product category.

Software Expansion with VMware

The infrastructure software division has become a meaningful earnings contributor, with VMware subscription conversions progressing steadily. Broadcom’s approach of migrating customers from perpetual licenses to annual subscription arrangements has generated pushback in some quarters but has produced the revenue durability and margin profile management targeted. The recurring nature of this revenue stream provides a meaningful counterbalance to the inherent cyclicality of semiconductor demand, and analysts have credited this mix shift with improving the quality of Broadcom’s earnings.

Profitability and Outlook

Operating cash flow of $27.54 billion and return on equity of 31.05% illustrate that Broadcom is not simply growing in absolute terms but doing so with strong capital efficiency. The company’s ability to convert revenue into cash at this rate, while simultaneously integrating a large software acquisition and investing in next-generation chip development, reflects the operational discipline that has defined Hock Tan’s tenure. Looking forward, the continued scaling of AI revenue and the stabilization of the VMware contribution are expected to sustain earnings growth through fiscal 2026 and beyond.

Management Team

Broadcom’s leadership remains anchored by CEO Hock Tan, who has guided the company since 2006 through a series of transformative acquisitions and strategic pivots that most observers initially questioned and later recognized as prescient. Tan’s approach is defined by rigorous capital discipline, a willingness to restructure acquired businesses aggressively, and an unwavering focus on free cash flow generation. The VMware integration is the largest test of that playbook to date, and the early financial results suggest the methodology is working as designed.

CFO Kirsten Spears has been a steady presence through the financial complexity of large-scale M&A, maintaining creditor confidence and shareholder communication during periods when the balance sheet carried significant acquisition-related leverage. The broader executive team brings together deep expertise in both semiconductor design and enterprise software operations, a combination that is genuinely difficult to assemble and that gives Broadcom an organizational advantage as the two sides of the business become increasingly integrated. This is a management team that has earned the benefit of the doubt through demonstrated execution rather than promises.

Valuation and Stock Performance

Broadcom shares currently trade at $332.31, well below their 52-week high of $414.61 and meaningfully below the analyst consensus price target of $455.10. The stock has pulled back from peak levels reached earlier in the cycle, creating a setup where the current price sits below even the lowest analyst price target of $335.00. The P/E ratio of 69.52 is elevated in absolute terms and reflects the market’s expectation of continued high growth, particularly from the AI revenue stream. Price-to-book of 5.61 against a book value of $59.22 per share similarly reflects a premium that the market has consistently been willing to assign to Broadcom’s earnings quality and growth visibility.

The market capitalization of approximately $1.58 trillion places Broadcom among the handful of largest companies in the world, and sustaining premium valuation at that scale requires consistent execution. Beta of 1.22 indicates the stock moves with somewhat more volatility than the broader market, which is not surprising given its sensitivity to AI infrastructure spending trends and enterprise software renewal cycles. For income-growth investors, the combination of a stock trading below its 52-week high and below the analyst target range, paired with a dividend that grew 10.2% in its most recent increase, presents a more balanced entry point than the stock offered when shares were approaching $415.

Risks and Considerations

The concentration of Broadcom’s AI semiconductor revenue among a small number of hyperscaler customers creates meaningful dependency risk. If any of the three largest XPU customers were to slow their custom silicon programs, bring development in-house, or redirect spending toward alternative architectures, the impact on Broadcom’s revenue trajectory could be significant. The company has acknowledged this concentration in its disclosures, and while these relationships are supported by multi-year design commitments, the technology landscape can shift faster than contract terms.

The VMware integration, while progressing well financially, has generated customer relations friction that deserves ongoing attention. Several large enterprise customers have publicly expressed dissatisfaction with Broadcom’s pricing changes following the acquisition, and a small number have begun evaluating alternative virtualization platforms. If customer attrition in the VMware base accelerates beyond what management has modeled, the subscription revenue trajectory that analysts are counting on could disappoint. Integration of large software businesses into hardware-centric cultures also carries execution risk that does not always show up in early financial results.

Broadcom carries a substantial debt load from its acquisition history, and while free cash flow generation provides a clear path to deleveraging, the balance sheet remains leveraged relative to pre-acquisition levels. A meaningful slowdown in free cash flow, whether from a cyclical semiconductor downturn or a software revenue shortfall, would reduce the financial flexibility that has supported both the dividend growth strategy and share repurchases. Interest expense also represents a real cost that limits the proportion of cash flow available for capital return.

Geopolitical risk, particularly with respect to China, remains a persistent consideration. Broadcom generates a portion of its semiconductor revenue from Chinese customers, and escalating export restrictions or retaliatory trade measures could affect both direct sales and the broader supply chain. Regulatory scrutiny of large technology companies has also intensified globally, and Broadcom’s scale and acquisition history make it a natural subject of ongoing antitrust attention in multiple jurisdictions.

Final Thoughts

Broadcom has constructed one of the more durable business models in technology, combining the growth optionality of custom AI silicon with the cash flow predictability of enterprise subscription software. The dividend growth story is genuine and well-supported, with a 14-year increase streak backed by $25 billion in annual free cash flow and a payout ratio that now sits at a comfortable 49.48% even on a GAAP basis. The most recent increase to $0.65 per quarter, a 10.2% step up, signals that management sees no reason to slow the cadence.

The current stock price below $333, sitting beneath the lowest analyst price target in a 45-analyst coverage universe with a strong buy consensus, is an unusual setup for a company of this quality. It does not guarantee near-term upside, and the valuation at 69 times earnings still demands continued execution. But for investors with a multi-year horizon who want exposure to AI infrastructure and enterprise software through a company with a demonstrated dividend growth commitment, Broadcom’s current position offers a more attractive balance of price, yield growth, and business quality than it has at several points over the past two years.

The risks are real and should be sized appropriately in any portfolio. But Broadcom has consistently turned skeptics into believers by delivering on ambitious targets, and the structural tailwinds driving its two core businesses show no signs of abating.