Updated 2/25/26

Bank OZK isn’t the kind of name that dominates headlines or trends on financial media. But for patient, income-minded investors, that might actually be a strength. Based in Little Rock, Arkansas, OZK has spent decades quietly building a reputation as a disciplined, well-run regional bank. Its specialty lies in real estate lending, especially construction loans, and it has carved out a unique corner of the market through smart underwriting and a conservative approach to growth.

Over the years, OZK has grown from a small community operation into a respected regional institution, all while maintaining the kind of balance sheet strength and earnings consistency that dividend investors love. It’s not flashy, but it’s dependable. And in the current market, that counts for a lot.

Recent Events

Bank OZK has continued its methodical expansion of the Corporate and Institutional Banking group, a strategic initiative management has been building out over the past several quarters. This diversification effort is designed to reduce the bank’s historical dependence on construction and commercial real estate lending, broadening the loan portfolio into new verticals while maintaining the disciplined underwriting standards the bank has long been known for. Progress on this front remains a key watch item heading into 2026.

The stock has recovered meaningfully from its 52-week low of $35.71, trading near $49 as of late February 2026, though it remains below the 52-week high of $53.66. That recovery reflects renewed investor confidence in the bank’s earnings durability and continued dividend growth, even as the broader regional banking sector has faced persistent questions about credit quality and margin pressure. OZK has largely navigated that environment without the kind of headline credit events that have rattled peers.

Short interest remains elevated at roughly 15.2 million shares, a figure that warrants attention for a stock of this size. The elevated short positioning likely reflects ongoing skepticism about commercial real estate concentrations across the regional banking universe rather than any company-specific deterioration. For long-term dividend investors, periods of elevated short interest in fundamentally sound businesses have historically created attractive entry points.

Key Dividend Metrics 🏦

📈 Forward Yield: 3.58%

💵 Annual Dividend: $1.78 per share

📆 Last Dividend Payment: $0.46 per share (January 13, 2026)

📊 Payout Ratio: 27.42%

📉 5-Year Avg Yield: 3.29%

📈 Recent Dividend Growth: Consecutive quarterly increases since at least early 2023

These numbers paint a picture of a stock that delivers solid income without stretching itself too thin. A yield of 3.58% is comfortably above the broader market average, and it’s backed by real earnings and a conservative payout ratio well under 30%. It’s the kind of dividend profile that doesn’t just provide income today, it also offers a compelling case for growing that income over time.

Dividend Overview

Bank OZK’s dividend story is one of quiet consistency. At $1.78 per share annually, the yield is not only above average but built on a strong foundation. Earnings per share currently sit at $6.20, meaning there is ample room for the bank to cover its dividend without any strain whatsoever. The payout ratio of 27.42% reflects just how wide that margin of safety truly is.

What really sets OZK apart is its record of raising the dividend every single quarter for more than a decade. Not every year, every quarter. The dividend has climbed from $0.35 per share in April 2023 to $0.46 per share in January 2026, a steady and uninterrupted progression that speaks to a culture of shareholder commitment. That most recent increase to $0.46 represents the latest step in a pattern that has delivered twelve consecutive quarterly raises over the period tracked here.

With a payout ratio sitting comfortably under 28% and earnings per share well above six dollars, OZK doesn’t need to stretch to maintain or grow its dividend. At a price-to-earnings ratio of 7.91 and a price-to-book ratio of 0.93, the stock offers that yield at what still looks like a meaningful discount to intrinsic value, with book value per share standing at $52.46 compared to the current price of $49.03.

The broader banking sector has seen its share of turbulence, but OZK’s fundamentals provide a wide margin of protection. Even if earnings soften or credit losses edge higher, the buffer between current earnings and the dividend is large enough to absorb a significant amount of deterioration before any distribution would come under pressure.

Dividend Growth and Safety

If you’re looking for a dividend that not only pays but grows, Bank OZK continues to deliver. The quarterly dividend has increased from $0.35 to $0.46 over roughly three years, representing annualized growth of close to 9%, which is more than respectable for a regional bank operating in a rate-sensitive environment. Better yet, that growth has been smooth and sequential, one quarter at a time, rather than lumpy or reactive.

Return on equity sits at 12.09% and return on assets at 1.81%, both healthy levels that indicate management is deploying capital effectively. Profit margin of 46% is strong for a regional bank of this size and adds further support to the view that earnings are sustainable through a range of economic scenarios.

A bank with disciplined lending practices, consistent profitability, and a payout ratio below 28% doesn’t have to rely on financial engineering to fund its dividend. Net income came in at approximately $699 million on revenue of roughly $1.56 billion, and the earnings power of the franchise remains intact. With EPS at $6.20 and the annual dividend at $1.78, OZK is retaining more than $4.40 per share in earnings each year, capital that supports continued book value growth and future dividend increases.

Unlike many higher-yielding stocks that look attractive on paper but come under pressure when credit conditions tighten, OZK offers both a solid current yield and the kind of underlying quality that keeps those payments arriving quarter after quarter. It’s the kind of stock dividend investors can accumulate quietly and let compound over time without losing sleep over the sustainability of the income stream.

Chart Analysis

Bank OZK has staged an impressive recovery over the past year, climbing 35.6% off its 52-week low of $36.16 to trade near $49.03 at the time of this writing. That kind of move from trough to current price reflects a meaningful shift in investor sentiment toward the stock, which faced significant selling pressure during the regional banking anxiety that gripped the sector in late 2024. The 52-week high of $52.16 remains the near-term ceiling to watch, and at roughly 6% below that level, OZK sits in a constructive zone, close enough to prior highs to suggest underlying strength but with enough room to confirm a breakout before declaring the technical picture fully resolved.

The moving average structure is encouraging for income-oriented investors who prefer to buy into established trends rather than speculate on bottoms. OZK’s 50-day moving average of $47.96 has crossed above its 200-day moving average of $47.54, forming what technicians call a golden cross, a configuration that historically signals a shift from a downtrend to a more sustained recovery phase. The current price sits above both averages, meaning the stock is not only trending higher on an intermediate basis but is also outpacing its longer-term baseline. When price, the 50-day, and the 200-day are all stacked in ascending order like this, it tends to reduce the probability of a sharp near-term reversal and gives dividend investors a more stable entry context.

The RSI reading of 43.95 is where the chart introduces a note of caution. At that level, momentum is neither overbought nor in deeply oversold territory, but it does lean toward the softer side of neutral. A reading in the low-to-mid 40s suggests that buying pressure has not yet fully returned with conviction, and that the recent price recovery may still be searching for a catalyst to push participation higher. For a stock that has already moved more than 35% off its lows, some consolidation in the RSI is not unusual, but investors should recognize that the chart is not flashing a screaming buy signal on momentum alone.

Taken together, the technical setup for OZK presents a mixed but reasonably constructive picture for dividend investors. The trend is positive, the moving average configuration is bullish, and the stock is trading above key support levels. The softer RSI reading and proximity to the 52-week high suggest that patience may be rewarded, as a period of consolidation near current levels could reset momentum and create a more durable base for the next leg higher. For investors focused on collecting OZK’s dividend while waiting for price appreciation, the current chart offers a defensible entry zone rather than a stretched or speculative one.

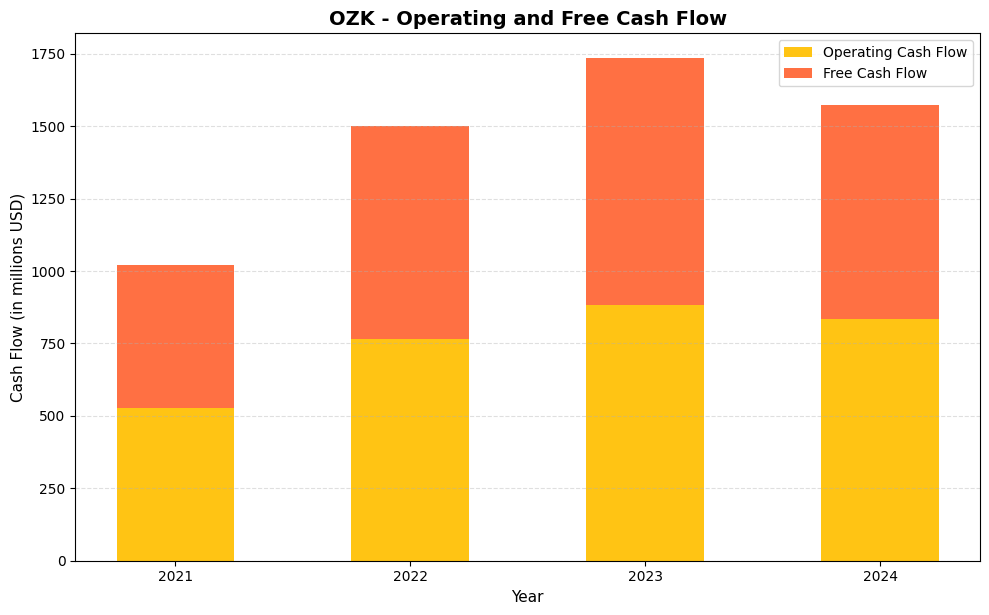

Cash Flow Statement

Bank OZK has demonstrated a compelling trajectory in cash generation over the four-year period, with operating cash flow climbing from $528.2 million in 2021 to a peak of $881.6 million in 2023 before settling at $834.5 million in 2024. Free cash flow has tracked closely alongside, reaching $852.4 million in 2023 and coming in at $738.8 million last year. The modest step down in 2024 is not a structural concern for dividend sustainability, as free cash flow of $738.8 million remains comfortably above the capital required to support OZK’s current dividend obligations. For income investors, a bank generating that level of distributable cash relative to its dividend outlay provides a meaningful cushion against credit cycle volatility or unexpected loan loss provisions.

What stands out across the full four-year span is how efficiently OZK has converted earnings into actual cash. The spread between operating and free cash flow has remained narrow throughout, with capital expenditures consuming only a small fraction of operating cash in each year, never more than roughly $96 million in the highest-spend year of 2024. That capital discipline reflects the asset-light nature of OZK’s deposit and lending model relative to industrial peers, and it means the vast majority of cash generated flows directly to activities that benefit shareholders, including dividends and retained capital supporting book value growth. The 2021 to 2023 ramp from $528 million to $881 million in operating cash flow signals that OZK’s earnings engine scaled meaningfully during that period, and even with the slight 2024 pullback, the bank sits on a cash flow base that supports continued dividend growth without stretching the payout ratio.

Analyst Ratings

The analyst community currently holds a consensus buy rating on Bank OZK, with nine analysts covering the stock. The mean price target sits at $53.78, representing approximately 10% upside from the current price of $49.03. The range of targets is reasonably wide, stretching from a low of $40.00 to a high of $62.00, which reflects the genuine uncertainty around commercial real estate credit quality that continues to divide opinion on regional bank valuations.

The $53.78 consensus target aligns closely with the stock’s 52-week high of $53.66, suggesting analysts broadly see fair value near recent peak levels rather than projecting a significant re-rating higher. The $62.00 bull case implies more optimistic assumptions about credit normalization and net interest margin expansion, while the $40.00 bear target reflects a scenario where commercial real estate stress intensifies and compresses earnings. At the current price, OZK sits closer to the midpoint of the range, leaving room for upside if macro conditions cooperate. The buy consensus is meaningful context given the elevated short interest, as it signals that fundamental analysts largely disagree with the bearish positioning visible in the float.

Earning Report Summary

Bank OZK has continued to post earnings that reinforce its reputation as one of the more consistent and disciplined operators in regional banking. The most recent available financial data shows full-year earnings per share of $6.20 on net income of approximately $699 million, reflecting the bank’s ongoing ability to generate strong returns from its lending franchise even as the rate environment has evolved.

Strong Bottom Line and Operational Efficiency

A profit margin of 46% is a standout figure for a regional bank, and it reflects the combination of OZK’s relatively low cost structure and its focus on higher-yielding construction and commercial real estate loans. Return on equity of 12.09% and return on assets of 1.81% are both above the regional bank median, suggesting that the bank is not just large but genuinely efficient in how it deploys the capital entrusted to it. These metrics have held up well despite the shifting rate backdrop, and they provide a strong foundation for continued earnings growth.

Balance Sheet Discipline and Capital Position

Book value per share has grown to $52.46, a figure that now sits above the current stock price of $49.03. That dynamic, where a bank trades below book value while posting returns on equity above 12%, is the kind of setup that value-oriented dividend investors find compelling. It suggests the market is pricing in some degree of credit risk or earnings normalization that may or may not materialize. Management has long emphasized conservative loan-to-value ratios in the real estate portfolio, and that discipline has historically protected the bank during periods of credit stress. The continued expansion of the Corporate and Institutional Banking group adds a layer of portfolio diversification that should gradually reduce concentration risk over time.

Management Team

At the helm of Bank OZK is George Gleason, who has served as Chairman and CEO since 1979. His leadership has been instrumental in transforming the bank from a small Arkansas institution into a regional powerhouse. Gleason’s long tenure provides continuity and a deep understanding of the bank’s operations and strategic direction.

Supporting Gleason is President Brannon Hamblen, who joined the bank in 2008. Hamblen has held various roles, including Director of Asset Management and Chief Operating Officer of the Real Estate Specialties Group, before becoming President in 2021. His experience in real estate lending aligns with the bank’s core competencies.

Tim Hicks serves as Chief Financial Officer, bringing a wealth of experience in corporate finance and investor relations. Hicks has been with Bank OZK since 2009, holding positions such as Chief Credit and Administrative Officer and Executive Director of Investor Relations. His financial acumen supports the bank’s fiscal discipline and strategic planning.

Cynthia Wolfe, the Chief Operating Officer, has been with the bank since 1997. She has played a pivotal role in expanding the bank’s presence, particularly in the Carolinas, and has held various leadership positions in lending and community banking.

This seasoned leadership team combines stability with a deep understanding of the bank’s operations, positioning Bank OZK for continued success.

Valuation and Stock Performance

Bank OZK’s stock is currently trading at a price-to-earnings ratio of 7.91, which remains well below the broader financial sector average. At $49.03 per share, the stock is also trading at a price-to-book ratio of 0.93, meaning investors are effectively purchasing the bank’s assets at a slight discount to their stated book value of $52.46 per share. That combination of below-market earnings multiple and sub-book pricing makes OZK one of the more attractively valued names in the regional banking space on a fundamental basis.

The analyst consensus price target of $53.78 implies roughly 10% upside from current levels, and the high-end target of $62.00 suggests a more substantial re-rating is possible if credit concerns abate and the bank continues executing on its diversification strategy. At nine analysts covering the stock with a buy consensus, the fundamental case for OZK is reasonably well-supported even as short interest remains elevated.

Over the past year, the stock has traveled a wide range, from a low of $35.71 to a high of $53.66. The recovery from that trough to the current $49 level reflects improving sentiment, and the stock now sits in the upper half of its 52-week range. The combination of a 3.58% yield, a payout ratio under 28%, and a price below book value creates a setup where investors are being paid to wait for a potential valuation re-rating while collecting a growing quarterly dividend.

Risks and Considerations

Bank OZK’s significant exposure to commercial real estate and construction lending remains the primary risk that investors need to weigh carefully. While the bank has a strong track record of disciplined underwriting, including conservative loan-to-value ratios that have historically provided meaningful downside protection, a sustained deterioration in commercial real estate values or a sharp rise in vacancy rates could still pressure loan performance. The concentration in this sector means that broader stress in commercial property markets would affect OZK more directly than banks with more diversified loan books.

The bank’s ongoing diversification into Corporate and Institutional Banking introduces a different kind of risk. Moving into new lending verticals requires developing expertise in underwriting profiles that differ from the construction and real estate specialties where OZK has built its edge. If that expansion moves too quickly or into segments where the bank lacks sufficient credit history, it could weaken the asset quality standards that have defined the franchise for decades.

Regulatory scrutiny is a persistent consideration for any bank with large-scale commercial real estate concentrations. Banking regulators have been attentive to CRE exposure across the regional banking sector, and changes in supervisory guidance or capital requirements tied to that asset class could increase compliance costs or constrain lending activity in ways that pressure both growth and profitability.

Market sentiment toward regional banks can create volatility that is disconnected from underlying fundamentals. Elevated short interest of roughly 15.2 million shares suggests meaningful bearish positioning in the stock, and any broader sector selloff or negative headline around commercial real estate credit could amplify downside moves even if OZK’s own portfolio performs well. Interest rate movements also remain a double-edged influence, with the potential to compress net interest margins if the rate environment shifts in an unfavorable direction.

Final Thoughts

Bank OZK has demonstrated a consistent ability to generate earnings and grow its dividend through multiple economic cycles, supported by a management team with unusual longevity and a business model built on conservative underwriting. The combination of a 3.58% yield, a payout ratio of 27.42%, and earnings per share of $6.20 against an annual dividend of just $1.78 creates one of the more durable income profiles available in regional banking today.

Trading below book value at a P/E of 7.91, with a buy consensus from nine analysts and a mean price target of $53.78, OZK offers a setup where valuation, income, and dividend growth all work in the investor’s favor simultaneously. The quarterly dividend has increased without interruption from $0.35 to $0.46 over the past three years, and there is no earnings-based reason to expect that streak to end anytime soon.

The risks tied to commercial real estate concentration and the evolving diversification strategy are real and deserve ongoing monitoring. But for investors who have a long time horizon and are comfortable with the sector dynamics, Bank OZK’s combination of income, value, and earnings quality makes it a compelling name to own and continue accumulating on weakness.