Updated 2/25/26

Boise Cascade isn’t a company that makes a lot of noise. It’s not one of those names you hear tossed around at every cocktail party or trending across financial Twitter. But if you’re someone who values consistent performance and thoughtful dividend policies, this wood products and building materials company might deserve a spot on your radar.

Headquartered in Boise, Idaho, the company manufactures engineered wood products and distributes building materials across North America. It’s a business deeply tied to the housing and construction cycle, so demand can ebb and flow with broader economic trends. But through those waves, Boise Cascade has quietly built a reputation for sound financial management and steady cash generation, two things dividend investors tend to care about most.

Recent Events

Boise Cascade has been navigating a housing market that remains under pressure from elevated mortgage rates and subdued new residential construction activity. The broader lumber and building materials sector has faced headwinds as homebuilding starts have stayed well below the levels seen during the post-pandemic boom, and that reality is showing up in BCC’s top and bottom lines. The company has responded by maintaining operational discipline and keeping its balance sheet conservative, which has helped it hold its footing even as the cycle works through a softer patch.

On the stock front, shares have pulled back meaningfully from their 52-week high of $108.42, recently trading around $83.62, a decline of roughly 23% from that peak. That compression reflects the market’s cautious stance on cyclical building materials names, not a deterioration of BCC’s competitive position. The company continues to operate its two core segments, wood products manufacturing and building materials distribution, with a focus on long-term positioning rather than chasing short-term volume at the expense of margins.

The dividend history tells an interesting story about how management thinks about capital allocation. Regular quarterly payments have been supplemented in prior periods with meaningful special dividends, including a $5.21 special distribution paid in September 2024 and a $5.20 special dividend in November 2023. Those special payouts reflect the company’s tendency to return excess cash when earnings allow, without permanently locking in a higher recurring obligation.

Key Dividend Metrics

💸 Forward Dividend Yield: 0.99%

📈 5-Year Average Dividend Yield: 0.71%

🧮 Payout Ratio: 16.77%

🏦 Dividend Rate (Annualized): $0.87

📆 Most Recent Quarterly Payment: $0.22

⏳ Last Ex-Dividend Date: November 2025

These figures paint the picture of a dividend that’s not oversized, but it’s reliable. With such a low payout ratio, there’s little pressure on management to maintain it even in tougher years, and the recent uptick in the quarterly rate from $0.21 to $0.22 signals continued confidence from the board.

Dividend Overview

Boise Cascade’s dividend isn’t going to turn heads at first glance. The yield sits just under 1%, which might seem underwhelming compared to higher-yielding income plays in other sectors. But when you look closer, what you see is a management team that prioritizes financial strength and avoids overextending itself during cyclical downturns.

Operating cash flow came in at $254 million over the trailing twelve months, a figure that more than covers the current dividend obligation at the existing payout ratio of 16.77%. There’s no strain here, no sense that the dividend is at risk. The company pays what it can comfortably afford, leaving room for capital investment or additional shareholder returns when conditions improve.

Rather than chasing a high yield to attract short-term attention, Boise Cascade focuses on keeping its core operations strong and rewarding shareholders gradually. That strategy might not scream excitement, but for income-focused investors who understand the cyclical nature of building materials, it reflects exactly the kind of conservatism that keeps dividends intact through the full cycle.

Dividend Growth and Safety

Here’s where Boise Cascade really separates itself from more aggressive payers in the cyclical space. That 16.77% payout ratio is a significant cushion. Even if earnings were cut substantially from current levels, the regular quarterly dividend would still be covered with room to spare. That’s the kind of security that lets dividend investors sleep well at night when housing data disappoints.

The most recent quarterly payment increased to $0.22 from the prior $0.21 level, a modest but meaningful step up that reflects management’s comfort with the current earnings and cash flow trajectory. The annualized rate of $0.87 compares favorably to the $0.84 rate from the prior year, confirming that dividend growth, while measured, remains intact. Dividend increases don’t come fast and furious here, but they do come thoughtfully, and the company has historically supplemented the regular payout with special dividends during peak earnings periods.

Compared to the five-year average yield of 0.71%, today’s yield of 0.99% represents a more favorable income entry point. That improvement comes courtesy of the stock’s price decline, not a change in dividend policy, which makes the current setup potentially attractive for investors building a diversified dividend portfolio with exposure to the building materials sector. The low payout ratio and solid operating cash generation provide a durable foundation for continued payments regardless of near-term cyclical pressure.

Chart Analysis

Boise Cascade’s chart tells a story of a stock that has been through a meaningful correction from its peak but is now attempting to stabilize on firmer technical ground. Over the past 52 weeks, BCC has traded across a wide range of $65.88 to $103.26, a spread of more than $37 per share that reflects the cyclical nature of the building products business and the market’s shifting expectations for housing activity. The current price of $83.62 sits roughly 19% below the 52-week high, meaning a substantial portion of the prior advance has been given back, yet the stock has also recovered nearly 27% from its 52-week low, which confirms that buyers have been willing to step in at lower levels.

The moving average picture is constructive for income investors monitoring entry points. BCC is currently trading above both its 50-day moving average of $81.48 and its 200-day moving average of $81.39, a configuration that places the stock in technically positive territory on both a near-term and longer-term basis. Importantly, the 50-day average has crossed above the 200-day average, forming what technicians refer to as a golden cross, a pattern historically associated with strengthening price momentum. The fact that both moving averages are closely clustered near $81.40 also suggests that this zone represents meaningful technical support, and a hold above that level would be an encouraging sign for investors considering a position.

The RSI reading of 36.23 adds an interesting dimension to the setup. At that level, BCC is approaching oversold territory without having fully crossed the traditional threshold of 30, which indicates that selling pressure has been persistent but has not yet reached a point of exhaustion. For dividend investors, this kind of momentum reading can be a useful context clue. It suggests the stock is not chasing momentum to the upside, and patient buyers accumulating near current prices are not competing with a crowded trade. A stabilization and reversal of the RSI back toward the mid-range would typically accompany a more sustained price recovery.

Taken together, the technical picture for BCC is one of cautious optimism. The golden cross, the position above both moving averages, and the proximity to solid support in the low-$80s all offer a reasonable foundation for dividend investors focused on total return. The distance from the 52-week high is a reminder that the stock has work to do to reclaim its prior strength, and the low RSI suggests momentum has not yet fully turned. For income-oriented investors, the current setup may represent a measured accumulation opportunity, particularly if the broader housing backdrop stabilizes and supports the fundamental case alongside the technical one.

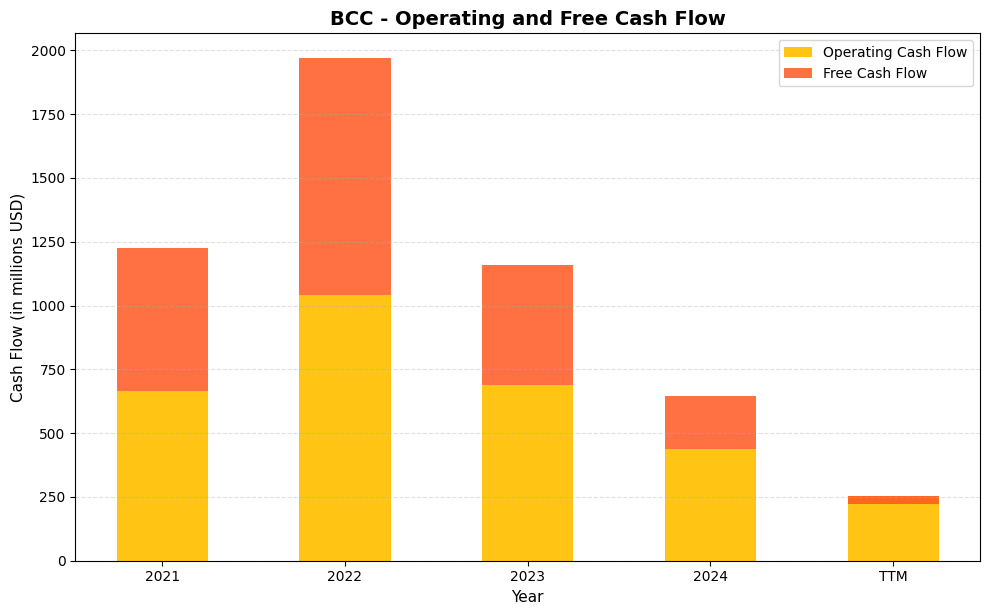

Cash Flow Statement

Boise Cascade’s cash flow profile has shifted meaningfully over the past several years, and the trajectory deserves close attention from income investors. Operating cash flow peaked at $1,041.2 million in 2022 before retreating to $687.5 million in 2023 and $438.3 million in 2024, with the trailing twelve months coming in at just $254.1 million. Free cash flow followed the same arc, compressing from a high of $927.1 million in 2022 down to $208.8 million in 2024 and turning slightly negative at -$31.3 million on a TTM basis. A negative free cash flow reading is not an automatic alarm for a cyclical building products company, but it does raise legitimate questions about near-term dividend coverage, particularly as BCC has historically leaned on robust free cash generation to fund its special dividends alongside the regular quarterly payout.

Stepping back across the full five-year window, the 2021 and 2022 results reflected an exceptionally favorable lumber and wood products pricing environment that is unlikely to repeat at the same magnitude in the near term. Capital expenditures have been climbing as BCC invests in capacity and operational efficiency, which is the primary reason free cash flow has compressed more sharply than operating cash flow alone would suggest. The $560.5 million in free cash flow generated in 2021 and the $927.1 million in 2022 gave management considerable flexibility to return capital aggressively, but that cushion has narrowed considerably entering 2025. For shareholders focused on the regular dividend, the payout remains modest enough relative to normalized earnings that the base distribution does not appear immediately at risk, though the era of outsized special dividends tied to peak-cycle cash generation has clearly given way to a more disciplined, cycle-aware capital return posture.

Analyst Ratings

Boise Cascade currently holds a consensus rating of “Buy” among the six analysts who cover the stock. The average 12-month price target sits at $95.50, which implies upside of roughly 14% from the current trading price of $83.62. The range of targets runs from a low of $81.00 to a high of $105.00, reflecting a reasonable spread of views on how quickly the housing cycle might recover and what that means for BCC’s earnings trajectory.

The consensus buy rating alongside a mean target that sits above the current price suggests analysts broadly view the recent weakness as an opportunity rather than a warning sign. The low end of the target range at $81.00 is modestly below where the stock is trading today, indicating that even the more cautious voices in the analyst community don’t see dramatic downside from current levels. The stock’s position near the lower end of its 52-week range and below the mean price target supports the view that the market may be discounting near-term cyclical headwinds more severely than fundamentals warrant.

With six analysts covering the name and a consensus leaning constructive, there’s a reasonable degree of institutional confidence in BCC’s ability to navigate the current slowdown and emerge with its financial discipline intact. Analysts pointing to the high end of the target range at $105.00 are likely giving more weight to a potential housing recovery tailwind in the back half of 2026.

Earning Report Summary

Revenue Takes a Breather

Boise Cascade’s most recent results reflected what many were expecting given the conditions in residential construction. Revenue came in at $6.4 billion over the trailing twelve months, a level that reflects the ongoing softness in homebuilding activity and the corresponding pullback in demand for engineered wood and building materials distribution. Both segments of the business have felt the impact of a market where mortgage rates have kept buyer activity constrained and builder starts have remained below historical norms.

Still Holding Its Ground

Even with the revenue environment under pressure, the company managed to stay profitable. Net income of approximately $133 million and earnings per share of $5.07 are clearly softer than the elevated figures posted during the peak of the construction cycle, but they confirm that BCC is not a business that loses money when conditions get difficult. The profit margin of just over 2% reflects the distribution-heavy revenue mix, which structurally carries lower margins than the manufacturing segment alone.

Cash Flow Remains the Foundation

Operating cash flow of $254 million over the trailing twelve months remains the most important number for dividend investors to track. Capital expenditures have pushed free cash flow into slightly negative territory, but that spending reflects deliberate investment decisions rather than operational weakness. The company is choosing to invest through the downturn, which positions it to benefit more fully when volume and pricing recover.

Balance Sheet Discipline

Boise Cascade continues to operate with a conservative financial posture. The price-to-book ratio of 1.46 against a book value per share of $57.33 reflects a balance sheet that has retained real value through the cycle. Debt levels remain modest, and the company’s approach to leverage has consistently prioritized flexibility over financial engineering. That conservatism is a feature, not a limitation, for long-term shareholders.

A Steady Hand

Management has been straightforward about the challenges facing the building materials sector, acknowledging the slowdown without abandoning the long-term narrative around U.S. housing undersupply. They’ve pointed to demographic trends and the structural shortage of existing homes as factors that should eventually support a more robust construction environment. In the meantime, BCC is managing inventory carefully and keeping expenses disciplined while continuing to invest in the business.

Management Team

Boise Cascade is led by a management team with deep roots in the building products industry. The leadership group has consistently prioritized balance sheet strength and disciplined capital allocation over aggressive growth strategies, a philosophy that has served the company well through multiple housing cycles. That conservative orientation shows up clearly in the company’s low leverage, substantial cash reserves, and measured approach to dividend increases.

The executive team has demonstrated a clear preference for returning capital to shareholders in ways that don’t overcommit the company’s financial flexibility. The combination of a modest but growing regular dividend with periodic special dividends during peak earning periods reflects a thoughtful approach to capital return that respects the cyclical nature of the business. Management has also shown a willingness to invest in capital expenditures during slower periods, building capacity and capability for the next upturn rather than simply pulling back and waiting it out.

Valuation and Stock Performance

As of February 25, 2026, Boise Cascade shares are trading at $83.62, sitting toward the lower end of their 52-week range of $65.14 to $108.42. The stock is trading well below its prior highs, and that compression has created a valuation setup that looks more interesting than it did when BCC was riding the peak of the construction cycle. The current P/E of 16.49 times trailing earnings is reasonable for a cyclical building materials business, particularly one with the balance sheet quality and dividend track record that BCC has established.

The price-to-book ratio of 1.46 suggests the market is assigning a modest premium to the company’s book value of $57.33 per share, which is not excessive given BCC’s history of generating meaningful returns through the cycle. With a market cap of approximately $3.1 billion and a beta of 1.23, the stock carries moderate sensitivity to broader market movements, which is consistent with its cyclical business profile.

The consensus analyst price target of $95.50 implies roughly 14% upside from current levels, and the high-end target of $105.00 would represent a return closer to 25%. With the stock trading below the mean analyst target and carrying a yield of just under 1%, the current entry point offers a combination of income and potential price recovery that income-growth investors may find worth considering as part of a diversified portfolio.

Risks and Considerations

The most significant risk for Boise Cascade remains the cyclicality of its end markets. The company’s revenue and earnings are closely tied to residential construction activity, and a prolonged period of elevated mortgage rates or weakening consumer confidence could extend the current downturn further than the market currently anticipates. Revenue of $6.4 billion and a profit margin just above 2% leave limited room for error if volumes soften materially from here.

Free cash flow turned negative over the trailing twelve months, reflecting elevated capital expenditures against a backdrop of compressed earnings. While this spending is intentional and forward-looking, it does mean the company is currently relying on its balance sheet and operating cash flow to fund both investment and dividends. Should capital spending remain elevated while revenue continues to soften, the financial flexibility that has defined BCC’s appeal could narrow.

Input cost volatility is another factor worth watching. Timber prices, resin costs, and transportation expenses can all move quickly in response to supply chain disruptions or shifts in commodity markets, and those movements can compress margins faster than revenue adjustments can offset them. BCC has generally managed these dynamics well, but they remain a persistent feature of the operating environment.

Finally, with a beta of 1.23, the stock tends to amplify broader market moves in both directions. In a risk-off environment where investors are rotating away from cyclical names, BCC can sell off more sharply than the overall market. That characteristic is not a reason to avoid the stock, but it’s a reason to size a position thoughtfully and maintain a longer holding horizon.

Final Thoughts

Boise Cascade stands out in the building materials space for its financial conservatism and disciplined approach to shareholder returns. The management team has navigated the current housing slowdown with the same steady hand it has applied through prior cycles, keeping the dividend intact, investing in future capacity, and maintaining a balance sheet that provides genuine flexibility. The recent quarterly dividend increase to $0.22 is a small but meaningful signal that the board remains confident in the company’s underlying position.

At a P/E of 16.49 and a price-to-book of 1.46, the valuation is not stretched, and the stock’s position near the lower half of its 52-week range gives long-term investors a more attractive entry than was available a year ago. The 0.99% yield won’t satisfy investors seeking high current income, but for those who understand the cyclical dynamic and appreciate the combination of a durable regular dividend, the potential for special distributions during upcycles, and a balance sheet built for resilience, BCC offers a thoughtful way to gain exposure to the long-term trajectory of U.S. housing demand.