Updated 2/25/26

Associated Banc-Corp (ASB), a regional bank headquartered in Wisconsin, operates over 200 branches across the Midwest and has steadily built a presence in commercial, retail, and wealth management services. Under the leadership of CEO Andrew Harmening, the company has leaned into strategic realignment, digital transformation, and a consistent dividend policy. ASB currently trades around $27.61, near the upper end of its 52-week range of $18.32 to $29.52, and offers a dividend yield of 3.41%. With earnings rebounding strongly to $2.77 per share and a payout ratio that has normalized to a comfortable 33.57%, the bank has moved past the one-time charges that clouded prior results. A seasoned executive team and improving fundamentals have the company in a more confident position heading into 2026.

Recent Events

Associated Banc-Corp has spent much of the past year executing on the balance sheet repositioning it telegraphed in prior periods. The strategic moves that generated one-time losses in 2024, including the sale of mortgage portfolio segments and investment securities, have largely been absorbed, and the bank is now benefiting from the cleaner asset mix that those transactions were designed to produce. Management has communicated that the repositioning phase is complete, and investor attention has shifted toward the pace of organic growth from here.

On the deposit and loan front, the bank has continued to see steady inflows, and its wealth management segment, which received additional focus following the arrival of Heath Sorenson to run Associated Trust Company in early 2025, has been expanding its contribution to fee-based revenue. That diversification away from pure net interest income has been a stated priority for the Harmening team, and the progress made over the past several quarters reflects that commitment.

Shares have climbed considerably off the lows seen in early 2025 and now trade near $27.61, approaching their 52-week high of $29.52. The recovery in the stock price tracks the improvement in reported earnings, with the trailing EPS of $2.77 representing a dramatic turnaround from the distorted figures that weighed on the valuation narrative a year ago. Short interest sits at roughly 6 million shares, a figure worth monitoring but not alarming given the overall float and the improving earnings trajectory.

💰 Key Dividend Metrics

📈 Forward Yield: 3.41%

📅 Last Dividend Payment: $0.24 per share (December 1, 2025)

💸 Annual Dividend Rate: $0.94

🔁 5-Year Average Yield: 4.08%

📊 Payout Ratio: 33.57%

💥 Dividend Growth (Recent): $0.23 → $0.24 per quarter

📉 Share Price vs Book: Price/Book of 0.94

✅ Earnings Coverage: EPS $2.77 vs Annual Dividend $0.94

Dividend Overview

The dividend picture at Associated Banc-Corp looks meaningfully healthier today than it did a year ago. The current yield of 3.41% sits below ASB’s own five-year average of approximately 4.08%, which is a reflection of how much the share price has recovered rather than any reduction in the payout itself. In fact, the dividend has continued to grow, with the quarterly payment stepping up from $0.23 to $0.24 in the fourth quarter of 2025, bringing the annualized rate to $0.94.

What changed most dramatically over the past year is earnings coverage. The payout ratio has dropped to 33.57%, a stark contrast to the unsustainable levels seen when one-time charges distorted reported earnings. With EPS now at $2.77, the dividend is covered more than twice over on a reported earnings basis, and operating cash flow of over $615 million provides additional support. This is the kind of coverage ratio that gives income investors confidence in the sustainability of future payments.

The stock trading at a slight discount to book value, with price-to-book at 0.94, means management still has an incentive to direct capital toward dividends and selective buybacks rather than acquisitions at a premium. For income-focused shareholders, that alignment tends to support continued dividend growth over time, even if the pace remains measured and deliberate rather than aggressive.

Dividend Growth and Safety

Associated Banc-Corp’s dividend history over the past two years reflects the bank’s characteristic approach: small, consistent increases tied to earnings progress rather than headline-grabbing jumps. The quarterly payment moved from $0.21 in early 2023 to $0.22 later that year, then to $0.23 in early 2024, and most recently to $0.24 in December 2025. That trajectory translates to annualized growth of roughly 7% over the two-year period, which is reasonable for a regional bank navigating a complex rate environment.

Dividend safety has improved substantially. The normalized payout ratio of 33.57% leaves ample room for further increases without straining the balance sheet, and operating cash flow of $615.7 million covers the total dividend obligation many times over. The bank is no longer in a position where investors need to wonder whether the next quarterly declaration might bring an uncomfortable surprise.

The beta of 0.79 means ASB shares tend to move with less volatility than the broader market, which is a trait that suits income investors well. Institutional ownership remains high, and that continued presence reinforces disciplined capital allocation. The combination of improving earnings, a conservative payout ratio, and steady cash generation suggests the dividend is on solid footing and that further incremental growth is achievable as long as credit quality holds and the rate environment remains reasonably supportive.

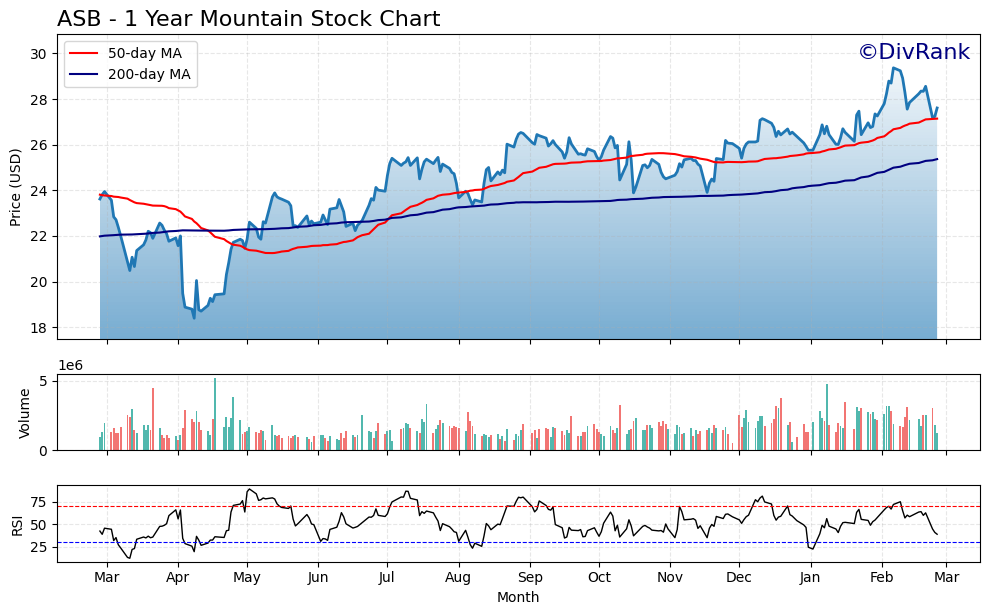

Chart Analysis

Associated Banc-Corp has had a strong recovery arc over the past twelve months, climbing from a 52-week low of $18.39 to its current price of $27.61, a gain of roughly 50% from the trough. That kind of base-to-present move reflects a meaningful shift in sentiment toward regional bank names broadly, and ASB has participated fully in that rotation. The stock reached a 52-week high of $29.37 earlier in the cycle, and at current levels it sits just under 6% below that peak, suggesting the bulk of the recovery rally is intact even as the shares have pulled back modestly from their highs.

The moving average picture is constructive for income investors watching entry points. ASB is trading above both its 50-day moving average of $27.14 and its 200-day moving average of $25.37, which confirms the intermediate and long-term trends are both pointed upward. More importantly, the 50-day has crossed above the 200-day, forming what technicians call a golden cross, a configuration that historically signals sustained upward momentum rather than a short-term bounce. The roughly $2.24 gap between the two moving averages gives the trend some structural cushion, meaning a modest pullback would not immediately threaten the longer-term trend line.

The RSI reading of 39.03 is the most interesting data point in this setup. That level places ASB close to technically oversold territory without having crossed the 30 threshold, which means the stock has shed some near-term heat without triggering panic selling. For a dividend investor, an RSI in the upper 30s on a stock sitting above both key moving averages is often an attractive combination, because it suggests consolidation rather than deterioration. Momentum has cooled from whatever drove the stock toward its annual high, but the underlying trend structure has not broken down.

For dividend-focused investors, the technical setup reads as cautiously favorable. The long-term trend is intact, the golden cross provides a bullish structural backdrop, and the softening RSI opens a window where patient buyers can accumulate without chasing a frothy momentum peak. The proximity to the 52-week high also means resistance is nearby, so investors adding here should expect some choppiness as the stock tests that $29 range again. Nothing in the chart suggests the dividend is under pressure from a price-action standpoint, and the recovery from the $18 low reinforces that the worst of the regional banking anxiety appears to be behind ASB for now.

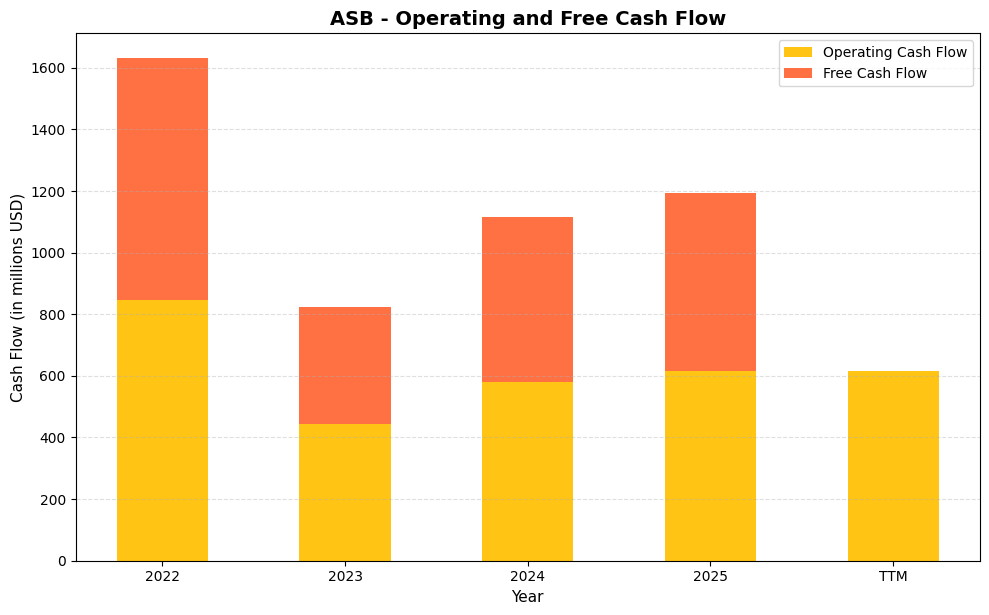

Cash Flow Statement

Associated Banc-Corp’s operating cash flow tells a story of recovery and stabilization following a sharp contraction in 2023. After generating $846.6 million in operating cash flow in 2022, that figure dropped significantly to $442.7 million in 2023, a decline that coincided with a challenging rate environment and elevated deposit competition across the regional banking sector. Since then, the trajectory has been constructive: operating cash flow rebounded to $580.2 million in 2024 and continued climbing to $615.7 million in 2025. Free cash flow has tracked closely alongside operating cash flow throughout this period, reaching $535.3 million in 2024 and $579.3 million in 2025, which signals that capital expenditure demands remain modest and disciplined. With the dividend currently consuming a manageable portion of that free cash flow generation, the payout appears well-supported at current levels.

The broader multi-year trend reveals a business that experienced meaningful cash flow volatility but has since demonstrated its ability to normalize. The 2022 peak of $783.9 million in free cash flow set a high bar, and while 2025’s $579.3 million figure still trails that mark, the consecutive annual improvements from 2023 onward reflect genuine operational progress rather than a one-time bounce. Capital efficiency has remained a quiet strength here, as the spread between operating and free cash flow has stayed narrow across all four years, indicating the bank is not consuming large amounts of cash to maintain or grow its asset base. For dividend investors, the combination of rising free cash flow, modest capital intensity, and a recovering earnings backdrop provides a reasonably firm foundation for both dividend maintenance and the potential for measured payout growth in the years ahead.

Analyst Ratings

Ten analysts currently cover Associated Banc-Corp, and the consensus price target range runs from a low of $29.00 to a high of $33.00, with a mean target of $30.20. With the stock trading at $27.61 as of late February 2026, the mean target implies upside of roughly 9% from current levels, which is a modest but meaningful premium for a stock that has already rallied significantly off its 2025 lows.

The absence of a formal consensus rating label reflects the somewhat divided views across the coverage universe, though the price target spread suggests a general belief that the stock still has room to appreciate. The floor of $29.00 sits above the current price, meaning even the most cautious analyst in the group sees some upside from here. That is a constructive setup, though investors should recognize that the easy part of the recovery trade, the move from deeply discounted to fairly valued, has likely already happened.

Analysts watching ASB are focused on whether the bank can continue growing net interest income in a rate environment that may shift over the course of 2026, and whether the wealth management buildout under Heath Sorenson’s leadership can contribute meaningfully to noninterest income. Progress on both fronts would likely support target price revisions toward the upper end of the current range.

Earning Report Summary

Associated Banc-Corp’s most recent full-year results represent a clean break from the distorted figures that dominated the prior reporting cycle. Total revenue came in at approximately $1.43 billion, and net income of $461 million translated to EPS of $2.77. Those numbers reflect the core earning power of the bank without the one-time restructuring charges that weighed so heavily on reported results in the prior period, and they provide a much cleaner baseline for evaluating the company’s ongoing earnings capacity.

Earnings Quality and Coverage

The profit margin of 33.12% is a meaningful improvement and reflects both the benefit of the repositioned balance sheet and better expense discipline across the franchise. Return on equity reaching 9.91% and return on assets at 1.08% are benchmarks that put Associated in line with well-regarded peers in the regional banking space. These are not exceptional figures, but they are respectable and suggest a business operating competently rather than one still working through fundamental challenges.

Operational Highlights

Operating cash flow of $615.7 million came in ahead of net income, a healthy sign for a bank of this scale. The wealth management segment continues to receive investment following the appointment of Heath Sorenson, and fee income diversification remains a medium-term priority for management. Credit quality metrics have remained manageable, and the bank has not indicated any material deterioration in loan performance. The combination of solid earnings, strong cash generation, and a normalized payout ratio leaves Associated in a position where capital allocation decisions, including continued dividend increases, can be made from a position of strength rather than constraint.

Management Team

Associated Banc-Corp is led by Andrew Harmening, who stepped into the CEO role in 2021. With a long background in retail and commercial banking, his approach has focused on modernizing the company’s operations while holding firm to its Midwestern roots. His prior leadership roles at larger institutions have helped bring a sharper focus on efficiency and customer experience, and the results of that approach are now more visible in the financial statements as the one-time noise from balance sheet repositioning has faded.

Supporting him is a team that brings a healthy balance of stability and experience. Derek Meyer serves as Chief Financial Officer and brings financial discipline to the table, especially important as the company manages capital allocation across dividends, loan growth, and potential share repurchases. The credit side is overseen by Patrick Ahern, while Angie DeWitt heads up human resources and has played a visible role in reshaping the company’s internal culture. Heath Sorenson, who joined in early 2025 to run Associated Trust Company, brings decades of wealth management experience to a segment the bank views as a key growth driver, and his integration into the leadership team has been a notable development over the past year.

Valuation and Stock Performance

As of late February 2026, ASB shares trade at $27.61, near the upper portion of their 52-week range of $18.32 to $29.52. The recovery from the lows of early 2025 has been substantial, driven by the normalization of reported earnings and the removal of balance sheet uncertainty that had weighed on investor confidence. The stock is no longer the deep-discount story it was a year ago, but it still offers a reasonable entry point for income-oriented investors.

The trailing price-to-earnings ratio of 9.97 is modest for a bank posting returns on equity near 10%, and the price-to-book ratio of 0.94 means shares are still trading at a slight discount to the company’s stated book value of $29.22 per share. That relationship has tightened considerably from the 0.72 price-to-book that characterized the stock during its trough, but a sub-1.0 multiple still suggests the market is not yet pricing in full credit for the bank’s asset base or its earnings recovery.

The dividend yield of 3.41% is lower than a year ago simply because the stock has moved higher, not because the payout has been reduced. For investors who initiated positions when the yield was near 4.8%, the total return picture looks attractive. For new buyers, the current yield combined with the prospect of continued incremental dividend growth and potential further appreciation toward analyst targets around $30.20 still makes a reasonable case for inclusion in an income-focused portfolio.

Risks and Considerations

The most significant shift in the risk profile over the past year is that earnings coverage of the dividend is no longer a concern at current levels. However, that improvement is tied to a normalization of earnings that followed a period of one-time charges, and sustaining EPS near $2.77 requires continued execution on both the loan growth and fee income fronts. Any deterioration in credit quality or a meaningful compression in net interest margins could pressure profitability and slow the pace of future dividend increases.

Interest rate dynamics remain a key variable for all regional banks, and Associated is no exception. If the Federal Reserve moves to cut rates more aggressively than currently anticipated in 2026, the spread income that drives net interest margin could compress, reducing the bank’s core earnings power. Conversely, a prolonged higher-for-longer rate environment creates its own risks around loan demand and credit performance. The bank’s balance sheet repositioning was partly designed to reduce this sensitivity, but it cannot be eliminated entirely.

The competitive landscape for regional banks has not become easier. Larger national institutions continue to invest heavily in digital capabilities, and fintech competitors remain active in deposit gathering and consumer lending. Associated’s community banking model and Midwest footprint provide some insulation, but the bank must continue investing in technology and service quality to retain and grow its customer base without allowing expenses to outpace revenue growth.

With short interest at roughly 6 million shares, there is a modest but present bearish position in the stock that could weigh on price action if sentiment shifts. The stock’s beta of 0.79 means it tends to be less volatile than the broader market, which is a feature for income investors, but it also means the shares may lag in a strong equity market environment where higher-beta names attract more capital.

Final Thoughts

Associated Banc-Corp has come a long way over the past twelve months. The stock has recovered strongly, earnings have normalized to a level that comfortably supports the dividend, and the payout ratio of 33.57% provides meaningful room for future increases. The quarterly dividend reaching $0.24 marks continued progress on a growth trajectory that began in 2023, and the underlying cash generation of the business supports the idea that this trend can continue.

The valuation is no longer the screaming discount it once was, but a price-to-book ratio just below 1.0 and a P/E under 10 still suggest the market is not fully pricing in the bank’s recovery or its longer-term earnings potential. For income investors, the combination of a 3.41% yield, a conservative payout ratio, and analyst price targets averaging $30.20 makes ASB a solid hold at current levels. New investors considering a position should weigh the reduced margin of safety relative to a year ago against the improved earnings quality and dividend sustainability that now characterize the story. How well management executes on wealth management growth and expense discipline will determine whether the stock can push toward and eventually through the top of the current analyst target range.