Updated 2/25/26

Avnet, Inc. (AVT) operates as a global distributor of electronic components, serving industrial, automotive, and technology markets. With nearly a century of experience and a presence across key global regions, the company has built a resilient business model centered around supply chain efficiency and deep manufacturer relationships. Its long-tenured leadership team emphasizes operational discipline, consistent cash flow generation, and thoughtful capital allocation. Trading near book value and supported by steady free cash flow, the stock currently offers a 2.03% dividend yield with a payout ratio just above 55%. While revenue and margin pressures persist across certain regions and end markets, Avnet maintains solid liquidity, manageable debt, and a track record of steady shareholder returns. Its valuation and stable fundamentals continue to make it a credible consideration for long-term investors focused on income and capital preservation.

Recent Events

Avnet has been navigating a sluggish demand environment across its major end markets as customers continue working through elevated inventory levels accumulated during the post-pandemic component shortage cycle. The broader electronic components distribution industry has faced persistent headwinds from cautious ordering patterns, particularly in industrial and automotive segments, and Avnet has not been immune. Revenue over the trailing twelve months came in at approximately $23.15 billion, reflecting the ongoing normalization of the supply chain cycle that has weighed on top-line growth since fiscal 2024.

On the capital return front, Avnet raised its quarterly dividend to $0.35 per share beginning with the September 2025 payment, up from $0.33, continuing its measured pattern of annual increases. The stock has rallied meaningfully from its 52-week low of $39.22 and now trades near $67.34, approaching the top of its 52-week range of $67.72. That recovery reflects improving investor sentiment around a potential upturn in the component distribution cycle, even as near-term earnings remain compressed relative to peak levels.

With shares trading close to their 52-week high, the stock has clearly attracted renewed interest from investors anticipating a cyclical recovery in semiconductor demand and end-market restocking. Management has remained focused on cost discipline and cash generation through the downturn, positioning the company to benefit as order volumes recover.

Key Dividend Metrics

📈 Forward Dividend Yield: 2.03%

💸 Forward Annual Dividend Rate: $1.38

🧮 Payout Ratio: 55.28%

📊 5-Year Average Dividend Yield: 2.45%

📆 Most Recent Dividend Payment: $0.35 per share (December 2025)

🔁 Dividend Frequency: Quarterly

💪 Free Cash Flow (TTM): $111.7 million

💼 Price/Book Ratio: 1.11

Dividend Overview

Avnet’s dividend profile has shifted somewhat since the prior report, with the yield compressing to 2.03% as the share price has climbed sharply toward its 52-week high. That yield now sits below the company’s five-year average of approximately 2.45%, which signals that new buyers are getting less income per dollar invested than they would have at the lows earlier in the year. Investors who accumulated shares when the stock was trading in the $39 to $45 range are sitting on a much more attractive cost-basis yield.

The annual dividend rate of $1.38 per share reflects the most recent increase to $0.35 per quarter, a step up from the $0.33 rate that was in place for four consecutive payments. With a payout ratio of 55.28% against trailing EPS of $2.46, the dividend is adequately covered, though the coverage is tighter than it appeared in prior years when earnings were running at higher levels. Free cash flow of $111.7 million over the trailing twelve months provides a narrower but still functional cushion relative to total dividend obligations.

The key dynamic to watch here is whether earnings recover as the component cycle turns. If EPS expands back toward prior-cycle levels, the payout ratio would compress again and the dividend would look substantially safer on a forward basis. For now, Avnet is funding its dividend from operating earnings, not from debt or asset sales, which is the right way to do it.

The stock currently trades at 1.11 times book value, a modest premium compared to the deep discount seen in prior periods. That shift reflects the rally in the share price and suggests the market is beginning to price in some recovery in fundamentals, though valuation remains far from stretched by most conventional measures.

Dividend Growth and Safety

Avnet has maintained a consistent pattern of incremental dividend increases over the past several years, and the most recent raise reinforces that discipline. The quarterly payout moved from $0.33 to $0.35 in September 2025, marking the continuation of a cadence that has taken the annual dividend from $1.16 in early 2023 to $1.38 today. That represents roughly 19% cumulative growth over approximately two and a half years, which is a respectable pace for a distributor operating through a cyclical trough.

The growth pattern from the dividend history is clear: $0.29 per quarter in early 2023, stepping up to $0.31 in mid-2023, then $0.33 in late 2024, and now $0.35. Each increase has been modest and deliberate, reflecting management’s preference for raises it can sustain through a full business cycle rather than aggressive hikes that might require a reversal during downturns. That approach has kept the dividend record clean, with no cuts in recent memory.

The payout ratio at 55.28% is higher than the sub-40% levels seen in more profitable periods, and that warrants some attention. The compression in net income, which came in at $207.5 million on roughly $23.2 billion in revenue, reflects just how thin margins are in distribution during a demand slowdown. A profit margin of 0.90% leaves limited room for error, and investors should monitor whether earnings expand as inventory restocking picks up across the customer base. That said, the company has demonstrated through prior cycles that it can generate meaningful cash flow even when margins are under pressure, and there is no current indication that the dividend is at risk of being reduced.

Chart Analysis

Avnet’s price action over the past year tells a compelling recovery story. Shares bottomed out at $40.67 on the 52-week low before embarking on a sustained climb that has carried the stock all the way to its current price of $67.34, which also happens to be the 52-week high. That 65.56% rise from trough to peak reflects a meaningful shift in market sentiment toward the company, and the fact that AVT is printing new highs rather than fading near resistance suggests the buyers are still in control as of this writing.

The moving average structure reinforces that bullish read. AVT is trading comfortably above both its 50-day moving average of $55.88 and its 200-day moving average of $52.24, with the 50-day sitting well above the 200-day in what technicians call a golden cross formation. Golden crosses are generally interpreted as a confirmation that a longer-term uptrend is intact, and the roughly $15 spread between current price and the 200-day average gives the stock meaningful cushion before any test of longer-term trend support would even become relevant for dividend investors monitoring their cost basis.

The RSI reading of 70.11 lands just above the conventional overbought threshold of 70, which warrants some attention. A reading at this level does not signal an imminent breakdown, but it does indicate that the stock has moved a long way in a short period and that near-term consolidation or a modest pullback would be a perfectly normal and healthy outcome. Investors initiating a new position at the current price should be mentally prepared for some short-term choppiness, even if the broader trend remains constructive.

For dividend investors, the overall technical picture is encouraging but argues for patience on entry. The trend is unambiguously positive, the moving average structure is sound, and the stock’s momentum has been strong. The overbought RSI simply means that waiting for a cooling-off period, ideally a pullback toward the $60 to $62 range where the 50-day moving average may eventually converge, could offer a more favorable starting yield and a reduced risk of buying into a short-term peak. Those already holding AVT for its income have little to be concerned about from a chart perspective.

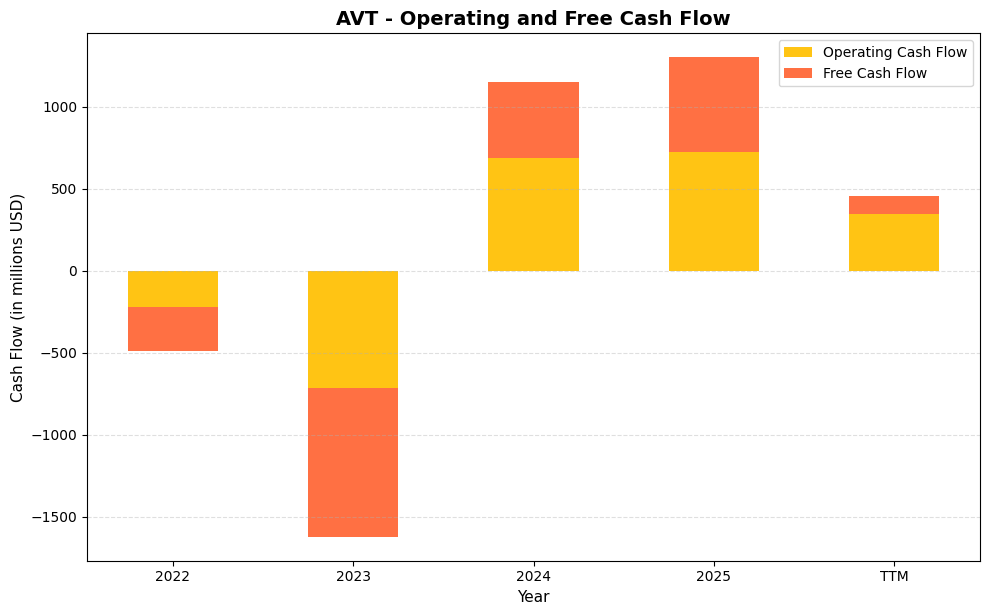

Cash Flow Statement

Avnet’s cash flow profile tells a compelling turnaround story that dividend investors should appreciate. Operating cash flow swung from deeply negative territory, posting ($219.3M) in 2022 and a more alarming ($713.7M) in 2023, to a strongly positive $690.0M in 2024 and $724.5M in 2025. Free cash flow followed the same arc, recovering from ($908.4M) in 2023 to $463.5M in 2024 and $577.0M in 2025. The TTM figures show some moderation, with operating cash flow at $344.0M and free cash flow at $111.7M, which likely reflects working capital timing rather than a structural reversal. Even at the TTM level, free cash flow comfortably covers Avnet’s annual dividend commitment, which runs well under $100M per year, leaving the payout on solid footing from a cash generation standpoint.

The broader multi-year trend here is one of capital discipline reasserting itself after a period of significant inventory buildup that pressured cash flows in 2022 and 2023. Distribution businesses like Avnet routinely see cash flow volatility tied to working capital cycles, and the sharp negative readings in those two years reflected aggressive stocking ahead of supply chain uncertainty rather than deteriorating business fundamentals. The unwinding of that inventory position drove the dramatic recovery in 2024 and 2025, demonstrating that management was ultimately effective at converting assets back into cash. For shareholders, the key takeaway is that the underlying cash generation capacity of the business is real and substantial, and the dividend, which has been maintained and modestly grown through this entire cycle, appears well supported as free cash flow normalizes toward the mid-cycle range.

Analyst Ratings

Analyst sentiment on Avnet remains cautious, and the current price near $67.34 is trading above the consensus mean price target of $59.25, which creates an interesting dynamic for prospective investors. With four analysts covering the stock, the range of targets spans from a low of $48.00 to a high of $69.00, suggesting meaningful disagreement about the near-term outlook. The mean target implies roughly 12% downside from current levels, while the high target of $69.00 sits just above where the stock is trading today, leaving very little room for upside in the most optimistic scenario.

The fact that AVT is trading above the analyst consensus mean is worth considering carefully. It suggests the market has already priced in a fair amount of recovery optimism, running ahead of where the analyst community currently sees fair value. With the stock approaching its 52-week high of $67.72, the technical and fundamental pictures are converging at a point where the risk-reward for new buyers is less favorable than it was earlier in the year when shares were trading in the low-to-mid $40s. The low target of $48.00 reflects ongoing concern about compressed margins, soft industrial demand, and the limited earnings power the company has shown at current revenue run rates. For income investors, the dividend yield of 2.03% at this price level provides less cushion than it did when the stock was significantly cheaper.

Earning Report Summary

Slower Top Line and Compressed Margins

Avnet’s most recent reported results reflect the ongoing challenges facing electronic component distributors as the industry works through a prolonged inventory correction cycle. Revenue on a trailing twelve-month basis came in at approximately $23.15 billion, with net income of $207.5 million producing diluted EPS of $2.46. Those numbers represent significant compression from the earnings peaks of prior years, when the component shortage environment inflated margins and drove exceptional profitability. The profit margin of 0.90% underscores just how narrow the economics of distribution become when demand is soft and customers are drawing down existing inventory rather than placing new orders.

Operating cash flow of $344 million reflects a more normalized working capital environment following the aggressive inventory liquidation that boosted cash generation in the prior fiscal year. The return on equity of 4.24% and return on assets of 3.12% are both below levels the company has achieved historically during stronger parts of the cycle, indicating that asset utilization and profitability have room to improve as volumes recover. Management has responded with continued cost discipline and a focus on maintaining the balance sheet in a position that allows the company to act opportunistically when demand conditions improve.

Regional Trends and What’s Holding Up

Avnet’s business spans three major geographic regions, and the demand environment has been uneven across them. Asia has historically shown more volatility but also more upside during recovery phases, as manufacturing activity in the region tends to respond quickly to changes in global electronics demand. The Americas and EMEA regions have continued to face headwinds from cautious industrial and automotive end customers who remain reluctant to commit to new inventory builds until they have greater visibility on end demand. The uneven regional picture is a consistent theme in the distribution business, and Avnet’s diversified footprint provides some natural balance even when individual regions are underperforming.

Within the business segments, the Electronic Components division remains the dominant earnings contributor, while the Farnell segment, which focuses on smaller-scale and design-stage distribution, continues to operate at thinner margins. Pricing pressure across both segments reflects the competitive nature of distribution and the tendency for component pricing to deflate during periods of excess supply. Management has focused on value-added services and customer relationships as differentiators, though in a commoditized business those advantages can be difficult to translate into sustained margin improvement.

What They’re Expecting Next

Management has been measured in its forward guidance, reflecting genuine uncertainty about the timing of a demand recovery across the company’s key end markets. The trajectory of the dividend, with the most recent increase to $0.35 per quarter, signals that management has confidence in the sustainability of cash flows at current levels even if earnings growth remains modest. Investors are watching for signs of restocking activity from industrial and automotive customers, which would represent the most direct catalyst for a meaningful improvement in revenue and margins. Until that restocking cycle begins in earnest, Avnet is likely to continue generating modest but positive free cash flow while maintaining its dividend and managing costs carefully.

Management Team

Avnet is led by a team with deep roots in the business and a strong grasp of the industry’s long-term rhythms. Phil Gallagher, the CEO, has spent decades at the company, rising through various operational roles before taking the helm. His leadership style reflects that background, focused on execution, supply chain optimization, and incremental progress rather than sweeping changes. That internal continuity has kept Avnet grounded even as the tech landscape around it continues to evolve.

The broader leadership bench mirrors this approach. Key executives across finance, operations, and global distribution bring years of experience, many having worked their way up inside the company. They have shown discipline with capital allocation, maintaining a balanced approach between reinvestment in the business, returning capital to shareholders, and managing the balance sheet. The decision to continue raising the dividend through a cyclical earnings trough is consistent with management’s long-standing philosophy of steady, sustainable shareholder returns. While this management team may not generate headlines, they have demonstrated a steady hand and a clear focus on durable performance across full business cycles.

Valuation and Stock Performance

Avnet’s stock has staged a dramatic recovery from its 52-week low of $39.22, now trading near $67.34 and approaching the top of its 52-week range at $67.72. That rally represents roughly 72% appreciation from the lows, a move that has materially changed the valuation picture compared to the prior report. The price-to-book ratio now stands at 1.11, a meaningful shift from the deep discount to book that made the stock look compelling at lower prices. Book value per share is $60.70, meaning the stock carries only a modest premium to net asset value, which is still reasonable for a business with stable cash generation.

The trailing price-to-earnings ratio of 27.37 reflects the compression in earnings rather than an expansion in the underlying business, since EPS of $2.46 is well below what the company has earned in stronger parts of the cycle. Investors paying today’s price are effectively betting on an earnings recovery that would bring that P/E ratio back down to more typical levels. The price-to-sales ratio remains compressed given the revenue scale, which is characteristic of low-margin distribution businesses. Enterprise value metrics similarly reflect the thin-margin nature of the industry.

From a total return perspective, the stock has been a strong performer over the past twelve months for investors who bought near the lows. Looking forward from current levels, the calculus is different. With the stock trading above the analyst mean price target of $59.25 and just below the high target of $69.00, the margin of safety that existed earlier in the year has narrowed considerably. The 2.03% dividend yield, while reliable, provides less of a buffer against downside at this price level. The stock remains a legitimate holding for investors already positioned, but the case for new buyers is more dependent on confidence in an earnings recovery than it was when the valuation offered a more obvious margin of safety.

Risks and Considerations

The cyclical nature of Avnet’s end markets remains the most significant near-term risk. Industrial, automotive, and communications customers are all sensitive to capital spending trends and macroeconomic conditions, and the prolonged inventory correction cycle has already demonstrated how quickly revenue and earnings can compress when those customers pull back on orders. If the anticipated restocking cycle is delayed further, the earnings recovery that the current stock price appears to anticipate may take longer to materialize than investors expect.

Geographic concentration and foreign currency exposure add complexity to the earnings picture. Avnet operates across the Americas, EMEA, and Asia, and currency movements can meaningfully affect reported results even when underlying business trends are stable. The European business in particular has faced persistent demand weakness, and a prolonged slowdown in industrial activity across that region could continue to weigh on consolidated results for the foreseeable future.

The semiconductor and component distribution ecosystem is subject to broad industry cycles that Avnet cannot control. When chip supply exceeds demand, pricing deflates, customers destabilize their ordering patterns, and distributors like Avnet get caught between manufacturers and customers in a margin squeeze. The company has navigated these cycles before, but the timing and magnitude of each cycle is difficult to predict, and the current cycle has proven more persistent than many market observers initially expected.

The payout ratio of 55.28% is elevated relative to where it has historically been, and with free cash flow of only $111.7 million, the financial flexibility to raise the dividend aggressively or conduct large share repurchases is more limited than it was during the peak cash flow years. While there is no immediate threat to the dividend, a further deterioration in earnings or a significant working capital build could pressure coverage ratios and limit the company’s options for capital allocation.

Finally, the competitive dynamics of distribution have not changed. Avnet operates in a fragmented, low-margin industry where scale, customer relationships, and digital capabilities all matter. Price competition is persistent, and maintaining market share requires ongoing investment in systems, logistics, and service quality. The business model is inherently exposed to disintermediation risk over the long term as manufacturers explore more direct relationships with large customers, though Avnet’s value-added services and global footprint provide meaningful protection against that scenario.

Final Thoughts

Avnet is a company that earns its place in an income-oriented portfolio through operational consistency and management discipline rather than exciting growth. The leadership team has navigated a difficult two-year stretch in the component distribution industry without sacrificing the dividend or taking on dangerous levels of financial risk. The continued, measured increases to the quarterly payout, now at $0.35, reflect a management team that is playing the long game rather than optimizing for short-term optics.

The picture has shifted meaningfully from the prior report, however. The stock is no longer trading at a discount to book value, the yield has compressed to 2.03%, and the share price has run above the analyst consensus price target. Investors who were positioned at lower prices have been rewarded, and the margin of safety that made the stock compelling at $39 to $45 is no longer as evident near $67. The investment case now rests more heavily on the expectation of an earnings recovery, which would normalize the P/E ratio and potentially support further dividend growth.

For patient, long-term investors who already own the stock, the dividend record and balance sheet stability provide reasons to hold. For those considering a new position at current levels, the calculus requires greater confidence in the timing and strength of the cyclical recovery. Avnet remains a fundamentally sound business with a track record of treating shareholders fairly, but at today’s price, patience and selectivity are warranted.