Updated 2/25/26

Avient Corporation (AVNT) is a specialty materials company focused on high-performance polymers and sustainable solutions, serving industries like healthcare, packaging, and automotive. With over $3.2 billion in annual revenue and a forward dividend yield of 2.57%, it combines steady cash flow with a shareholder-friendly capital approach. Led by CEO Dr. Ashish Khandpur, formerly of 3M, the leadership team has emphasized innovation, operational efficiency, and disciplined financial management. The stock has staged a meaningful recovery from its 52-week low of $27.48, now trading near $41.66, with a consensus analyst price target of $48.25.

Recent Events

Avient has navigated a notable turnaround over the past several months, with the stock climbing sharply off its 52-week low of $27.48 to its current level near $41.66, well within striking distance of the 52-week high of $44.85. That kind of price recovery reflects improving investor confidence in the company’s ability to execute on its specialty materials strategy, even as the broader chemicals sector has faced an uneven demand environment. The company’s focus on higher-margin engineered materials and sustainable solutions continues to differentiate it from more commoditized chemical producers.

Management has continued to invest in the business while maintaining its commitment to the dividend, which saw a modest increase at the end of 2025 when the quarterly payment moved to $0.275 per share. That incremental raise, while small, reinforces the tone of disciplined, consistent capital return that has defined Avient’s approach under Dr. Khandpur’s leadership. The company’s specialty positioning across healthcare, packaging, and mobility end markets has helped sustain relatively stable demand, even as some industrial segments have softened.

Operating cash flow came in at $301.6 million over the trailing twelve months, a meaningful improvement from prior periods, and free cash flow reached $335 million, a figure that comfortably covers the annual dividend cost and leaves room for reinvestment. The stock’s beta of 1.44 reflects an elevated sensitivity to broader market moves, which partly explains the wide swing in the 52-week range, but the underlying business has been considerably more stable than the share price action might suggest.

Key Dividend Metrics

💰 Forward Dividend Yield: 2.57%

📈 5-Year Average Yield: 2.33%

📆 Last Dividend Payment: $0.28 per share

📉 Payout Ratio: 121.62% (GAAP); well-covered on a free cash flow basis

💸 Annual Dividend Rate: $1.09

📊 Free Cash Flow Coverage: Strong at $335.0M vs. ~$100M annual dividend cost

🔍 Dividend Growth Trend: Steady and conservative, with a December 2025 increase to $0.275/quarter

These are the types of numbers that matter when you’re building a portfolio designed to generate real, reliable income.

Dividend Overview

Avient’s dividend continues to do what income investors appreciate most: show up consistently and grow modestly over time. The current forward yield of 2.57% sits slightly above the stock’s five-year average yield of roughly 2.33%, a reflection of both deliberate payout increases and some residual share price discount relative to where the stock has historically traded on a valuation basis.

At $1.09 per share annually, the dividend has grown steadily from the $0.248 quarterly rate in early 2023, moving through $0.258, then $0.27, and most recently to $0.275 in December 2025. That progression reflects management’s preference for measured, sustainable increases rather than aggressive hikes that could create stress if conditions deteriorate. The latest quarterly payment of $0.28 per share continues that pattern.

The GAAP payout ratio of 121.62% looks elevated at first glance, but it tells an incomplete story. GAAP net income of $81.9 million reflects charges and accounting items that don’t consume cash, and the more relevant measure for dividend sustainability is free cash flow coverage. With $335 million in free cash flow against a dividend cost of roughly $100 million annually, the actual cash coverage ratio is comfortably above three times, a genuinely healthy position for an income-oriented holding.

Avient’s liquidity profile further supports dividend confidence. The company continues to generate operating cash flow well in excess of its capital needs and dividend obligations, and its balance sheet management has remained disciplined even as the company carries a meaningful debt load from past acquisitions.

Dividend Growth and Safety

Dividend safety at Avient comes down to the gap between what the business earns in cash and what it pays out, and that gap remains wide. Free cash flow of $335 million is substantially above the annual dividend cost, giving management significant flexibility to maintain and grow the payout even if earnings encounter a temporary setback. The GAAP payout ratio of 121.62% is elevated because reported EPS of $0.89 is suppressed by non-cash charges and amortization from prior acquisitions, but the free cash flow picture is far more reassuring.

Looking at the dividend history, the growth has been steady if unspectacular. The quarterly rate moved from $0.248 in early 2023 to $0.275 by December 2025, representing cumulative growth of about 10.9% over roughly three years. That’s not the kind of double-digit annual growth that makes headlines, but it reflects a management team that prioritizes sustainability over optics. The most recent increase to $0.275, followed by the last recorded payment of $0.28, suggests the cadence of small, consistent raises remains intact.

Return on equity of 3.55% and return on assets of 3.77% are modest, reflecting the capital-intensive nature of specialty chemicals and the ongoing amortization burden from acquisitions. However, the operating cash flow of $301.6 million and free cash flow of $335 million tell a more encouraging story about the underlying cash-generating power of the business. For dividend investors, the cash flow metrics are the ones that actually fund the quarterly check, and those metrics remain strong.

Institutional ownership remains substantial, reflecting continued confidence from professional investors who are looking past near-term earnings noise toward the company’s longer-term positioning in high-performance and sustainable materials. That institutional support adds a measure of stability to the shareholder base and signals that the smart money continues to see long-term value in the business model.

Chart Analysis

Avient’s chart tells a compelling recovery story over the past twelve months. The stock carved out a 52-week low of $27.24 and has since rallied more than 52% to its current price of $41.66, closing in on the 52-week high of $43.28 with just 3.74% of ground left to cover. That kind of sustained upward move, built over multiple months rather than a single sharp spike, suggests genuine buying conviction rather than a momentum-chasing flare. For income investors, a stock that recovers strongly from a meaningful low while holding its dividend intact tends to signal improving business fundamentals beneath the surface.

The moving average picture reinforces that constructive view. Avient’s 50-day moving average currently sits at $35.97 and its 200-day moving average at $33.91, with the share price trading above both lines. Equally important, the 50-day has crossed above the 200-day, forming what technicians call a golden cross, a configuration that historically reflects a shift from a downtrending to an uptrending regime. The widening gap between those two averages and the current price of $41.66 indicates that the trend has not only turned positive but has built meaningful momentum behind it.

Momentum as measured by the Relative Strength Index comes in at 65.25, a reading that warrants some attention. The RSI is elevated but has not yet crossed into the conventionally overbought zone above 70, which means the stock is showing strength without flashing an immediate red flag for new buyers. That said, a reading in the mid-60s does suggest Avient has already absorbed a large portion of near-term buying interest, and investors initiating a position here should be prepared for the possibility of a consolidation or modest pullback before any further advance.

Taken together, the technical setup is broadly favorable for a dividend investor considering Avient at current levels. The trend is positive, the moving averages are aligned in a bullish configuration, and the proximity to the 52-week high indicates the stock is operating from a position of strength rather than distress. The primary caution is valuation relative to recent price gains. Investors who missed the move off the lows may want to scale into a position or wait for a pullback toward the $38 to $40 range, where the 50-day moving average would provide a more natural support level and a better starting yield on cost.

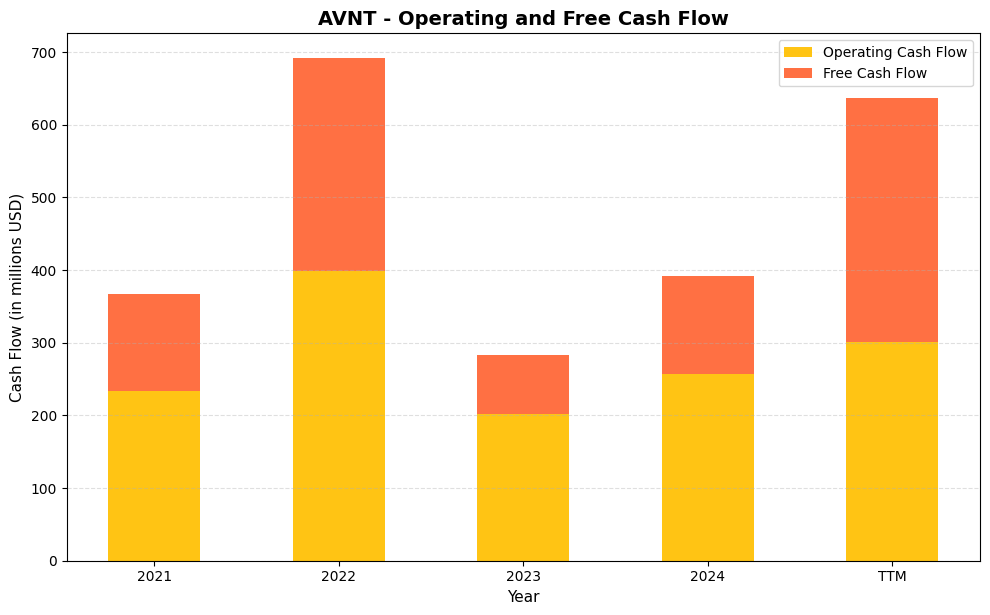

Cash Flow Statement

Avient’s cash generation has been uneven over the four-year period, but the direction of travel into 2024 and the TTM period is encouraging for dividend investors. Operating cash flow dipped sharply to $201.6M in 2023 from $398.4M in 2022, a decline that reflected margin pressure and working capital headwinds following the Dyneema acquisition integration. The recovery to $256.8M in 2024 and $301.6M on a TTM basis signals that the business is regaining its cash-conversion rhythm. Free cash flow tells a similarly reassuring story, climbing from $82.2M in 2023 back to $134.9M in 2024 and then jumping to $335.0M on a TTM basis, a level that comfortably covers the current dividend obligation and leaves meaningful room for incremental capital return or debt reduction.

The TTM free cash flow figure of $335.0M is notably higher than operating cash flow of $301.6M, which suggests favorable working capital timing or reduced capital expenditure intensity in the most recent trailing period, and investors should watch whether that spread normalizes in coming quarters. Stepping back across the full dataset, the 2022 peak of $292.9M in free cash flow represented a high-water mark that the company is now approaching again from a different angle, one built on a larger, more diversified asset base after the Dyneema deal. Capital spending has remained disciplined, with the gap between operating and free cash flow averaging roughly $100M in the non-TTM years, which is consistent with a specialty materials company maintaining its manufacturing infrastructure without overextending on growth capex. For dividend growth investors, the trend from 2023’s trough back toward prior peak levels reinforces that Avient’s payout, which has been steadily increased over recent years, rests on a foundation that is strengthening rather than eroding.

Analyst Ratings

The analyst community holds a constructive view on Avient, with a consensus rating of Strong Buy across eight covering analysts. That level of conviction is notable for a mid-cap specialty chemicals company that has faced some near-term earnings pressure, and it suggests analysts are looking past current GAAP noise toward the company’s free cash flow generation and longer-term positioning in high-value materials.

Price targets span a wide range, from a low of $36.00 to a high of $56.00, with the mean consensus sitting at $48.25. At the current price of $41.66, the mean target represents upside of roughly 16%, while the high end of the range implies more than 34% potential appreciation. The low-end target of $36.00, which sits below the current market price, likely reflects more conservative assumptions around margin recovery and macro conditions rather than a fundamentally bearish thesis on the business.

The breadth of the target range, nearly $20 from low to high, reflects genuine uncertainty about the pace of earnings normalization and how quickly the company can grow its adjusted EPS from current depressed GAAP levels. Still, the fact that the consensus sits firmly in Strong Buy territory while the stock trades at a meaningful discount to the mean target suggests the analyst community views the current entry point as attractive for investors with a patient, multi-year time horizon. For income-focused investors, the combination of a Strong Buy consensus and a dividend yield sitting modestly above its historical average adds to the appeal of the current setup.

Earning Report Summary

Avient Corporation has continued to demonstrate operational resilience through a period of uneven industrial demand, with trailing twelve-month revenue reaching $3.26 billion. That topline figure reflects the company’s ability to sustain meaningful scale across its specialty materials platform even as some end markets, particularly in industrial and automotive, have faced softer conditions. The steady revenue base provides a reliable foundation for cash flow generation and supports the ongoing dividend commitment.

On the bottom line, GAAP net income came in at $81.9 million, producing earnings per share of $0.89. That figure is weighed down by acquisition-related amortization and non-cash charges that are a consistent feature of Avient’s reported results, and the gap between GAAP EPS and the company’s underlying cash generation is substantial. Operating cash flow of $301.6 million and free cash flow of $335 million are far more indicative of the business’s true earning power than the headline EPS number.

Margin and Profitability Trends

The profit margin of 2.51% on a GAAP basis reflects the amortization burden more than it reflects operational weakness. The company’s operating cash flow margin, which divides $301.6 million by $3.26 billion in revenue, comes in near 9.2%, a more competitive figure that speaks to genuine operational leverage in the specialty materials business. Return on assets of 3.77% and return on equity of 3.55% are modest but stabilizing, and both metrics should improve as the company continues to optimize its portfolio toward higher-margin engineered materials and reduces acquisition-related drag over time.

Segment Positioning

Avient’s two primary segments, Color, Additives, and Inks and Specialty Engineered Materials, continue to serve as complementary revenue streams across healthcare, packaging, mobility, and industrial end markets. The healthcare and packaging verticals have been the most resilient, providing a degree of defensive balance that helps offset softness in more cyclical industrial demand. Management’s ongoing emphasis on sustainable formulations and performance materials is designed to capture secular growth in end markets that are increasingly demanding specialized, higher-value inputs.

Outlook

With analyst consensus firmly in Strong Buy territory and a mean price target of $48.25, the investment community appears to expect a meaningful recovery in adjusted earnings as amortization charges moderate and operating leverage improves. The combination of strong free cash flow, a well-covered dividend, and continued strategic investment in high-performance materials positions Avient as a business that is building toward a more compelling earnings profile, even if the GAAP results have not yet fully reflected that progress.

Management Team

Avient Corporation is led by Dr. Ashish K. Khandpur, who stepped into the role of President and CEO in December 2023. With nearly 30 years of experience at 3M, he brings a deep understanding of materials science, technology development, and global business strategy. His arrival signaled a continued focus on innovation, operational excellence, and long-term growth, and his tenure so far has been characterized by steady execution and a disciplined approach to capital allocation that has resonated with the company’s dividend-focused investor base.

Alongside Dr. Khandpur, the leadership team includes Jamie Beggs, who serves as Senior Vice President and Chief Financial Officer. Her financial expertise and background in corporate finance and capital markets have been instrumental in maintaining the company’s strong cash flow discipline and balance sheet management. The team also includes Philip G. Clark, Ph.D., as Chief Technology Officer, who is guiding the company’s research and development initiatives in sustainable and high-performance materials. The broader executive bench blends experience across finance, technology, and operations, and is supported by a board of directors chaired by Richard H. Fearon, ensuring strategic oversight and strong governance.

Valuation and Stock Performance

Avient’s stock has staged a meaningful recovery from its 52-week low of $27.48, with shares now trading near $41.66 and approaching the 52-week high of $44.85. That recovery represents a gain of over 50% from the low, a move that reflects improving investor sentiment toward the specialty chemicals sector and growing confidence in Avient’s free cash flow generation. The current price sits at a roughly 7% discount to the mean analyst price target of $48.25, suggesting some upside remains even after the strong run from the lows.

The P/E ratio of 46.81 looks elevated on a GAAP basis, but as discussed in the earnings section, GAAP EPS of $0.89 significantly understates the company’s cash earning power due to acquisition-related amortization. The price-to-book ratio of 1.61, against a book value per share of $25.92, reflects a modest premium to tangible assets that is consistent with a specialty materials business carrying significant intangible value in its customer relationships, formulations, and technical expertise. The market cap of approximately $3.82 billion places Avient squarely in mid-cap territory, where it benefits from institutional coverage without the liquidity constraints of smaller companies. With a beta of 1.44, the stock tends to amplify broader market moves, which explains the wide 52-week range but also creates opportunities for patient investors to accumulate at more attractive yields during pullbacks.

Risks and Considerations

The GAAP payout ratio of 121.62% will naturally draw attention from investors screening for dividend safety, and while the free cash flow coverage is genuinely strong, the gap between reported earnings and cash generation does reflect real non-cash costs that will persist as long as Avient carries a significant intangible asset base from past acquisitions. If adjusted earnings do not recover as analysts expect, the optics of a triple-digit payout ratio could weigh on sentiment even if the dividend itself is never at risk from a cash perspective.

Avient carries a meaningful debt load, a legacy of its acquisitive growth strategy, and while the company has managed that leverage carefully, a rising interest rate environment or a deterioration in operating cash flow could increase the cost of refinancing and reduce financial flexibility. The balance between servicing debt, investing in the business, and growing the dividend requires sustained cash generation, and any macro shock that pressures volumes or margins could force difficult tradeoffs.

The specialty chemicals industry is sensitive to raw material price movements, and input cost volatility remains a genuine risk. If petrochemical feedstocks or specialty additives spike in price, Avient’s ability to pass through cost increases to customers depends on contract structures and competitive dynamics that can vary significantly by end market. Packaging and healthcare tend to offer better pricing power than industrial segments, but the company is not fully insulated from margin pressure in a rapid cost-inflation scenario.

International operations introduce currency and geopolitical exposure that can affect both reported revenue and earnings. With a significant portion of business conducted outside the United States, shifts in the euro, renminbi, or other currencies can create meaningful translation headwinds. Trade policy changes, particularly around tariffs on specialty chemicals or the inputs Avient uses, could also affect cost structures and competitive positioning in ways that are difficult to predict or fully hedge.

Final Thoughts

Avient Corporation continues to make a quiet but compelling case for income investors who value free cash flow discipline over headline earnings optics. The business generates substantially more cash than its GAAP results suggest, the dividend is well-covered on any meaningful measure of cash generation, and the trajectory of modest, consistent payout increases reflects a management team that thinks carefully about sustainable capital return.

The stock’s recovery from its 52-week low has been impressive, and with the mean analyst target at $48.25 against a current price of $41.66, the upside case remains intact even at current levels. The combination of a Strong Buy consensus, a free cash flow yield that substantially exceeds the dividend requirement, and continued strategic investment in high-performance and sustainable materials positions Avient as a business building steadily toward a more compelling earnings profile. For patient, income-focused investors, the story here is one of quiet compounding rather than dramatic catalysts, and sometimes that is exactly what a well-constructed dividend portfolio needs.