Updated 2/25/26

Based in Oklahoma, this regional bank has been operating for decades and doing so with an impressive level of financial discipline. It’s not trying to be the flashiest stock in your portfolio. What it offers instead is stability, prudent management, and a dividend that has steadily grown along with the business. For income-focused investors, that kind of quiet reliability is exactly what you want. With deep roots in its communities and a conservative balance sheet, BancFirst continues to be a solid name for those building long-term income.

Recent Events

BancFirst has continued to operate quietly and effectively through the early months of 2026. The bank delivered full-year 2025 earnings per share of $7.11, a meaningful step up from the $6.44 reported in 2024, reflecting continued momentum in net interest income and disciplined expense management. That earnings growth helped push net income to approximately $240.6 million on revenues of roughly $685 million, both representing solid year-over-year improvements for a bank of its size and regional scope.

The bank raised its quarterly dividend to $0.49 per share beginning with the September 2025 payment, up from $0.46, marking the latest in a series of consistent annual increases. That raise brought the trailing annual dividend rate to $1.96 per share, reinforcing the bank’s commitment to steady shareholder returns without overextending its payout capacity.

On the balance sheet front, BancFirst maintained the conservative posture that has long defined its approach. Return on equity held at 14.14%, and profit margins remained healthy at just over 35%. Insider ownership remains high, which continues to signal meaningful alignment between management and long-term shareholders. The stock has pulled back from its 52-week high of $138.77, trading around $114.25 as of late February 2026, creating a more attractive entry point for income investors who may have missed the earlier run.

Key Dividend Metrics

📅 Dividend Date: December 31, 2025

⛔ Ex-Dividend Date: September 30, 2025

💰 Forward Dividend Yield: 1.70%

📈 5-Year Average Yield: 1.97%

📊 Payout Ratio: 26.72%

💸 Trailing Annual Dividend Rate: $1.96

🧾 Last Quarterly Dividend: $0.49

🪙 Last Stock Split: 2-for-1 on August 1, 2017

Dividend Overview

BancFirst isn’t trying to be a high-yield dividend stock. What it offers instead is a modest, reliable, and consistently growing dividend backed by solid fundamentals. At the current share price of $114.25, the dividend yield sits at 1.70%, running a bit below the five-year average of 1.97%. That gap reflects the strong price appreciation the stock has seen over recent years rather than anything negative about the dividend itself.

With a payout ratio of just 26.72%, the dividend has considerable breathing room. That conservative ratio is a deliberate strategy, allowing the bank to reinvest in growth while still returning capital to shareholders. It also provides a meaningful buffer if economic conditions soften. At $7.11 in earnings per share against a $1.96 annual dividend, there is more than five dollars of earnings per share that remains after funding the distribution.

In short, this is a bank that doesn’t need to stretch to pay its dividend, and that’s exactly the kind of setup income investors should seek out.

Dividend Growth and Safety

Dividend growth has been a steady part of BancFirst’s playbook. The recent dividend history tells the story clearly. The quarterly payment moved from $0.40 in early 2023 to $0.43 by mid-2023, then to $0.46 in September 2024, and most recently to $0.49 beginning in September 2025. Each step up has been measured and supported by underlying earnings growth, which is precisely how a conservative regional bank should manage its dividend program.

The safety profile of that dividend is strong. A payout ratio under 27% means the bank would need to see a dramatic and prolonged drop in earnings before the dividend came under any real pressure. Earnings per share of $7.11 provide ample coverage, and the return on equity of 14.14% demonstrates that the bank is generating attractive returns on shareholder capital without taking on excessive risk.

BancFirst’s beta of 0.65 adds another layer of comfort for income-focused investors. The stock tends to move meaningfully less than the broader market, which smooths out the ride and supports confidence in the sustainability of distributions through different economic environments. In a landscape where many dividend stocks carry trade-offs, whether too much debt, elevated payout ratios, or pronounced economic sensitivity, BancFirst stands out for being quietly strong across all of those dimensions.

Chart Analysis

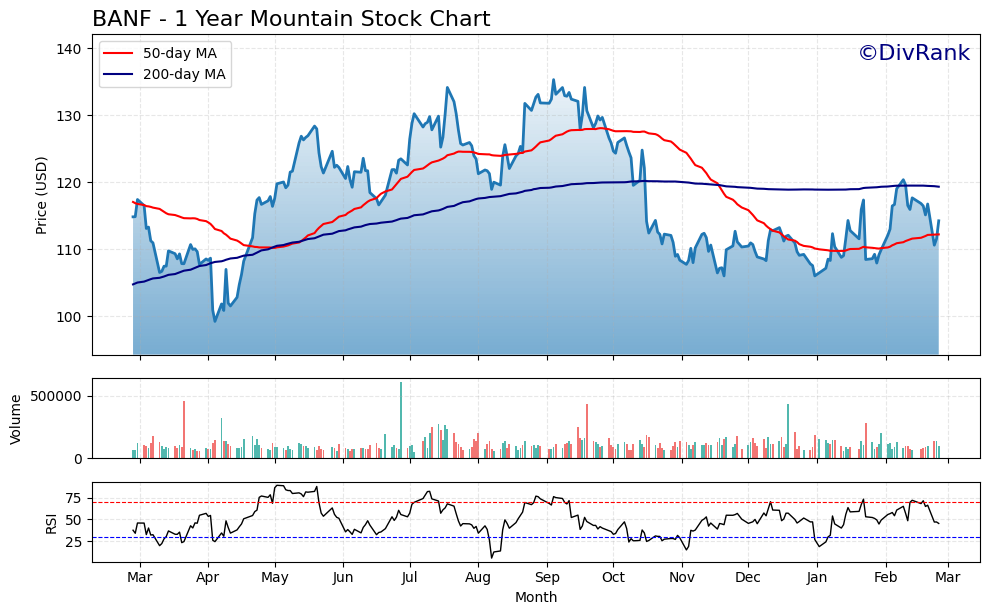

BancFirst Corporation’s price action over the past year tells a story of a stock that ran hard, peaked, and has since spent considerable time giving back those gains. Shares touched a 52-week high of $135.34 before retreating to a low of $99.22, a range that reflects the broader volatility that hit regional bank stocks as rate expectations shifted through the cycle. The current price of $114.25 sits roughly in the middle of that range, sitting 15.58% off the peak but also 15.14% above the trough, which suggests the worst of the selling pressure may have run its course even if a full recovery has not yet materialized.

The moving average picture is where dividend investors need to pay close attention. At $114.25, BANF is trading above its 50-day moving average of $112.22, which is a constructive near-term signal and indicates some stabilization in buying interest over the past several weeks. The more cautious signal comes from the 200-day moving average, currently sitting at $119.35, well above the current price. The 50-day has crossed below the 200-day, forming what technicians call a death cross, a configuration that historically reflects a weakening intermediate trend and tends to keep more momentum-oriented buyers on the sidelines until price can recover above the longer-term average.

The RSI reading of 45.39 reinforces the neutral-to-cautious picture. The indicator is sitting just below the midpoint of its scale, neither in oversold territory that would signal a potential snap-back nor in overbought territory that would raise concerns about near-term exhaustion. For a stock that has already corrected meaningfully from its highs, a mid-range RSI reading like this often reflects a market that is still in the process of deciding direction rather than committing to a new leg in either way.

For dividend investors, the technical setup is best described as a waiting game. BANF is not flashing distress signals from a valuation or income perspective, but the chart is not yet presenting a clean entry setup either. Investors focused on accumulating shares at favorable prices might find the current range reasonable given the proximity to the 50-day moving average, though patience is warranted until the stock can demonstrate it has the momentum to reclaim the $119 area and close the gap with the 200-day average. Those already holding shares for the income stream have little technical reason for alarm, as the price remains well above its annual low and the dividend itself is what drives the long-term thesis here.

Cash Flow Statement

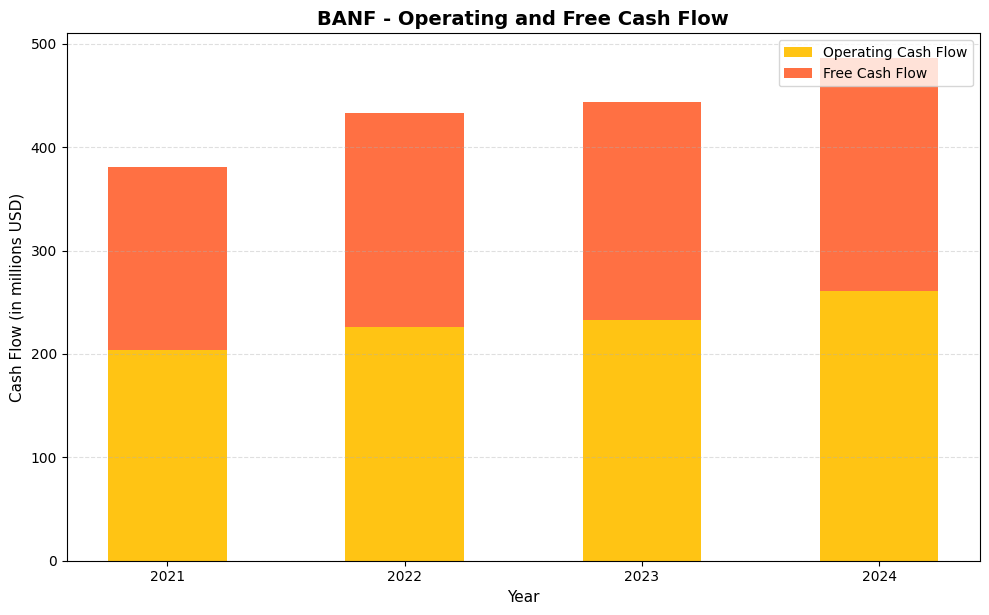

BancFirst’s cash generation has been consistently strong and trending in the right direction. Operating cash flow climbed from $203.9 million in 2021 to $261.2 million in 2024, a gain of roughly 28% over four years, while free cash flow moved in lockstep from $176.7 million to $224.5 million over the same period. The spread between operating and free cash flow has remained relatively narrow throughout, which reflects disciplined capital expenditure management rather than a business that consumes heavy reinvestment just to maintain its earnings base. For dividend investors, this kind of free cash flow trajectory is exactly the foundation you want to see underlying a payout, because it confirms that distributions are being funded by genuine cash generation rather than accounting earnings that may not fully convert to spendable dollars.

The multi-year trend here tells a story of steady compounding rather than lumpy or cyclical cash production. Free cash flow has grown in each year shown, and the year-over-year increases have been meaningful without requiring dramatic revenue swings to achieve them. Capital efficiency looks solid as well, with free cash flow consistently representing well over 85% of operating cash flow across the entire period, meaning very little cash is being consumed by capital spending relative to what the business produces. For shareholders, that combination of rising absolute free cash flow and high conversion efficiency means BancFirst enters each new dividend decision from a position of financial comfort, with room to sustain its current payout, fund modest increases, and still retain capital to support organic balance sheet growth.

Analyst Ratings

Analyst coverage of BancFirst remains limited, with three analysts currently tracking the stock. The consensus price target sits at $123.67, with a low of $123.00 and a high of $125.00. With shares trading at $114.25 as of late February 2026, the average target implies upside of roughly 8% from current levels, suggesting that the analysts following the name see the recent pullback from the 52-week high as an opportunity rather than a warning sign.

No recent formal rating changes or named analyst actions are available in the current data, which reflects the limited sell-side coverage that tends to follow smaller regional banks like BancFirst. The tight clustering of price targets between $123 and $125 indicates a broadly consistent view among the analysts who do cover the stock. That consensus suggests confidence in the bank’s earnings trajectory even as the share price has retreated from its peak near $138.77. For income investors, the combination of an achievable analyst price target and a growing dividend makes the current entry point worth considering on its merits.

Earnings Report Summary

Strong Full-Year 2025 Performance

BancFirst delivered a strong 2025, with full-year earnings per share reaching $7.11, up from $6.44 in 2024. Net income for the year came in at approximately $240.6 million, a record for the bank and a continuation of the multi-year earnings growth trend that has defined this institution. Revenue reached roughly $685 million, reflecting healthy loan demand and net interest income that benefited from the rate environment while noninterest income streams continued to contribute meaningfully to the top line.

Profit margins expanded modestly, with the bank reporting a net profit margin of 35.13%. Return on equity held at 14.14%, which is a respectable figure for a regional bank and reflects the efficiency with which BancFirst deploys shareholder capital. The bank’s conservative underwriting culture continued to keep credit costs in check, supporting bottom-line results even as some peers faced pressure from deteriorating loan books.

Balance Sheet and Capital Position

The balance sheet remained in solid shape through year-end 2025. Book value per share stood at $53.49, and with the stock trading at $114.25, the price-to-book ratio of 2.14 reflects the premium investors are willing to pay for the bank’s earnings consistency and dividend track record. The bank’s market capitalization reached approximately $3.83 billion, placing it comfortably in the regional bank category while retaining the operational focus and community orientation that has long characterized its model.

Short interest of roughly 781,500 shares is modest relative to the float, suggesting that bearish conviction against the stock is limited. That low short interest, combined with meaningful insider ownership, points to a shareholder base that is broadly aligned with the bank’s long-term strategy.

Management’s Outlook

CEO David Harlow has maintained a consistent message heading into 2026, pointing to the strength of the Oklahoma and Texas regional economies as a tailwind for loan demand and deposit growth. Management’s emphasis on quality underwriting over volume growth, and on maintaining a conservative balance sheet through economic cycles, continues to define the bank’s strategic posture. With earnings per share already at $7.11 and the payout ratio well below 30%, there is clear runway for continued dividend growth alongside earnings expansion.

Management Team

BancFirst’s leadership is anchored by a team with deep roots in the company and the broader Oklahoma banking community. David Harlow serves as CEO and President, having stepped into the role in 2017 after leading the Oklahoma City market. His predecessor, David Rainbolt, transitioned to Executive Chairman and remains actively involved in strategic planning and acquisitions.

The executive bench includes Hannah Andrus, who was appointed Chief Financial Officer in early 2024. Andrus brings a background in public accounting and internal finance, following her tenure at Ernst & Young. Her appointment followed the departure of longtime CFO Kevin Lawrence.

The broader management team features a mix of long-serving executives and newer faces, reflecting a balance of institutional knowledge and fresh perspectives. This continuity at the top has helped the bank maintain a consistent strategic direction focused on steady growth and conservative financial management, characteristics that have served shareholders well through varying economic environments.

Valuation and Stock Performance

As of late February 2026, BANF shares are trading around $114.25, which sits in the lower half of the 52-week range of $97.02 to $138.77. The stock has pulled back meaningfully from its peak near $138.77, creating what appears to be a more reasonable entry point for income investors who may have found the stock fully valued at higher prices. The current level represents a discount of roughly 18% from the 52-week high, even as the underlying business continues to perform well.

From a valuation standpoint, BANF trades at a trailing P/E of 16.07 times the $7.11 in earnings per share, which is a modest multiple for a bank generating a 14.14% return on equity with a conservative payout ratio and growing dividend. The price-to-book ratio of 2.14 times the $53.49 book value per share reflects investor confidence in the quality of the loan book and the consistency of earnings. While that book multiple carries a premium to many regional bank peers, it appears justified given the track record of earnings growth and disciplined capital management.

Analyst price targets cluster between $123 and $125, implying upside of roughly 8% to 9% from current levels. Combined with the 1.70% dividend yield, the total return potential from this price is in the high single digits over a twelve-month horizon, which is a reasonable expectation for a low-beta, high-quality regional bank.

Risks and Considerations

The interest rate environment remains a key variable for BancFirst’s earnings trajectory. While the bank benefited from higher rates over recent years through expanded net interest margins, any sustained shift toward lower rates could compress margins and slow earnings growth. The bank’s ability to manage deposit costs and loan repricing will be central to how it navigates whatever rate path emerges through 2026 and beyond.

Geographic concentration presents another consideration. BancFirst’s operations are largely centered in Oklahoma and parts of Texas, meaning the bank’s performance is meaningfully tied to the health of those regional economies. Energy sector volatility, agricultural conditions, and state-level employment trends all have an outsized influence on loan demand, credit quality, and deposit growth relative to banks with more diversified footprints.

Credit quality is always worth monitoring for any regional bank. Nonperforming loans ticked up modestly in prior periods, and while the overall credit picture remains sound, any further deterioration in the loan book could require higher provisioning and weigh on net income. The bank’s conservative underwriting standards have historically kept credit costs low, but a regional economic downturn could test that track record.

Finally, operational risks including cybersecurity threats and an evolving regulatory environment are persistent considerations across the banking industry. BancFirst’s ongoing investments in technology infrastructure and compliance are intended to address these risks, but they remain real factors that income investors should keep in mind when sizing a position.

Final Thoughts

BancFirst continues to exhibit the hallmarks of a well-managed regional bank, with a strong leadership team, solid financial metrics, and a clear commitment to growing shareholder returns over time. The dividend has now reached $1.96 per share on an annualized basis, up from $1.78 just a couple of years ago, and the payout ratio of under 27% leaves plenty of room for further increases as earnings continue to grow. At a P/E of just over 16 times and with the stock sitting roughly 18% below its 52-week high, the current price offers income investors a more attractive setup than the stock has presented for much of the past year. For investors who value steady compounding, conservative management, and a dividend that grows quietly but reliably, BancFirst remains a name worth holding.