Updated 2/25/26

Bristol-Myers Squibb (BMY) has made meaningful progress in its ongoing portfolio transition, as newer therapies in oncology, immunology, and cardiovascular disease continue to gain commercial footing. With shares trading near $61.30 and a forward yield of 4.04%, the stock offers a competitive income stream backed by $11.1 billion in free cash flow. The payout ratio has risen to roughly 72% on a reported earnings basis, though that figure reflects the uneven nature of GAAP earnings in a heavy acquisition cycle rather than any true strain on the dividend. A recovering share price, a recently raised quarterly dividend, and a consensus buy rating from 24 analysts all point to a more constructive market view of BMY than was the case just a year ago.

Recent Events

Bristol-Myers Squibb has been active on several fronts heading into early 2026. The company raised its quarterly dividend to $0.63 per share beginning with the January 2026 payment, continuing a pattern of annual increases that has now lifted the per-share quarterly rate from $0.57 in early 2023 to its current level. That kind of consistent progression signals management’s confidence in the durability of the company’s cash generation even as the product portfolio continues to shift.

On the pipeline front, Cobenfy, BMY’s treatment for schizophrenia that launched in late 2024, has been building physician adoption at a pace that analysts are watching closely. The cardiovascular franchise has also drawn attention, with Camzyos continuing to expand its patient base in hypertrophic cardiomyopathy. Meanwhile, Reblozyl has maintained strong momentum in myelodysplastic syndromes and beta-thalassemia, reinforcing the contribution of what the company calls its growth portfolio. These developments have helped steady investor sentiment after a period of significant concern about patent expirations on legacy drugs like Eliquis, Revlimid, and Opdivo.

The company also continues to manage its debt load from the Celgene acquisition and subsequent deals, making measured progress in paying down obligations while preserving the operational flexibility to pursue pipeline opportunities. Shares have recovered substantially from their 52-week low of $42.52, now trading near the top of their annual range at $61.30, reflecting a meaningful improvement in market confidence over the past several months.

Key Dividend Metrics 🧮💸📈🔒

🧮 Annual Dividend Rate: $2.52

💸 Forward Dividend Yield: 4.04%

📈 5-Year Average Yield: 3.52%

🔒 Payout Ratio: 71.97%

📆 Last Dividend Payment: $0.63 per share (January 2, 2026)

📉 Recent Dividend Increase: From $0.62 to $0.63 per quarter

A yield above 4% remains well above BMY’s five-year average of 3.52%, which means investors are still collecting an above-average income stream even as the share price has recovered from its lows. The payout ratio looks elevated at 72% on a GAAP basis, but free cash flow coverage tells a more reassuring story, with $11.1 billion in annual free cash flow comfortably supporting the dividend obligation.

Dividend Overview

Bristol-Myers Squibb has built its dividend reputation on consistency rather than speed. The company does not chase aggressive payout growth, but it does move the dividend in the right direction every year, and that reliability is a meaningful feature for income-focused investors. The most recent increase, from $0.62 to $0.63 per quarter effective with the January 2026 payment, is modest in percentage terms but continues an unbroken sequence of annual raises that stretches back several years.

The current yield of 4.04% still sits above the company’s five-year average, offering new investors an entry point that remains historically generous. While EPS has been clouded by acquisition-related charges and amortization, the underlying cash generation of the business is what actually funds the dividend, and on that measure, BMY is on solid footing. Operating cash flow of $14.2 billion and free cash flow of $11.1 billion leave ample room to cover the dividend and still pursue capital allocation priorities.

Management has been deliberate about aligning dividend growth with the company’s actual financial trajectory rather than making promises the balance sheet cannot keep. That measured approach may not generate headlines, but it is exactly the kind of discipline that sustains a long-term income investment through difficult operating periods.

Dividend Growth and Safety

The dividend growth story at BMY is modest but real. Looking at the recent payment history, the quarterly dividend moved from $0.57 in early 2023 to $0.60 at the start of 2024, then to $0.62 at the start of 2025, and most recently to $0.63 beginning in January 2026. That trajectory represents annual increases of roughly 5%, 3%, and 1.6% respectively, reflecting a company that is calibrating its dividend growth to match its financial progress through a complex transition period.

On the safety front, the 71.97% payout ratio based on reported EPS of $3.46 looks less alarming when placed in context. The company generated $11.1 billion in free cash flow against a total annual dividend obligation that, at $2.52 per share on roughly two billion shares outstanding, represents approximately $5 billion per year. That leaves more than $6 billion in surplus free cash flow after dividends, providing a substantial cushion even before considering the company’s $14.2 billion in operating cash flow.

BMY’s beta of 0.29 is among the lowest in the large-cap pharmaceutical space, meaning the stock tends to absorb broader market turbulence without dramatic price swings. For dividend investors who rely on their income stream and do not want outsized portfolio volatility, that low-beta characteristic is a genuine advantage. Debt remains a consideration, but the combination of strong cash generation, a manageable dividend obligation relative to free cash flow, and consistent management discipline supports a view that the dividend is secure.

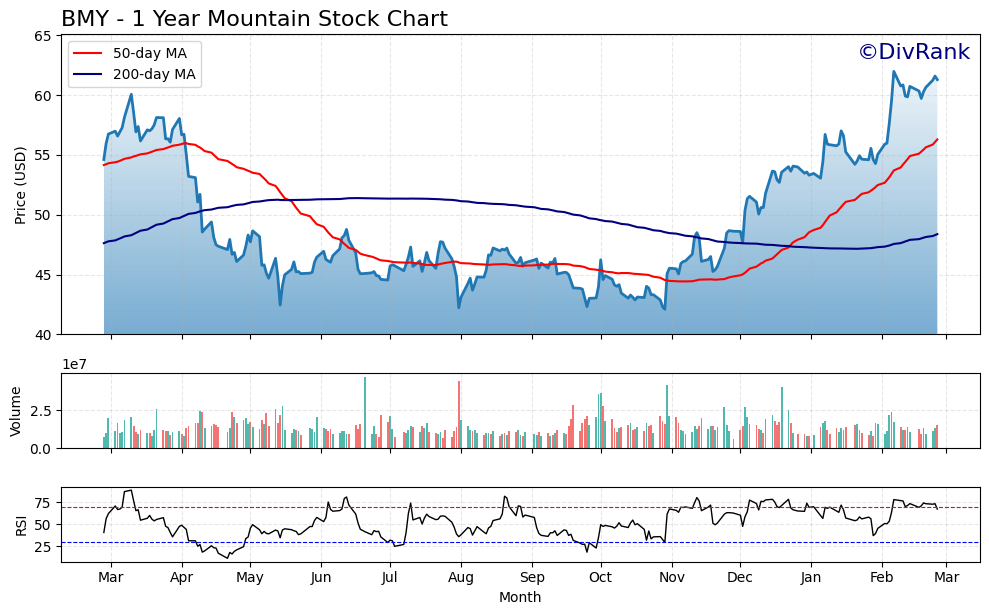

Chart Analysis

Bristol-Myers Squibb has staged a remarkable recovery over the past year, climbing from a 52-week low of $42.10 to its current price of $61.30, a gain of roughly 45.6% from trough to present. That kind of price appreciation is not what most investors expect from a large-cap pharmaceutical dividend payer, but BMY spent much of the prior period being heavily discounted as the market priced in patent cliff concerns and pipeline uncertainty. The stock is now trading within striking distance of its 52-week high of $61.99, sitting just 1.11% below that level, which means the recovery has been broad, sustained, and is approaching a technical test of overhead resistance at that ceiling.

The moving average picture is unambiguously constructive. BMY is trading comfortably above both its 50-day moving average of $56.30 and its 200-day moving average of $48.38, and the 50-day has crossed above the 200-day to form what technicians call a golden cross. This pattern, where shorter-term price momentum pulls the 50-day above the longer-term 200-day average, is one of the more reliable signals that a sustained uptrend has taken hold rather than a brief speculative bounce. The spread between the current price and the 200-day average is now over $12, or roughly 26%, which reflects just how decisively sentiment has shifted toward BMY over the past several months.

The RSI reading of 67.13 deserves careful attention. At that level, BMY is approaching but has not yet reached the traditional overbought threshold of 70, which means momentum remains strong without flashing an immediate reversal warning. For dividend investors who are considering a new position, this is a nuanced signal. The stock has enough upward momentum to suggest the trend is intact, but the RSI leaves little margin before conditions become stretched, and given that BMY is simultaneously pressing against its 52-week high, a period of consolidation or modest pullback in the near term would not be surprising.

For income-focused investors, the overall technical setup is encouraging as a confirmation of improving fundamental sentiment rather than as a standalone entry signal. The golden cross, the sustained position above both key moving averages, and the recovery from deeply oversold levels earlier in the year all suggest that the worst of the selling pressure has passed. Investors who already hold BMY for the dividend can take comfort in a chart that now supports the thesis. Those looking to initiate a position may want to watch for any consolidation near the $58 to $60 range, which would offer a more favorable risk-adjusted entry while the broader uptrend remains intact.

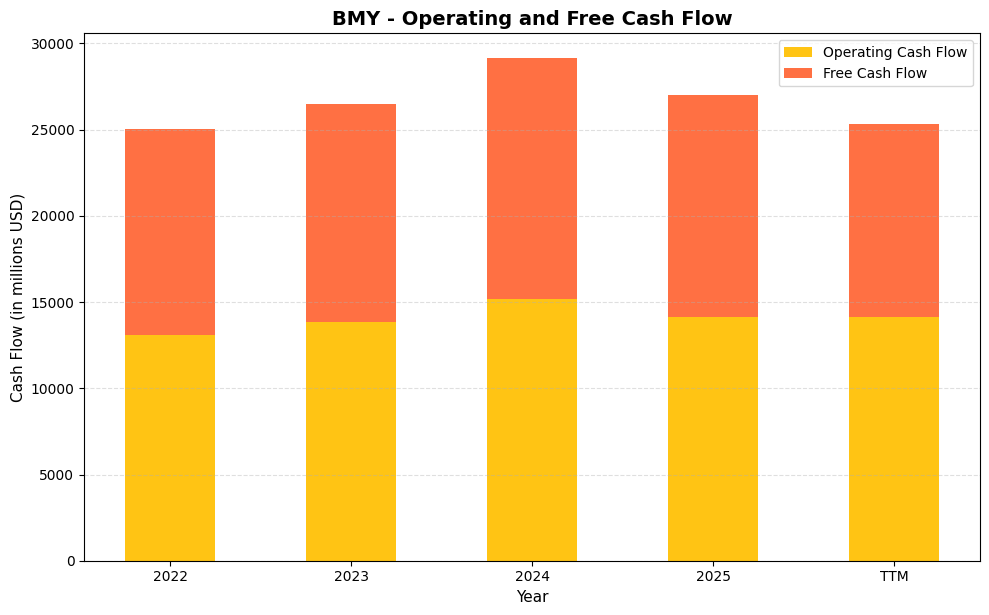

Cash Flow Statement

Bristol Myers Squibb’s cash generation tells a genuinely compelling story for dividend investors. Operating cash flow climbed from $13,066 million in 2022 to a peak of $15,190 million in 2024, a gain of roughly 16% over just two years, before settling back to $14,156 million in 2025. Free cash flow followed the same arc, rising from $11,948 million in 2022 to $13,942 million in 2024 and then moderating to $12,845 million in 2025. Even at the lower 2025 level, the company is converting operating cash flow to free cash flow at a rate above 90%, which reflects a relatively lean capital expenditure requirement and a business that does not need to spend heavily on physical infrastructure to maintain its earnings power. With BMY’s annual dividend obligation running well below its free cash flow output, the payout carries substantial coverage from actual cash generation rather than relying on accounting earnings that can be distorted by amortization charges related to acquisitions.

Zooming out across the full period shown, the trend reinforces confidence in the dividend’s durability even as the top line faces near-term pressure from patent expirations on key products. The company generated at least $11.9 billion in free cash flow in every single year from 2022 through 2025, demonstrating a consistency that matters more to income investors than any single peak year. The TTM free cash flow of $11,147 million reflects some working capital timing and integration costs from the Karuna and RayzeBio acquisitions, but the operating cash flow base of $14,156 million shows the underlying engine remains intact. Capital efficiency has been solid throughout, with free cash flow representing roughly 89% to 92% of operating cash flow in most years, meaning management is not sacrificing cash returns to shareholders in order to fund runaway capital spending. For long-term dividend investors, a company producing north of $11 billion in annual free cash flow while paying a dividend that costs roughly $5 billion per year represents a margin of safety that is difficult to dismiss.

Analyst Ratings

The analyst community has grown notably more constructive on Bristol-Myers Squibb, with 24 analysts now carrying a consensus buy rating on the stock. The mean price target of $61.83 sits just above the current price of $61.30, suggesting that at current levels the stock is trading roughly in line with the average analyst view of fair value. However, the range of targets is wide, spanning from a low of $40.00 to a high of $75.00, which reflects genuine disagreement about how quickly the growth portfolio can offset legacy revenue pressure.

The high target of $75.00 implies approximately 22% upside from current levels and likely reflects optimism around the commercial trajectories of Cobenfy, Camzyos, and Reblozyl, along with the possibility that the pipeline delivers additional late-stage approvals on schedule. The low target of $40.00 represents a more bearish view, presumably incorporating a scenario where generic erosion of Eliquis and Opdivo accelerates faster than new products can compensate. With the stock currently near the consensus mean target, investors are essentially being asked to take a view on which scenario is more likely rather than collecting an obvious valuation discount.

The buy consensus does suggest that the majority of analysts believe BMY’s pipeline and cash flow profile justify ownership at current prices, and the 4.04% yield provides income investors with a meaningful return while waiting for the growth thesis to develop. Any positive pipeline readouts or better-than-expected commercial uptake from newer therapies could serve as catalysts for price target upgrades that pull the mean figure higher.

Earning Report Summary

Solid Top-Line Growth

Bristol-Myers Squibb finished the trailing twelve-month period with revenue of approximately $48.2 billion, representing meaningful top-line expansion compared to the prior year as the growth portfolio continued to scale. Eliquis and Opdivo remain significant contributors, though their trajectories are increasingly well understood by the market. The more encouraging development has been the acceleration of newer products, with Reblozyl in particular demonstrating strong volume growth in hematology indications, and Camzyos building out its patient base in obstructive hypertrophic cardiomyopathy as prescriber familiarity increases.

Cobenfy, the schizophrenia treatment that launched in late 2024, has moved through its early commercial phase and is generating growing attention as a mechanistically differentiated option in a category where innovation has been limited for decades. Its contribution to overall revenue is still modest relative to the larger portfolio, but the launch trajectory matters significantly for the long-term growth story, and management has expressed confidence in its commercial potential as market access improves.

Profitability Improving

Net income of $7.05 billion represents a sharp reversal from the prior year’s reported loss, as the non-recurring charges that weighed heavily on GAAP results in 2024 have largely cycled through. EPS of $3.46 on a reported basis reflects this improvement, and the profit margin of 14.64% shows the business is generating meaningful earnings leverage off its revenue base. Return on equity of 40.44% and return on assets of 10.29% both speak to the productivity of BMY’s asset base, even with the elevated intangible asset load from prior acquisitions.

Looking ahead, the company’s guidance framework centers on continued revenue growth from the newer portfolio, offset in part by ongoing generic pressure on Revlimid and the eventual biosimilar competition that will affect Eliquis and Opdivo. Management has been consistent in its messaging that the growth portfolio is on track to more than replace the revenue at risk from legacy expirations, though the precise timing of that crossover remains the central question for investors evaluating the stock today.

Management Team

Bristol-Myers Squibb’s leadership team has navigated a genuinely difficult period with a steady hand, managing the integration of multiple large acquisitions while preserving the operational discipline needed to sustain the dividend and maintain investment-grade financial flexibility. The strategic direction has remained consistent: invest in a diversified pipeline across oncology, immunology, and cardiovascular disease, build out the commercial infrastructure to support new launches, and use the company’s strong cash generation to steadily reduce the debt accumulated through acquisition activity.

CEO Christopher Boerner, who took the helm in late 2023 following Giovanni Caforio’s tenure, has maintained continuity in both strategy and capital allocation philosophy. The management team has been transparent about the headwinds facing legacy products and has positioned the company’s growth portfolio as the primary vehicle for sustaining long-term shareholder value. What comes through in both the financial results and the public communications is a leadership group that understands the income investor base and treats dividend stability as a core commitment rather than an afterthought. The combination of long-term strategic focus and operational execution capability continues to be one of BMY’s underappreciated strengths.

Valuation and Stock Performance

At $61.30, Bristol-Myers Squibb is trading near the upper end of its 52-week range of $42.52 to $63.33, reflecting a substantial recovery from the lows seen earlier in the past year. The P/E ratio of 17.72 on reported earnings is more moderate than the sub-8 forward multiples that characterized the stock when it was deeply out of favor, suggesting that the market has begun to assign more credit to the improving earnings trajectory as acquisition-related charges fade. That re-rating has been meaningful for shareholders who held through the turbulence.

The price-to-book ratio of 6.76 against a book value per share of $9.07 reflects the intangible-heavy nature of a pharmaceutical balance sheet built through major acquisitions, and it does not tell investors much about intrinsic value on its own. More informative is the free cash flow yield, which at $11.1 billion against a market cap of approximately $124.8 billion implies a free cash flow yield of roughly 8.9%, a level that remains attractive relative to large-cap peers and provides a strong foundation for the 4.04% dividend yield.

The stock’s beta of 0.29 makes BMY one of the more stable large-cap names available to income investors, and that characteristic has value in an environment where market volatility can be unpredictable. With the stock near the consensus analyst mean target of $61.83, the near-term upside from valuation expansion alone is limited, but the combination of a 4% yield, improving earnings, and a pipeline with multiple potential catalysts suggests the total return case remains reasonable for patient investors.

Risks and Considerations

The most pressing risk for Bristol-Myers Squibb remains the patent cliff surrounding its largest legacy revenue contributors. Eliquis, co-commercialized with Pfizer, faces biosimilar competition that will intensify over the coming years, and Opdivo operates in an increasingly crowded checkpoint inhibitor market where pricing pressure is a persistent reality. Revlimid has already seen significant generic erosion. The central question for investors is whether the growth portfolio can scale fast enough to absorb the revenue that will be lost from these products, and while the commercial trajectories are encouraging, that transition carries execution risk.

Debt levels continue to warrant attention, even as the company makes progress in reducing the obligations it took on through the Celgene acquisition and subsequent deals. The balance sheet carries meaningful leverage, and while current free cash flow generation is more than sufficient to manage debt service alongside the dividend, any unexpected deterioration in operating results or a significant pipeline setback could put pressure on the financial flexibility that management currently enjoys.

New product launches like Cobenfy and Camzyos offer genuine growth potential, but commercial execution in specialty therapeutics is rarely linear. Reimbursement decisions, formulary placement, and the pace of physician adoption all affect how quickly a new product reaches its commercial potential, and setbacks in any of these areas could delay the revenue ramp that the bull case assumes. The competitive landscape in oncology and immunology is particularly intense, with well-funded rivals consistently bringing new agents to market.

The broader regulatory and pricing environment in pharmaceuticals also represents an ongoing consideration. Policy developments around drug pricing reform, Medicare negotiation, and international reference pricing can affect revenue assumptions in ways that are difficult to model precisely. BMY’s diversified portfolio provides some insulation, but the company is not immune to sector-wide policy headwinds that could reset expectations across the industry.

Final Thoughts

Bristol-Myers Squibb sits at an interesting inflection point. The worst of the GAAP earnings turbulence appears to be behind it, the growth portfolio is gaining commercial traction, and the share price recovery from the $42 lows suggests the market is beginning to price in a more constructive outcome for the pipeline transition. The dividend has continued to grow, reaching $0.63 per quarter, and the free cash flow coverage remains robust enough to keep that income stream secure through the uncertainties ahead.

The 4.04% yield, while no longer at the exceptional levels seen when the stock was deeply oversold, still represents above-average income for a large-cap healthcare name with BMY’s cash flow profile and strategic positioning. For investors who can look past the near-term noise around patent expirations and are willing to be patient while new therapies scale, the combination of income and potential capital appreciation is a reasonable proposition at current prices.

The risks are real and worth taking seriously, particularly on the debt and legacy revenue fronts. But Bristol-Myers has consistently demonstrated the cash generation capacity and management discipline to navigate complex transitions, and the current pipeline gives the company more tools than it has had in years to sustain growth through the coming patent cliff. For income investors with a multi-year time horizon, BMY remains a core-worthy holding with a dividend that continues to earn its place in a diversified portfolio.