Updated 2/25/26

Ashland Inc. (ASH) continues to work through its strategic repositioning as a focused specialty chemicals company, with shares recovering meaningfully from their lows but still trading well below the peaks seen two years ago. At $62.22, the stock has climbed back toward the upper end of its 52-week range of $45.21 to $65.65, reflecting cautious optimism from investors as operational improvements take hold. The company carries a net loss on a trailing basis due to significant non-cash charges, but operating cash flow remains solidly positive at $243 million and free cash flow of $135 million continues to underpin the dividend comfortably. CEO Guillermo Novo’s focus on high-margin segments like personal care and life sciences remains the central narrative, and the dividend, now at $1.66 annually, has kept its slow and steady upward trajectory intact.

Recent Events

Ashland has remained active on the operational and strategic front heading into early 2026. The company has continued executing on its portfolio simplification strategy, exiting lower-margin product lines while doubling down on its core specialty additives and personal care segments. These moves have been well received by analysts who see the long-term margin profile improving even as near-term revenue reflects the pruning process. The specialty chemicals sector broadly has faced some headwinds from softer industrial demand in Europe and cautious destocking among pharmaceutical customers, both of which have touched Ashland’s volume picture.

On the balance sheet side, Ashland recorded a net loss of $670 million on a trailing twelve-month basis, a figure that is heavily influenced by impairment charges and restructuring costs rather than operational deterioration. Return on assets remains positive at 2.09%, and the company’s operating cash flow of $243 million demonstrates that the underlying business continues to generate real cash. Management has kept capital expenditures disciplined, allowing free cash flow of approximately $135 million to cover dividend obligations with room to spare. The market cap now sits at approximately $2.85 billion, a recovery from the sub-$2.4 billion levels seen in the prior report period.

Key Dividend Metrics

💵 Forward Yield: 2.57%

📆 5-Year Average Yield: 1.52%

📈 Dividend Growth: Modest upward trend continues

🔁 Payout Ratio: 40%

🏦 Free Cash Flow Coverage: Strong at $135M vs. ~$76M required

📊 Last Ex-Dividend Date: December 1, 2025

📍 Annual Dividend: $1.66 per share

🔍 Dividend Safety: Well-supported by operating cash flow

Dividend Overview

The current forward yield of 2.57% is lower than the 3.21% level cited in the prior report, and that shift tells an important story. The yield has compressed not because the dividend was cut, but because the stock has recovered from its lows. Shares near $62 reflect a better-valued business than the stock trading in the low $50s did, and income investors who entered at those depressed levels are now seeing both yield and capital appreciation working in their favor simultaneously.

The annual dividend of $1.66 represents the cumulative effect of Ashland’s steady, incremental increases over the past several years. The payout ratio remains at 40%, which is conservative and appropriate for a company still navigating a multiyear transformation. Management is not forcing growth in the dividend to attract income investors, and that restraint is actually a positive sign. It tells you the board is prioritizing long-term sustainability over short-term optics.

With free cash flow of $135 million and an estimated annual dividend obligation in the $76 million range based on current share count and payout, the coverage ratio is healthy. Even in a scenario where free cash flow steps down modestly due to higher capital spending or softer volumes, the dividend would not be at risk under normal operating conditions.

Dividend Growth and Safety

Looking at the recent dividend history, the pattern is clear and consistent. Payments moved from $0.385 per quarter in mid-2023 to $0.405 in mid-2024, and then again to $0.415 in mid-2025, bringing the annualized rate to $1.66. That’s a steady grind higher rather than a surge, and it aligns perfectly with Ashland’s overall management philosophy of prioritizing stability over flash.

The most recent increase, from $0.405 to $0.415, represents roughly a 2.5% raise. In the context of a company still absorbing restructuring charges and working to stabilize its top line, that kind of continued commitment to dividend growth is meaningful. Management is signaling confidence in the cash-generating ability of the core business even as the reported net income line is distorted by non-cash charges.

The safety of the dividend is grounded in operating cash flow of $243 million, which provides a much broader cushion than the free cash flow figure alone. Return on assets of 2.09% is modest but positive, confirming that the company’s asset base is still working productively. Short interest stands at approximately 3.9 million shares, a slight uptick from prior levels but still representing a relatively small bearish position relative to overall float. The payout ratio of 40% and the free cash flow coverage both argue convincingly that this dividend is on firm ground.

Chart Analysis

Ashland’s price action over the past year tells a story of meaningful recovery and emerging technical strength. The stock carved out a 52-week low of $45.45 before staging a sustained rally that has carried shares to $62.22, representing a gain of roughly 37% off that trough. That kind of base-to-peak move in a specialty chemicals name reflects a genuine shift in investor sentiment, and the proximity to the 52-week high of $64.80 suggests the bulls remain in control. Trading within 4% of a yearly peak is a constructive position for income investors who want to see price appreciation working alongside the dividend.

The moving average picture reinforces the bullish intermediate-term case. ASH is trading above both its 50-day moving average of $61.58 and its 200-day moving average of $53.67, and the 50-day has crossed above the 200-day to produce a golden cross formation. That configuration is one of the more reliable signals that a longer-term downtrend has been replaced by an uptrend, and the roughly $8 spread between the two averages indicates the cross is not a recent or fragile development. For dividend investors, a stock holding comfortably above both trend lines tends to offer a more stable total return environment compared to one where price is chopping around an overhead moving average.

The RSI reading of 42.85 introduces a nuance worth understanding in context. On a standalone basis, a reading in the low-to-mid 40s suggests the stock is drifting toward oversold territory rather than exhibiting the overheated momentum one might expect given the chart’s strong year-to-date performance. This likely reflects some consolidation and profit-taking near the 52-week high rather than a deterioration in the underlying trend. For patient dividend-focused buyers, a moderating RSI while the longer-term trend structure remains intact can actually represent a more favorable entry point than chasing a reading above 70.

Taken together, the technical setup for ASH is broadly supportive for income investors building or adding to a position. The golden cross, the distance traveled from the 52-week low, and the stock’s ability to hold above both key moving averages all point to a constructive trend. The cooling RSI and the modest gap below the 52-week high suggest the stock may need a brief digestion period before its next leg, but nothing in the current chart structure signals a breakdown is imminent. Investors collecting the dividend here appear to be doing so from a position of relative technical stability.

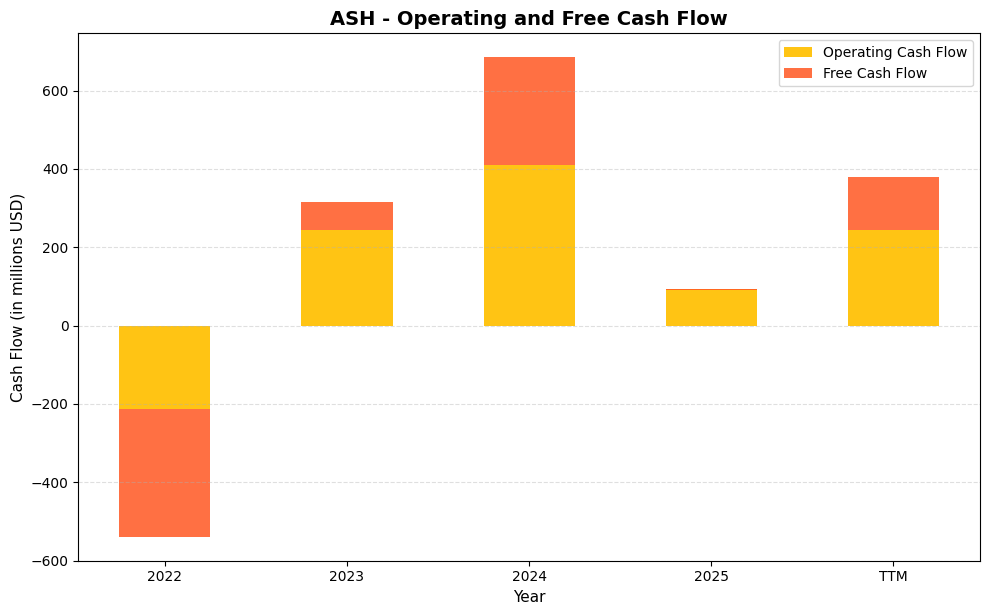

Cash Flow Statement

Ashland’s cash flow profile has improved meaningfully since the sharp deterioration in fiscal 2022, when operating cash flow came in at negative $213.0 million and free cash flow fell to negative $326.0 million. The recovery through fiscal 2023 and into fiscal 2024 was substantial, with operating cash flow climbing to $243.0 million and then $411.0 million respectively, while free cash flow reached $274.0 million in 2024. That trajectory gave dividend investors a credible foundation to assess payout sustainability. Fiscal 2025 represents a notable step back, with operating cash flow contracting to $94.0 million and free cash flow briefly dipping to negative $4.0 million, a figure that warrants attention even if TTM numbers have since recovered to $243.0 million in operating cash flow and $135.2 million in free cash flow. At the TTM free cash flow level, coverage of the current dividend remains intact, though the margin is not wide enough to be taken for granted.

Putting the full trend in context, the swing from deeply negative free cash flow in 2022 to a peak of $274.0 million in 2024 reflects the combination of restructuring efforts, portfolio streamlining, and improving working capital discipline that Ashland pursued over this period. The 2025 compression appears tied to elevated capital expenditures and transitional costs rather than a fundamental deterioration in the business, a distinction that matters when evaluating whether the dividend is structurally supported or at risk. Capital efficiency improved considerably through the 2023 to 2024 window, and the TTM recovery suggests the worst of the 2025 pressure may be fading. For shareholders focused on income, the key question is whether Ashland can sustain free cash flow consistently above its annual dividend obligation, and the current TTM reading of $135.2 million indicates the company is covering that requirement, though investors should monitor quarterly cash generation closely given the volatility this series has demonstrated.

Analyst Ratings

The analyst community holds a consensus buy rating on Ashland, with 10 analysts currently covering the stock. The mean price target of $68.00 implies upside of roughly 9% from the current price of $62.22, a more modest premium than was available when the stock traded in the low $50s. The range of targets runs from a low of $60.00 to a high of $73.00, indicating that even the most cautious analysts see limited downside from current levels while more optimistic voices believe the stock can push into the low $70s as the turnaround matures.

The tight clustering of price targets around the $60 to $73 range reflects a generally aligned view among analysts that Ashland is appropriately valued at current levels but has room to move higher as execution on the specialty chemicals strategy becomes more visible in the financial results. The low target of $60.00 sitting just below the current price is worth acknowledging as a reminder that the stock is no longer trading at a deep discount the way it was when it sat near $45. Investors entering at current prices are buying closer to fair value than at a dramatic discount, which means the margin of safety is narrower than it was in early 2025.

Earning Report Summary

Ashland’s most recent financial results present a picture that requires some unpacking. Revenue of approximately $1.81 billion on a trailing twelve-month basis reflects the ongoing effects of portfolio pruning and softer demand in select end markets, particularly pharmaceutical excipients where customer destocking has been a persistent headwind. The company’s deliberate exit from lower-margin product categories continues to suppress the top line even as it improves the underlying quality of revenue.

The net loss of $670 million is the most striking headline figure, and it demands context. A significant portion of that loss stems from goodwill impairment charges and restructuring-related write-downs rather than from the cash-generating operations of the business. The negative EPS of $14.53 similarly reflects these non-cash charges. Return on equity of negative 29.98% follows directly from those impairment hits to book value rather than from sustained operational underperformance. The profit margin of negative 38.34% is jarring at face value but again is dominated by charges that do not recur in cash form.

What tells the real operating story is the $243 million in operating cash flow and the $135 million in free cash flow. Personal care, life sciences, and specialty additives continue to be the segments driving that cash generation. Management has consistently pointed to adjusted EBITDA as the most representative profitability measure, and on that basis the business remains meaningfully positive. The direction of travel in free cash flow, up sharply from the prior year, is the most important number in the financial statements for dividend investors evaluating whether Ashland can sustain and grow its payout.

Management Team

Ashland continues to be led by Guillermo Novo, who has served as Chair and CEO since 2019. Novo’s background spanning Versum Materials, Air Products, and Dow Chemical has been central to shaping the company’s current strategy of concentrating on high-value specialty applications and exiting commodity-adjacent product lines. His consistent messaging around margin improvement and portfolio focus has given investors a clear framework for evaluating progress, even if the timeline has been longer and bumpier than originally hoped.

CFO Kevin Willis has been with the company since 2013 and continues to oversee financial strategy, capital allocation, and investor relations. Willis has been a steady hand through multiple phases of Ashland’s transformation, and his consistent emphasis on cash flow discipline has helped the company maintain its dividend through a period of significant earnings volatility. Chief Technology Officer Dr. Osama Musa leads the innovation pipeline, which remains important as Ashland competes on the basis of formulation expertise rather than commodity volume. Eileen Drury as Chief Human Resources Officer has supported the organizational changes that come with restructuring a specialty chemicals business of this scope. The segment leadership, including Jim Minicucci in Personal Care and Dago Caceres in Specialty Additives, reflects management’s focus on empowering the business units that are expected to drive the next phase of growth.

Valuation and Stock Performance

At $62.22, Ashland shares have recovered substantially from the $45 range that marked the low end of the past 52 weeks, and the stock now sits close to the upper end of that range at $65.65. The price-to-book ratio of 1.52, based on book value per share of $41.04, represents a modest premium to tangible assets, a meaningful shift from the prior report when the stock traded below book value at a price-to-book of 0.92. That change in valuation multiple reflects the market’s improving confidence in the business even as the earnings picture remains clouded by non-cash charges.

The P/E ratio is not applicable given the trailing net loss, so investors are appropriately relying on cash flow and book value metrics to anchor their valuation work. With a market cap of approximately $2.85 billion and free cash flow of $135 million, the price-to-free-cash-flow multiple is around 21 times, which is not cheap but is reasonable for a specialty chemicals business with improving margins and a clear strategic direction. The 2.57% yield remains above the S&P 500 average and is backed by a 40% payout ratio, making it an attractive income component within a diversified portfolio. Beta of 0.42 reflects Ashland’s historically low volatility relative to the broader market, a characteristic that income investors tend to appreciate.

Risks and Considerations

The net loss of $670 million and the negative profit margin of 38.34% are numbers that cannot be entirely dismissed even when their non-cash origins are understood. If impairment charges reflect genuine long-term deterioration in the value of certain business units rather than conservative accounting adjustments, the book value and earnings recovery thesis would face a more serious challenge. Investors need to monitor whether the assets being written down are truly stabilizing or whether further charges could follow in subsequent periods.

Revenue of $1.81 billion represents a business that has shrunk considerably from its prior scale, and the company’s ability to grow from this base is not guaranteed. Pharmaceutical end markets have been soft, and while personal care has shown resilience, specialty additives face competition from larger chemical companies with greater pricing power. If demand in key end markets does not recover as expected, top-line pressure could persist longer than the current consensus assumes.

Debt remains a consideration even as management has worked to reduce leverage. The combination of a debt load inherited from earlier acquisitions and a period of compressed earnings means that interest coverage deserves ongoing attention. While operating cash flow of $243 million provides meaningful debt service capacity, a deterioration in that figure due to volume weakness or margin pressure would tighten the financial picture more quickly than the headline balance sheet suggests. The low beta of 0.42 can also give investors a false sense of security in periods when sector-specific or company-specific risks materialize regardless of broader market conditions.

Final Thoughts

Ashland’s story in early 2026 is one of measured progress rather than dramatic resolution. The stock has recovered from its lows, the dividend has continued to grow incrementally, and free cash flow has improved in a way that gives the income thesis real credibility. The challenges have not disappeared, and the reported financial statements still carry the weight of non-cash charges that distort the profitability picture. But the operating engine of the business, as reflected in $243 million of operating cash flow, continues to run.

For dividend growth investors, Ashland offers a 2.57% yield backed by a conservative 40% payout ratio and improving free cash flow generation. The valuation at 1.52 times book is no longer the deep discount that existed a year ago, which means the easy money from price recovery has largely been made. What remains is a more nuanced thesis around whether Ashland’s specialty chemicals portfolio can deliver the margin expansion and revenue stabilization that management has been promising. The next several quarters will be the proving ground for that case.